|

市場調査レポート

商品コード

1683221

貯蔵穀物用殺虫剤:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Stored Grain Insecticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 貯蔵穀物用殺虫剤:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 109 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

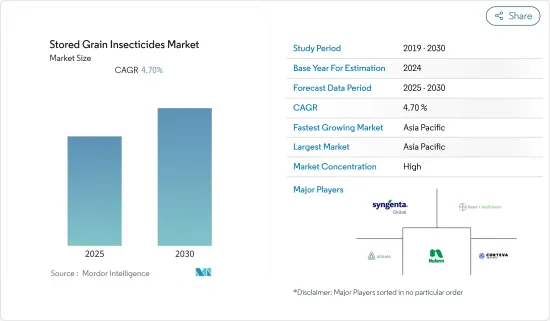

貯蔵穀物用殺虫剤市場は予測期間中にCAGR 4.7%を記録すると予測されます。

ポストハーベスト段階でのより良い価格を求める市場圧力の持続と、ポストハーベスト・ロスの削減への注目の高まりが、市場成長を促進する主な要因です。各国の多くの小規模農家では貯蔵施設が不足しているため、余剰穀物を貯蔵することができず、収穫後のロスが増加しています。加えて、各国政府は迫り来る食糧貯蔵危機への対応にますます注力するようになっており、ハイテク穀物貯蔵サイロの建設に向けた拠出が増加しています。このことは、昆虫用穀物保護剤の需要を増大させる可能性が高いです。世界中で蔓延しているパンデミックは、サプライ・チェーンの混乱による穀物の在庫と貯蔵の増加をもたらしています。貯蔵穀物を害虫の侵入から守るため、農家は貯蔵穀物用殺虫剤の需要を増加させる傾向にあります。したがって、ロジスティクス分野を除けば、COVID-19の影響が2021年第3四半期まで拡大すれば、市場はさらに世界中で成長すると見られています。

貯蔵穀物用殺虫剤の市場動向

貯蔵穀物害虫-一人当たり損失

害虫、ダニ、げっ歯類、鳥類の侵入により、年間約13億トンの食用穀物が廃棄されています。殺虫剤の使用は、サイロ、穀物箱、倉庫内の昆虫や害虫を駆除する非常に効果的な方法です。国連食糧農業機関(FAO)によると、ポストハーベスト農産物の平均生産損失は、先進国で年間約5%、先進国で年間約7%、発展途上国で年間約7%と推定されています。特にインドや中国などの新興経済国では、ポストハーベスト・ロスの削減に対する関心が高まっており、調査期間中に倉庫用殺虫剤の販売を強化できる好機と思われます。殺虫剤は貿易プロセスにおいて必須であり、検疫プロセスにおいても重要です。というのも、数少ない作物、特に園芸作物から有害物質を除去することは、輸出市場における農産物の品質を高めるために不可欠だからです。このような場合、殺虫剤による化学治療は、高い効率で機能する唯一の技術です。

アジア太平洋が市場を独占

FAOの報告によると、インドの温帯作物栽培地域では気温が上昇しているため、昆虫の活動が活発化しています。このため、米、トウモロコシ、小麦などの作物の栽培において、平均気温が1℃上昇するごとに約10~25%の全国的な損失が生じています。インドで穀物貯蔵に被害を与える最も一般的な昆虫は、イネゾウムシ、カプラ・ビートル、グレイン・ガ、レッサー・グレイン/フード・グレイン/パディ・ボーラーです。これらは、米、小麦、トウモロコシ、ジョワー、大麦、その他の穀物に至るまで、多くの貯蔵穀物に影響を及ぼしています。このような昆虫による貯蔵穀物への侵入が増加しているため、国内の貯蔵穀物用殺虫剤の市場はさらに拡大しています。しかし、IRRIの報告によると、インドにおける貯蔵穀物用殺虫剤の過剰使用や誤用は、コメやその他の穀物の自然な防除メカニズムを破壊しているため、FSSAIはこのような殺虫剤の使用に規制上の上限を設定しています。そのため、FSSAIはこのような殺虫剤の使用に規制の上限を設定しています。このことは、予測期間における市場の成長をある程度抑制することになると思われます。

貯蔵穀物用殺虫剤産業の概要

貯蔵穀物用殺虫剤市場は競争が激しく、さまざまな中小企業が世界で相応のシェアを占めています。そのため、非常に厳しい競合が発生しています。世界各地の大手企業による合併・買収活動が活発化していることも、市場が統合されている主な要因の一つです。北米とアジア太平洋の2地域は、競合の活動が最も活発な地域です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 製品タイプ別

- 有機リン酸塩

- ピレスロイド

- バイオ殺虫剤

- その他

- 用途別

- 農場内

- 農場外

- 輸出

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- アフリカ

- 南アフリカ

- その他のアフリカ

- 北米

第6章 競合情勢

- 最も採用された戦略

- 市場シェア分析

- 企業プロファイル

- Bayer CropScience AG

- Degesch America Inc.

