|

市場調査レポート

商品コード

1773473

プロバイオティクスベースの栄養補助食品市場機会、成長促進要因、産業動向分析、2025年~2034年予測Probiotics Based Dietary Supplement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| プロバイオティクスベースの栄養補助食品市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月17日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

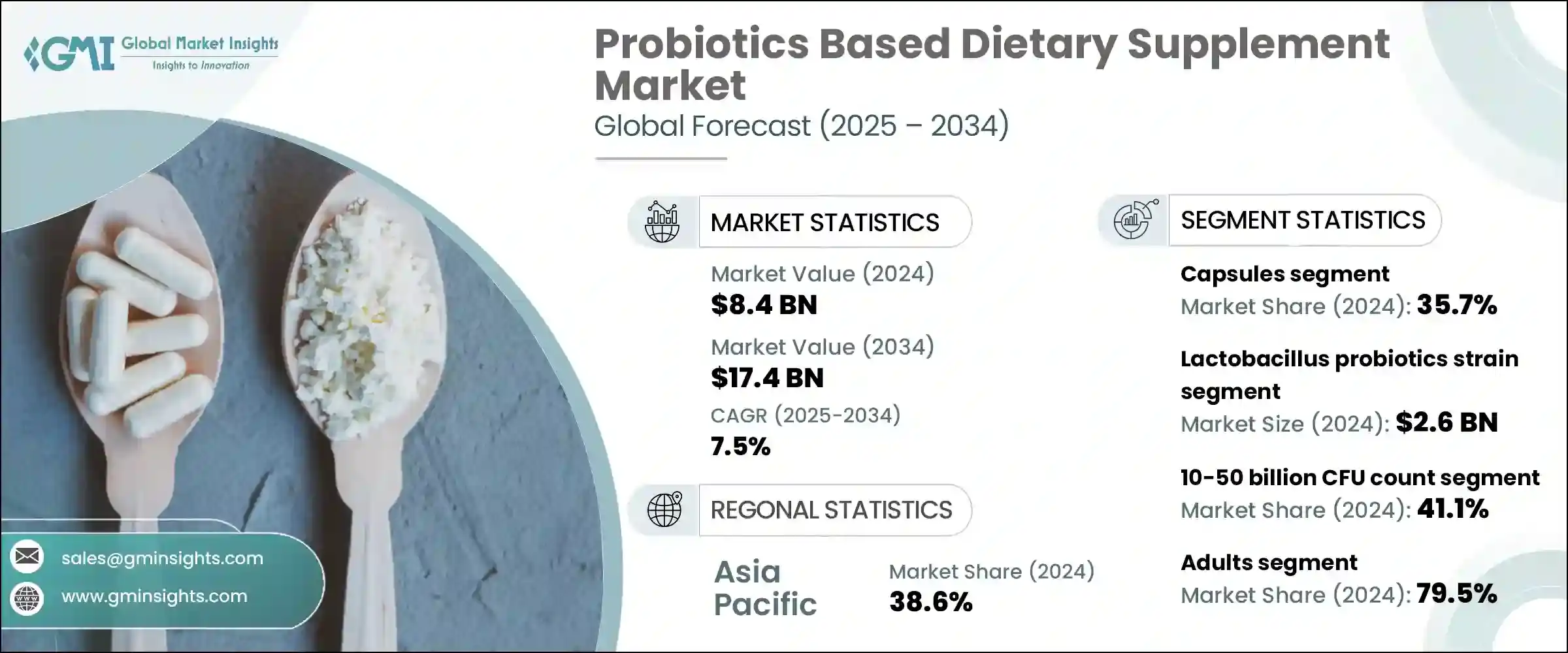

世界のプロバイオティクスベースの栄養補助食品市場は、2024年には84億米ドルと評価され、CAGR 7.5%で成長し、2034年には174億米ドルに達すると推定されています。

乳酸菌、ビフィズス菌、サッカロミセスなどの生きた菌株で作られたこれらのサプリメントは、消化のバランスをサポートし、免疫力を高め、腸と脳の健康を強化します。消化器系の健康、予防的健康、アレルゲンフリーの選択肢に対する意識の高まりが、需要に拍車をかけています。今日の消費者は、高CFU、マルチストレイン製剤、グミや小袋のような便利な形態を選んでいます。乳幼児、高齢者、健康志向の成人の間で、特に北米とアジア太平洋を中心に利用が広がっているため、臨床検証、送達システム、クリーンラベル製品にイノベーションの余地が生まれています。

