|

市場調査レポート

商品コード

1683114

北米のレディトゥドリンクコーヒー市場:市場シェア分析、産業動向、成長予測(2025~2030年)North America Ready to Drink Coffee - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のレディトゥドリンクコーヒー市場:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 222 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

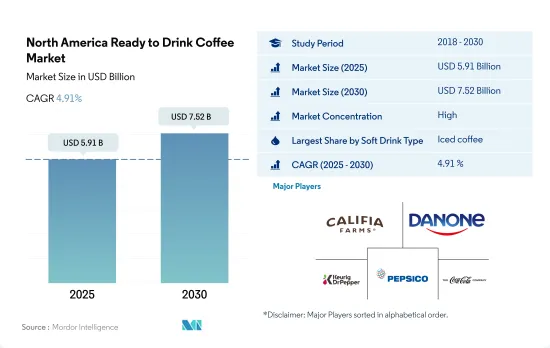

北米のレディトゥドリンクコーヒー市場規模は2025年に59億1,000万米ドルと推定され、2030年には75億2,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは4.91%で成長する見込みです。

より健康的で機能的なRTDコーヒー飲料の革新が成長を牽引

- 北米では、アイスコーヒー、コールドブリュー、コーヒーベースのエナジードリンクなどの製品を含むRTD(レディトゥドリンク)コーヒーの人気が急上昇しています。これらの製品の利便性と携帯性が、時間に追われる消費者の心を打りました。Z世代の消費者は、ホットコーヒーよりもRTDコーヒーに惹かれています。これを受けて、各ブランドはRTDコーヒーの品揃えを強化しています。この動向は、2022年現在、米国人口の約20.88%、カナダ人の22%、メキシコ人の27%がZ世代に該当するという事実によってさらに拍車がかかっています。さらに、より健康的で機能的なRTDコーヒーへのシフトも顕著です。2023年には、北米の消費者の約35%が低糖質のRTDコーヒーを好むと回答しました。メーカー各社はこれに注目し、低糖、乳製品不使用、植物由来の代替品を導入して、この需要の高まりに対応しています。

- 2018~2023年にかけて、北米のアイスコーヒー市場の年間平均成長率(CAGR)は4.59%でした。冷たい飲料は北米の消費者の大多数にとって好ましい選択肢です。アイスコーヒーは便利であると思われがちだが、さまざまなフレーバーや剤形があり、甘味が加えられていることも多いです。この人気は、今後数年間の市場成長の原動力になると予想されます。

- コールドブリューコーヒーは、2024~2030年のCAGR値が6.24%と予測されており、成長という点ではトップランナーになると考えられます。コールドブリューコーヒーは、酸味が少なくカフェインが豊富なことで知られ、砂糖や添加物を加えない自然な甘みがあります。ニトロ・コールド・ブリューのように炭酸を含むものもあります。このため、RTDコールドブリューコーヒーは、炭酸飲料や発泡性飲料以外のさわやかな冷たい飲料を求める人々にとって魅力的な選択肢となっています。

便利な飲料への需要が高まっているため、メキシコが今後の市場のフロントランナーになると予想されます。

- 北米のレディトゥドリンク(RTD)コーヒー市場は堅調な伸びを示し、2021~2023年にかけて売上額は9.43%急増しました。この成長は、RTDコーヒー製品に対する消費者需要の高まりが、メーカーに新しく革新的な製品の投入を促していることに起因しています。特に、2022~2023年にかけて、スターバックス、ダンキン、カリフィア・ファームズ、ラ・コロンブなどの有名ブランドが、消費者を魅了する様々なRTDコーヒーオプションを発表しました。

- 米国は北米のRTDコーヒー市場を独占しており、その大きなコーヒー消費量に支えられています。同国のコーヒー消費量は14億ポンドで、世界のコーヒー消費量の約20%を占めます。さらに、米国はコーヒー豆の主要輸入国であり、2021年の輸入量は30億ポンドを超えます。機能性成分入り飲料の導入はコーヒー消費をさらに促進しています。これらの製品は、従来カフェインと関連付けられてきた集中力や生産性を高めるだけでなく、その他の健康面にも対応しているからです。

- 北米以外ではメキシコが最も急成長しており、2024~2030年のCAGRは金額ベースで6.03%と予想されます。都市化の進展と中間所得層の拡大が、同国のRTD茶市場を牽引しています。メキシコでも都市化が進んでおり、便利で持ち運びに便利な飲食品に対する需要が高まっています。世界銀行の報告によると、メキシコの都市化率は前年82.6%で、世界平均の都市化率56.6%を大きく上回っており、2023年時点で人口の82.6%が都市部に居住しています。

