|

|

市場調査レポート

商品コード

1644491

インドのオフィス不動産:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India Office Real Estate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのオフィス不動産:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

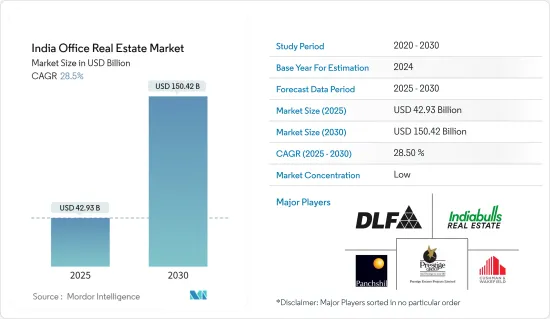

インドのオフィス不動産市場規模は2025年に429億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは28.5%で、2030年には1,504億2,000万米ドルに達すると予測されます。

H12024年、インドのオフィス市場はこれまでで最高の業績を達成し、目覚しい成長軌道を継続しました。ムンバイ、デリー-NCR、ベンガルール、チェンナイ、コルカタ、プネー、ハイデラバードの上位7都市すべてが、2024年上半期に100万平方フィート(msf)以上の画期的なグロス・リース量を記録しました。さらに、リース量は2024年上半期に33.5msfに達し、上半期としては過去最高となり、2019年に記録した前回ピークを上回りました。この堅調な伸びは、インドのオフィス市場の回復力と強さを裏付けています。

ハイブリッドワークモデルが普及し、軟質なワークスペースへの需要が急増する中、オフィス不動産の状況は変革の時を迎えています。伝統的オフィススペースが依然として重要である一方、フレキシビリティへのシフトが顕著です。このシフトの背景には、ワークライフバランスの改善、コスト効率の向上、適応性の高い職場環境に対する要望があります。これを受けて、オフィスの大家は物件を進化させ、柔軟な賃貸条件や最新の設備を導入しています。一方、入居者は充実したワークプレイスを求めるだけでなく、成長意欲を高めるために多様な戦略を取り入れています。

インドのオフィス不動産市場動向

ITとBPMセクターがオフィス需要を牽引

インドでは、オフィスセクターがダイナミックな急成長を遂げ、前年比53%増の30億米ドルを超える投資を集めています。この上昇の主要要因は、世界のケイパビリティセンター(GCC)からの需要の高まりと、現在市場全体のリース活動の46%を占めるインド企業による活発なリース活動です。

GCCのモデルもまた、コスト裁定や標準化を中心としたセンターから、顧客体験や技術主導のハブへと進化しつつあります。技術は一貫してオフィススペースのリース需要を牽引しています。全体の需要の約35%を占めるハイテクセクターの影響力は、ベンガルールやハイデラバードなどの都市では40%を超えています。政府のインフラ投資に後押しされ、BFSIセクターも繁栄しています。一方、ハイブリッドワークの台頭は軟質なワークスペースの重要性を浮き彫りにしています。また、世界サプライチェーンの再編により、エンジニアリングや製造業も拡大しています。

ベンガルールがオフィス不動産ブームを牽引

インド産業連盟によると、インドのITの中心地であるベンガルールは、2030年までに3億3,000万~3億4,000万平方フィートのオフィスストックを誇り、国内の商業不動産市場における優位性を維持すると予測されています。2024年6月現在、同市のオフィスストックは2億2,300万平方フィートを超え、10年前の1億平方フィートから2倍以上に急増しています。2024年上半期には、10万平方フィートを超えるオフィススペースの取引が前年同期比54%急増し、2023年上半期の1,018万平方フィートから2024年上半期には1,569万平方フィートに増加しました。この成長により、同市は国内主要都市の中でオフィススペースの主要拠点となっています。

2030年に向けて、ベンガルールのオフィス市場は主に技術、エンジニアリング、製造業、BFSIセクターが牽引するとみられます。さらに、ライフサイエンス、航空、自動車産業もこの需要急増に大きく貢献する存在として浮上しています。現在、技術セクターが市の年間吸収額の30~35%を占め、商業の中心地であるアウター・リング・ロードやホワイトフィールドで強い存在感を示しています。

2022~2024年6月までの間に、ベンガルールはインドにおけるGCCからの需要において圧倒的な41%のシェアを占めました。この実績は、熟練した労働力、最高級のグレードA資産、強固なハイテクインフラといったベンガルール独自の提供に起因しています。

インドのオフィス不動産業概要

インドのオフィス不動産市場は、国内外からの参入企業によって競争環境が形成されているため、非常に競争が激しいです。第2級都市には中小企業にとって多くのビジネス機会があります。国内のオフィス不動産開発業者には、Indiabulls Real Estate、DLF Ltd.、Prestige Estate Projects Ltd.、Supertech Limited、Oberoi Realtyなどがあり、オフィス不動産コンサルタント会社には、Cushman &Wakefield、CBRE Groupなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の規制と施策

- 政府の規制と取り組み

- サプライチェーン/バリューチェーン分析

- インドのオフィス不動産セクターにおける技術革新洞察

- 地政学とパンデミックが市場に与える影響

第5章 市場力学

- 市場促進要因

- インドにおけるBPMとITセクターの急成長

- 外国投資の拡大

- 市場抑制要因

- 建設コストの上昇

- 規制のハードル

- 市場機会

- インドにおけるeコマースと製造業の拡大

- 政府によるインフラ支援

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- 主要都市

- バンガロール

- ハイデラバード

- ムンバイ

- その他の都市

第7章 競合情勢

- 市場集中度概要

- 企業プロファイル

- Savills

- Cushman & Wakefield

- CBRE Group

- JLL

- Panchshil Realty

- Indiabulls Real Estate

- DLF Limited

- Prestige Estate Projects Ltd

- Supertech Limited

- Oberoi Realty

- HDIL Ltd*

- その他の企業

第8章 市場機会と今後の動向

第9章 付録

- マクロ経済指標(GDP分布、活動別)

- 経済統計-運輸・倉庫業の経済への貢献

- 対外貿易統計-輸出・輸入(製品別)

The India Office Real Estate Market size is estimated at USD 42.93 billion in 2025, and is expected to reach USD 150.42 billion by 2030, at a CAGR of 28.5% during the forecast period (2025-2030).

