|

市場調査レポート

商品コード

1644573

中国のeコマース:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)China E-commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のeコマース:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

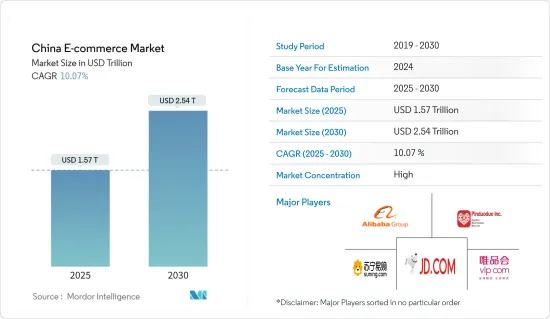

中国のeコマース市場規模は2025年に1兆5,700億米ドルと推定され、予測期間(2025~2030年)のCAGRは10.07%で、2030年には2兆5,400億米ドルに達すると予測されます。

主要ハイライト

- 同地域のeコマース市場の成長を促す主要要因は、スマートフォン主導のMコマース文化、革新的なデジタル決済システム、ライブコマースプラットフォームの台頭などです。

- 膨大な人口を抱える中国のeコマース市場は世界最大です。中国のeコマース市場は過去数年間に急速に発展したが、これは主にインターネットとスマートフォンの普及率の高さ、オンラインショッピングに対する消費者の信頼感の高まり、eコマースプラットフォームの出現、さまざまな代替決済ソリューションが原動力となっています。

- 代替決済ソリューションは、eコマース購入増加の主要受益者でした。AlipayやWeChatペイなどの決済ソリューションは、eコマースプラットフォームで急速に成長しています。Alipayは、Alibaba・グループが所有するすべてのeコマースプラットフォームにおける主要な決済ツールです。一方、Tencentが提供するWeChat Payは、その巨大なソーシャルメディアユーザー基盤を活用してオンライン決済を推進しています。中国の顧客がeコマースを受け入れ続けるにつれて、これらの決済ソリューションは勢いを増すと予想されます。

- 不便で、しばしば対立する対面ショッピングの文化が、この地域の買い物客にeコマースプラットフォームの分かりやすい信頼性を受け入れる動機付けとなりました。また、オンライン注文の返品や返金の確保など、さまざまなショッピング活動で簡単に利用できます。さらに、中国の数百万人の出稼ぎ労働者が提供する低コストの配送サービスにより、JD.comやAlibaba・グループのような企業は、国内どこでも即日配送を可能にしています。

- 支援的な施策が存在する一方で、eコマース・参入企業は引き続き規制上のハードルに直面しています。特に、データのローカライゼーションと個人データ保護に関する厳しい規制は、市場への参入を計画している非中国企業にとって課題となっています。中国共産党(CCP)は、一連のデジタル施策として「グレート・ファイアウォール・オブ・チャイナ」を提唱しています。中国共産党は独自の消費者データ法、特に個人情報保護法とデータセキュリティ法を導入しました。これらの規制は、中国市場への参入を目指す米国企業に課題を突きつけています。

- COVID-19の大流行は、農村部でもオンラインショッピングの売上を押し上げ、政府は開発が遅れている地域のデジタルインフラの改善に投資しました。パンデミック後は、食料品、健康食品、家庭用品など、以前はファッションや電子機器カテゴリーが中心だったeコマースカテゴリーの数が増加しました。

中国のeコマース市場動向

B2B eコマースの成長が期待される

- 中国企業は業務の合理化と効率化のためにデジタルソリューションを採用する傾向を強めており、B2B eコマースプラットフォームの需要が加速しています。加えて、中国政府は好意的な施策やイニシアティブを通じて、デジタル化とeコマースの成長を積極的に推進しています。

