|

市場調査レポート

商品コード

1644790

英国の決済-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)United Kingdom Payment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の決済-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

英国の決済市場規模は2025年に5,477億米ドルと推定され、予測期間(2025~2030年)のCAGRは11.6%で、2030年には9,481億2,000万米ドルに達すると予測されます。

英国の決済サービスは、Paypal、Samsung Pay、Mastercard、American Express、Shopifyなどのデジタル決済アプリケーションを採用し、決済の受付や送金を行う方向に急速にシフトしています。インターネット普及率の上昇やオンライン小売の急成長などの要因により、この動向は予測期間中も続くと予想されます。

主要ハイライト

- 顧客行動、購買動向、ニーズの変化に伴い、英国の決済市場は大きな変化を迎えています。英国の決済市場に影響を与える動向としては、キャッシュレス経済、モバイルバンキング、即時決済、デジタルコマース、規制機関の影響拡大などが挙げられます。また、電子決済に対する意識の高まりや、進化し続ける決済インフラの開発により、日常的な取引における電子決済の利用が促進されています。

- 英国の決済市場は力強い進化を遂げており、新たなプロバイダー、プラットフォーム、決済ツールがこの地域に導入されています。同地域におけるインターネットの利用拡大とスマートフォンの普及は、同国のデジタル決済市場を大きく牽引すると予想されます。デジタルギフトカードセグメントも世界的に急成長しているセグメントです。ギフトカードの需要が前四半期比で増加し続けているため、BNPL企業はこの機会を利用して英国での成長をさらに加速させようとしています。

- 同市場では、主要企業による合併、買収、投資が、顧客へのリーチと様々な用途への要求を満たすためのビジネスとそのプレゼンスを向上させる戦略の一環として確認されています。例えば、2022年7月、英国の銀行Virgin Moneyは、顧客が決済を数ヶ月に分散できる新しいクレジットカードの発売を宣言し、競争が激化するBNPL(Buy Now, Pay Later)セグメントに参入しました。また、2022年5月には、スウェーデンのBNPL会社TreydがシリーズAラウンドで約1,050万米ドルを調達しました。この資金調達により、同社は英国に進出し、ストックホルムとロンドンで事業を展開することになります。

- しかし、特に国境を越えた取引の場合、標準的な立法施策が確立されていないことが、予測期間を通じて市場全体の成長を制限しかねない大きな懸念事項となっています。

- パンデミック(世界的大流行)により、英国では非接触型決済の普及が加速しました。その結果、オンライン決済件数が増加し、デジタル決済手段の利用が増加しました。また、消費者や企業のニーズの変化に対応するため、新たな決済技術やソリューションが開発され、決済産業の技術革新が促進されました。

英国の決済市場の動向

カード決済が大きく成長

- デビットカードとクレジットカードは、国内で使用される主要な決済手段のひとつです。英国小売業協会(BRC)の2022年決済調査(BRC 2022 Payments Survey)の結果によると、デビットカードは英国で好まれる決済方法として地歩を固め続けており、2021年には小売取引全体の67.28%を占めることが明らかになりました。

- さらに、UK Financeの「Payment Markets Report」によると、デビットカードによる支払額は2032年までに270億円以上に増加すると予測されており、これは非接触型決済、オンラインショッピング、あらゆる規模の企業でカードが受け入れられつつあることなどが背景にあるようです。こうした新興国市場の開拓は、予測期間中の市場成長にプラスの影響を与えると分析されます。

- さらに、同市場では、顧客にリーチし、さまざまなアプリケーションの要件を満たすためのプレゼンスを向上させる事業戦略の一環として、主要企業によるさまざまな重要な製品の発表、合併、買収、投資が行われています。例えば、2023年2月、世界のオンラインファッション企業であるASOSとCapital One UKは、新たな独占的クレジットカード提携を発表しました。この提携により、2023年後半には、対象となる買い物客向けに新しいASOSクレジットカードが発行されます。このカードは、ASOSやその他の店舗で買い物をする際に、クレジットカードを利用することでしか得られない様々な特典や機能を記載しています。

- U.K. Financeによると、2021年7月時点の英国のクレジットカード口座数は約5,224万件であったが、2022年7月時点では約5,312万件となり、クレジットカード口座数は着実に増加しています。同国におけるクレジットカード口座数の増加は、予測期間を通じて同市場にさまざまな成長機会をもたらすと考えられます。

eコマースとMコマースの普及が決済市場を牽引する展望

- インターネットが普及し、スマートフォンの利用率が過去最高を記録している現在、モバイルコマースが普及し、eコマース市場の勢力図が変化しています。英国国家統計局(Office for National Statistics)によると、2022年12月現在、インターネットによる総売上高は、英国の小売売上高のほぼ25%を占めています。

