|

市場調査レポート

商品コード

1644886

北米のセキュアアクセスサービスエッジ:市場シェア分析、産業動向、成長予測(2025~2030年)North America Secure Access Service Edge - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のセキュアアクセスサービスエッジ:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

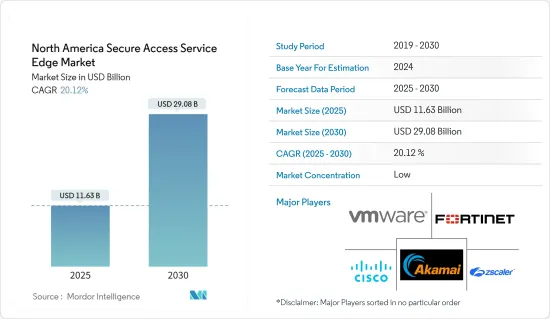

北米のセキュアアクセスサービスエッジ市場規模は、2025年に116億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは20.12%で、2030年には290億8,000万米ドルに達すると予測されます。

SASEの普及に伴い、SASEソリューションの導入、管理、サポートを行う有資格者の需要が増加しています。その結果、ベンダーや独立系団体が提供するトレーニングや認定プログラムの数が増加しています。これらの技術の効率的な導入と利用を可能にするため、ITチームはSASEの能力獲得に注力しています。

主要ハイライト

- SASEは、ネットワーク全体で統一されたセキュリティ基準と暗号化を実施することで、企業が厳格なコンプライアンス要件を達成するのに役立ちます。トランスミッション中やクラウドアプリケーションに保管されるデータを保護することで、規制違反や関連する罰金の可能性を最小限に抑えることができます。例えば、医療機関は、患者データを保護するための厳しい規制基準を遵守することが求められています。

- SASEの使用は、十分なセキュリティプロトコルや技術の不足によって強く奨励されています。SASEのような包括的で適応性の高いセキュリティソリューションは、脅威の拡大、リモートワーク問題、クラウド移行、コンプライアンス義務に対処する組織にとって、ますます必要になってきています。このような緊急のセキュリティ問題に対処するだけでなく、サイバーセキュリティの人材不足を解消し、現代の脅威や困難に直面しても、拡大性、事業継続性、回復力を保証します。

- データプライバシーと法規制の遵守が義務付けられていることは、SASEビジネスを拡大する強力な力となっています。企業は、厳格なデータ保護規則を遵守し、罰則を回避し、ブランドを保護するために、SASEのような完全なセキュリティソリューションの必要性を認識しています。コンプライアンスを保証するツールとしてのSASEの需要は、個人情報保護に関する法律が変化し続け、国際的に広まり、現代のサイバーセキュリティやデータ保護の取り組みに不可欠なものとなっているため、今後も拡大すると予想されます。

- クラウドベースのソリューションに対する需要は、技術の進歩と消費者のクラウド志向の高まりによって急増しています。技術によって、ユーザーは遠隔地からデータにアクセスできるようになりました。オンプレミスのインフラを維持するよりも、データをクラウドに移行した方がコストとリソースの面で効率的だという認識が企業の間で高まっていることが、クラウドベースのソリューションに対する需要を促進しています。

- COVID-19の流行は、デジタルトランスフォーメーションの取り組みが急速に進むにつれて、企業のSASE採用を加速させました。ネットワーキングの融合によってクラウドの導入が加速し続ける中、ますますリモートでモバイルになった従業員をより適切にサポートするためには、セキュリティが不可欠です。

- 2023年3月、ネットワーキングとセキュリティの融合を推進する世界のサイバーセキュリティ企業であるフォーティネットは、フォーティネットのシングルベンダーSASEソリューションであるFortiSASEに対する複数の機能強化を発表し、SaaS、プライベートアプリケーション、インターネットにわたるデジタルリソースのさらなる展開の柔軟性と新たなセキュアアクセス機能を実現しました。

北米のセキュアアクセスサービスエッジ市場の動向

ITと通信エンドユーザー産業が大きな市場シェアを占める見込み

- 北米、特に米国は、ITと電気通信セグメントの主要企業であることが多いです。この地域は堅調な通信産業、多数の技術企業、ITインフラへの多額の投資を誇っています。例えば、米国を拠点とするITインフラサービスのサプライヤーであるKyndrylは、2023年5月、フォーティネットが提供するマネージドセキュア・アクセスサービスエッジ(SASE)ソリューションを発表しました。このソリューションは、Kyndrylのネットワークとセキュリティサービスと、フォーティネットのクラウド型セキュリティとセキュアネットワーキングソリューションを組み合わせたもので、さまざまな業種の顧客向けにミッションクリティカルなネットワークの設計、構築、保守、アップグレードを行っています。このような取り組みにより、ITと電気通信のエンドユーザー部門でSASEソリューションが大幅に採用されるようになりました。

