|

市場調査レポート

商品コード

1644565

フィリピンのeコマース:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Philippines E-commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フィリピンのeコマース:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

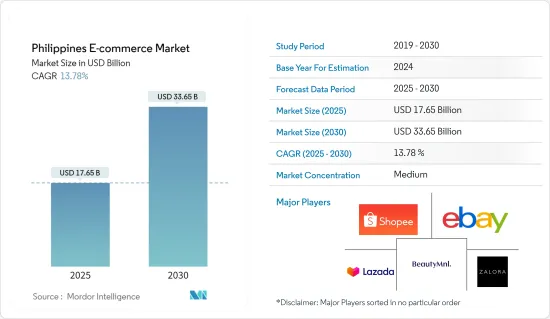

フィリピンのeコマース市場規模は2025年に176億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは13.78%で、2030年には336億5,000万米ドルに達すると予測されています。

商品やサービスのオンライン購入・販売はeコマースとして知られています。アフィリエイト・マーケティング戦略もeコマース企業の定義に含まれる可能性があります。オンライン販売を拡大するために、ユーザーは自社サイトやアマゾンのような有名小売業者、ソーシャルメディアなどのeコマース・プラットフォームを活用することができます。

主なハイライト

- 好調な経済とデジタルに精通した人々が多いことから、フィリピンは東南アジアで最も急成長しているeコマース市場のひとつです。多くのウェブサイトやデジタル・アプリケーションが、地元、地域、そして世界のライバルを相手に市場シェア獲得にしのぎを削っています。フィリピンでは接続性が向上し、インフラが整備されているため、フィリピンの人口の大部分がインターネットに接続できるようになっています。フィリピンのインターネット接続人口は通常、コンピュータやモバイル機器を通じて国内のeコマース市場にアクセスしています。

- オンライン小売の最大の動向のひとつは、プラットフォームの融合です。顧客は、商品の評価や価格、購入、プラットフォームの新しいオンライン決済オプションを利用した支払いなど、オールインワンのショッピング体験を好みます。その結果、ポータルサイト、ソーシャルメディア、テレビ通販、オーバー・ザ・トップ・メディア・サービス(OTT)などでオンラインショッピング機能が利用できるようになった。その結果、各社のプラットフォームは人気を集めています。

- 無線技術とインターネット技術の急速な開発は、オンライン小売とeコマースの進歩に大きな影響を与えています。スマート・デバイスの利用しやすさ、通信インフラの進歩、購買力の上昇、時間の不足、利便性の向上により、企業はテクノロジーを導入し、顧客の拡大するニーズに対応せざるを得なくなり、オンライン食品注文という新たなビジネス・モデルの開発が加速しています。

- 急速な発展にもかかわらず、フィリピンではまだ、経営とテクノロジーをより多くの人々が利用できるようにはなっていないです。eコマースの進歩も、国のテクノロジーとインターネット部門を促進するためのインフラ構想を定めていない政府高官や地元組織の不作為によって遅れています。この地域のトラフィックの増加に対応するため、国内の通信事業者や政府はインターネットの速度を向上させる必要があります。

- フィリピンのeコマースにとって転機となったのはCOVID-19の大流行でした。この流行は、閉鎖と移動制限をもたらし、需要を記録的な高水準に押し上げ、オンラインマーケットプレースに新たな買い手と売り手を引きつけ、プレーヤーに長期的な発展をもたらしました。eコマース業界は、消費者にオンライン・ショッピングの利便性を認識させ、オンライン・ショッピングに慣れている消費者に追加購入を促した封じ込め努力の結果、流行から大きな恩恵を受けました。

フィリピンeコマース市場動向

市場を大きく支配するファッション業界

- COVID-19が流行する前は、フィリピン人はオンラインで金銭的な約束をすることをためらっていました。そのため、フィリピン人は食料品やその他の必需品をオンラインで購入せざるを得なくなり、eコマース取引数が急増しました。何千ものフィリピン人ビジネス・オーナーが急速に追いつき、フェイスマスクから電子消費財まで、あらゆるものを提供するオンライン・ストアをオープンしました。ファッションや化粧品の分野では、著名な企業もeコマース活動を活発化させました。

