|

市場調査レポート

商品コード

1645098

欧州の内燃エンジン市場:シェア分析、産業動向・統計、成長予測(2025~2030年)Europe Internal Combustion Engines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の内燃エンジン市場:シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

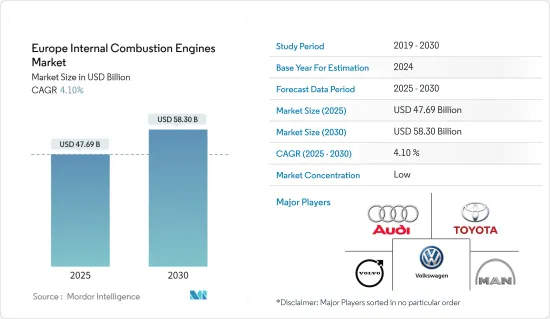

欧州の内燃エンジン市場規模は2025年に476億9,000万米ドルと予測され、予測期間(2025~2030年)のCAGRは4.1%で、2030年には583億米ドルに達すると予測されます。

主要ハイライト

- 中期的には、ICE二輪車需要の増加とプラグインハイブリッド内燃車(PHEV)の台頭が、予測期間中の欧州の内燃エンジン車市場の成長を牽引すると予測されます。

- 一方、バッテリー電気自動車市場の台頭と、グリーン気候目標に関するクリーン燃料の採用需要は、予測期間中の欧州の内燃エンジン市場の成長を妨げると予想されます。

- 技術革新とプラグインハイブリッド車における最新技術の適応は、予測期間中、欧州の内燃エンジン市場に機会を創出すると考えられます。

- ドイツが市場を独占しており、予測期間中に最も高い成長率を記録する可能性も高いです。

欧州の内燃エンジン市場の動向

ディーゼルが市場で大きなシェアを占める

ディーゼルエンジンは、1870年代から使用されている最も重要な内燃エンジンの一つです。これらのエンジンは、空気とディーゼルの混合気の燃焼後に機械エネルギーを発生するように設計されています。空気とディーゼルの混合気を点火するためにスパークプラグのような補助部品は使わず、エンジンブロック内で動くピストンによって圧縮される空気の温度上昇を利用します。

ディーゼルICEエンジンは燃費がよく、ガソリンエンジンよりも加速性、牽引力、運搬力に優れています。そのため、ディーゼルエンジンは欧州ではかなり身近で人気のある燃料源となっています。

ディーゼルは、欧州連合(EU)がよりクリーンなエネルギー源を採用する取り組みを行っているにもかかわらず、欧州では重要な輸送用燃料となっています。2023年には、欧州の新規登録車の13.6%がディーゼル内燃エンジンを搭載しており、欧州の強力な顧客基盤を占めています。

ディーゼル内燃エンジン車市場のかなりのシェアは、バス(商用と自家用)、公用車、トラック、バンに見られます。欧州自動車工業会(ACEA)によると、2023年においても、ディーゼルエンジン搭載バスはEUで最も人気があり、バスの新車販売台数の62.3%を占めています。

2023年には、ディーゼルエンジンを搭載したICEエンジンも、欧州のトラック部門で重要かつ強力な基盤を築いた。ACEAによると、EUで新規登録されたトラックの95.7%はディーゼルエンジンで、1.5%は電気自動車でした。さらに、欧州ではトラックの生産台数が増加しました。2023年、欧州では60万3,437台のトラックが生産され、商用車の総生産台数は前年比で約20.3%増加しました。

2023年10月、世界最大のエクスプレス輸送会社であるFedEx Corp.の子会社FedEx Express Europeは、英国で自社所有のトラック5台の燃料として水素化処理植物油(HVO)再生可能ディーゼルの検査運用を開始すると発表しました。これにより、ディーゼルエンジン市場の参入企業は、再生可能ディーゼルに適応するために製品の変更を行い、安全な将来の展望を提供することになります。

したがって、このようなシナリオは、今後数年間でディーゼルエンジンの大きなシェアを持つ可能性が高いです。

ドイツが市場を独占する可能性が高い

近年、ドイツでは、バス、自動車、二輪車、トラックなど、すべての商用車と自家用車において、化石燃料から電気自動車への大きな移行が見られます。しかし、こうした新興国市場の開拓は、PHEVセグメントの技術進歩により市場に悪影響を与えていないです。

