低電圧開閉装置市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Low Voltage Switchgear Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034- 発行日

- ページ情報

- 英文 138 Pages

- 納期

- 2~3営業日

- 商品コード

- 1699403

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

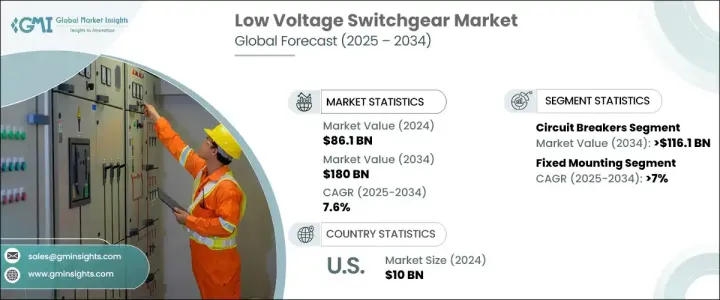

低電圧開閉装置の世界市場規模は2024年に861億米ドルとなり、2025年から2034年にかけてCAGR 7.6%で拡大すると予測されています。

電力消費の増加、インフラの拡大、スマートグリッドソリューションの技術進歩がこの成長を後押ししています。同市場は産業、商業、住宅用途にまたがり、自動化動向、再生可能エネルギーの採用、厳格な安全規制などに支えられています。新興経済諸国における急速な都市化と工業化が、特にデータセンター、商業スペース、工業施設での需要を加速しています。発電・配電インフラへの投資の増加は、先進的な開閉装置・ソリューションの需要を促進しています。インダストリー4.0と産業オートメーションへの移行は市場を再形成し、インテリジェントでデジタル統合された開閉装置の必要性を高めています。AI主導の予測分析を備えたスマートシステムは、電気障害の早期検出を可能にし、効率と信頼性を高める。

保護タイプ別では、サーキットブレーカー部門は、電気部門への大規模な投資に牽引され、2034年までに1,161億米ドルを超えると予測されています。将来の電力需要を満たすために800億米ドルを超える産業投資が予想され、需要をさらに押し上げます。持続可能なエネルギー源へのシフトは、低電圧開閉装置の必要性を高めています。2024年には、クリーンエネルギー技術を含むエネルギープロジェクトに1,100億米ドル以上が割り当てられ、市場の成長軌道を浮き彫りにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 861億米ドル |

| 予測金額 | 1,800億米ドル |

| CAGR | 7.6% |

固定式取り付け分野は、費用対効果、信頼性、設置の容易さが原動力となり、2034年までのCAGRは7%を超えると予想されます。産業、商業、公共事業分野で広く応用されているため、市場の主要な構成要素となっています。人口増加や都市拡張と相まって電力への依存度が高まっているため、特にインフラ整備が急速に進んでいる地域では、低電圧開閉装置に対する需要が高まっています。

米国市場は着実な成長を遂げており、2022年には87億米ドル、2023年には93億米ドル、2024年には100億米ドルに達します。電気インフラへの大規模な投資が、さまざまな業界の低電圧開閉装置需要を促進しています。投資家所有の公益事業会社は、2023年に約1,700億米ドルを送電網拡張に充当しており、市場の潜在力が高いことを示しています。さらに、約1,340億米ドルが電力建設プロジェクトに向けられ、開閉装置・ソリューションの需要をさらに押し上げています。このようなプロジェクトの増加は、北米全体の市場を強化し、その上昇軌道を強化します。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:プロテクション別、2021年~2034年

- 主要動向

- サーキットブレーカー

- ACB

- MCCB

- MCB

- MSP

- MPCB

- ヒューズ

- ヒューズスイッチディスコネクター

- ヒューズ付きディスコネクター

- その他

第6章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- 固定マウント

- プラグイン

- 引き出し式

第7章 市場規模・予測:定格電流別、2021年~2034年

- 主要動向

- 1000アンペア以下

- 1000アンペア~5000アンペア

- 5000アンペア超

第8章 市場規模・予測:定格電圧別、2021年~2034年

- 主要動向

- 250ボルト以下

- 250ボルト~750ボルト

- 750ボルト超

第9章 市場規模・予測:電流別、2021年~2034年

- 主要動向

- 交流

- 直流

第10章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 変電所

- 配電

- 力率改善

- サブ配電

- モーター制御

第11章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第12章 企業プロファイル

- ABB

- Bharat Heavy Electricals

- CG Power and Industrial Solutions

- E+I Engineering

- Eaton

- Fuji Electric

- General Electric

- HD Hyundai Electric

- Hitachi

- Hyosung Heavy Industries

- Lucy Group

- Mitsubishi Electric

- Ormazabal

- Schneider Electric

- Siemens

- Skema

- Toshiba

目次

The Global Low Voltage Switchgear Market was valued at USD 86.1 billion in 2024 and is projected to expand at a CAGR of 7.6% from 2025 to 2034. Increasing electricity consumption, infrastructure expansion, and technological advancements in smart grid solutions are driving this growth. The market spans industrial, commercial, and residential applications, supported by automation trends, renewable energy adoption, and stringent safety regulations. Rapid urbanization and industrialization in developing economies are accelerating demand, particularly in data centers, commercial spaces, and industrial facilities. Growing investments in power generation and distribution infrastructure are fueling demand for advanced switchgear solutions. The transition toward Industry 4.0 and industrial automation is reshaping the market, increasing the need for intelligent and digitally integrated switchgear. Smart systems equipped with AI-driven predictive analytics enable early detection of electrical faults, enhancing efficiency and reliability.

