|

市場調査レポート

商品コード

1850365

自律走行トラック:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Autonomous Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自律走行トラック:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

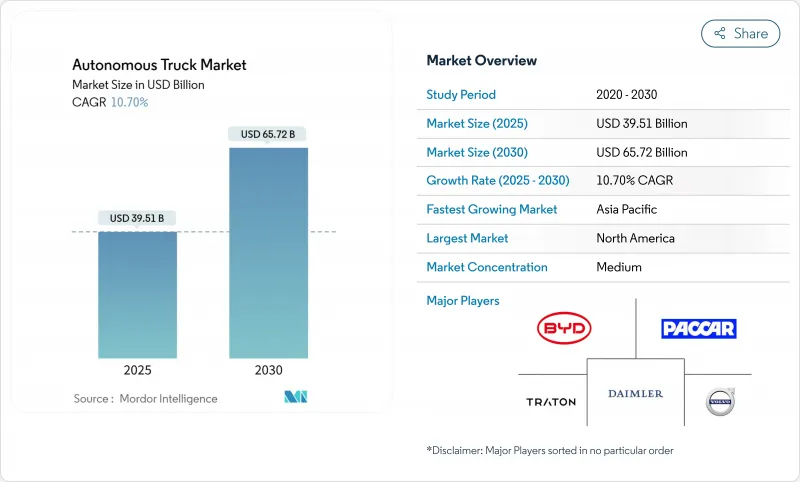

自律走行トラック市場規模は2025年に395億1,000万米ドルと推定・予測され、予測期間中(2025-2030年)のCAGRは10.70%で、2030年には657億2,000万米ドルに達すると予測されます。

ドライバー不足と人件費の高騰は、従来のフリートにとって大きな課題であり、資産利用率の高いヘビーデューティ・プラットフォームの採用を促進しています。緊急ブレーキ・システムなどの規制義務化とセンサー価格の下落が、近代化と商業パイロットを加速させています。レベル4トラックが長距離路線で信頼できることが証明されるにつれ、利害関係者は、より早い投資回収サイクル、トレーラーの回転率の向上、燃料と排出ガスの節約から利益を得て、自律走行トラック市場を拡大展開に向けて前進させています。

世界の自律走行トラック市場の動向と洞察

ドライバー不足と幹線輸送の人件費上昇

米国トラック協会(American Trucking Associations)は、2024年に8万人以上の大型ドライバーが未就職であると報告しており、ドライバーの退職が新規参入を上回るため、このギャップは拡大すると予想されています。休憩の義務化と時間外労働の割増は、総所有コストを膨れ上がらせ、500マイルを超えるルートでは24時間365日の自律走行が経済的に魅力的となります。テキサスの回廊沿いでレベル4のパイロットが成功し、トレーラーの回転数が倍増し、マイルあたりの人件費が35%以上削減されました。ロジスティクスメジャーは現在、自律的な幹線と人間によるラスト・マイル・ループで補完されたネットワークを再設計しています。

年中無休のハブ間物流への需要

eコマースのフルフィルメント窓口やジャスト・イン・タイムの製造は、24時間体制のキャパシティを求めています。州間高速道路の管理されたアクセスは、センサーの認識と冗長性の目標に適しており、フリートは予測可能なレーンに自律型クラス8トラクターを配車することができます。オーロラ社は2024年にダラスとヒューストン間の1,200マイルのドライバー・アウト・ランを完了し、ハブ・ツー・ハブ・モデルのアップタイムの約束を検証しました。小売業の荷送人は、結果として生じる待ち時間の短縮を在庫の縮小に結びつけ、専用の自律走行能力の長期契約を推進しています。

パッチワークのようなグローバル規制とクロスボーダー責任

カリフォルニア州のAB316は、人間のオペレーターが乗っていない10,000ポンド以上の自律走行トラックを制限しているが、これは米国の政策が断片的であることを浮き彫りにしています。ブリュッセルが2026年までに統一的な枠組みを作ろうと推進しているにもかかわらず、EU加盟国間でも同様の矛盾が見られます。こうした不一致は、個別の許可、保険特約、データ報告ワークフローを必要とし、規模の経済を希薄化させ、大陸全体の展開を先送りしています。

セグメント分析

大型トラクターは、2024年の自律走行トラック市場規模の64.5%を占め、人件費が燃料費をしのぐ最大の経費ラインである長距離レーンの自動化による経済的レバレッジを反映しています。フリートCFOモデルは、レベル4システムが95%の稼働率で500マイルのデューティサイクルをパスした場合の投資回収期間を4年未満としています。ミディアムデューティユニットは、地域の食料品や小包の輸送に重点を置き、より厳しい車両重量制限と増加する都市部へのアクセス制限のバランスをとっています。ライトデューティ自律走行バンは、eコマースの量に後押しされ、CAGR15.1%と最も速い成長を遂げます。

技術提携により大型車のリーダーシップが強化されます。ダイムラートラックは、自律走行が可能なフレートライナー・カスケーディア・トラクターのバッチをテキサス州での試験用にTorc Robotics社に出荷し、工場設置型の冗長アーキテクチャに対するOEMのコミットメントを示しました。一方、小型車メーカー各社は、材料費を削減するためにカメラのみの認識を利用し、自治体の規則が進化すれば、ラストマイルの自律走行に備えます。この乖離した軌道は、バーベル市場の分裂を示唆しています。