PHEVまたはプラグインハイブリッド電気自動車は、ディーゼルエンジンまたはガソリンエンジンと、EV充電ステーションで充電可能な大容量バッテリーパックと電気モーターを組み合わせたハイブリッドEVの一種です。従来のPHEVは、電気モーターとバッテリーパックを搭載しているが、すべての動力をガソリンまたはディーゼルから得ています。

ドイツでは、ガソリンとディーゼルを動力源とする内燃エンジン車が増加しており、化石燃料と非化石燃料の両方が使用されています。

PHEVを別にしても、ドイツではかなりの数のディーゼル車とガソリン内燃車が共有されています。ドイツKBA連邦交通局によると、2023年のドイツの新車販売台数は、2022年の販売台数データと比較して7.3%増加し、ガソリン車の販売台数が13.3%増の97万9,000台と最も大きく伸び、ガソリン車とディーゼル車の市場シェアが全体的に上昇しました。

2023年3月、欧州連合(EU)とドイツは、乗用車とトラック用のガソリンエンジンとディーゼルエンジンを含む内燃エンジンの一部を2035年以降も販売することを認めることで合意したと発表しました。この決定は、ドイツの市場関係者に強い将来展望をもたらすものです。

ドイツKBA連邦運輸局によると、2023年12月の四輪乗用車新車登録台数のうち、ディーゼルエンジン車とガソリンエンジン車の合計シェアは、全パワートレイン車の総販売台数の45.5%です。

以上のことから、予測期間中、ドイツが欧州の内燃エンジン市場を独占することになります。

欧州の内燃エンジン産業概要

欧州の内燃エンジン市場は半分断されています。この市場の主要企業には、Audi、Volkswagen Group、VolvoAB、MAN SE、Bayerische Motoren Werke AG、Hyundai Motors、Toyota Motor Corporationなどが含まれます(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- ICE二輪車需要の増加

- プラグインハイブリッド内燃エンジン車(PHEV)の台頭

- 抑制要因

- バッテリー電気自動車市場の成長

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 容量別

- 50~200 cm3

- 201~800 cm3

- 801~1,500 cm3

- 1,501~3,000 cm3

- 燃料タイプ別

- ガソリン

- ディーゼル

- その他

- 地域別

- 英国

- イタリア

- フランス

- ドイツ

- ロシア

- ノルディック

- トルコ

- その他の欧州

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- 市場参入企業

- Volkswagen Group

- Volvo AB

- MAN SE

- Bayerische Motoren Werke AG

- Hyundai Motors

- Toyota Motor Corporation

- 市場参入企業

- 市場ランキング分析

- その他の著名な企業一覧

第7章 市場機会と今後の動向

- プラグインハイブリッド車の技術革新と最新技術の採用

The Europe Internal Combustion Engines Market size is estimated at USD 47.69 billion in 2025, and is expected to reach USD 58.30 billion by 2030, at a CAGR of 4.1% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, increasing demand for ICE two-wheelers and the rise of plug-in hybrid ICE vehicles (PHEV) are expected to drive the growth of the Europe Internal Combustion Engines Market during the forecast period.

- On the other hand, the rising battery electric vehicle market and demand for the adoption of cleaner fuels in regard to the green climate goals are expected to hinder the growth of Europe's internal combustion engine market during the forecast period.

- Nevertheless, technological innovation and adaptation of the latest technologies in plug-in hybrid vehicles are likely to create opportunities for the European internal combustion engine market during the forecast period.

- Germany dominates the market and is also likely to witness the highest grwoth during the forecast period.

Europe Internal Combustion Engines Market Trends

Diesel to have Significant Share in the Market

Diesel engines are one of the most significant internal combustion engines that have been in use since the 1870s. These engines are designed to generate mechanical energy after the combustion of an air-diesel mixture. No auxiliary component like a spark plug is used to ignite the air-diesel mixture; instead, it uses the elevating temperature of the air, which is compressed by a piston moving inside an engine block.

Diesel ICE engines are fuel-efficient and have better acceleration, towing, and hauling potential than gasoline engines. Thus, they have been quite a familiar and popular fuel source in Europe.

Diesel has been an important transportation fuel in Europe despite the European Union's initiatives to adopt cleaner energy sources. In 2023, 13.6 % of the newly registered vehicles in Europe had internal combustion engines that used diesel, thus accounting for a strong customer base in Europe.