In terms of protection type, the circuit breaker segment is projected to surpass USD 116.1 billion by 2034, driven by significant investments in the electrical sector. Industry investments exceeding USD 80 billion are anticipated to meet future electricity demands, further boosting demand. The shift toward sustainable energy sources is amplifying the need for low voltage switchgear. In 2024, over USD 110 billion was allocated to energy projects, including clean energy technologies, highlighting the market's growth trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $86.1 Billion |

| Forecast Value | $180 Billion |

| CAGR | 7.6% |

The fixed mounting segment is expected to register a CAGR of over 7% through 2034, driven by cost-effectiveness, reliability, and ease of installation. Its widespread application in industrial, commercial, and utility sectors makes it a key market component. The increasing reliance on electricity, coupled with population growth and urban expansion, is intensifying demand for low voltage switchgear, especially in regions experiencing rapid infrastructure development.

The U.S. market has witnessed steady growth, reaching USD 8.7 billion in 2022, USD 9.3 billion in 2023, and USD 10 billion in 2024. Extensive investments in electrical infrastructure are fueling demand for low voltage switchgear across various industries. Investor-owned utilities allocated approximately USD 170 billion toward grid expansion in 2023, signaling strong market potential. Additionally, around USD 134 billion was directed toward power construction projects, further driving demand for switchgear solutions. The increasing number of such projects is set to bolster the market across North America, reinforcing its upward trajectory.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Protection, 2021 – 2034 (USD Million, Units)

- 5.1 Key trends

- 5.2 Circuit breakers

- 5.2.1 ACB

- 5.2.2 MCCB

- 5.2.3 MCB

- 5.2.4 MSP

- 5.2.5 MPCB

- 5.3 Fuse

- 5.3.1 Fuse-Switch disconnector

- 5.3.2 Switch disconnector with fuse

- 5.3.3 Others

Chapter 6 Market Size and Forecast, By Product 2021 – 2034 (USD Million, Units)

- 6.1 Key trends

- 6.2 Fixed mounting

- 6.3 Plug-in

- 6.4 Withdrawable unit

Chapter 7 Market Size and Forecast, By Rated Current 2021 – 2034 (USD Million, Units)

- 7.1 Key trends

- 7.2 ≤ 1000 Ampere

- 7.3 > 1000 Ampere to ≤ 5000 Ampere

- 7.4 > 5000 Ampere

Chapter 8 Market Size and Forecast, By Voltage Rating 2021 – 2034 (USD Million, Units)

- 8.1 Key trends

- 8.2 ≤ 250 volts

- 8.3 > 250 volts to ≤ 750 volts

- 8.4 > 750 volts

Chapter 9 Market Size and Forecast, By Current 2021 – 2034 (USD Million, Units)

- 9.1 Key trends

- 9.2 AC

- 9.3 DC

Chapter 10 Market Size and Forecast, By Application 2021 – 2034 (USD Million, Units)

- 10.1 Key trends

- 10.2 Substation

- 10.3 Distribution

- 10.4 Power factor correction

- 10.5 Sub distribution

- 10.6 Motor control

Chapter 11 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.2.3 Mexico

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 France

- 11.3.3 Germany

- 11.3.4 Italy

- 11.3.5 Russia

- 11.3.6 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Australia

- 11.4.3 India

- 11.4.4 Japan

- 11.4.5 South Korea

- 11.5 Middle East & Africa

- 11.5.1 Saudi Arabia

- 11.5.2 UAE

- 11.5.3 Turkey

- 11.5.4 South Africa

- 11.5.5 Egypt

- 11.6 Latin America

- 11.6.1 Brazil

- 11.6.2 Argentina

Chapter 12 Company Profiles

- 12.1 ABB

- 12.2 Bharat Heavy Electricals

- 12.3 CG Power and Industrial Solutions

- 12.4 E + I Engineering

- 12.5 Eaton

- 12.6 Fuji Electric

- 12.7 General Electric

- 12.8 HD Hyundai Electric

- 12.9 Hitachi

- 12.10 Hyosung Heavy Industries

- 12.11 Lucy Group

- 12.12 Mitsubishi Electric

- 12.13 Ormazabal

- 12.14 Schneider Electric

- 12.15 Siemens

- 12.16 Skema

- 12.17 Toshiba

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 138 Pages

- 納期

- 2~3営業日