- 東南アジアの近隣諸国とともに、フィリピンのeコマース環境は絶えず拡大し、変化しています。ファッション小売業界において、モールの実店舗は常に重要な経済パラダイムであったが、パンデミックはこれを完全に変えてしまいました。

- フィリピンはここ数年、新しいファッション関連企業の進出を奨励しています。そのため、国内では新しいブランドによるeコマース市場を活用し、卸売業、小売業ともに市場は成長を続けています。

- フィリピンのeコマースは、オンライン消費者の間で人気が急上昇しています。これらのプラットフォームは、幅広い品揃えを提供するだけでなく、競争力のある価格設定を誇っています。その結果、eコマース市場は大きな成長軌道に乗り、2030年まで続くと予測されています。特に、Shopeeは月間7,000万人以上のウェブ訪問者を集めてトップに立ち、次いでLazadaが毎月約3,700万人の訪問者を集めています。Meltwaterによる洞察によると、2023年第3四半期に、フィリピン人回答者の57%が毎週オンラインで買い物をすると回答し、その中でも食料品のオンラインショッピングを選ぶ人が目立った。

- さらに、可処分所得の増加と贅沢な出費により、ファッション業界における消費者の需要はより複雑で多様になっています。その他の活動には、レジャーや文化活動といった生活を豊かにする消費の増加、インターネット販売の増加、高齢化、消費者の中心層の変化などがあります。

インターネット利用の増加、オンライン決済、携帯電話が市場を牽引

- フィリピンのeコマース市場は、まだまだ拡大・発展の余地があります。フィリピンの消費者がデジタル・ライフスタイルを採用することが、その大きな原動力となっています。世界銀行によると、フィリピンは東アジア太平洋地域で最もダイナミックな経済のひとつです。2023年、フィリピンは東南アジアで最も急速に成長する経済国として浮上し、政府の野心的な目標である6.0~7.0%をわずかに下回る5.6%の成長率を誇る。このデータはIMFの2024年経済予測から引用しました。

- 同国は、5Gとインターネット・サービスの急速な開発を目の当たりにしています。2023年、グローブ・テレコムは5Gインフラを大幅に強化し、新たに894のサイトを導入しました。この拡大により、首都圏では97.90%、ビサヤとミンダナオにまたがる主要都市では92.36%という卓越した屋外カバレッジを実現しました。

- フィリピンはデジタル決済でリードしており、GCash、Maya、PayMongoといったさまざまなプラットフォームを誇っています。2024年4月、フィリピンは、包括的即時決済システム(IIPS)であるHigalaを開始し、デジタル決済をさらに推し進めました。この動きは、国内の経済的に恵まれていない人々のリアルタイムの支払いコストを削減することを目的としています。

- ノルウェーの国営多国籍通信会社Telenor ASAが2023年8月に実施した調査によると、フィリピンでは回答者の38%がモバイル端末で5G接続を主に使用していると回答しました。一方、回答者の10%は5Gネットワークを利用していなかった。

- さらに、地元のオンライン商店の大半はモバイルフレンドリーなウェブサイトやアプリを持っており、モバイルベースのeコマース購入の成長を促しています。その結果、モバイルフレンドリーなアプリケーションやウェブサイトを持つことは、eコマース分野で成功するために不可欠であると広く考えられています。

フィリピンeコマース業界の概要

フィリピンのeコマースは細分化されており、主要なプレーヤーが存在します。新たな競合のイントロダクションより、市場競争は激化しており、フィリピンに進出している外国企業はeコマース市場を活用しています。プラットフォームは、さまざまなパートナーシップに基づくプログラムを通じて、新たな加盟店を受け入れています。企業はまた、フィリピンの他の地域の販売者により良いサービスと迅速な配送を提供することで、リーチを広げることに力を注いでいます。