- 中国はさまざまな要因に後押しされ、世界のeコマースのリーダーとして台頭してきました。14億人を超える人口を抱える中国は、製品やサービスのオンライン購入に熱心な膨大な消費者層を擁しています。そのため、B2B eコマースプラットフォームは、企業が売上を伸ばし、サプライチェーンを最適化し、コストを削減し、透明性を向上させるのに役立っています。市場の参入企業は、広告エクスペリエンスの向上をサポートし、販売者が収益ベースの融資に素早くアクセスできるビジネスキャッシングを提供することで、販売者を支援しています。

- 主要なB2Bプラットフォームは、融資、ロジスティクス、マーケティングなどのサービスを提供するエコシステムを拡大し、ビジネス向けのワンストップソリューションを構築しています。さらに、中国のB2Bプラットフォームが国境を越えた取引を促進し、企業が国際市場をより容易に利用できるようにする動向も高まっています。中国インターネット・ネットワーク情報センターのデータによると、中国のオンライン買い物客の数は、2022年の8億4,529万人から2023年には9億1,496万人に増加しました。企業は数量を増やすために、B2Bプラットフォームからの支援を必要としています。

- 中小企業は、従来のオフラインの流通チャネルからオンラインプラットフォームへと販売やサービスを移行しています。このようにオンラインとオフラインのチャネルが融合することで、各セグメントで課題が生じる一方で、オンラインショッピングにおける顧客の嗜好の変化に対応する大きな機会も生まれています。そのため、中小企業はB2Bのeコマースプラットフォームを活用することで、事業範囲を拡大し、より大規模な競争に打ち勝つ傾向が強まっています。

- B2B企業がB2Cでのショッピング体験を重視するようになるにつれ、柔軟で相互運用可能なeコマース・アーキテクチャの必要性が最も重要になっています。B2BとB2Cの両方でビッグデータの重要性が急増しています。多国籍企業(MNC)は膨大なデータプールを活用し、対象顧客に焦点を当て、パーソナライズされた体験を作り、ロケーションベースのサービスを提供し、多様な市場で競合分析を実施しています。

ファッションとアパレルが最大のシェアを占める

- 技術とデジタル革新は、中国のファッションeコマースの展望を再構築しています。市場の拡大に伴い、企業は進化する消費者の嗜好に合わせるため、新しい技術を迅速に導入しています。このシフトには、オンライン小売サイトの技術統合、優れた顧客体験のためのデジタル変革の活用、シームレスなコマース・エコシステムの構築などが含まれます。中国商務部の発表によると、2023年のオンライン小売売上高の22%は、衣料品、フットウェア、繊維製品のカテゴリーが占めています。

- オンラインショッピングの人気の高まりは、中国におけるモバイルインターネットの高い普及率とインターネットのアクセシビリティとスピードに支えられ、この地域におけるオンライン買い物客の増加をもたらしました。AI、AR、VRイノベーションに投資する市場参入企業は、オンラインショッピング体験を強化し、消費者がバーチャルで服を視覚化し、試着することを容易にしています。

- 2024年6月、中国の大手ファストファッションブランドであるSheinは、Ntx Groupとの戦略的パートナーシップを発表しました。この提携は、先進的人工知能(AI)技術を統合することで、Sheinのデザインと生産ワークフローに革命を起こすことを目的としています。NtxのAI主導の手法を活用することで、Sheinは市場投入までの時間を大幅に短縮することを目指しています。これにより、Sheinはわずか7日以内にeコマースプラットフォームに新しいファッション・アイテムを導入し、5日以内に商品を確実に届けることができます。

- ライブ・ストリーミングは中国におけるeコマースの一般的な形態であり、主要なオピニオン・リーダーが自身のライブ・ビデオ放送を行っています。同時に、視聴者にさまざまな商品や製品を売り込みます。ライブストリーミングeコマースの最も大きな利点は、全国各地、特に大都市以外の多くの人々にリーチできることです。ライブストリーミングをより農村部や低層都市を対象にすることで、企業はブランド認知度を高め、視聴者を中国全土に拡大することができます。

