欧州の菓子類包装:市場シェア分析、産業動向、成長予測(2025~2030年)

Europe Confectionery Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 142 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644479

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

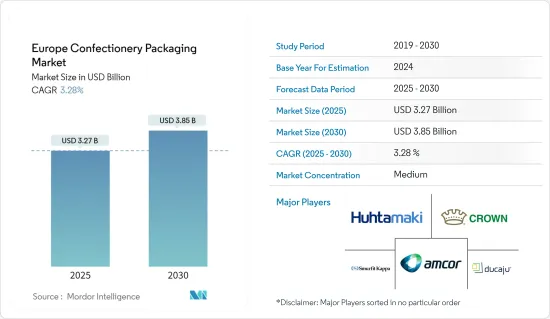

欧州の菓子類包装市場規模は2025年に32億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは3.28%で、2030年には38億5,000万米ドルに達すると予測されます。

パンデミックは間違いなく世界中の商業を混乱させ、主にサプライチェーンの重要性を浮き彫りにしました。他の必須インフラ部門と同様に、菓子類産業もこうした課題から大きな影響を受けています。例えば、2021年6月現在、ドイツの菓子類産業は、ビジネスが正常に戻るのは早くても来年以降になるだろうと述べています。連邦ドイツ菓子類工業会(BDSI)の調査では、2021年第1四半期における中規模会員の経済発展が調査されました。同調査によると、コロナウイルス危機により、産業は依然として緊張状態にあります。

主要ハイライト

- パンデミック(COVID-19)の影響で菓子類の消費は記録的な落ち込みを見せた。例えば、ドイツの菓子類は過去20年間で初めての輸出不振を記録しました。特に、EU加盟国はドイツの菓子類輸出の約80%を受け入れています。ロックダウン、物流の障害、失業者の増加、家計所得の減少が菓子類の売上減少の大きな要因となっています。

- プラスチック製の菓子類包装は、プラスチック材料が軽量で扱いやすいため、他の製品よりも消費者の間で人気があります。大手メーカーも、製造コストの低さから、容器やスタンドパウチのようなプラスチック包装を好んで使用しています。

- 市場には、先進的で費用対効果が高く、サステイナブル包装ソリューションが多種多様に登場しており、製品としてのプラスチックは世界的に受け入れられています。このため、Amcorのような地域の参入企業は、菓子類包装の需要に応えるために新しいプラスチック製品フォーマットを導入しています。

- しかし、スタンドアップパウチ(SUP)は調査対象地域で大きな需要と消費者の関心を集めています。SUPへの関心が再び高まっている背景には、生産・充填速度の高速化を実現する新しい包装機械の開発、シール効率の先進化など、さまざまな要因があります。さらに、その他の技術的進歩により、ラミネート材料の機能性が向上し、耐熱性や耐貫通性が向上しています。

- 菓子類包装・欧州によると、健全な成長により、菓子、チョコレート、生鮮食品を含むほとんどのエンドユーザー市場の生産量が増加しています。軽量で持ち運びが容易な顧客に優しい製品に対する需要の高まりは、世界の菓子類包装市場で欧州の市場シェアが高いことの重要な要因と考えられます。持続可能性への注目の高まり、製品の賞味期限延長に対するニーズの高まり、衛生基準の向上、使いやすさを重視する顧客志向は、調査対象市場の主要促進要因です。

- さらに、包装指令は包装と包装廃棄物の管理に関する各国の措置を調和させることを目的としています。さらに、EU諸国は、すべての包装について生産者責任制度を確立するよう指示されています。EUは、2025年までにすべての包装材の65%をリサイクルすることを目標としており、そのうちプラスチック包装材の50%、アルミニウム包装材の50%、紙・段ボール包装材の75%をリサイクルすることを計画しています。さらにEUは、2030年までに全包装材の70%をリサイクルすることを目標としています。

欧州の菓子類包装市場の動向

チョコレートが大きな市場シェアを占める見込み

- チョコレートは酸化を防ぎ、チョコレートの味と香りを保護する材料で包装されます。チョコレートは酸素に触れると古くなり、風味が損なわれます。そのため、バージン繊維の板紙が使用されるが、外部の臭いの移りを緩和し、保存性を確保するためのバリアも必要です。

- さらに、チョコレートバーは通常、チョコレートに直接触れるアルミホイル、チョコレートバー全体を覆う化粧紙スリーブ、または一次包装と二次包装の役割を果たすPETフィルムの2つの方法のいずれかで包装されます。

- 包装はチョコレートの購買行動において重要な役割を果たしています。チョコレートは誰かへの贈り物として購入されることが多いため、チョコレートの包装は特に重要です。したがって、チョコレートの品質はそれを包む包装と同じくらい重要であることが多くの研究で指摘されています。消費者がその製品に馴染みがない場合、消費者は最も心地よい包装のものを選ぶ傾向があります。