- Syngenta AG

- Corteva AgriScience

- Nufarm Ltd

- Douglas Products

- Adama Agricultural Solutions Ltd.

- UPL Limited

第7章 市場機会と今後の動向

第8章 COVID-19の影響評価

The Stored Grain Insecticides Market is expected to register a CAGR of 4.7% during the forecast period.

Sustaining market pressure for better prices during the post-harvest stage and increasing focus on the reduction of post-harvest losses are the major factors driving the market growth. Lack of storage facilities in many small scale farms across various countries led to the inability to store surplus grains resulting in increased post harvest losses. Additionally, the respective governments are increasingly focusing toward keeping pace with its looming food storage crises and has increased the contribution toward the construction of high-tech grain storage silos. This is likely to augment the demand for insect grain protectants. The prevailing pandemic across the globe has resulted in increased stocking and storage of grains due to the disruption of supply chain. In order to protect the stored grains from pest infestation, farmers tend to demand the stored grains insecticide at an increasing level. Hence apart from logistics sector, the impact of COVID-19 if extended to the third quarter of 2021,the market is further observed to grow across the globe.

Stored Grain Insecticide Market Trends

Stored grain pest- per capita loss

Owing to the infestation of pests, mites, rodents, and birds, around 1,300 million metric ton of food grains are being wasted annually. The use of insecticides is a very effective method to control insects and pests in silos, grain bins, and warehouses. According to Food and Agricultural Organization (FAO), the average production loss of the post-harvest produce is estimated to be around 5% in the developed countries, 7% in industrialized countries, and around 7% in developing countries, annually. The increasing concerns toward reducing post-harvest losses, especially from the emerging economies, such as India and China, seems to be an opportunity, which can enhance the sales of warehouse insecticides during the study period. Insecticides are mandatory for trade processes and are important for the quarantine process, as elimination of toxic substances from few crops, especially horticulture crops, is essential to increase the quality of produce in the export market. In such cases, chemical treatment with insecticides is only the technique available, which works with high efficiency.

Asia Pacific Dominates the Market

According to a report by FAO, insect activity is on the rise because of the increasing temperature in the temperate crop-growing regions of India. This, in turn, is leading to the nationwide losses in the cultivation of crops, such as rice, corn, and wheat, by about 10-25% with per degree Celsius rise in mean surface temperature. The most common insects damaging grain storages in India are the rice weevil, the khapra beetle, the grain moth, and the lesser grain/ hooded-grain/ paddy borer. These affect a host of stored grains ranging from rice, wheat, maize, jowar, barley, and other grains. The increase in infestation of stored grains by such insects is further enhancing the market for stored grain insecticides in the country. However, according to reports by IRRI, the overuse and misuse of stored grain insecticides in India is disrupting the natural control mechanisms of rice and other grains, and hence, the FSSAI has set a maximum regulatory limit to the usage of such insecticides. This is going to deter the growth of the market to some extent in the said forecast period.

Stored Grain Insecticide Industry Overview

The storage grain insecticide market is highly competitive, with various small- and medium-sized companies coining reasonable shares in the world. This has resulted in a very stiff competition. The increasing merger and acquisition activities by the major players in different parts of the world is one of the major factors for the consolidated nature of the market. North America and the Asia-Pacific are the two regions showing maximum competitor activities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions and Market Definition

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Organophosphate

- 5.1.2 Pyrethroids

- 5.1.3 Bio-Insecticides

- 5.1.4 Others

- 5.2 By Application type

- 5.2.1 On Farm

- 5.2.2 Off Farm

- 5.2.3 Export shipments

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of South America

- 5.3.5 Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adapted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Bayer CropScience AG

- 6.3.2 Degesch America Inc.

- 6.3.3 Syngenta AG

- 6.3.4 Corteva AgriScience

- 6.3.5 Nufarm Ltd

- 6.3.6 Douglas Products

- 6.3.7 Adama Agricultural Solutions Ltd.

- 6.3.8 UPL Limited