- 2024年6月- フィリピンの進行中のデジタル変革に基づき、貿易産業省(DTI)はTikTokとの協議を主導しました。その目的は、フィリピンの革新的な経済を強化するために、既存の関係を強化し、新たな協力関係を模索することです。DTIはこの提携を、フィリピン国内でのeコマースを推進する上で極めて重要な動きと捉えています。想定される成果は、デジタルマーケットプレースが大きく成長し、企業、消費者、そして経済全体に恩恵をもたらすことです。TikTokが現地の零細・中小企業(MSME)に大きな影響力を持つことで、生産部門におけるeコマースの導入が加速することが期待されます。これにより、質の高い雇用機会が創出され、フィリピン製品の国際競争力が高まることが期待されます。

- 2024年6月-GHL Systems Berhadの子会社であるGHLシステムズフィリピン(GHLフィリピン)は、フィリピン企業向けにアリペイ+の統合を促進しました。これにより、フィリピン国内の企業は、対面取引とeコマースの両方で、アジアの著名なモバイルウォレットからのデジタル決済を利用できるようになります。この統合により、フィリピンの電子商取引は大幅に強化される見込みです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 主な市場動向と小売業全体に占めるeコマースのシェア

- COVID-19がeコマース売上に与える影響

第5章 市場力学

- 市場促進要因

- ファッション業界からの需要の高まり

- インターネットとスマートフォンの普及

- 市場の課題

- インターネットの低速化

- フィリピンのeコマース産業に関する主要な人口動向とパターンの分析(人口、インターネット普及率、eコマース普及率、年齢と所得などを含む対象範囲)

- フィリピンのeコマース産業における主な取引形態の分析(現金、カード、銀行振込、ウォレットなどの一般的な決済手段を含む範囲)

- フィリピンにおける越境eコマース産業の分析(越境の市場価値と主要動向)

- アジア太平洋地域のeコマース産業におけるフィリピンの位置づけ

第6章 市場セグメンテーション

- B2C eコマース別

- 予測期間の市場規模(GMV)

- 用途別

- 美容・パーソナルケア

- 家電

- ファッション・アパレル

- 飲食品

- 家具・家庭用品

- その他(玩具、DIY、メディアなど)

- B2B eコマース別

- 予測期間の市場規模

第7章 競合情勢

- 企業プロファイル

- Lazada Group

- Shopee

- eBay Inc.

- Zalora

- Metrodeal

- Carousell

- Galleon(Sterling Galleon Corporation)

- BeautyMNL(Taste Central Curators Inc.)

- Inter IKEA Systems B.V.

- Ubuy Co.

- Sephora Digital SEA Pte Ltd

- Kimstore

- Perfume Philippines

第8章 投資分析

第9章 市場の将来展望

The Philippines E-commerce Market size is estimated at USD 17.65 billion in 2025, and is expected to reach USD 33.65 billion by 2030, at a CAGR of 13.78% during the forecast period (2025-2030).

Online purchasing and selling of products and services is known as e-commerce. Affiliate marketing strategies are also a possible part of the definition of an e-commerce firm. To increase online sales, users can leverage e-commerce platforms like their own website, through a well-known retailer like Amazon, or social media.

Key Highlights

- Due to its strong economy and a significant number of digitally savvy people, the Philippines is one of Southeast Asia's fastest-growing e-commerce markets. Many websites and digital applications are striving for market share against local, regional, and global rivals. Owing to better connectivity in the Philippines and the developing infrastructure, a growing portion of the country's sizeable population is now connected to the Internet. The connected population of the Philippines typically accesses the nation's e-commerce market through computers and mobile devices.

- One of the biggest trends in online retail is platform convergence. Customers prefer an all-in-one shopping experience that includes product ratings and prices, buying, and making payments using the platforms' new online payment options. Consequently, online shopping features are available on portal websites, social media, TV home shopping, over-the-top media services (OTT), etc. As a result, their platforms are becoming more popular.