北米のレディトゥドリンクコーヒー市場動向

消費者は多忙なライフスタイルに合わせて便利で持ち運びしやすい飲料を求める傾向が強まり、同セグメントの売上を牽引しています。

- RTDコーヒーの消費は特に18~39歳が多いです。2022年には、アメリカ人労働者の平均が週に14.15米ドル以上を消費する傾向にあることが観察されました。

- 北米地域では、Z世代とミレニアル世代の消費者が、他の年齢層の中で最も高いブランドロイヤルティを公言しています。米国の消費者の73%が、特定の小売店、ブランド、店舗に「忠実」であると考えています。

- インフレはコーヒー生豆価格や輸送費など、コーヒービジネスのあらゆる側面に影響を及ぼしています。パンデミックに関連したサプライチェーンの課題は、インフレとコーヒー卸売価格の上昇に寄与しています。しかし、市場は堅調に推移しており、価格は経済的な水準に維持されています。

- 米国では、業務用ブランドから職人やグルメ志向のものまで、多種多様なRTDコーヒーが販売されており、消費者は様々なフレーバーから選ぶことができます。RTDコーヒーは米国市場において、特にホットコーヒーの代用品として重要な位置を占めています。

北米のレディトゥドリンクコーヒー産業概要

北米のレディトゥドリンクコーヒー市場はかなり統合されており、上位5社で92.71%を占めています。この市場の主要企業は、Califia Farms, LLC、Danone S.A.、Keurig Dr Pepper, Inc.、PepsiCo, Inc.、The Coca-Cola Companyがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 消費者の購買行動

- イノベーション

- ブランドシェア分析

- 規制の枠組み

第5章 市場セグメンテーション

- ソフトドリンクタイプ

- コールドブリューコーヒー

- アイスコーヒー

- その他のRTDコーヒー

- 包装タイプ

- アセプティック包装

- ガラス瓶

- 金属缶

- ペットボトル

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンラインショップ

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他

- オントレード

- オフトレード

- 国名

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- BRC Inc.

- Califia Farms, LLC

- Chamberlain Coffee Inc.

- Costco Wholesale Corporation

- Danone S.A.

- Keurig Dr Pepper, Inc.

- La Colombe Holdings, Inc.

- Luigi Lavazza S.p.A.

- Nestle S.A.

- PepsiCo, Inc.

- The Central America Bottling Corporation

- The Coca-Cola Company

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The North America Ready to Drink Coffee Market size is estimated at 5.91 billion USD in 2025, and is expected to reach 7.52 billion USD by 2030, growing at a CAGR of 4.91% during the forecast period (2025-2030).

Innovations in RTD coffee drinks with healthier and functional drinks driving growth

- North America witnessed a surge in the popularity of ready-to-drink (RTD) coffee, encompassing products such as iced coffee, cold brew, and coffee-based energy drinks. The convenience and portability of these offerings have struck a chord with time-pressed consumers. Gen Z consumers are gravitating toward RTD coffee over its hot counterpart. In response, brands are ramping up their RTD coffee portfolios. This trend is further fueled by the fact that, as of 2022, approximately 20.88% of the US population, 22% of Canadians, and 27% of Mexicans fall into the Gen Z age bracket. Moreover, there is a discernible shift toward healthier and more functional RTD coffee options. In 2023, about 35% of North American consumers expressed a preference for low-sugar RTD coffees. Manufacturers are taking note and introducing low-sugar, dairy-free, and plant-based alternatives to cater to this growing demand.

- From 2018 to 2023, the value of the iced coffee market in North America witnessed a compound annual growth rate (CAGR) of 4.59%. Cold beverages are the preferred choice for a majority of North American consumers. Iced coffee, often seen as convenient, is available in a range of flavors and formulations, often with added sweetness. This popularity is expected to drive the market's growth in the coming years.

- Cold brew coffee is poised to be the frontrunner in terms of growth, with a projected CAGR value of 6.24% from 2024 to 2030. Cold brew, known for its lower acidity and ample caffeine content, has a natural sweetness without any added sugars or additives. Some variants even offer carbonation, such as nitro cold brew. This makes RTD cold brew coffee an enticing option for those seeking a refreshing, cold beverage other than soda or fizzy drinks.