- さらに、Network-as-a-Service(NaaS)は、シームレスな通信、データ転送、クラウド接続に必要なネットワークインフラを提供するため、ITと電気通信組織にとって不可欠です。これらの組織は、堅牢でスケーラブルなネットワーキングソリューションに大きく依存しています。例えば、2023年7月、米国を拠点とする通信会社ルーメン・ Technologiesは、通信セクターを変革する計画の一環として、同社のNaaS(Network-as-a-Service)(NaaS)プラットフォームの主力機能を発表しました。ルーメンは、ネットワークサービスの購入、利用、管理において消費者に柔軟性を与えることで、従来の電気通信をクラウド化しようとしています。

- 全体として、SASE市場におけるIT・通信エンドユーザーの垂直成長は、このセグメント特有のサイバーセキュリティニーズ、セキュアなリモートアクセスの必要性、通信サービスの保護、デジタルトランスフォーメーションとクラウドの採用という広範な動向によって牽引されています。

- 5Gの画期的なレイテンシー、スループット、信頼性機能は、新しい産業、ビジネス、消費者向けサービスをサポートします。5Gは、世界のSASEベンダーがネットワークをより包括的に捉え、新たなセキュリティ脅威に対抗するためのベストプラクティスを開発することを促すと考えられます。Network as a Serviceソリューション・プロバイダーは、5Gの登場により、ネットワークのコスト効率を改善する有利な機会を得ると考えられます。通信産業では、ネットワークの自動化やその他の技術の統合が進み、5Gへの需要が高まっている

- GSMAによると、COVID-19パンデミックの影響を考慮して修正された予測では、北米での5G利用は短期的に減速すると予想されています。しかし、2023~2025年にかけて、5Gの利用はCOVID-19以前の予測と比べて1,300万接続増えると予想されています。

米国が大きな市場シェアを占める見込み

- 米国は先進経済国であり、先進技術の導入と受容、ネットワーク自動化の開発、クラウドベースのサービスの急増に大きく傾斜しており、セキュアアクセスサービスエッジ市場に貢献しています。さらに、エンドユーザー産業のデジタル化の進展と、Cisco Systems Inc.、Vmware Inc.、Palo Alto Networks、Versa Networks Inc.、Akamai Technologiesといった著名ベンダーの存在が、市場の成長に寄与しています。

- さらに、企業のデジタル変革の急速な加速に伴い、セキュリティのクラウド化が進んでいます。さらに、エンドユーザー産業におけるクラウドサービスの大幅な導入により、ネットワークインフラの安全性を確保し、複雑さを軽減してスピードと俊敏性を向上させる必要があります。このことは、今後数年間、市場ベンダーに大きな成長機会をもたらすと分析されています。

- 提供形態別では、NaaS(Network-as-a-Service)セグメントが米国で今後数年間に大幅な成長を遂げると分析されています。同市場は、様々な業種におけるクラウドソリューションの浸透、IoTやインダストリー4.0の登場、DDoSやデータ侵害の増加などにより、大きく成長すると予測されます。これらすべての要因が、米国におけるNaaS(Network-as-a-Service)の需要を促進すると予想されます。GSMAによると、北米では2025年までに、産業用モノのインターネット(IoT)と消費者の接続数が約54億に増加すると予想されています。

- さらに、同国には3つの主要クラウドサービスプロバイダーがあります。Amazon Web Services、MicrosoftのAzure、Google Cloudです。また、5G、自律走行、IoT、ブロックチェーン、人工知能、ゲームといった主要な技術革新の拠点とも考えられています。SASEの機能を統合することで、ゼロトラストセキュリティ機能を企業アーキテクチャに収束させることができ、これは信頼されたネットワークセキュリティ体制を実現する上で最も重要です。このように、SASEソリューションはエンドユーザーのネットワークとセキュリティアーキテクチャを変革し、サイバーリスク、コスト、複雑性を軽減すると分析されています。

