シンガポールの交通インフラ建設:市場シェア分析、産業動向、成長予測(2025年~2030年)

Singapore Transportation Infrastructure Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644810

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

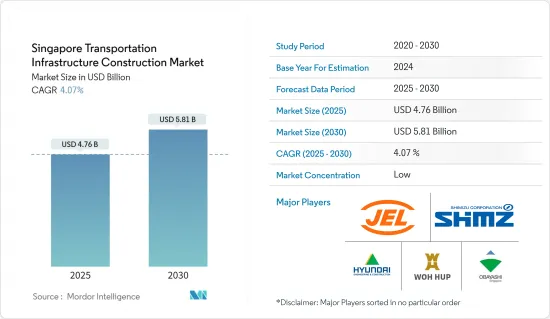

シンガポールの交通インフラ建設市場規模は2025年に47億6,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.07%で、2030年には58億1,000万米ドルに達すると予測されます。

建築建設庁(BCA)は、2023年の総建設需要を270億SGD(200億8,000万米ドル)から320億SGD(238億米ドル)の範囲と予測しています。公共部門の需要は総需要の約60%を占め、160億SGD(119億米ドル)から190億SGD(141億3,000万米ドル)になると予想されます。これは、HDBがBTOフラットの供給を拡大する中、引き続き堅調な公共住宅パイプラインに支えられています。

産業・施設建築の需要は、浄水場や教育施設、コミュニティ・クラブなどのプロジェクト増加に支えられ、健全なペースで伸び続けると予想されます。土木建設需要は、MRT路線やその他のインフラ建設に下支えされ、安定的に推移すると予想されます。

シンガポールの建設産業は、国のインフラ支出の増加に伴い、2022年にはCOVID-19以前の活動レベルに戻ると予想されました。商工省の最新データによると、建設産業の成長率は2022年第1四半期の2.4%に対し、第2四半期は3.3%となりました。

しかし、2021年9月から2022年2月にかけて実施された政府の労働者確保策によって部分的に緩和された労働力不足が、建設産業に影響を及ぼす可能性があります。

建設部門は、原油価格の上昇と世界のサプライチェーンの混乱にも影響を受けています。これは資材価格、機械、輸送コストの上昇につながりました。しかし、公共セクターのプロジェクトが牽引する建設需要の継続により、2024年には建設セクターの成長が見込まれています。

シンガポールの交通インフラ建設市場動向

同国における地下鉄の拡大

シンガポールの地下鉄システムの野心的な拡大は、国内企業だけでなく、この都市国家で実績のある外資系企業にも選択的な契約を提供し続けています。

2022年1月、同国の陸上交通局(LTA)は、クロスアイランド線フェーズ1(CRL1)の駅とトンネルの設計・建設に関する2件の土木契約を、合計契約額1億1,050万米ドルで発注しました。シンガポール企業と日本企業が受注しました。

全長29km、12の駅を持つクロスアイランド線は、シンガポールで8番目の路線です。ジュロン湖地区、プンゴル・デジタル地区、チャンギ地区などのハブを結び、東部、北東部、西部の各回廊の既存と将来の開発に対応します。駅の半数近くは他の鉄道路線と接続し、通勤客の利便性を高めています。

セラングーン・ノース駅とトンネルの設計・建設の最初の契約は、シンガポールのHock Lian Seng Infrastructureが5,830万米ドルで獲得しました。

Hock Lian Seng Infrastructureは、サークル・ラインのキム・チュアン・デポとマリーナ・ベイ駅を建設し、現在はトムソン・イースト・コースト・ライン(TEL)のマックスウェル駅の建設に携わっています。

2つ目の契約は、タビストック駅とトンネルの設計・建設で、契約金額は4億700万米ドル。

同社はシンガポールで長い経験を持ち、ダウンタウンラインのベンクーレン駅とマター駅、TELのアッパー・トムソン駅を建設しています。

チャンギ空港T-5工事の再開

パンデミックのため2年間中断していたシンガポールのチャンギ空港第5ターミナル(T5)の建設が再開されました。第一期工事は2024年頃に開始され、T5は2020年代半ばにオープンする予定です。新ターミナルは、チャンギ・イーストにある既存のチャンギ空港と同じ土地面積(1,080ha)に建設されます。年間約5,000万人の旅客を収容できるよう設計されたT5は、交通量の増加に合わせて2段階に分けて建設できる柔軟性を持っています。T5によって提供される追加容量は、地域と世界のハブ空港としてのチャンギ空港の地位を強化すると期待されています。

