|

|

市場調査レポート

商品コード

1687906

航空機エンジンMRO-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Aircraft Engine MRO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空機エンジンMRO-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 157 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

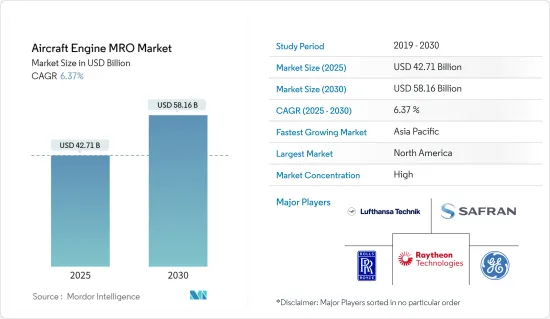

航空機エンジンMRO市場規模は2025年に427億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.37%で、2030年には581億6,000万米ドルに達すると予測されます。

COVID-19パンデミックが航空機エンジンMRO市場に与えた影響は大きいです。大量の航空機が保管され、稼働率が低下した結果、航空機エンジンMRO需要は2020年に大きく落ち込みました。しかし、2021年には航空産業は緩やかな回復を見せ始め、旅客数と航空機の移動が増加しました。これにより、航空機の整備、修理、オーバーホール活動の需要が増加しました。

航空会社や軍の急速な機体拡大計画は、予測期間中に航空機エンジンMRO市場の成長をさらに押し上げると予想されます。

一部の国では、防衛費の不足により、老朽化した軍用機の耐用年数を延長する計画があるため、軍用機の老朽化が大きな需要を生む可能性があります。

新型航空機への新世代エンジンの導入は、航空機エンジンのさらなるMRO需要を増加させると予想されます。新型エンジンは旧型機よりも高価な材料が必要となります。

エンジンMROの参入企業別、全体的なメンテナンスプロセスの効率を高め、全体的なターンアラウンドタイムを短縮し、安全性を向上させるために、メンテナンス活動をデジタル化し、自動化する先進技術の導入は、今後数年間の市場の成長を後押しすると予想されます。

航空機エンジンMRO市場動向

民間航空セグメントが市場シェアで市場を独占

民間航空セグメントは現在最も高い市場シェアを占めており、予測期間中もその優位性は続くと予想されます。これは、軍用航空に比べて民間航空は保有機数が多いこと、一般航空に比べてエンジンのメンテナンス費用が高いことが主要理由です。近年、航空会社とMROサービスプロバイダとの間で、航空機エンジンのメンテナンスに関するいくつかの新しい契約が結ばれています。例えば2021年11月、SR TechnicsはVietjet Airと、VietjetのAirbusA320とAirbusA321に搭載されているCFM56-5BエンジンのMROサービスを提供する覚書を締結しました。この契約は1億5,000万米ドルで締結されました。この契約では、同社はエンジンのメンテナンス、部品要件、修理、技術、訓練サービスを提供する予定です。同社は、VietjetとSR Technicsの合弁事業として、新しい航空訓練センターを設立する予定です。

同様に、MROサービスプロバイダは、業務用エンジンMROサービスに対する需要の高まりに対応するため、様々な国でのプレゼンスを拡大しています。この点に関して、S7 Technicsは2021年9月、シェレメーチエヴォ空港(モスクワ)にCFM56-5Bと-7BエンジンとHoneywell131-9A/9B補助動力装置(APU)のオーバーホールを行う新しいエンジン整備工場を開設する計画を発表しました。新工場の整備能力は、年間最大100台のAPUと最大42台のエンジンに達する見込みです。

このような民間航空会社との複数のサービスプロバイダとの提携は、航空機エンジンの耐空性と飛行の安全性を維持するための継続的なサービスのために、予測期間中も長く続いています。このようなパートナーシップにより、予測期間中、民間部門が最も高い市場シェアで市場をリードすると予想されます。

予測期間中、アジア太平洋が最も高い需要を生み出す見込み

アジア太平洋は過去10年間で航空機保有台数が大幅に増加し、エンジンMROサービスの需要が高まり、予測期間中市場をリードすると予想されます。その結果、米国や欧州の複数のMROサービスプロバイダがこの地域にメンテナンス施設を設置するようになりました。さらに、いくつかの航空会社は、海外のメンテナンスコストを削減するために、エンジンMROサービスプロバイダと提携し、社内能力を開発しています。例えば

中国国際航空は2022年9月、中国にジョイントベンチャー(JV)の整備・修理・オーバーホール(MRO)施設を設立すると発表しました。新しい施設であるBeijing Aero Engine Services Company Limitedは、Rolls-Royceのトレント700、トレントXWB-84、トレント1,000の航空エンジンのMROサポートを記載しています。中国国際航空とRolls-Royceは、それぞれ50%の株式を保有し、約26億1,000万元(約3億7,820万米ドル)の契約を結んでいます。

同地域へのメーカーの投資もまた、同地域での高収益、ひいては市場の成長を牽引しています。国際的な大手航空機エンジンメーカーであるサフランは2022年2月、中国の蘇州に新たなMRO施設を開設すると発表しました。この施設は現在設立中で、2022年末までに稼動する予定です。同社が所有する5,200平方メートルの修理ステーションは、戦略的なコミットメントに役立ち、中東とインドにまたがる同社のMRO施設とリンクし、同社を世界の主要航空会社のMROサービスの最適な選択肢にします。

2022年7月、Safranはインドのハイデラバードに最大2億米ドルを投資して同社最大のMRO施設を設立することも発表しました。この施設は年間300件のエンジン工場訪問に対応でき、特にインド市場を独占するCFM56、Leap 1A、Leap 1Bエンジンに対応します。この大規模な施設は、Safranのアジアのエンジン顧客向けのMRO施設としても使用される予定です。このようないくつかの投資、政府の奨励、旅客流入の潜在的な増加により、予測期間中、アジア太平洋で市場は大きな成長率を示すことが期待されています。

航空機エンジンMRO産業概要

航空機エンジンMRO市場の主要企業は、Lufthansa Technik、Rolls-Royce Holding PLC、Raytheon Technologies Corporation、General Electric Company、Safran SAです。主要なエンジンMROプロバイダは、エンジンMROの顧客を増やすために、長期的なパートナーシップを結んだり、ジョイントベンチャーを形成したりしています。例えば、2022年6月、ST Engineeringは、同社の商用航空宇宙事業が、世界有数の航空宇宙エンジンメーカーであるSafran Aircraft Enginesと、ST EngineeringがCFM56-5Bと-7Bエンジンのエンジンメンテナンス(工場訪問)オフロードを提供するための5年契約を締結したと発表しました。この複数年契約により、ST EngineeringとSafran Aircraft Enginesは、航空旅行がパンデミックから徐々に回復するにつれて予測されるエンジンMRO活動の増加に対応できるようになる可能性があります。経済的安定性という点では市場内の参入企業にとって計り知れない利点があるにもかかわらず、軍や民間航空会社との既存参入企業の長期契約は、新規参入参入企業の障壁となる可能性があります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

- 米ドルの通貨換算レート

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- エンジンタイプ別

- タービンエンジン

- ターボプロップ

- ターボファン

- ターボシャフト

- ピストンエンジン

- タービンエンジン

- 用途別

- 民間航空

- 軍用機

- 一般航空

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Lufthansa Technik

- Rolls-Royce Holding PLC

- Raytheon Technologies Corporation

- General Electric Company

- Safran SA

- Singapore Technologies Engineering Ltd

- Delta Air Lines Inc.

- Hong Kong Aircraft Engineering Company Limited(HAECO)

- MTU Aero Engines AG

- Textron Inc.

- Honeywell International Inc.

- Israel Aerospace Industries Ltd

- S7 Technics

- SR Technics Switzerland Ltd

- Other Players

- Lockheed Martin Corporation

- AFI KLM E& M

- Magnetic MRO AS

- Sanad Aerotech

第7章 市場機会と今後の動向

The Aircraft Engine MRO Market size is estimated at USD 42.71 billion in 2025, and is expected to reach USD 58.16 billion by 2030, at a CAGR of 6.37% during the forecast period (2025-2030).

The impact of the COVID-19 pandemic on the aircraft engine MRO market has been significant. As a result of a large number of stored aircraft and lower utilization, the aircraft engine MRO demand significantly dropped in 2020. However, in 2021, aviation began to witness a gradual recovery, leading to increased passenger traffic and aircraft movements. This has led to an increase in demand for aircraft maintenance, repair, and overhaul activities.

The rapid fleet expansion plans of the airlines and military forces are anticipated to boost further the aircraft engine MRO market growth during the forecast period.

The aging military aircraft fleet in some countries may generate significant demand, as some have plans to extend the service life of these aging aircraft due to a lack of defense funding.

The introduction of newer generation engines in new aircraft is anticipated to increase the aircraft engine further MRO demand. The new engines will have more expensive material requirements than the older aircraft.

The introduction of advanced technologies that will digitize and automate maintenance activities to increase overall maintenance process efficiency, reduce the overall turnaround time, and improve safety by the engine MRO players is anticipated to boost the market's growth in the coming years.

Aircraft Engine MRO Market Trends

The Commercial Aviation Segment Dominates the Market in Terms of Market Share

The commercial aviation segment currently has the highest market share, and it is expected to continue its dominance during the forecast period. This is majorly due to the large fleet of commercial aviation compared to military aviation and the high cost of engine maintenance cost compared to general aviation. In recent years, several new contracts have been signed for the maintenance of aircraft engines between airlines and MRO service providers. For instance, in November 2021, SR Technics signed a Memorandum of Understanding (MoU) with Vietjet Air to provide MRO services for CFM56-5B engines onboard Vietjet's Airbus A320 and Airbus A321 aircraft fleet. The agreement was signed worth USD 150 million. Under the contract, the company is expected to provide engine maintenance, component requirements, repair, technical, and training services. It will set up a new Aviation training center as a joint venture between Vietjet and SR Technics.

Similarly, MRO service providers are expanding their presence in various countries to cater to the growing demand for commercial engine MRO services. In this regard, in September 2021, S7 Technics announced its plan to open a new engine maintenance facility at Sheremetyevo airport (Moscow) to overhaul CFM56-5B and -7B engines and Honeywell 131-9A/9B auxiliary power units (APU). The maintenance capacity of the new shop is expected to reach up to 100 APUs and up to 42 engines per year.

Multiple such service provider partnerships with commercial carriers are extending long into the forecast period for continued service of aircraft engines to be airworthy and safe for flight. Due to these partnerships, the commercial segment of the market is expected to lead the market with the highest market share during the forecast period.

Asia-Pacific is Expected to Generate the Highest Demand During the Forecast Period

Asia-Pacific has experienced significant growth in the total aircraft fleet over the past decade, which has increased the demand for engine MRO services and is expected to lead the market during the forecast period. This has resulted in several MRO service providers from the United States and Europe establishing their maintenance facilities in this region. Furthermore, several airlines have partnered with engine MRO service providers to reduce overseas maintenance costs to develop in-house capabilities. For instance,

Air China, in September 2022, announced that they are entering a Joint Venture (JV) maintenance, repair, and overhaul (MRO) facility in China. The new facility, Beijing Aero Engine Services Company Limited, will provide MRO support on the Rolls-Royce Trent 700, Trent XWB-84, and Trent 1000 aero engines. Air China and Rolls-Royce each hold 50% of the shares in the joint venture with a contract, accounting for about 2.61 billion yuan (about USD 378.2 million).

Manufacturer investments in the region are also driving high revenues and, consequently, market growth in the region. Safran - a large international aircraft engine manufacturer, in February 2022 announced the opening of a new MRO facility in Suzhou, China. The facility is being set up and is expected to be operational by the end of 2022. The company-owned 5,200 sq meter repair station helps it in strategic commitments, linking it to the company's MRO facilities across the Middle-Eastern and Indian facilities, making the company an optimal choice for MRO services for major airlines globally.

In July 2022, Safran also announced that it would invest up to USD 200 Million to set up its biggest MRO facility in Hyderabad, India. The facility would be capable of handling up to 300 engine shop visits annually, especially catering to the CFM56, Leap 1A, and Leap 1B engines that dominate the Indian market. This large facility is also expected to be used as an MRO facility for Safran's Asian engine customers. Due to several such investments, government incentivization, and the potential increase in passenger influx, the market is expected to witness significant growth rates in the Asian-Pacific region during the forecast period.

Aircraft Engine MRO Industry Overview

The prominent players in the aircraft engine MRO market are Lufthansa Technik, Rolls-Royce Holding PLC, Raytheon Technologies Corporation, General Electric Company, and Safran SA. The major engine MRO providers are entering into long-term partnerships or forming joint ventures to grow their engine MRO customers. For instance, in June 2022, ST Engineering announced that their Commercial Aerospace business had signed a five-year agreement with Safran Aircraft Engines, a global-leading aerospace engine manufacturer, for ST Engineering to provide engine maintenance (shop visit) offload for the CFM56-5B and -7B engines. This multi-year agreement may allow ST Engineering and Safran Aircraft Engines to meet the forecasted rise of engine MRO activities as air travel gradually recovers from the pandemic. Despite being an immense advantage for the players within the market in terms of economic stability, the long-term contracts of the established players with the armed forces and commercial airlines may act as a barrier for new players to enter the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

- 1.3 Currency Conversion Rates for USD

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size and Forecast by Value - USD billion, 2018 - 2027)

- 5.1 By Engine Type

- 5.1.1 Turbine Engine

- 5.1.1.1 Turboprop

- 5.1.1.2 Turbofan

- 5.1.1.3 Turboshaft

- 5.1.2 Piston Engine

- 5.1.1 Turbine Engine

- 5.2 By Application

- 5.2.1 Commercial Aviation

- 5.2.2 Military Aviation

- 5.2.3 General Aviation

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Egypt

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Lufthansa Technik

- 6.2.2 Rolls-Royce Holding PLC

- 6.2.3 Raytheon Technologies Corporation

- 6.2.4 General Electric Company

- 6.2.5 Safran SA

- 6.2.6 Singapore Technologies Engineering Ltd

- 6.2.7 Delta Air Lines Inc.

- 6.2.8 Hong Kong Aircraft Engineering Company Limited (HAECO)

- 6.2.9 MTU Aero Engines AG

- 6.2.10 Textron Inc.

- 6.2.11 Honeywell International Inc.

- 6.2.12 Israel Aerospace Industries Ltd

- 6.2.13 S7 Technics

- 6.2.14 SR Technics Switzerland Ltd

- 6.3 Other Players

- 6.3.1 Lockheed Martin Corporation

- 6.3.2 AFI KLM E&M

- 6.3.3 Magnetic MRO AS

- 6.3.4 Sanad Aerotech