- 市場のベンダーは、この機会を利用し、SASEソリューションを通じてサイバー耐性を強化する革新的なSASEソリューションを発表しています。例えば、2023年4月、AccentureとPalo Alto Networksは共同で、Palo Alto NetworksのAIを搭載したPrisma SASEによるセキュアアクセスサービスエッジ(SASE)ソリューションを記載しています。このソリューションにより、企業はサイバー耐性を向上させ、ビジネス変革への取り組みを加速できるようになります。

北米のセキュアアクセスサービスエッジ産業概要

北米のセキュアアクセスサービスエッジ市場は、Cisco Systems Inc.、VMware Inc.、Fortinet Inc.、Akamai Technologies Inc.、Zscaler Inc.などの大手企業が存在し、セグメント化されています。同市場の参入企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するため、提携や買収などの戦略を採用しています。

- 2024年4月、CloudCoverはSHI Internationalとパートナーシップを結び、先進的脅威防止サイバーセキュリティプラットフォームの世界展開を拡大。比類のないサプライチェーンを持つエンド・ツー・エンドのITソリューションの世界的リーダーであるSHIは、クラウドカバー独自のXDR/SASESaaS(Security-as-a-Service)プラットフォームをセキュリティポートフォリオの一部として提供しています。クラウドカバーは先進的サイバーリスク管理を提供し、マイクロ秒単位のリスク認識と制御を実現します。さらに、賠償責任保護を組み込んだ手法によるネットワーク内サイバーセキュリティ保険システムを確立しています。

- 2024年1月、技術インフラサービスプロバイダーのKyndrylは、Ciscoとの提携により、2つの先進的セキュリティサービスを導入しました。これらのサービスは、顧客のセキュリティ管理を強化し、サイバーインシデントへのプロアクティブな対応を可能にすることを目的としています。新しいサービスである「Kyndryl Consult Security Services Edge(SSE)with Cisco Secure Access」と「Kyndryl Managed SSE with Cisco Secure Access」は、サイバーセキュリティソリューションの大きな進化を意味します。

- 2023年8月、AI/MLを活用した統合セキュアアクセスサービスエッジ(SASE)の世界プロバイダーであるバーサネットワークスは、リアルタイムで悪意のある行動を特定する新しい組み込み型生成AI機能、セキュアな生成AIツール、ネットワークとセキュリティのオペレーショナルエクセレンスの強化を含むVersaAIの一連の機能強化を発表しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- マクロ経済要因が市場に与える影響の評価

第5章 市場力学

- 市場促進要因

- SD-WAN、FWaaS、SWG、CASB、ZTNA機能を組み合わせた単一のネットワークアーキテクチャに対するニーズの高まり

- セキュリティ手順とツールの欠如

- データ保護と規制法へのコンプライアンスの義務化

- 市場抑制要因

- クラウドリソース、クラウドセキュリティアーキテクチャ、SD-WAN戦略に関する知識の欠如

- 分散したデータへのアクセスとネットワークの管理・保護が困難

第6章 市場セグメンテーション

- 提供タイプ別

- NaaS(Network-as-a-Service)

- SaaS(Security-as-a-Service)

- 組織規模別

- 大企業

- 中小企業

- 産業別

- BFSI

- IT・通信

- 小売

- 医療

- 政府機関

- 製造業

- その他

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Cisco Systems Inc.

- VMware Inc.

- Fortinet Inc.

- Akamai Technologies Inc.

- Zscaler Inc.

- Cloudflare Inc.

- Versa Networks Inc.

- Broadcom Corporation

- Forcepoint

- Aryaka Networks Inc.

- McAfee Corp.

- Citrix Systems Inc.

- Barracuda Networks Inc

- Verizon Communications Inc.

- Juniper Networks Inc.

- Aruba Networks

第8章 投資分析

第9章 市場の将来展望

The North America Secure Access Service Edge Market size is estimated at USD 11.63 billion in 2025, and is expected to reach USD 29.08 billion by 2030, at a CAGR of 20.12% during the forecast period (2025-2030).

Demand for qualified individuals to implement, manage, and support SASE solutions increases as SASE adoption spreads. As a result, the number of training and certification programs provided by vendors and independent groups has increased. To enable the efficient deployment and use of these technologies, IT teams are concentrating on gaining competence in SASE.

Key Highlights

- SASE helps enterprises achieve strict compliance requirements by enforcing uniform security standards and encryption across the network. It minimizes the chances of regulatory infractions and related fines by safeguarding data during transmission and when kept in cloud applications. For instance, a healthcare institution is expected to abide by stringent regulatory standards for protecting patient data, including safeguarding data during information and idle state.