In H12024, India's office market achieved its best performance to date, continuing its impressive growth trajectory. All top seven cities - Mumbai, Delhi-NCR, Bengaluru, Chennai, Kolkata, Pune, and Hyderabad - recorded groundbreaking gross leasing volumes of at least 1 million sq. ft (msf) in H1 2024. Additionally, leasing volumes reached 33.5 msf in H1 2024 , marking the best-ever first half and surpassing the previous peak set in 2019. This robust growth underscores the resilience and strength of the Indian office market.

As hybrid work models gain traction and the demand for flexible workspaces surges, the landscape of office real estate is poised for transformation. While traditional office spaces remain significant, a pronounced shift towards flexibility is evident. This shift is fueled by aspirations for improved work-life balance, cost efficiencies, and the demand for adaptable work settings. In response, office landlords are evolving their properties, introducing flexible leasing terms and modern amenities. Meanwhile, occupiers are not only seeking enriched workplace experiences but are also embracing diverse strategies to bolster their growth ambitions.

India Office Real Estate Market Trends

IT and BPM Sectors Drive Demand for Office Space

In India, the office sector has witnessed a dynamic surge, attracting investments exceeding USD 3 billion, marking a 53% rise from the prior year. This upswing is largely fueled by the escalating demand from Global Capability Centers (GCCs) and vigorous leasing endeavors by Indian corporations, which presently constitute 46% of the overall market leasing activities.

The GCC model is also now evolving from primarily cost arbitrage/standardisation focused centers to customer experience and technology led hubs. Technology consistently drives the demand for office space leasing. Accounting for approximately 35% of the overall demand, the tech sector's influence surges beyond 40% in cities such as Bengaluru and Hyderabad. Bolstered by government infrastructure investments, the BFSI sector is flourishing. Meanwhile, the rise of hybrid work has spotlighted the importance of flexible workspaces. Additionally, engineering and manufacturing sectors have expanded, fueled by global supply chain realignments.

Bengaluru Leads the Boom for Office Real Estate

Bengaluru, India's IT capital, is projected to maintain its dominance in the country's commercial real estate market, boasting an office stock of 330-340 million sq. ft by 2030, as per the Confederation of Indian Industry. As of June 2024, the city's office stock has surged to over 223 million sq. ft, more than doubling from 100 million sq. ft from a decade ago. In H1 2024, transactions for office spaces exceeding 100,000 sq. ft surged by 54% year-on-year, climbing from 10.18 million sq. ft in H1 2023 to 15.69 million sq. ft in H1 2024. This growth positions the city as the leading hub for office space among all major cities in the country.

In the lead-up to 2030, Bengaluru's office market is poised to be primarily driven by the technology, engineering, manufacturing, and BFSI sectors. Additionally, life sciences, aviation, and the automobile industry are emerging as significant contributors to this demand surge. Currently, the technology sector dominates, accounting for 30-35% of the city's annual absorption, with a strong presence in the commercial hubs of Outer Ring Road and Whitefield.

Between 2022 and June 2024, Bengaluru commanded a dominant 41% share in the demand from GCCs in India. This achievement is attributed to Bengaluru's unique offerings: a skilled workforce, premium Grade-A assets, and a robust tech infrastructure.

India Office Real Estate Industry Overview

The Indian office real estate market is highly competitive, as the sector's domestic and foreign participants have created a competitive environment. There are many opportunities for small and medium companies in tier 2 cities. Some of the office real estate developers in the country include Indiabulls Real Estate, DLF Ltd., Prestige Estate Projects Ltd., Supertech Limited, and Oberoi Realty, and office real estate consultancy firms include Cushman & Wakefield, CBRE Group, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Policies and Regulations

- 4.3 Government Regulations and Initiatives

- 4.4 Supply Chain/Value Chain Analysis

- 4.5 Insights into Technological Innovation in the India Office Real Estate Sector

- 4.6 Impact of Geopolitics and Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid growth of BPM and IT sectors in India

- 5.1.2 Growing foreign investments

- 5.2 Market Restraints

- 5.2.1 Rising construction costs

- 5.2.2 Regulatory hurdles

- 5.3 Market Opportunities

- 5.3.1 Expanding e-commerce and manufacturing sectors in India

- 5.3.2 Infrastructure support from government

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 Major Cities

- 6.1.1 Bangaluru

- 6.1.2 Hyderabad

- 6.1.3 Mumbai

- 6.1.4 Other Cities

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 Savills

- 7.2.2 Cushman & Wakefield

- 7.2.3 CBRE Group

- 7.2.4 JLL

- 7.2.5 Panchshil Realty

- 7.2.6 Indiabulls Real Estate

- 7.2.7 DLF Limited

- 7.2.8 Prestige Estate Projects Ltd

- 7.2.9 Supertech Limited

- 7.2.10 Oberoi Realty

- 7.2.11 HDIL Ltd*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

- 9.1 Macroeconomic Indicators (GDP Distribution, by Activity)

- 9.2 Economic Statistics - Transport and Storage Sector Contribution to the Economy

- 9.3 External Trade Statistics - Export and Import, by Product