- 同地域では、スマートフォン主導のMコマースや、同地域のさまざまな市場参入企業が提供する革新的なデジタル決済ソリューションの台頭に支えられ、オンラインショッピングの普及率が上昇しました。例えば、中国国家統計局が報告しているように、中国の消費財産業は2023年に約6兆6,400億米ドル(47兆1,000億人民元)の小売総売上高を記録し、同国のeコマース市場の成長を牽引しています。

中国のeコマース産業概要

中国のeコマース市場は統合されており、以下のような大手企業が存在します。 Alibaba Group, JD.com, and Pinduoduo Inc. これらの市場参入企業は市場の大きなシェアを占めています。地域企業は、新しい決済システムの導入や戦略的提携や買収を通じて、市場での存在感を高めています。

- 2024年6月、eコマースの世界的リーダーであり小売業者でもあるJD.comは、世界的ファッション企業であるInditexとの戦略的提携を発表しました。この提携は、Inditexの有名ファッションブランドMassimo Duttiの旗艦店をJD.comのプラットフォームで立ち上げることを目的としています。Inditexのこの動きは、中国の広範なデジタル消費者層を取り込むことを目的としています。この店舗では、アパレル、アクセサリー、JDの顧客向けに作られた限定商品など、約1,000アイテムを含む幅広い商品を展示しています。

- 2024年5月、フランスの高級コングロマリットであるLVMHは、Alibabaとの協業を強化し、その先進的なクラウドと人工知能の能力を活用しました。この動きは、中国市場におけるLVMHの足跡を強化することを目的としています。この提携は、オンラインショッピング体験の強化に重点を置くと同時に、ますます洗練された実店舗への投資に重点を置いた。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 主要市場動向と小売業全体に占めるeコマースのシェア

- COVID-19がeコマース売上に与える影響

第5章 市場力学

- 市場促進要因

- 市場を牽引するライブストリームeコマース

- オンラインショッピングの普及がeコマース市場を押し上げる

- 市場課題

- 現地のeコマース法と知的財産権執行に関する課題

- 中国のeコマース産業に関する主要な人口動向とパターンの分析(人口、インターネット普及率、eコマース普及率、年齢・所得などを含む範囲)

- 中国のeコマース産業における主要取引形態の分析(現金、カード、銀行振込、ウォレットなどの一般的な決済手段を含みます。)

- 中国における越境eコマース産業の分析(越境の現在の市場規模と主要動向)

- アジア太平洋のeコマース産業における中国の現在の位置づけ

第6章 市場セグメンテーション

- B2C eコマース別

- 市場セグメンテーション-用途別

- 美容・パーソナルケア

- 民生用電子機器

- ファッション・アパレル

- 飲食品

- 家具と家庭

- その他(玩具、DIY、メディアなど)

- 市場セグメンテーション-用途別

- B2B eコマース別

第7章 競合情勢

- 企業プロファイル

- JD.com

- Alibaba.com

- Pinduoduo Inc

- Suning.com

- Vipshop Holdings Ltd

- Xiaohongshu(Little Red Book)

- JuMei.com

- Yihaodian

- Dangdang Inc.

- Mogujie

第8章 投資分析

第9章 市場の将来展望

The China E-commerce Market size is estimated at USD 1.57 trillion in 2025, and is expected to reach USD 2.54 trillion by 2030, at a CAGR of 10.07% during the forecast period (2025-2030).

Key Highlights

- The primary factors driving the growth of the e-commerce market in the region are smartphone-driven m-commerce culture, innovative digital payment systems, and rising live-commerce platforms, among others.

- With a vast population, the Chinese e-commerce market is the world's largest. The Chinese E-commerce market evolved rapidly during the past few years, primarily driven by high Internet and smartphone penetration, increased consumer confidence in online shopping, the emergence of e-commerce platforms, and various alternative payment solutions.

- Alternative payment solutions were the primary beneficiary of rising e-commerce purchases. Payment solutions such as Alipay and WeChat Pay are rapidly growing for e-commerce platforms. Alipay is a primary payment tool on all the e-commerce platforms owned by the Alibaba Group. On the other hand, WeChat Pay, which is offered by Tencent, leverages its massive social media user base to push online payments. As Chinese customers continue to embrace e-commerce, these payment solutions are expected to gain momentum.