- The use of SASE is strongly encouraged by the shortage of sufficient security protocols and technologies. An all-encompassing and adaptable security solution like SASE is becoming increasingly necessary for organizations dealing with an expanding threat landscape, remote work issues, cloud migrations, and compliance obligations. In addition to addressing these urgent security issues, it closes the cybersecurity talent gap and guarantees scalability, business continuity, and resilience in the face of contemporary threats and difficulties.

- The mandatory observance of data privacy and regulatory legislation is a strong force behind expanding the SASE business. Businesses are realizing the necessity of a complete security solution like SASE to assist them in complying with strict data protection rules, avoiding penalties, and safeguarding their brand. The demand for SASE as a tool for assuring compliance is anticipated to grow as privacy legislation continues to change and spread internationally, making it an essential part of contemporary cybersecurity and data protection initiatives.

- The demand for cloud-based solutions surges due to the growing technological advances and consumer propensity toward the cloud. Technology allows the user to access data from remote locations. The increasing realization among companies about the cost and resource efficiency of shifting data to the cloud rather than maintaining on-premise infrastructure is driving the demand for cloud-based solutions among enterprises.

- The COVID-19 pandemic accelerated the enterprise's SASE adoption as digital transformation initiatives advanced rapidly. As cloud adoption continues to accelerate through the convergence of networking, security is critical to better support an increasingly remote and mobile workforce.

- In March 2023, Fortinet, the global cybersecurity firm driving the convergence of networking and security, announced several enhancements to FortiSASE, Fortinet's single-vendor SASE solution, enabling additional deployment flexibility and new secure access capabilities for digital resources across SaaS, private applications, and the internet.

North America Secure Access Service Edge Market Trends

IT and Telecom End-user Industry is Expected to Hold Significant Market Share

- North America, particularly the United States, is often a major player in the IT and telecom sectors. The region boasts a robust telecommunications industry, numerous technology companies, and significant investment in IT infrastructure. For instance, in May 2023, Kyndryl, a US-based supplier of IT infrastructure services, introduced a managed secure access service edge (SASE) solution powered by Fortinet that intends to assist clients in implementing advanced network security measures. The solution combines Kyndryl's network and security services with Fortinet's cloud-delivered security and secure networking solutions to design, construct, maintain, and upgrade mission-critical networking for clients across sectors. Such initiatives led to substantial adoption of SASE solutions in the IT and telecom end-user vertical.

- Moreover, network-as-a-service (NaaS) is essential for IT and telecom organizations because it provides the network infrastructure necessary for seamless communication, data transfer, and cloud connectivity. These organizations rely heavily on robust and scalable networking solutions. For instance, in July 2023, Lumen Technologies, a US-based telecom company, introduced its flagship feature on its network-as-a-service (NaaS) platform as a part of its plan to transform the telecom sector. Lumen is transforming traditional telecom into the cloud by giving consumers flexibility in purchasing, utilizing, and managing networking services.

- Overall, the IT and telecom end-user vertical growth in the SASE market is driven by the sector's specific cybersecurity needs, the imperative for secure remote access, the protection of telecommunications services, and the broader trends of digital transformation and cloud adoption.

- 5G's revolutionary latency, throughput, and reliability capabilities will support new industrial, business, and consumer services. It will encourage the global SASE vendors to embrace a more holistic view of the network and develop best practices to combat new security threats. Network as a service solution provider will get more lucrative opportunities to improve the network's cost efficiency with the advent of 5G. The rising integration of network automation and other technologies in the telecom industry is increasing the demand for 5G.

- According to GSMA, the forecasts revised for the impact of the COVID-19 pandemic expect a short-term slowdown in using 5G in North America. However, from 2023 to 2025, the 5G take-up is expected to account for 13 million more connections compared to the pre-COVID-19 forecast.

United States is Expected to Hold Significant Market Share

- The United States is a developed economy with a significant inclination toward implementing and accepting advanced technology, development in network automation, and surge in cloud-based services, thereby contributing to the secure access service edge market. Moreover, the growing digitization among end-user industries, coupled with the presence of prominent market vendors like Cisco Systems Inc., Vmware Inc., Palo Alto Networks, Versa Networks Inc., and Akamai Technologies, contribute to the market's growth.

- Further, security is moving to the cloud with the rapid acceleration of the digital transformation of businesses. Additionally, the significant adoption of cloud services in the end-user industries necessitates securing the network infrastructure and reducing complexity to improve speed and agility. This is analyzed to create substantial growth opportunities for market vendors in the coming years.