- The quick development of wireless and Internet technology has significantly impacted online retailing and e-commerce advancement. The accessibility of smart devices, advancements in telecommunications infrastructure, rising purchasing power, a lack of time, and additional convenience have compelled businesses to adopt technology and meet customers' expanding needs, which has sped up the development of this new business model for online food ordering.

- Despite its rapid progress, the Philippines has not yet made management and technology more accessible to wider audiences. E-commerce advancements have also been delayed by government officials and local organizations' inaction in defining infrastructure initiatives to promote the nation's technology and internet sectors. To accommodate the growing traffic in the area, carriers and governments in the nation need to make increases in internet speeds.

- A turning point for e-commerce in the Philippines was the COVID-19 pandemic, which resulted in lockdown and movement restrictions, drove demand to record highs, attracted new buyers and sellers to online marketplaces, and provided players with long-term development. The e-commerce industry benefited greatly from the epidemic as a result of containment efforts that made consumers aware of the convenience of online shopping and encouraged seasoned online shoppers to make additional purchases.

Philippines E-commerce Market Trends

Fashion Industry to Dominate the Market Significantly

- Before the COVID-19 outbreak, Filipinos hesitated to make financial commitments online. Due to the obstruction, Filipinos were obliged to purchase food and other needs online, this skyrocketed the number of e-commerce transactions. Thousands of Filipino business owners rapidly caught up, opening online stores offering everything from face masks to electronic consumer items. In the fashion and cosmetics sectors, prominent corporations also increased their E-commerce activities.

- With its Southeast Asian neighbors, the Philippines' e-commerce environment is continually expanding and changing. Physical storefronts at malls have always been a significant economic paradigm in the fashion retail industry, but pandemics have completely altered this.

- The Philippines has encouraged new fashion-related businesses to establish operations there for the past few years. Because of this, the market has continued to grow, in the wholesale and retail industries, utilizing the e-commerce market with new brands domestically.

- The e-commerce landscape in the Philippines is witnessing a surge in popularity among online consumers. These platforms not only offer a wider array of products but also boast competitive pricing. Consequently, the e-commerce market is on a trajectory of significant growth, with projections extending to 2030. Notably, Shopee leads the pack, drawing in over 70 million monthly web visitors, closely followed by Lazada, which sees around 37 million visitors each month. Insights from Meltwater reveal that, during the third quarter of 2023, a substantial 57% of Filipino respondents reported making weekly online purchases, with a notable portion opting for online grocery shopping.

- Moreover, due to rising disposable incomes and lavish spending, consumer demands in the fashion industry are becoming more complex and diverse. Other elements include the rise of life-enriching consumption, such as leisure and cultural activities, an increase in internet sales, an aging population, and a shift in the core demographic of consumers.

Increased Internet Use, Online Payments, and Mobile Phones to Drive the Market

- The Philippines' e-commerce market has a lot of room to expand and advance. Filipino consumers' adoption of a digital lifestyle is the key force behind this. According to the World Bank, the Philippines has one of the most dynamic economies in the East Asia Pacific area. In 2023, The Philippines emerged as Southeast Asia's fastest-growing economy, boasting a 5.6% growth rate, slightly below the government's ambitious target of 6.0-7.0%. This data is sourced from the IMF's Economic Forecast for 2024.

- The country is witnessing rapid development in 5G and internet services. In 2023, Globe Telecom significantly bolstered its 5G infrastructure, introducing 894 new sites. This expansion led to an outstanding outdoor coverage of 97.90% in the National Capital Region and 92.36% in major cities spanning the Visayas and Mindanao.

- The Philippines leads in digital payments, boasting a range of platforms like GCash, Maya, and PayMongo. In April 2024, the nation furthered its digital payment landscape with the launch of Higala, an Inclusive Instant Payment System (IIPS). This move aims to reduce real-time payment costs for the financially underserved in the country.