- An inconvenient and often confrontational in-person shopping culture helped motivate shoppers in the region to embrace the straightforward reliability of e-commerce platforms. Also, they are easy to use in various shopping activities for making returns and securing refunds for online orders. Moreover, the low-cost delivery services provided by China's millions of migrant laborers enable companies like JD.com and Alibaba Group to provide same-day delivery anywhere in the country.

- While supportive policies exist, e-commerce players continue to face regulatory hurdles. Notably, strict regulations on data localization and personal data protection pose challenges, especially for non-Chinese companies planning to enter the market. The "Great Firewall of China" is described by the Chinese Communist Party (CCP) as a series of digital policies. The CCP introduced its own consumer data laws, notably the Personal Information Protection Law and Data Security Law. These regulations pose challenges for US firms looking to enter the Chinese market.

- The COVID-19 pandemic drove online shopping sales, even in rural areas, with the government investing in improving digital infrastructure in less developed regions. Post-pandemic, the number of e-commerce categories, such as groceries, health products, and home essentials, grew, which were previously dominated by the fashion and electronic categories.

China E-commerce Market Trends

B2B E-commerce is Expected to Witness Growth

- Chinese businesses are increasingly adopting digital solutions to streamline operations and improve efficiency, accelerating the demand for B2B e-commerce platforms. Additionally, the Chinese government is actively promoting digitalization and the growth of e-commerce through favorable policies and initiatives.

- China has risen as a global e-commerce leader, propelled by various factors. With a population surpassing 1.4 billion, the nation presents a vast consumer base keen on purchasing products and services online. Thus, B2B e-commerce platforms help businesses grow sales, optimize their supply chains, reduce costs, and improve transparency. Market players help sellers by supporting them in improving their advertising experience and providing business cash advances that can give sellers quick access to revenue-based loans.

- Major B2B platforms are expanding their ecosystems to offer services, including financing, logistics, and marketing, creating one-stop solutions for businesses. Moreover, there is a growing trend of Chinese B2B platforms facilitating cross-border transactions, helping businesses tap into international markets more easily. As per the data from the China Internet Network Information Center, the number of online shoppers in China rose to 914.96 million in 2023 from 845.29 million in 2022. Businesses require assistance from B2B platforms to increase sales volume.

- Small and medium-sized enterprises (SMEs) are shifting from conventional offline sales channels to online platforms for their sales and services. This blending of online and offline channels presents challenges across sectors but also opens up significant opportunities to cater to evolving customer preferences in online shopping. Thus, SMEs are increasingly leveraging B2B e-commerce platforms to expand their reach and compete on a larger scale.

- As B2B companies increasingly focus on B2C shopping experiences, the need for flexible, interoperable e-commerce architecture becomes paramount. The significance of Big Data in both B2B and B2C is surging. Multinational corporations (MNCs) leverage vast data pools to focus on their target customers, craft personalized experiences, deliver location-based services, and conduct competitor analyses across diverse markets.

Fashion and Apparel Hold the Largest Share

- Technology and digital innovation are reshaping China's fashion e-commerce landscape. With the market expanding, businesses are swiftly adopting new tech to align with evolving consumer tastes. This shift involves tech integration on online retail sites, leveraging digital transformations for superior customer experiences, and crafting a seamless commerce ecosystem. As per the Ministry of Commerce China, the clothing, footwear, and textiles categories contributed to 22% of online retail sales revenue in 2023.

- The rising popularity of online shopping has resulted in an increase in the number of online shoppers in the region, supported by high mobile internet penetration and the accessibility and speed of the Internet in China. Market players investing in AI, AR, and VR innovations are enhancing the online shopping experience, making it easier for consumers to visualize and try on clothes virtually.

- In June 2024, Shein, a leading Chinese fast-fashion brand, announced a strategic partnership with Ntx Group. The collaboration aims to revolutionize Shein's design and production workflows by integrating advanced artificial intelligence (AI) technologies. By harnessing Ntx's AI-driven methodologies, Shein aims to significantly reduce its time-to-market. Through this, Shein can introduce new fashion items to its e-commerce platform within just seven days and ensure product delivery within five days, which is faster than traditional design and production methods.