- By offering type, the network-as-a-service segment is analyzed to witness substantial growth in the United States over the coming years. The market is expected to grow significantly, owing to the greater penetration of cloud solutions across various industry verticals, the advent of IoT and Industry 4.0, and the growing number of DDoS and data breaches. All these factors are expected to drive the demand for network-as-a-service offerings in the United States. According to GSMA, in North America, by 2025, the number of industrial Internet of Things (IoT) and consumer connections is expected to increase to about 5.4 billion.

- Further, the country has three major cloud service providers: Amazon Web Services, Microsoft's Azure, and Google Cloud. It is also considered the hub for major technological innovations such as 5G, autonomous driving, IoT, blockchain, artificial intelligence, and gaming. Integrating SASE capabilities converges zero trust security capabilities into enterprise architectures, which is paramount in achieving a trusted network security posture. Thus, SASE solutions are analyzed to transform the end-user's network and security architecture to reduce cyber risk, costs, and complexity.

- Market vendors are capitalizing on the opportunity and launching innovative SASE solutions to enhance cyber resiliency through SASE solutions. For instance, in April 2023, Accenture and Palo Alto Networks collaborated to deliver joint secure access service edge (SASE) solutions powered by the Palo Alto Networks AI-powered Prisma SASE. The solution will enable organizations to improve cyber resilience and accelerate business transformation efforts.

North America Secure Access Service Edge Industry Overview

The North American secure access service edge market is fragmented with the presence of major players like Cisco Systems Inc., VMware Inc., Fortinet Inc., Akamai Technologies Inc., and Zscaler Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- April 2024: CloudCover formed a partnership with SHI International to extend the global reach of its advanced threat-prevention cybersecurity platform. SHI, a global leader in end-to-end IT solutions with an unparalleled supply chain, offers CloudCover's unique XDR/SASE security-as-a-service platform as part of its security portfolio. CloudCover delivers advanced cyber risk management, providing microsecond risk awareness and control. Additionally, it has established an in-network cybersecurity insurance system with methods that embed liability protection.

- January 2024: Kyndryl, a technology infrastructure services provider, introduced two advanced security services in partnership with Cisco. These services aim to enhance customers' security controls and enable proactive responses to cyber incidents. The new offerings, Kyndryl Consult Security Services Edge (SSE) with Cisco Secure Access and Kyndryl Managed SSE with Cisco Secure Access, represent a significant advancement in cybersecurity solutions.

- August 2023 - Versa Networks, the global provider in AI/ML powered Unified Secure Access Service Edge (SASE), announced a set of enhancements to VersaAI that includes new embedded generative AI capabilities to identify malicious behaviors in real-time, secure generative AI tools, and enhance network and security operational excellence.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Need For a Single Network Architecture that combines SD-WAN, FWaaS, SWG, CASB, and ZTNA Capabilities

- 5.1.2 Lack of Security Procedures and Tools

- 5.1.3 Mandatory Compliance with Data Protection and Regulatory Legislation

- 5.2 Market Restraints

- 5.2.1 Lack of Knowledge on Cloud Resources, Cloud Security Architecture, and SD-WAN strategy

- 5.2.2 Difficult in Accessing Such Dispersed Data While Managing And Safeguarding These Networks

6 MARKET SEGMENTATION

- 6.1 By Offering Type

- 6.1.1 Network-as-a-Service

- 6.1.2 Security-as-a-Service

- 6.2 By Organization Size

- 6.2.1 Large Enterprises

- 6.2.2 Small and Medium Enterprises

- 6.3 By EndUser Vertical

- 6.3.1 BFSI

- 6.3.2 IT and Telecom

- 6.3.3 Retail

- 6.3.4 Healthcare

- 6.3.5 Government

- 6.3.6 Manufacturing

- 6.3.7 Other End-user Industries

- 6.4 By Country

- 6.4.1 United States

- 6.4.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 VMware Inc.

- 7.1.3 Fortinet Inc.

- 7.1.4 Akamai Technologies Inc.

- 7.1.5 Zscaler Inc.

- 7.1.6 Cloudflare Inc.

- 7.1.7 Versa Networks Inc.

- 7.1.8 Broadcom Corporation

- 7.1.9 Forcepoint

- 7.1.10 Aryaka Networks Inc.

- 7.1.11 McAfee Corp.

- 7.1.12 Citrix Systems Inc.

- 7.1.13 Barracuda Networks Inc

- 7.1.14 Verizon Communications Inc.

- 7.1.15 Juniper Networks Inc.

- 7.1.16 Aruba Networks