|

市場調査レポート

商品コード

1913292

セキュア・アクセス・サービス・エッジ(SASE)市場の機会、成長促進要因、業界動向分析、予測(2026年~2035年)Secure Access Service Edge Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| セキュア・アクセス・サービス・エッジ(SASE)市場の機会、成長促進要因、業界動向分析、予測(2026年~2035年) |

|

出版日: 2025年12月26日

発行: Global Market Insights Inc.

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

概要

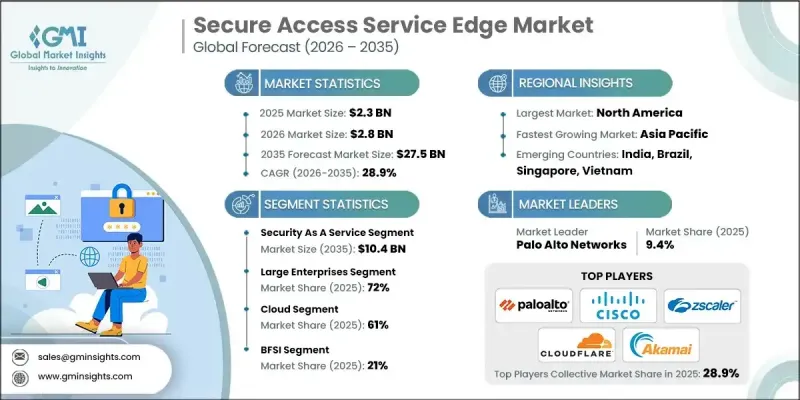

世界のセキュア・アクセス・サービス・エッジの市場規模は、2025年に23億米ドルと評価され、2035年までにCAGR28.9%で成長し、275億米ドルに達すると予測されています。

様々な業界の組織がクラウド提供型アプリケーションへの移行を加速しており、これにより企業ネットワークとセキュリティの設計方法が再定義されています。クラウドホスト型ソフトウェアへの依存度が高まる中、企業は従来の境界ベースの防御から離れ、統一された接続性とセキュリティを提供するクラウド中心のSASEアーキテクチャを採用しつつあります。企業は、場所を問わずユーザーとデバイスに対して一貫した保護と最適化されたパフォーマンスをますます必要としています。この需要が、運用上の柔軟性を維持しながら安全な世界のアクセスをサポートする、集中管理型のポリシー駆動型SASEプラットフォームの導入を推進しています。分散型ワークフォース、クラウド移行、スケーラブルなインフラストラクチャの必要性が、企業のセキュリティ戦略を再構築しています。組織は、進化するビジネスオペレーションと長期的なデジタルトランスフォーメーションの目標を支援するため、管理の簡素化、より強力なIDベースの制御、統合されたネットワークとセキュリティモデルの優先度を高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026年~2035年 |

| 開始時価値 | 23億米ドル |

| 予測金額 | 275億米ドル |

| CAGR | 28.9% |

断片化されたセキュリティツールの利用拡大により、運用上の複雑さとコストが増大し、組織はネットワークとセキュリティを統合プラットフォームへ統合する動きを加速させています。統合型SASEの導入により、企業はIT環境の近代化、ベンダーの乱立抑制、管理の効率化を実現できます。ゼロトラスト原則の普及に伴い、SASEフレームワーク内の統合された本人確認とアクセス制御は、不正な移動を制限し、認証情報に基づくリスクを低減するのに役立ちます。

セキュリティ・アズ・ア・サービスは、2025年に52%のシェアを占め、2035年までに104億米ドルに達すると予測されています。企業は従来のモデルに代わるクラウドネイティブセキュリティサービスへの依存度を高めており、保護を強化しながらハイブリッドおよびクラウドファーストの運用を支援しています。これらのサービスに組み込まれた高度な分析と自動化は、脅威の検出と対応の効率性を向上させます。

大企業セグメントは2025年に72%のシェアを占め、2035年までに183億米ドル規模に成長すると予測されています。これらの組織は、複雑な世界の運用、厳格なセキュリティ要件、2年を超える長期導入サイクルに対応するためSASEを採用しています。高可用性、拡張性、カスタマイズ可能なポリシー、強力なサービス保証が主要な導入要因であり続けています。