- Live streaming is a prevalent form of e-commerce in China, where key opinion leaders conduct live video broadcasts of themselves. At the same time, they market different goods and products to their audiences. The most significant advantage of live-streaming e-commerce is its ability to reach many people spread throughout the country, especially those outside of major cities. By targeting live streams in more rural areas and lower-tier cities, companies can increase brand awareness and expand their audience to all parts of China.

- Online shopping penetration increased in the region, supported by the rise of smartphone-driven m-commerce and innovative digital payment solutions offered by various market players in the area. For instance, as reported by the National Bureau of Statistics of China, China's consumer goods industry recorded total retail sales of around USD 6.64 trillion (CNY 47.1 trillion) in 2023, driving the growth of the e-commerce market in the country.

China E-commerce Industry Overview

The Chinese e-commerce market is consolidated, with the presence of major players such as Alibaba Group, JD.com, and Pinduoduo Inc. These market players hold a significant share of the market. The regional companies are increasing their market presence by introducing new payment systems and entering into strategic partnerships or acquisitions.

- June 2024: JD.com, a global e-commerce leader and retailer, unveiled a strategic alliance with Inditex, a player in global fashion. This collaboration aims to launch the flagship store for Inditex's renowned fashion label, Massimo Dutti, on JD.com's platform. This move by Inditex aims to tap into China's expansive digital consumer base. The store showcases an extensive range of products, including nearly 1,000 items, across apparel, accessories, and exclusive offerings tailored for JD's clientele.

- May 2024: The French luxury conglomerate LVMH enhanced its collaboration with Alibaba, tapping into its advanced cloud and artificial intelligence capabilities. This move aimed to bolster LVMH's footprint in the Chinese market. The alliance focused on enhancing their online shopping experiences while simultaneously investing in increasingly sophisticated brick-and-mortar retail outlets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Defination

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Key Market Trends and Share of E-commerce of Total Retail Sector

- 4.4 Impact of COVID-19 on the E-commerce Sales

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Livestream E-commerce to drive the Market

- 5.1.2 Growing Penetration of Online Shoppers to Boost the E-commerce Market

- 5.2 Market Challenges

- 5.2.1 Challenges Related to Local E-commerce Law and Intellectual Property Enforcement

- 5.3 Analysis of Key Demographic Trends and Patterns Related to E-commerce Industry in China (Coverage to Include Population, Internet Penetration, E-commerce Penetration, Age & Income etc.)

- 5.4 Analysis of the Key Modes of Transaction in the E-commerce Industry in China (Coverage to Include Prevalent Modes of Payment Such as Cash, Card, Bank Transfer, Wallets, etc.)

- 5.5 Analysis of Cross-Border E-commerce Industry in China (Current Market Value of Cross-border & Key Trends)

- 5.6 Current Positioning of China in the E-commerce Industry in Asia Pacific

6 MARKET SEGMENTATION

- 6.1 By B2C E-commerce

- 6.1.1 Market Segmentation - by Application

- 6.1.1.1 Beauty and Personal Care

- 6.1.1.2 Consumer Electronics

- 6.1.1.3 Fashion and Apparel

- 6.1.1.4 Food and Beverages

- 6.1.1.5 Furniture and Home

- 6.1.1.6 Others (Toys, DIY, Media, etc.)

- 6.1.1 Market Segmentation - by Application

- 6.2 By B2B E-commerce

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 JD.com

- 7.1.2 Alibaba.com

- 7.1.3 Pinduoduo Inc

- 7.1.4 Suning.com

- 7.1.5 Vipshop Holdings Ltd

- 7.1.6 Xiaohongshu (Little Red Book)

- 7.1.7 JuMei.com

- 7.1.8 Yihaodian

- 7.1.9 Dangdang Inc.

- 7.1.10 Mogujie