- リボラーが行った調査によると、消費者の目は主に包装の情報の大きさに引かれます。左から右へ、上から下へと要素に注目する傾向があります。消費者は、この2つのパターンを組み合わせた包装メッセージを、より大きなインパクトをもって知覚します。

- さらに、2021年2月、Nestleの「Smarties」ブランドは、チョコレート菓子類にリサイクル可能な紙包装の採用を計画しました。スマーティーズは、リサイクル可能な紙製包装に切り替えた最初の世界的菓子ブランドのひとつであり、世界中で毎年販売されている約2億5,000万個のプラスチックパックを取り除くことになります。

最大の市場シェアを占める英国

- 英国の菓子類市場は、メーカー各社が英国の消費者を甘いものに溺れさせる新たな手段を開発し、拡大しています。英国の消費者が小売店で購入できる製品の数は、消費者の革新的な製品に対する要求の高まりにより、膨大な数に拡大しています。NestleのWonkaブランドやCadbury Dairy MilkのMarvellous Creationsに代表されるように、より冒険的な製品はすぐにスタイルを真似されます。その上、味覚とブランドの嗜好は、個々の堅実な需要を可能にしています。

- 2020年11月にconfectionerynews.comに掲載されたレポートによると、消費者は2019年よりも5,000万英ポンドのチョコレートを購入したと報告されており、ロックダウン中のスーパーマーケットでのマルチパックやシェアリングバーの購入が主要要因となっています。食料品店はまた、人気ブランドのシェアリングバーの需要が37%増加し、そのラベルの売上が5分の1に急増したことを明らかにしました。菓子類産業におけるこうした需要動向の高まりは、国内における包装ソリューションの需要を増加させると考えられます。

- プラスチック包装廃棄物に対する懸念が高まる中、同市場の大手菓子類メーカー数社は、プラスチックフリーのソリューションへの切り替えを進めています。例えば、最近、セルフリッジからQVC、海外の店舗でグルメ菓子を販売しているFlower & Whiteは、ヒートシール可能なコーティングを施した紙ベースのパウチを使用した最新のグルメ商品を発表しました。さらに、同社は、持続可能性の向上とエネルギー削減への広範なコミットメントの一環として、紙スリーブ入りのヒット商品「Meringue Bar」シリーズをリニューアルしました。

- さらに2020年には、Nestleの有名ブランドであるSmartiesの菓子類にリサイクル可能な紙包装を採用し、英国で発売を開始しました。これは、スマーティーズ製品の90%と、すでにリサイクル可能な紙包装で包装されている製品の10%の移行を意味します。Smartiesは、リサイクル可能な紙包装に切り替えた最初の世界的菓子類ブランドとなり、全世界で毎年販売されている約2億5,000万個のプラスチックパックを省くことになります。

- さらに、英国とアイルランドで毎年約1億4,000万個の菓子類シェアバッグを販売しているNestleの英国・アイルランド事業では、包装を15%削減するためにバッグのデザインを変更します。これにより、同社の年間サプライチェーンから83トンのプラスチックが取り除かれることになります。

欧州の菓子類包装産業概要

欧州の菓子類包装市場は競争が激しいです。市場で大きなシェアを持つ大手企業は、様々な地域で顧客基盤を拡大しています。また、多くの企業が市場シェアと収益性を高めるために、複数の企業と戦略的かつ協力的な取り組みを形成しています。市場の最近の動向をいくつか発表します。

- 2021年7月-イタリアのFerreroは菓子シリーズ用に紙ベースの包装材を開発しました。この新包装は、紙フィルムを使用したキンダーベーカリー製品の新しい包装方法を特徴としており、同国の紙の流れにおけるリサイクルに適しています。

- 2020年9月-Amcorは、菓子・スナック向けのリサイクル可能な軟質レトルトパウチの発売を発表しました。このパウチは賞味期限が長く、耐熱性と共に高いバリア性を備えています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 市場促進要因

- 小型化と欧州でのわずかではあるがベースラインの成長に牽引される単位数量の成長

- リサイクル可能な材料や生分解性材料の使用など、持続可能性に後押しされた包装革新

- 製品メーカーは、印刷と包装のイノベーションを活用することで競合優位性を獲得するため、引き続き包装に注力

- 市場課題

- 包装規制のダイナミックな性質が硬質プラスチックベースの製品販売に影響を与え続ける

- エコシステム分析

- 産業の魅力-ポーターのファイブフォース分析

- 菓子類包装産業におけるCOVID-19の影響

第5章 欧州の菓子類市場概要

- 現在の市場シナリオ

- 欧州の流通チャネルと平均包装サイズの網羅性

- 欧州の上位5ベンダーの分析

第6章 市場セグメンテーション

- タイプ別

- プラスチック(ラップ、フィルム、容器、スタンドパウチ)