- COVID-19パンデミック時の政府規制は、世界中の多くの産業の操業停止につながりました。この大規模な操業停止により、顧客はeコマース・ウェブサイトでのショッピングや小売に切り替えることを余儀なくされ、Buy Now Pay Later決済オプションの利用が増加しました。Worldpayによると、Buy Now Pay Later(BNPL)は2021年の6.2%から2025年には12.1%と、eコマース決済におけるシェアがほぼ倍増すると予想されています。

- さらに、国内でのモバイルショッピングの成長により、eウォレットの利用が徐々に増加しています。eウォレットの利用はカードの2倍のスピードで伸びており、Paypalがその先頭を走っています。オンラインショッピング利用者が他の欧州諸国との国境を越えたショッピングを好むようになり、英国でのeWalletの採用はさらに加速すると予想されます。

- Airnowによると、2022年9月現在、グレートブリテン(GB)のGoogle PlayストアでトップのショッピングアプリはASDAリワードで、調査期間中に52万ダウンロードを超えました。2位はVintedで、英国のGoogle Playユーザーによるダウンロード数は約25万8,000件でした。したがって、英国のGoogle Playストアにおけるショッピングアプリの総ダウンロード数の増加に伴い、予測期間を通じて同市場はかなりの成長機会を目の当たりにすると予想されます。

英国の決済産業概要

英国の決済市場は、少数の参入企業が大きなシェアを占めているため、統合されているように見えます。英国の決済市場の主要企業は、より多くの地域の消費者にリーチを広げるため、買収や提携を採用しています。決済市場の主要企業には、Paypal、Stripe、Amazon Pay、Mastercard Inc.、Sage Payなどがあります。

2023年10月、ユーザーのクレジットカードとデビットカードを1枚のカードとアプリに統合する金融スーパーアプリ「Curve」が、英国で初めてクレジットカードを発行しました。新しく登場したクレジットカードは、Curveのすべての機能を備え、より高い柔軟性と安全性を備えています。顧客は既存のカードをデジタルのカーブウォレットにリンクさせることができ、アプリで選択したカードがクレジットカードで決済される際に課金されます。

2023年7月、AIを活用した世界決済ネットワークであるKlarnaは、英国の百貨店Libertyと提携し、無利息決済オプションを提供しました。この提携により、リバティの顧客はKlarnaの無利息決済オプションを使ってスマートに買い物ができ、Klarnaアプリで支出を管理できるようになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業利害関係者分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 国内における決済環境の進化

- 国内におけるキャッシュレス取引の拡大に関連する主要市場動向

- COVID-19が同国の決済市場に与える影響

第5章 市場力学

- 市場促進要因

- 購買力の増加に支えられたmコマースや越境ECの台頭を含むeコマースの高い普及率

- 市場のデジタル化を促進する主要小売企業と政府による支援プログラム

- リアルタイム決済、特に国内におけるBuy Now Pay Laterの成長

- 市場課題

- 特に国境を越えた取引の場合、標準的な立法施策の欠如が残る。

- 市場機会

- キャッシュレス社会への移行

- 新規参入企業によるイノベーションが普及を促進する

- デジタル決済産業における主要規制と基準

- 主要事例と使用事例の分析

- 英国の決済産業に関する主要な人口動向とパターンの分析(人口、インターネット普及率、銀行普及率/非銀行人口、年齢・所得などを含む)

- 英国における顧客満足度重視の高まりと世界の動向の融合に関する分析

- 英国における現金離れと非接触型決済モードの台頭に関する分析

第6章 市場セグメンテーション

- 決済モード別

- 販売時点情報管理(POS)

- カード決済(デビットカード、クレジットカード、銀行融資プリペイドカードを含む)

- デジタルウォレット(モバイルウォレットを含む)

- 現金

- その他

- オンライン販売

- カード決済(デビットカード、クレジットカード、銀行融資プリペイドカードを含む)

- デジタルウォレット(モバイルウォレットを含む)

- その他(代金引換、銀行振込、Buy Now, Pay Laterを含む)

- 販売時点情報管理(POS)

- エンドユーザー産業別

- 小売

- エンターテインメント

- 医療

- ホスピタリティ

- その他

第7章 競合情勢

- 企業プロファイル

- PayPal Payments Private Limited

- Stripe, Inc.

- Worldpay, Inc.

- Amazon Payments, Inc

- Mastercard, Inc.

- PayPoint plc.

- 2Checkout.com, Inc.

- Visa, Inc

- Klarna Inc.

- SumUp Inc.