チャンギ空港のインフラは、旅客ターミナル、滑走路、誘導路、整備棟とサービス、地上支援設備で構成されています。チャンギ空港の既存の4つの旅客ターミナルは、年間8,200万人の旅客を収容できます。ターミナル5は完成時に年間5,000万人の旅客を収容する予定です。

シンガポールの交通インフラ建設産業概要

シンガポールの交通インフラ建設市場は非常に多様化しており、国内外から複数の企業が進出しています。同セグメントへの政府投資の動向の高まりから、今後数年間は安定した市場推移が見込まれます。多数のプロジェクトが進行中であるため、市場には常に新規参入の余地があります。同市場の主要企業には、Samsung C&T、Hyundai E&C、Daaelim Industrial、GS E&C、Daewoo E&Cなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 市場力学

- 促進要因

- 観光産業の増加

- 持続可能性と環境への懸念

- 抑制要因

- 財政的制約

- 高いメンテナンスと維持費

- 機会

- 技術の進歩

- 促進要因

- バリューチェーン/サプライチェーン分析

- 産業の規制と施策

- このセグメントにおける技術開発

- 産業の競合-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者/買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響

第5章 市場セグメンテーション

- モード別

- 道路

- 鉄道

- 航空

- 港湾・内陸水路

第6章 競合情勢

- 概要(全体市場シェア、市場集中度と主要企業、企業比較分析)

- 企業プロファイル

- Woh Hup Holdings Pte Ltd

- Shimizu Corporation

- Jurong Engineering Limited

- Hyundai Engineering & Construction Co. Ltd.

- Obayashi Singapore Private Limited

- Koh Brothers Building & Civil Engineering Contractor Pte Ltd

- Tiong Seng Group

- Lum Chang Holdings Limited

- Daelim Industrial Co Ltd

- CSC Holdings Limited*

- その他の企業(概要/主要情報)

第7章 シンガポールの交通インフラ建設市場の将来

第8章 付録

第9章 免責事項

目次

The Singapore Transportation Infrastructure Construction Market size is estimated at USD 4.76 billion in 2025, and is expected to reach USD 5.81 billion by 2030, at a CAGR of 4.07% during the forecast period (2025-2030).

Building and Construction Authority (BCA) predicts total construction demand for 2023 to be in the range of SGD 27 billion (USD 20.08 bn) to SGD 32 billion (USD 23.80 bn). Public sector demand is expected to account for about 60% of the total demand, ranging from SGD 16 billion (USD 11.90 bn) to SGD 19 billion (USD 14.13 bn). This is underpinned by a continuing strong public housing pipeline amid HDB's expansion of BTO flats supply.

Industrial and institutional building demand is expected to continue to grow at a healthy pace, underpinned by more projects for water treatment plants and educational buildings, as well as community clubs. Civil engineering construction demand should remain stable, underpinned by MRT line and other infrastructure construction.

Singapore's construction industry was expected to return to pre-COVID-19 activity levels in 2022 as the country's infrastructure spending increased. According to the latest data from the Ministry of Commerce and Industry, the construction industry grew by 3.3 percent in the second quarter of 2022 compared to the 2.4 percent recorded in the first quarter of 2022.

However, the construction industry may be affected by the labor shortage, which has been partially alleviated by the government's worker retention scheme, which was implemented between September 2021 and February 2022.

The construction sector has also been impacted by increasing oil prices and disruptions to global supply chains. This has led to an increase in material prices, machinery, and transportation costs. However, with continued construction demand driven by public sector projects, the construction sector is expected to grow in 2024.

Singapore Transportation Infrastructure Construction Market Trends

Metro Expansion in the Country

The ambitious expansion of Singapore's metro system continues to provide choice contracts for domestic firms and foreign ones with track records in the city-state.