- 紙・板紙(ラッパー、二次パックなど)

- 金属容器

- ガラス瓶・ジャー

- 菓子類別

- チョコレート

- 砂糖ベース

- ガム

- その他の菓子類

- 国別

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- その他の欧州

第7章 競合情勢

- 企業プロファイル

- Huhtamaki OYJ

- Ducaju NV

- Amcor PLC

- Smurfit Kappa Group

- Crown Holdings

- WestRock Company

- Berry Global

- International Paper

第8章 市場展望

目次

The Europe Confectionery Packaging Market size is estimated at USD 3.27 billion in 2025, and is expected to reach USD 3.85 billion by 2030, at a CAGR of 3.28% during the forecast period (2025-2030).

The pandemic undoubtedly disrupted commerce across the globe, primarily highlighting the critical nature of the supply chain. Like the other essential infrastructure sectors, the confectionery industry has also been significantly affected by these challenges. For instance, as of Jun 2021, the German confectionery industry stated that it does not expect the business to return to normal until next year at the earliest. A survey by the Federal Association of the German Confectionery Industry (BDSI) examined the economic development of medium-sized members in the first quarter of 2021. It stated that the industry remains tense owing to the coronavirus crisis.

Key Highlights

- Consumption of confectionery products witnessed a record fall due to the COVID-19 pandemic lockdowns. For instance, the German confectionery registered the first slump in exports in the past 20 years. Notably, member countries of the European Union receive around 80% of the German confectionery exports. With lockdowns, logistical hurdles, and increased unemployment, falling household incomes were the significant drivers for declining confectionery sales.

- Plastic Confectionery packaging has become popular among consumers over other products, as plastic material is lightweight and easier to handle. Even significant manufacturers have preferred to use plastic packaging like Containers & Stand-up Pouches, owing to the lower cost of production.

- A wide variety of advanced, cost-effective, and sustainable packaging solutions emerging in the market, and plastic as a product, has been accepted globally. This has led to the regional players, such as Amcor, introducing new plastic product formats to cater to the demand for confectionery packaging.

- However, Stand-up Pouches (SUPs) are witnessing significant demand and consumer interest in the studied region. The revived interest in SUPs can be attributed to various factors, including developing new packaging machinery, which delivers higher production and filling speeds, and advances in sealing efficiencies. In addition, other technological advances have helped to improve functionality and better heat and puncture resistance of the laminate material.

- According to Confectionery Packaging Europe, healthy growth has increased production for most end-user markets, including sweets, chocolate, and fresh foods. The increased demand for customer-friendly products which are lightweight and easily transportable can be considered as a significant factor behind Europe's high market share in the global confectionery packaging market. Increasing focus on sustainability, the increased need for extended product shelf life, rising standards of hygiene, and customer focus on ease of use are the primary drivers of the studied market.

- Further, the Packaging Directive aims to harmonize national measures on the packaging and the management of packaging waste. Moreover, the EU countries are directed to ensure that producer responsibility schemes are established for all packaging. The EU has targeted to recycle 65% of all packaging materials, of which they have planned to recycle 50% of plastic packaging, 50% of Aluminum packaging, and 75% of paper and cardboard packaging by 2025. Further, the EU targets to recycle 70% of all packaging materials by 2030.

Europe Confectionery Packaging Market Trends

Chocolate is Expected to Hold Significant Market Share

- Chocolate is packaged in materials that prevent oxidation and protect the taste and aroma of the chocolate. Chocolate can get stale when exposed to oxygen and lose its flavor; therefore, it becomes inedible, rendering it unfit to sell. Hence, virgin fiber paperboard is used, but barriers are also needed to mitigate the transfer of external odors and ensure shelf life.

- Moreover, chocolate bars are typically wrapped in one of two ways: aluminum foil which is in direct contact with the chocolate, and a decorative paper sleeve that fits over the entire bar, or PET films, that serves as primary and secondary packaging.

- Packaging plays a vital role in chocolate purchasing behavior. Packaging of chocolates is particularly relevant as chocolate is often purchased as a gift for someone else. Thus, many studies indicated that the quality of the chocolate is as important as the packaging that wraps it. If the consumer is not familiar with the product, then the consumer tends to choose the one with the most pleasant packaging.

- According to a study conducted by Rebollar, the consumer's eye is primarily drawn to the size of the information on the packaging. It tends to focus on the elements from left to right and from top to bottom. The consumers perceive the packaging message that combines these two patterns with a more significant impact.