第8章 投資分析

第9章 市場の将来展望

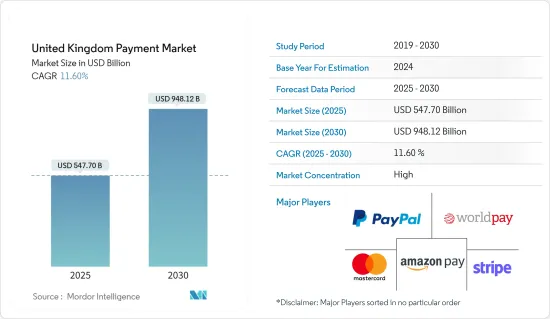

The United Kingdom Payment Market size is estimated at USD 547.70 billion in 2025, and is expected to reach USD 948.12 billion by 2030, at a CAGR of 11.6% during the forecast period (2025-2030).

The payment services in the United Kingdom are rapidly shifting towards adopting digital payment applications, such as Paypal, Samsung Pay, Mastercard, American Express, and Shopify, to accept and transfer payments. With factors like increasing internet penetration and rapid growth in online retailing, this trend is expected to continue over the forecast period.

Key Highlights

- As per the changes in customer behavior, buying trends, and needs, the payments market in the United Kingdom is witnessing significant changes. A few trends influencing the payments market in the United Kingdom are cashless economies, mobile banking, instant payments, digital commerce, and the growing impact of regulatory agencies. Moreover, increased awareness of electronic payments and continuously developing evolving payment infrastructure have successfully facilitated using electronic payment methods for day-to-day transactions.

- The payment market in the United Kingdom has recorded strong evolution, with new providers, platforms, and payment tools being introduced in the region. The increased usage of the internet and smartphone penetration in the region is anticipated to drive the digital payments market in the studied country significantly. The digital gift card segment is another fast-growing vertical globally. As the demand for gift cards continues to rise quarter-on-quarter, BNPL firms are looking to capitalize on the opportunity to further accelerate their growth in the United Kingdom.

- The market is witnessing mergers, acquisitions, and investments by key players as part of its strategy to improve business and their presence to reach customers and meet their requirements for various applications. For instance, In July 2022, British bank Virgin Money declared the launch of a new credit card that would enable customers to spread their payments over several months, entering the increasingly competitive buy now, pay later (BNPL) space. Also, in May 2022, Swedish buy now, pay later (BNPL) firm Treyd raised a sum of around USD 10.5 million in a Series A round. The funding would help the company expand to the U.K. and operate out of Stockholm and London.

- However, the lack of a standard legislative policy remains, especially in the case of cross-border transactions could be a major matter of concern that can limit the overall market's growth throughout the forecast period.

- The pandemic boosted the adoption of contactless payments in the U.K. With the closure of physical stores during lockdowns, consumers turned to online shopping, driving a significant increase in e-commerce transactions. This led to an increase in online payment volumes and a rise in the use of digital payment methods. Also, it has driven innovation in the payment industry, with new payment technologies and solutions being developed to meet the changing needs of consumers and businesses.

UK Payment Market Trends

Card Payments to Witness Significant Growth

- Debit and Credit cards are one of the primary payment methods used within the country. As per payments, card payments now account for nearly 90% of all retail transactions in the U.K. According to the findings from the British Retail Consortium's (BRC) 2022 Payments Survey, it has revealed that debit cards have continued to gain ground as the preferred payment method in the U.K., accounting for 67.28% of all retail transactions in 2021.

- Further, according to UK Finance's Payment Markets Report, forecasted debit card payment volumes will increase to over 27 billion by 2032, likely driven by contactless payments, online shopping, and the ever-increasing levels of card acceptance among businesses of all sizes. Such developments are analyzed to positively influence the market growth over the forecast period.

- Moreover, the market is witnessing various significant product launches, mergers, acquisitions, and investments by key players as part of its business strategy to improve its presence to reach customers and meet their requirements for various applications. For instance, in February 2023, ASOS, the global online fashion firm, and Capital One UK announced a new and exclusive credit card partnership. The partnership will launch a new ASOS credit card for eligible shoppers, available later in 2023. It will provide a range of benefits and features that only come with using a credit card when they shop at ASOS and elsewhere.

- According to U.K. Finance, as of July 2021, there were approximately 52.24 million credit card accounts in the U.K., whereas as of July 2022, there was approximately 53.12 million credit card accounts in the U.K., representing a steady increase in the overall count of credit card accounts. This rise in the overall number of credit card accounts within the country will provide the market with various growth opportunities throughout the forecast period.