- According to a survey conducted by Telenor ASA, a Norwegian majority state-owned multinational telecommunications company, in August 2023, 38% of respondents in the Philippines reported predominantly using a 5G connection on their mobile devices. In contrast, 10% of respondents did not utilize a 5G network.

- Additionally, the majority of local online merchants have mobile-friendly websites and apps, which hastens the growth of mobile-based e-commerce purchases. Consequently, having a mobile-friendly application or website is widely regarded as being essential for success in the e-commerce sector.

Philippines E-commerce Industry Overview

The Philippines' E-commerce is fragmented with the presence of key players in the country. With the introduction of new competitors, the market has become highly competitive, and foreign players entering the nation take advantage of the E-commerce market. The platforms accept new merchants through a variety of partnership-based programs. Businesses also put a lot of effort into broadening their reach by giving sellers in other parts of the Philippines better service and faster delivery.

- June 2024 - Building on the Philippines' ongoing digital transformation, the Department of Trade and Industry (DTI) led discussions with TikTok. Their objective is to fortify existing ties and explore new collaborations, all in a bid to bolster the nation's innovative economy. DTI views this partnership as a pivotal move in advancing e-commerce within the Philippines. The envisioned outcome is a digital marketplace set for substantial growth, benefitting businesses, consumers, and the broader economy. With TikTok's significant influence over local micro, small, and medium enterprises (MSMEs), it is expected an accelerated adoption of e-commerce in production sectors. This, in turn, promises to create high-quality employment opportunities and enhance the global competitiveness of Philippine products.

- June 2024 - GHL Systems Philippines Inc. (GHL Philippines), a subsidiary of GHL Systems Berhad, has facilitated the integration of Alipay+ for Philippine businesses. This move allows local businesses to accept digital payments from prominent Asian mobile wallets, both in face-to-face transactions and e-commerce. The integration is poised to significantly enhance the e-commerce landscape in the Philippines.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness-Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Key Market Trends and Share of E-commerce of Total Retail Sector

- 4.4 Impact of COVID-19 on the E-commerce Sales

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand from Fashion Industry

- 5.1.2 Penetration of Internet and Smartphone Usage

- 5.2 Market Challenges

- 5.2.1 Low Internet Speed

- 5.3 Analysis of Key Demographic Trends and Patterns Related to E-commerce Industry in Philippines (Coverage to include Population, Internet Penetration, E-commerce Penetration, Age & Income etc.)

- 5.4 Analysis of the Key Modes of Transaction in the E-commerce Industry in Philippines (Coverage to Include Prevalent Modes of Payment such as Cash, Card, Bank Transfer, Wallets, etc.)

- 5.5 Analysis of Cross-Border E-commerce Industry in Philippines (Current Market Value of Cross-Border & Key trends)

- 5.6 Current Positioning of Country Philippines in the E-commerce Industry in Asia-Pacific

6 MARKET SEGMENTATION

- 6.1 By B2C E-commerce

- 6.1.1 Market Size (GMV) for the Forecast Period

- 6.1.2 By Application

- 6.1.2.1 Beauty and Personal Care

- 6.1.2.2 Consumer Electronics

- 6.1.2.3 Fashion and Apparel

- 6.1.2.4 Food and Beverage

- 6.1.2.5 Furniture and Home

- 6.1.2.6 Others (Toys, DIY, Media, etc.)

- 6.2 By B2B E-commerce

- 6.2.1 Market Size for the Forecast Period

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Lazada Group

- 7.1.2 Shopee

- 7.1.3 eBay Inc.

- 7.1.4 Zalora

- 7.1.5 Metrodeal

- 7.1.6 Carousell

- 7.1.7 Galleon (Sterling Galleon Corporation)

- 7.1.8 BeautyMNL (Taste Central Curators Inc.)

- 7.1.9 Inter IKEA Systems B.V.

- 7.1.10 Ubuy Co.

- 7.1.11 Sephora Digital SEA Pte Ltd

- 7.1.12 Kimstore

- 7.1.13 Perfume Philippines