- Furthermore, in February 2021, Nestle's Smarties brand planned to adopt recyclable paper packaging for its chocolate confectionery products. Smarties is one of the first global confectionery brands to switch to recyclable paper packaging, removing around 250 million plastic packs sold worldwide every year.

United Kingdom Accounts for the Largest Market Share

- The UK confectionery market is expanding as manufacturers develop new means of tempting the UK consumer base to indulge its sweet tooth. A vast number of products available to UK consumers at retail is expanding due to the increasing consumer demand for innovation. More adventurous products are quickly imitated in style, as exemplified by Nestle's Wonka brand and Cadbury Dairy Milk's Marvellous Creations. Besides, the taste and brand preferences allow for individual solid demand.

- According to a report published on confectionerynews.com in November 2020, consumers have reportedly bought GBP 50 million more chocolates than they did in 2019, majorly driven by multipacks and sharing bars purchases at supermarkets during the lockdown. The grocers also revealed that the demand for popular brand sharing bars rose by 37%, while sales for its labels jumped by a fifth. Such increasing demand trends in the confectionery industry will likely increase the demand for packaging solutions in the country.

- With rising concerns over plastic packaging wastes, several leading confectionery players in the market are switching over to plastic-free solutions. For instance, recently, Flower & White, which sells its gourmet treats in outlets from Selfridges to QVC, and overseas, unveiled its latest gourmet product using a paper-based pouch with a heat-sealable coating. Further, the company has also relaunched its successful Meringue Bars' range in paper sleeves as part of a broader commitment to improve sustainability and reduce energy.

- Further, in 2020, Nestle's famous brand Smarties was launched with recyclable paper packaging for its confectionery products in the United Kingdom. It represents the transition of 90% of the Smarties range and 10% of the range already packed in recyclable paper packaging. Smarties will be the first global confectionery brand to switch to recyclable paper packaging, omitting approximately 250 million plastic packs sold globally every year.

- Further, Nestle UK and Ireland operations, which sell approximately 140 million confectionery sharing bags in the United Kingdom and Ireland every year, are redesigning their bags to deliver a 15% cut in packaging. This would remove 83 tons of plastic from its annual supply chain.

Europe Confectionery Packaging Industry Overview

The European Confectionery Packaging Market is competitive. The major players with a significant share in the market are expanding their customer base across various regions. In addition, many companies are forming strategic and collaborative initiatives with multiple companies to increase their market share and profitability. Some of the recent developments in the market are:

- July 2021 - Ferrero developed a paper-based packaging material for its confectionary range in Italy. The new packaging features a new method of wrapping Kinder Bakery products using paper film, suitable for recycling in the country's paper stream.

- September 2020 - Amcor announced the launch of a recyclable flexible retort pouch for confectioneries and snacks. This pouch has a long shelf life and offers a high barrier along with a heat-resistant feature.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Unit Volumes Driven by Downsizing and Baseline Growth Albeit Marginal in Europe

- 4.2.2 Packaging Innovations Driven by Sustainability, such as the Use of Recyclable and Biodegradable Materials

- 4.2.3 Product Manufacturers Continue to Focus on Packaging to Gain a Competitive Advantage by Leveraging Printing and Packaging Innovations

- 4.3 Market Challenges

- 4.3.1 Dynamic Nature Of Packaging Regulation Continues to Affect Rigid Plastic-based Product Sales

- 4.4 Industry Ecosystem Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6 Impact of COVID-19 on the Confectionery Packaging Industry

5 OVERVIEW OF CONFECTIONERY MARKET IN EUROPE

- 5.1 Current Market Scenario

- 5.2 Coverage on Distribution Channels and Average Pack Size in Europe

- 5.3 Analysis of the Top Five Vendors in Europe

6 MARKET SEGMENTATION

- 6.1 BY TYPE

- 6.1.1 Plastic (Wraps, Films, Containers, and Stand-up Pouches)

- 6.1.2 Paper and Paperboard (Wrappers, Secondary Packs, etc.)

- 6.1.3 Metal Containers

- 6.1.4 Glass Bottles and Jars

- 6.2 BY CONFECTIONERY TYPE

- 6.2.1 Chocolate

- 6.2.2 Sugar-based

- 6.2.3 Gums

- 6.2.4 Other Confectionery Types

- 6.3 BY COUNTRY

- 6.3.1 Germany

- 6.3.2 United Kingdom

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Russia

- 6.3.6 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Huhtamaki OYJ

- 7.1.2 Ducaju NV

- 7.1.3 Amcor PLC

- 7.1.4 Smurfit Kappa Group

- 7.1.5 Crown Holdings

- 7.1.6 WestRock Company

- 7.1.7 Berry Global

- 7.1.8 International Paper

8 MARKET OUTLOOK

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 142 Pages

- 納期

- 2~3営業日