米国におけるセキュア・アクセス・サービス・エッジ市場は、2025年に7億5,340万米ドルに達しました。米国を拠点とする組織は、リモートワーク、クラウド拡張、高まるサイバーリスクを支援するため、国家的なゼロトラスト構想に沿いながらセキュリティフレームワークの近代化を急速に進めています。分散型チームのパフォーマンス、スケーラビリティ、ユーザーエクスペリエンスを向上させるクラウドネイティブプラットフォームへの需要は引き続き高まっています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 成長促進要因

- クラウドおよびSaaSの急速な普及

- リモートおよびハイブリッド勤務体制の拡大

- サイバーセキュリティ脅威の増加と攻撃の高度化

- セキュリティの複雑性とベンダーの乱立を削減する必要性

- ゼロトラストセキュリティフレームワークの加速

- 業界の潜在的リスク・課題

- レガシーインフラとの統合課題

- データプライバシーとベンダーロックインに関する懸念

- 市場機会

- 中小企業(SMB)および中堅市場セグメントへの拡大

- AIを活用した脅威検知に対する需要の拡大

- エッジコンピューティングアプリケーションの導入拡大

- マルチクラウドおよびハイブリッドクラウドの近代化イニシアチブ

- 成長可能性分析

- 規制情勢

- 北米

- 米国 - カリフォルニア州消費者プライバシー法

- カナダ - 個人情報保護及び電子文書法

- 欧州

- 英国 - データ保護法

- ドイツ - 連邦データ保護法

- フランス - デジタル共和国法

- イタリア - 個人データ保護法

- スペイン - データ保護及びデジタル権利に関する基本法

- アジア太平洋

- 中国 - 個人情報保護法

- 日本 - 個人情報の保護に関する法律

- インド - デジタル個人情報保護法

- ラテンアメリカ

- ブラジル - 一般データ保護法

- メキシコ - 民間事業者が保有する個人データの保護に関する連邦法

- アルゼンチン - 個人データ保護法

- 中東・アフリカ

- アラブ首長国連邦 - 個人データ保護法

- 南アフリカ - 個人情報保護法

- サウジアラビア - 個人データ保護法

- 北米

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- コスト内訳分析

- 開発コスト構造

- 研究開発費分析

- マーケティング及び販売費用

- 特許分析

- 事例研究

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- 将来の市場見通しと機会

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:提供別(2021年~2034年)

- ネットワーク・アズ・ア・サービス

- セキュリティ・アズ・ア・サービス

第6章 市場推計・予測:展開モデル別(2021年~2034年)

- クラウド

- オンプレミス

第7章 市場推計・予測:企業規模別(2021年~2034年)

- 大企業

- 中小企業

第8章 市場推計・予測:最終用途別(2022年~2035年)

- BFSI

- IT・通信

- 小売

- ヘルスケア

- 政府

- 製造業

- エネルギー・公益事業

- 教育

- その他

第9章 市場推計・予測:地域別(2022年~2035年)

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- ポルトガル

- クロアチア

- ベネルクス

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- タイ

- インドネシア

- ベトナム

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

第10章 企業プロファイル

- グローバル企業

- Cisco

- Palo Alto Networks

- Fortinet

- Zscaler

- Cloudflare

- Akamai

- Broadcom VMware

- Juniper Networks

- Aruba Networks HPE

- Verizon

- AT&T Cybersecurity

- Check Point Software Technologies

- IBM Security

- McAfee Enterprise Trellix

- BT Group British Telecom

- 地域企業

- SonicWall

- Forcepoint

- Barracuda Networks

- WatchGuard Technologies

- Sophos

- Sangfor Technologies

- Cyberoam

- SecPod

- T-Systems

- 新興/ディスラプター企業

- Netskope

- Cato Networks

- Versa Networks

- Aryaka

- Perimeter 81

- Tailscale

- Axis Security