A fair share of the diesel ICE engine market can be seen in the buses (commercial and private), government vehicles, trucks, and vans. According to the European Automobile Manufacturers' Association (ACEA), in 2023, diesel-powered buses remained the most popular in the EU, accounting for 62.3% of all new bus sales.

In 2023, diesel-powered ICE engines also saw a significant and strong base in the European trucking sector. According to ACEA, 95.7% of all newly registered trucks in the European Union run on diesel, while 1.5% were electric. Further, truck production increased in the European region. In 2023, nearly 603437 trucks were manufactured in Europe, which increased the total commercial vehicle production by around 20.3%, as compared to the previous year.

In October 2023, FedEx Corp. subsidiary company FedEx Express Europe, the world's largest express transportation company, announced the beginning of trialing hydrotreated vegetable oil (HVO) renewable diesel to fuel five of its company-owned trucks in the United Kingdom. This will provide a safe future outlook for the diesel engine market players, making changes in their products to adapt to renewable diesel.

Hence, such a scenario is likely to have a significant share of diesel engines in the coming years.

Germany to Likely to Dominate the Market

In recent years, Germany has seen a huge transition from Fossil fuels to Electric vehicles in all commercial and private vehicles, including Buses, Cars, Two-wheelers, and Trucks. Still, these developments have not negatively affected the market due to technological advancements in the PHEV sector.

A PHEV or a plug-in hybrid electric vehicle is a type of hybrid EV that combines a diesel or gasoline engine with a large battery pack and an electric motor that an EV charging station can recharge. Conventional PHEV automobiles have an electric motor and battery pack but derive all their power from gasoline or diesel.

The growing popularity among the nations' family households and the use of Plug-In Hybrid Electric vehicles in public transport and commercial heavy vehicles is key to the growth of Gasoline and Diesel powered ICE engines in Germany, showing a resonant use of both Fossil and Non-Fossil use.

Even apart from the PHEVs, Germany shares a significant number of diesel- and petrol-ICE-powered cars. According to the German KBA Federal Transport Authority, new sales of cars in Germany marked a rise of 7.3% in 2023, when compared to 2022 sales data, in which Petrol vehicle sales saw the most significant boost, rising by 13.3% to 979,000, leading to an overall market share increase for petrol and diesel-powered cars.

In March 2023, the European Union and Germany announced having reached an agreement allowing some internal combustion engines, including petrol and diesel engines, for Passenger cars and Trucks to be sold beyond 2035. The decision thus provides a strong future outlook for the market players in Germany.

According to the German KBA Federal Transport Authority, among the registration of new four-wheeler passenger vehicles in December 2023, the combined share of diesel and gasoline-powered vehicles was 45.5% of the total cars sold of all powertrains.

Thus, on the basis of the above points, Germany will dominate the European internal combustion engine market during the forecast period.

Europe Internal Combustion Engines Industry Overview

The Europe Internal Combustion Engines Market is semi-fragmented. The key players in this market include(in no particular order) Audi, Volkswagen Group, Volvo AB, MAN SE, Bayerische Motoren Werke AG, Hyundai Motors, and Toyota Motor Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing demand for ICE two-wheelers

- 4.5.1.2 Rise of plug-in hybrid ICE vehicles (PHEV)

- 4.5.2 Restraints

- 4.5.2.1 Rising Battery electric vehicle market

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By capacity

- 5.1.1 50 cm3 to 200 cm3

- 5.1.2 201 cm3 to 800 cm3

- 5.1.3 801 cm3 to 1500 cm3

- 5.1.4 1501 cm3 to 3000 cm3

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.2.3 Others

- 5.3 Geography

- 5.3.1 United Kingdom

- 5.3.2 Italy

- 5.3.3 France

- 5.3.4 Germany

- 5.3.5 Russia

- 5.3.6 NORDIC

- 5.3.7 Turkey

- 5.3.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Market Players

- 6.3.1.1 Volkswagen Group

- 6.3.1.2 Volvo AB

- 6.3.1.3 MAN SE

- 6.3.1.4 Bayerische Motoren Werke AG

- 6.3.1.5 Hyundai Motors

- 6.3.1.6 Toyota Motor Corporation

- 6.3.1 Market Players

- 6.4 Market Ranking Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological innovation and adaptation of the latest technologies in plug-in hybrid vehicles