E-commerce and Rising Adoption of M-commerce is Expected to Drive the Payments Market

- In the age of the internet, and during a time when smartphone usage is reaching all-time highs, mobile commerce has gained traction and thus changed dynamics within e-commerce along the way. As per the Office for National Statistics (UK), as of December 2022, total internet sales accounted for almost 25% of all retail sales in Great Britain.

- The government regulations during the COVID-19 pandemic led to the shutdown of many industries worldwide. The major shutdown compelled customers to switch to e-commerce websites for shopping and retailing, which increased the usage of the Buy Now Pay Later payment option. According to Worldpay, Buy Now Pay Later (BNPL) is expected to nearly double its share of e-com payments, from 6.2% in 2021 to 12.1% by 2025.

- Moreover, the growth of mobile shopping in the country is gradually increasing the usage of eWallets. eWallet utilization is growing at twice the speed of cards, with PayPal leading the way. The adoption of eWallets in the UK is expected to accelerate even more as online shoppers prefer cross-border shopping with the rest of Europe.

- As per Airnow, as of September 2022, the leading shopping app in the Google Play Store in Great Britain (GB) was ASDA Rewards, with over 520 thousand downloads in the examined period. Vinted ranked second, with roughly 258 thousand downloads by Google Play users in Great Britain. Hence, with the rise in the total number of downloads of shopping apps in the Google Play Store in Great Britain, the market is expected to witness considerable growth opportunities throughout the forecast period.

UK Payment Industry Overview

The United Kingdom payments market appears to be consolidated owing to the few of the players holding significant share in the market. Major players in the United Kingdom payments market are adopting acquisitions and partnerships to expand their reach to more regional consumers. Some major payment market companies are Paypal, Stripe, Amazon Pay, Mastercard Inc., and Sage Pay.

In October 2023, the Financial super app Curve, which consolidates users' credit and debit cards into one card and app, launched its first-ever credit card in the United Kingdom. The newly launched credit card has all the features of Curve, supercharged with greater flexibility and security. Customers can link their existing cards to a digital Curve Wallet, and whichever card they select in the app is charged when they use their credit card to pay.

In July 2023, Klarna, the AI-powered global payments network, collaborated with British department store Liberty to offer its interest-free payment options. The collaboration will enable Liberty's customers to shop smarter with Klarna's interest-free payment options and manage their spending through the Klarna app.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness-Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Evolution of the payments landscape in the country

- 4.5 Key market trends pertaining to the growth of cashless transaction in the country

- 4.6 Impact of COVID-19 on the payments market in the country

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Proliferation of E-commerce, including the rise of m-commerce and cross-border e-commerce supported by the increase in purchasing power

- 5.1.2 Enablement Programs by Key Retailers and Government encouraging digitization of the market

- 5.1.3 Growth of Real-time Payments, especially Buy Now Pay Later in the country

- 5.2 Market Challenges

- 5.2.1 Lack of a standard legislative policy remains especially in the case of cross-border transactions

- 5.3 Market Opportunities

- 5.3.1 Move towards Cashless Society

- 5.3.2 New Entrants to Drive Innovation Leading to Higher Adoption

- 5.4 Key Regulations and Standards in the Digital Payments Industry

- 5.5 Analysis of major case studies and use-cases

- 5.6 Analysis of key demographic trends and patterns related to payments industry in the United Kingdom (Coverage to include Population, Internet Penetration, Banking Penetration/Unbanking Population, Age & Income etc.)

- 5.7 Analysis of the increasing emphasis on customer satisfaction and convergence of global trends in the United Kingdom

- 5.8 Analysis of cash displacement and rise of contactless payment modes in the United Kingdom

6 MARKET SEGMENTATION

- 6.1 By Mode of Payment

- 6.1.1 Point of Sale

- 6.1.1.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.1.2 Digital Wallet (includes Mobile Wallets)

- 6.1.1.3 Cash

- 6.1.1.4 Others

- 6.1.2 Online Sale

- 6.1.2.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.2.2 Digital Wallet (includes Mobile Wallets)

- 6.1.2.3 Others (includes Cash on Delivery, Bank Transfer, and Buy Now, Pay Later)

- 6.1.1 Point of Sale

- 6.2 By End-user Industry

- 6.2.1 Retail

- 6.2.2 Entertainment

- 6.2.3 Healthcare

- 6.2.4 Hospitality

- 6.2.5 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 PayPal Payments Private Limited

- 7.1.2 Stripe, Inc.

- 7.1.3 Worldpay, Inc.

- 7.1.4 Amazon Payments, Inc

- 7.1.5 Mastercard, Inc.

- 7.1.6 PayPoint plc.

- 7.1.7 2Checkout.com, Inc.

- 7.1.8 Visa, Inc

- 7.1.9 Klarna Inc.

- 7.1.10 SumUp Inc.