In January 2022, the country's Land Transport Authority (LTA) awarded two civil contracts for the design and construction of Cross Island Line Phase 1 (CRL1) stations and tunnels at a combined contract value of USD 110.5 million. The contracts went to a Singaporean firm and a Japanese one.

Twenty-nine kilometers in length and with 12 stations, the Cross Island Line is Singapore's eighth. It will serve existing and future developments in the eastern, northeastern, and western corridors, linking hubs such as Jurong Lake District, Punggol Digital District, and Changi region. Nearly half of its stations will connect with other rail lines, increasing connectivity for commuters.

The first contract for the design and construction of Serangoon North station and tunnels has been won by Singaporean firm Hock Lian Seng Infrastructure at a contract value of USD 58.3 million.

Hock Lian Seng built the Kim Chuan Depot and Marina Bay station for the Circle Line and is currently involved in building Maxwell station along the Thomson-East Coast Line (TEL).

The second contract, for the design and construction of Tavistock station and tunnels, has been awarded to Japanese infrastructure company Sato Kogyo at a contract value of USD 407 million.

With long experience in Singapore, the company built Bencoolen and Mattar stations on the Downtown Line as well as Upper Thomson station on the TEL.

Resumption of work at T-5 of Changi Airport

After a gap of two years due to the pandemic, the construction of Changi Airport Terminal 5 (T5) in Singapore is back on track - this time with a new modular design and improved resilience and sustainability measures. The first phase of construction is expected to start around 2024, with T5 set to open in the mid-2020s. The new terminal will be built in the same land area as the existing Changi Airport (1,080ha) in Changi East. Designed to accommodate around 50 million passengers annually, T5 has the flexibility to build in two phases as traffic volumes increase. The additional capacity provided by T5 is expected to bolster Changi Airport's position as a regional and global hub.

The Changi Airport infrastructure comprises the passenger terminals, the runways, the taxiways, the maintenance buildings and services, and the ground support equipment. Changi Airport's four existing passenger terminals can accommodate 82 million passengers annually. Terminal 5 is expected to accommodate 50 million passengers annually upon completion.

Singapore Transportation Infrastructure Construction Industry Overview

The transport infrastructure construction market in Singapore is highly diversified, with several domestic and foreign players operating in the market. The market is expected to remain stable over the next few years due to the growing trend of government investment in the sector. Due to the large number of projects in the pipeline, there is always scope for new entrants into the market. Some of the key players in the market include Samsung C&T, Hyundai E&C, Daaelim Industrial, GS E&C, and Daewoo E&C, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increase In Tourism Industry

- 4.2.1.2 Sustainability and Environmental Concerns

- 4.2.2 Restraints

- 4.2.2.1 Financial Constraints

- 4.2.2.2 High Maintenance and Keep Up

- 4.2.3 Opportunities

- 4.2.3.1 Technological Advancements

- 4.2.1 Drivers

- 4.3 Value Chain / Supply Chain Analysis

- 4.4 Industry Policies and Regulations

- 4.5 Technological Developments in the Sector

- 4.6 Industry Attaractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers/Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Mode

- 5.1.1 Roadways

- 5.1.2 Railways

- 5.1.3 Airways

- 5.1.4 Ports and Inland Waterways

6 COMPETITIVE LANDSCAPE

- 6.1 Overview (Overall Market Share, Market Concentration and Major Players, and Companies' Comparison Analysis)

- 6.2 Company Profiles

- 6.2.1 Woh Hup Holdings Pte Ltd

- 6.2.2 Shimizu Corporation

- 6.2.3 Jurong Engineering Limited

- 6.2.4 Hyundai Engineering & Construction Co. Ltd.

- 6.2.5 Obayashi Singapore Private Limited

- 6.2.6 Koh Brothers Building & Civil Engineering Contractor Pte Ltd

- 6.2.7 Tiong Seng Group

- 6.2.8 Lum Chang Holdings Limited

- 6.2.9 Daelim Industrial Co Ltd

- 6.2.10 CSC Holdings Limited*

- 6.3 Other Companies (Overview/Key Information)

7 FUTURE OF SINGAPORE TRANSPORTATION INFRASTRUCTURE CONSTRUCTION MARKET

8 APPENDIX

9 DISCLAIMER

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日