Due to the increasing demand for convenient beverages, Mexico is expected to be the future front-runner in the market studied

- The North American ready-to-drink (RTD) coffee market witnessed robust growth, with sales surging by 9.43% in value from 2021 to 2023. This growth can be attributed to the rising consumer demand for RTD coffee products, prompting manufacturers to introduce new and innovative offerings. Notably, in 2022-2023, renowned brands such as Starbucks, Dunkin', Califia Farms, and La Colombe unveiled a range of RTD coffee options to captivate consumers.

- The United States dominates the North American RTD coffee market, bolstered by its significant coffee consumption. The country's coffee consumption stands at 1.4 billion pounds, accounting for roughly 20% of global coffee consumption. Additionally, the United States is a major coffee bean importer, with imports exceeding 3 billion pounds in 2021. The introduction of functional ingredient-infused beverages further fuels coffee consumption, as these offerings not only enhance focus and productivity, traditionally associated with caffeine, but also cater to other health aspects.

- Mexico is observed to be the fastest-growing country, apart from the Rest of North America, with an expected CAGR of 6.03% by value from 2024 to 2030. Growing urbanization and expansion in the middle-class community are driving the market for RTD tea in the country. Mexico is also becoming increasingly urbanized, leading to a higher demand for convenient and portable food and beverage options. As per World Bank reports, the urbanization rate in Mexico was 82.6% the previous year, which was way above the average global rate of urbanization, 56.6%, with 82.6% of the population residing in urban areas as of 2023.

North America Ready to Drink Coffee Market Trends

Consumers are increasingly seeking convenient and portable beverage options to fit their busy lifestyles, thereby driving segment sales

- RTD coffee consumption is particularly high the age group of 18 to 39-year consumers. It was observed that in 2022, an average of american worker has a tendency to spent over USD 14.15 per week.

- n the North American region, Gen Z and Millennial consumers professed the highest brand loyalty among other age groups. 73% of United States consumers consider themselves "loyal" to certain retailers, brands, and stores.

- Inflation has affected every aspect of coffee businesses, including green coffee prices and transportation costs. Pandemic-related supply chain challenges have contributed to inflation and increased wholesale coffee prices. However, the market stood steady with players maintaining the prices to an economical level.

- In the US, there is a wide variety of RTD coffee available, ranging from commercial brands to artisan and gourmet options, allowing consumers to choose from a variety of flavors. It is important to note that RTD coffee has a significant place in the United States market, particularly as a substitute for hot coffee.

North America Ready to Drink Coffee Industry Overview

The North America Ready to Drink Coffee Market is fairly consolidated, with the top five companies occupying 92.71%. The major players in this market are Califia Farms, LLC, Danone S.A., Keurig Dr Pepper, Inc., PepsiCo, Inc. and The Coca-Cola Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumer Buying Behaviour

- 4.2 Innovations

- 4.3 Brand Share Analysis

- 4.4 Regulatory Framework

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Soft Drink Type

- 5.1.1 Cold Brew Coffee

- 5.1.2 Iced coffee

- 5.1.3 Other RTD Coffee

- 5.2 Packaging Type

- 5.2.1 Aseptic packages

- 5.2.2 Glass Bottles

- 5.2.3 Metal Can

- 5.2.4 PET Bottles

- 5.3 Distribution Channel

- 5.3.1 Off-trade

- 5.3.1.1 Convenience Stores

- 5.3.1.2 Online Retail

- 5.3.1.3 Specialty Stores

- 5.3.1.4 Supermarket/Hypermarket

- 5.3.1.5 Others

- 5.3.2 On-trade

- 5.3.1 Off-trade

- 5.4 Country

- 5.4.1 Canada

- 5.4.2 Mexico

- 5.4.3 United States

- 5.4.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BRC Inc.

- 6.4.2 Califia Farms, LLC

- 6.4.3 Chamberlain Coffee Inc.

- 6.4.4 Costco Wholesale Corporation

- 6.4.5 Danone S.A.

- 6.4.6 Keurig Dr Pepper, Inc.

- 6.4.7 La Colombe Holdings, Inc.

- 6.4.8 Luigi Lavazza S.p.A.

- 6.4.9 Nestle S.A.

- 6.4.10 PepsiCo, Inc.

- 6.4.11 The Central America Bottling Corporation

- 6.4.12 The Coca-Cola Company

7 KEY STRATEGIC QUESTIONS FOR SOFT DRINK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms