|

市場調査レポート

商品コード

1644974

北米の低圧開閉装置:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)North America Low Voltage Switchgear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の低圧開閉装置:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

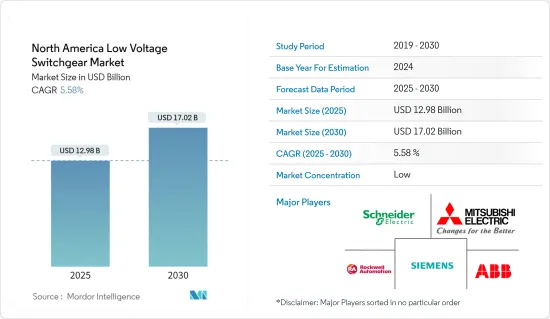

北米の低圧開閉装置市場規模は2025年に129億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.58%で、2030年には170億2,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、再生可能エネルギー導入の増加や建設活動の活発化といった要因が、この市場の大きな成長促進要因となっています。北米全域で配電システムの数が増加しており、低圧開閉装置市場の需要が大幅に増加しています。

- その一方で、高い設置コストやプロジェクト実行の遅延が市場の成長を抑制しています。

- 一次配電網と二次配電網にまたがる低圧開閉装置の需要は、市場成長にとって有利な機会を生み出す可能性が高いです。

北米の低圧開閉装置市場動向

配電セグメントが大きな成長を遂げる

- 配電システムには、送電線、変電器、変圧器、その他の機器のネットワークが含まれ、電力を輸送してエンドユーザーに供給します。配電システムは、一次配電と二次配電に分けられます。一次配電は、発電所から地域の変電所まで高圧電力を送電することを指します。二次配電とは、低圧の電力をエンドユーザーに供給することです。

- 北米では工業化と都市化が急速に進み、多数の商業・産業事業体が出現しています。このため、データセンター、製造業、その他の産業が大幅に成長しています。この動向は、開閉装置など様々な送電や配電機器に対する需要を増加させると予想されます。

- 従来の発電源から再生可能エネルギーへの急速な移行は、地域全体の配電網拡大需要をさらに強化します。2022年には、約817.8TWhの電力が再生可能エネルギー源から発電されています。

- 工業化と都市化に伴い、電力需要は増加しています。そのため、米国とカナダでは配電システムの需要が増加しています。

- 米国エネルギー情報局(EIA)によると、2022年の米国の総電力消費量は約4兆500億kWhでした。米国の産業・商業部門による直接電力使用量は、2022年の最終消費電力量の約3%です。

- したがって、上記の点から、予測期間中は配電システムが大きな市場シェアを占めると予想されます。

市場を独占する米国

予測期間中、米国が低圧開閉装置市場を独占すると予想されます。化石燃料ベースの発電からクリーンなエネルギー源ベースの発電への移行により、送配電インフラ需要が増加しています。

同国では、太陽光、風力、バイオエネルギー、バイオメタンなど、よりクリーンなエネルギー源による発電への移行が進んでいます。このような発電源の設置が増加することで、配電網の拡大需要が高まり、低圧開閉装置の設置がさらに増加します。IRENAによると、2022年の同国の再生可能エネルギー設備容量は約351.67GWであった、

また、同国では配電システムのアップグレードへの投資も増加しています。スマートグリッド技術の確立と国内の急速な工業化も、低圧開閉装置市場の成長を後押ししています。

また、主要な市場参入企業は国内の配電網を拡大しており、海外の参入企業も米国の配電市場に参入しています。例えば、2021年4月、イタリアを拠点とするエネルギー企業エネルは、エネルギー配給事業を米国市場に拡大する計画を発表しました。同社は今後2年間で配電網に約195億2,000万米ドルを投資する計画で、2030年までに約722億3,000万米ドルの投資を準備しています。

上記のような要因が、予測期間中の米国の低圧開閉装置市場の成長を促進すると考えられます。

北米の低圧開閉装置産業概要

低圧開閉装置市場は細分化されています。この市場の主要企業(順不同)には、ABB Ltd.、Mitsubishi Electric Corporation、Schneider Electric、Rockwell Automation、Toshiba Corporationなどがあります。

Toshiba Corporationによると、同社の戦略的手法には、ソリューションと高付加価値サービスの提供と能力を高めることにより、有機的成長の触媒として機能する同社の製造施設の拡大が含まれます。例えば、2023年3月、Siemensはフランクフルト・フェッヘンハイムの開閉装置工場を拡大するために3,261万米ドルを投資しました。16万平方メートルの敷地に、スマートで完全自動化された高速倉庫と、既存ホールの1,200平方メートルの増築が行われます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 再生可能エネルギーの導入拡大

- 抑制要因

- 高い設置コスト

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途

- 変電

- 配電

- 設置

- 屋外

- 屋内

- 電圧範囲

- 250V以下

- 250 V-750 V

- 750V-1,000V

- 地域

- 米国

- カナダ

- その他の北米地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- ABB Ltd.

- Mitsubishi Electric Corporation

- Schneider Electric

- Rockwell Automation

- Siemens AG

- WEG

- Fuji Electric

- Hitachi

- Toshiba Corporation

第7章 市場機会と今後の動向

- 一次と二次配電網における低圧開閉装置需要

The North America Low Voltage Switchgear Market size is estimated at USD 12.98 billion in 2025, and is expected to reach USD 17.02 billion by 2030, at a CAGR of 5.58% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the growing installation of renewable energy and rising construction activities are the significant growth driving factors for this market. The rising number of distribution systems across North America significantly increases the demand for the low-voltage switchgear market.

- On the other hand, high installation costs, as well as delays in the project execution, restrains the growth of the market.

- Nevertheless, the low-voltage switchgear demand across primary and secondary distribution networks will likely create lucrative opportunities for market growth.

North America Low Voltage Switchgear Market Trends

Distribution Segment to Witness a Significant Growth

- The distribution system includes a network of power lines, substations, transformers, and other equipment to transport and deliver electrical power to the end users. The distribution system is divided into two categories primary and secondary distribution. The primary distribution refers to transmitting high-voltage electricity from the power plant to the local substations. The secondary distribution refers to the delivery of lower-voltage electricity to end-users.

- North America is witnessing a rapid increase in industrialization and urbanization, leading to the emergence of numerous commercial and industrial entities. This led to substantial growth in data centers, manufacturing, and other industries. This trend is anticipated to increase the demand for various transmission and distribution equipment such as switchgear, etc.

- The rapid transition from conventional sources of electricity generation to renewable sources further bolsters the demand for distribution network expansion across the region. In 2022, around 817.8 TWh of electricity has been generated from renewable energy sources.

- Along with industrialization and urbanization, the electricity demand has increased. Thus, increasing the demand for distribution systems in the United States and Canada.

- According to U.S. Energy Information Administration (EIA), total electricity consumption in the United States in 2022 was about 4.05 trillion kWh. Direct electricity use by the industrial and commercial sectors in the United States was about 3% of total electricity end-use consumption in 2022.

- Therefore owing to the above points, the distribution system is expected to hold a significant market share during the forecasted period.

United States to Dominate the Market

The United States is anticipated to dominate the low-voltage switchgear market during the forecast period. The transition from fossil fuel-based electricity generation to clean sources-based energy generation increases the transmission and distribution infrastructure demand.

The country's transition towards cleaner sources of energy generation, such as solar, wind, bioenergy, biomethane, and others. The increasing installation of such electricity-generating sources increases the demand for the expansion of the distribution networks, which further increases the installation of low-voltage switchgear. According to IRENA, the country's installed renewable energy capacity was around 351.67 GW in 2022,

In addition, the investment in upgrading the distribution systems is also increasing in the country. Establishing smart grid technology and rapidly growing industrialization within the country is also responsible for driving growth in the low-voltage switchgear market.

The key market players are also expanding their distribution networks within the country, and several foreign players are also entering the U.S. distribution market. For instance, In April 2021, Enel, an Italy-based energy company, announced its plans to expand its energy distribution business into the U.S. market. The company planned to invest around USD 19.52 billion in distribution networks over the next two years, and it has prepared to invest around USD 72.23 billion by 2030.

The factors mentioned above are likely to drive growth in the low-voltage switchgear market in the United States during the forecast period.

North America Low Voltage Switchgear Industry Overview

The low voltage switchgear market is fragmented. Some of the key players in this market (not in a particular order) include ABB Ltd., Mitsubishi Electric Corporation, Schneider Electric, Rockwell Automation, and Toshiba Corporation, among others.

According to the Toshiba Corporation, the company's strategic methods include, expaning company's manufacturing facilities that act as catalysts for the organic growth by increasing its solutions and high-value services offerings and capabilities. For instance, in March 2023, Siemens invested USD 32.61 million to expand its switchgear plant in Frankfurt-Fechenheim. A smart, fully automated high-speed warehouse and a 1,200 square-meter extension to an existing hall are being built on the 160,000 square-meter site.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Installation of Renewable Energy

- 4.5.2 Restraints

- 4.5.2.1 High Installation Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Substation

- 5.1.2 Distribution

- 5.2 Installation

- 5.2.1 Outdoor

- 5.2.2 Indoor

- 5.3 Voltage Range

- 5.3.1 Below 250 V

- 5.3.2 250 V - 750V

- 5.3.3 750V - 1000 V

- 5.4 Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABB Ltd.

- 6.3.2 Mitsubishi Electric Corporation

- 6.3.3 Schneider Electric

- 6.3.4 Rockwell Automation

- 6.3.5 Siemens AG

- 6.3.6 WEG

- 6.3.7 Fuji Electric

- 6.3.8 Hitachi

- 6.3.9 Toshiba Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Low-voltage Switchgear Demand across Primary and Secondary Distribution Networks