2024年の自律走行トラック市場シェアでは、SAE 1-2ドライバーアシストスイートが58.2%を占めるが、スポットライトはレベル4に移り、2030年までにCAGR 26.25%の成長が予測されます。2024年から2025年にかけて、ドライバーアウトパイロットの年率換算導入台数は140%増加し、資本流入はL4ロードマップを持つ企業に有利です。2025年に顧客への納入が予定されているボルボのVNL自律走行プラットフォームは、フルルート自律走行がプレミアムサービス契約を解除するというOEMの信念を示しています。レベル3は、規制がフォールバックの準備態勢を必要とする場合の橋渡し的ソリューションであることに変わりはないが、規制当局が一定の通路におけるドライバーの完全排除を温存するにつれて、その商業的窓口は狭まりつつあります。

投資家はこの移行を支持している:Waabiは、UberとNvidiaが主導するシリーズBラウンドで2億米ドルを確保し、AIファーストのシミュレーションに磨きをかけ、ロードテストの走行距離を80%削減しました。このような資金流入は、スケーラブルなバーチャルトレーニングがホモロゲーションを迅速化し、レベル4参入企業の収益までの時間を短縮するという信念を裏付けています。高精細マッピングのコストが低下するにつれて、市場アナリストは、レベル4が2030年までにアクティブな貨物輸送距離の30%シェアを突破し、資産スケジューリングの論理と保険引受規範を再構築すると予想しています。

自律走行トラック市場は、トラックタイプ(小型トラック、その他)、自動運転レベル(SAEレベル1-2(ドライバーアシスト)、その他)、ADAS機能(アダプティブクルーズコントロール、車線逸脱警告、その他)、コンポーネント(LIDAR、RADAR、カメラ、その他)、ドライブタイプ(ICエンジン、バッテリーエレクトリック、ハイブリッド、その他)、地域別に分類されています。市場予測は金額(米ドル)および数量(ユニット)で提供されます。

地域別分析

北米は、州レベルの試験的枠組みが容認されていることと、48,000マイルの州間高速道路システムが車線中心の自律性を支持していることから、2024年の自律走行トラック市場シェアの33.7%を獲得しました。テキサス州は、ダラス、ヒューストン、エルパソ、フェニックスを結ぶ商業路線を有し、オーロラ、コディアック、ボルボ、DHLが収益を生む積荷を運航しています。ベンチャー企業の資金調達は引き続き堅調で、2024年から2025年にかけて10億米ドルを超える資金を新興企業が調達したが、これは近い将来の収益化に対する投資家の自信を反映しています。

欧州は2024年の収益の約3分の1に貢献しました。ドイツ、スウェーデン、オランダは、UNECEのサイバーセキュリティと車線維持に関する指令の早期導入により、テストの先陣を切っています。ボルボとダイムラーのソフトウェアJVは、2026年のGSRの段階的導入に先立ち、EUのOEMメーカーに無線アップグレード可能なプラットフォームを提供します。国境を越えた貨物は、スカンジナビア-ハンブルグ間のようなデジタル・コリドー試験を通じて前進しているが、各国の認証スケジュールはまだまちまちで、大陸全体の規模を拡大する妨げとなっています。

アジア太平洋地域は依然としてCAGR21.4%で最も急成長している地域です。中国交通運輸省は全国的なスマートハイウェープロジェクトを承認し、2025年半ばまでに地元企業が2,000万kmの走行距離を達成することを可能にしました。日本は、2027年までに幹線道路をレベル4でカバーすることを目標に掲げ、自律走行インセンティブと水素・バッテリー充電デポへの支援を組み合わせています。韓国の「K-Mobility 2030」計画はテレマティクスの普及を加速させ、インドは先発組のニッチ分野として自律的な鉱業と港湾運送に注目しています。Autowareのようなオープンソースのスタックは、地域のインテグレーターに、左ハンドルの都市グリッド向けに認識をカスタマイズする足がかりを与えます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ドライバー不足と長距離輸送の労働コストの上昇

- 24時間365日対応のハブツーハブ物流の需要

- 安全規制の強化(例:米国のAV法案、EU GSR)

- プラトゥーニングによる燃料節約と排出ガス規制

- 自律性とゼロエミッションパワートレインの相乗効果

- オープンソースの自律スタックが参入障壁を下げる

- 市場抑制要因

- 不完全な国際規制と国境を越えた責任

- サイバーセキュリティとOTAアップデートのリスク

- LiDAR/センサースイートの高コスト

- ティア1回廊を超える高解像度HDマップの不足

- バリューチェーン/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額(米ドル)と数量(単位))

- トラックの種類別

- 小型トラック

- 中型トラック

- 大型トラック

- 自律性のレベル別

- SAEレベル1-2(運転支援)

- SAEレベル3(条件付き)

- SAEレベル4(高)

- SAEレベル5(フル)

- ADAS機能別

- アダプティブクルーズコントロール

- 車線逸脱警報

- 渋滞アシスト

- ハイウェイパイロット

- 自動緊急ブレーキ

- 死角検知

- 車線維持支援

- コンポーネント別

- ライダー

- レーダー

- カメラ

- 超音波およびその他のセンサー

- AIコンピューティングモジュール

- ドライブタイプ別

- 内燃機関

- バッテリー電気

- ハイブリッド

- 水素燃料電池

- 地域別

- 北米

- 米国

- カナダ

- その他北米地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- トルコ

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- AB Volvo

- Daimler Truck AG

- Traton SE

- PACCAR Inc.

- BYD Co. Ltd.

- Tesla, Inc.

- TuSimple

- Aurora Innovation

- Waymo Via

- Plus.ai

- Torc Robotics

- Kodiak Robotics

- Nikola Corp.

- Einride

- Embark Technology

- Hyzon Motors

- Gatik AI

- Volvo-Uber ATG JV

- Scania

- Navistar