乳製品不使用、透明性を重視した製品、持続可能な調達へのシフトは、健康志向と環境志向の栄養における幅広い動向を反映しており、プロバイオティクスを予防的健康の中心的な柱として位置づけています。消費者はますます成分表を吟味するようになり、倫理的価値観や食事制限に沿ったクリーンラベルの処方を求めるようになっています。このような行動の変化は、植物由来でアレルゲンを含まないプロバイオティクス・サプリメントへの需要を加速させ、各ブランドに非乳製品担体、天然香料、生分解性パッケージなどの革新を促しています。免疫力、気分、活力全般における腸の役割に対する認識が高まるにつれ、プロバイオティクスはもはやニッチなサプリメントではなく、毎日の必需品と見なされるようになっています。この進化は、トレーサビリティ、環境への責任、現代のライフスタイルに合わせた個別化された健康成果など、メーカーが製品開発に取り組む方法を変えつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 84億米ドル |

| 予測金額 | 174億米ドル |

| CAGR | 7.5% |

カプセルは35.7%のシェアを占め、2024年には30億米ドルに達します。カプセルの成功は、正確な投与量、長い保存期間、使いやすさによるものです。ベジタリアン、ゼラチン、遅延放出タイプは多様な消費者ニーズに対応し、プロバイオティクスが胃酸に耐えて腸まで届くことを保証します。個人に合わせた腸内健康法への関心が高まる中、消化、免疫、メンタルヘルスに合わせた高CFUカプセルのオプションが特に求められています。

乳酸菌株セグメントは30.4%のシェアを占め、2024年の市場規模は26億米ドルです。L.acidophilus、L.rhamnosus、L.plantarumなどの臨床的に裏付けされた菌株は、腸内細菌叢を改善し、免疫力を強化し、乳糖不耐症を改善することで知られています。胃酸に強く、単一菌株と複数菌株のブレンドの両方に適応できることから、乳製品不使用やビーガンのプロバイオティクス製品に人気があり、特に北米とアジアの市場で普及しています。

アジア太平洋プロバイオティクスベースの栄養補助食品市場は2024年に38.6%のシェアを占めました。この地域の成長の原動力は、消化器系と免疫系の健康に対する意識の高まり、乳糖不耐症率の上昇、都市化、機能性食品に対する需要の高まりです。地元および国際的なブランドは、消費者のニーズを満たすために小売店の存在感を高め、研究開発を拡大し、乳糖不使用で植物由来のプロバイオティクス・オプションを提供しています。政府主導のウェルネス・キャンペーン、中間層の増加、および発酵食品の地域的人気が、大量採用に寄与しています。

主な世界的イノベーターおよび販売業者には、ヤクルト本社、BioGaia AB、Nestle S.A.、Danone S.A.、Chr. Hansen Holding A/S.などがあります。大手企業は、系統の多様化と透明性のある表示によって競争力を強化し、健康志向でアレルゲンに敏感な消費者にアピールしています。また、腸脳、免疫、消化器系の健康強調表示を検証するための臨床試験にも投資しています。ビーガン用カプセル、ディレイド・リリース・オプション、グミ、パウダーなど、フォーマットの革新は、幅広い層へのアクセスを広げています。企業はeコマース・チャネルや消費者直販モデルを拡大する一方で、ヘルスケア専門家や食品ブランドとパートナーシップを結び、信頼性を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品形式別、2021~2034年

- 主要動向

- カプセル

- ベジタリアンカプセル

- ゼラチンカプセル

- 遅延放出カプセル

- その他

- タブレット

- チュアブル錠

- 腸溶錠

- その他

- 粉末

- 個包装

- バルク容器

- その他

- 液体

- ショット

- ドロップ

- その他

- グミ

- ゼラチンベース

- ペクチンベース

- その他

- その他

第6章 市場推計・予測:プロバイオティクス菌株別、2021~2034年

- 主要動向

- 乳酸菌

- L.アシドフィルス

- L.ラムノサス

- L.プランタラム

- L.カゼイ

- L.ロイテリ

- その他

- ビフィズス菌

- B.ビフィダム

- B.ロンガム

- B.ラクティス

- B.ブレーヴェ

- その他

- 連鎖球菌

- S.サーモフィルス

- その他

- バチルス

- B.コアグランス

- バチルス・サブチリス

- その他

- サッカロミセス

- S.ボウラルディ

- その他

- 多菌株製剤

- その他

第7章 市場推計・予測:CFU数別、2021~2034年

- 主要動向

- 10億CFU未満

- 10億~100億CFU

- 100億~500億CFU

- 500億CFU以上

第8章 市場推計・予測:消費者層別、2021~2034年

- 主要動向

- 大人

- 18~34歳

- 35~54歳

- 55歳以上

- 子供

- 乳児(0~2歳)

- 子供(3~12歳)

- 青少年(13~17歳)

第9章 市場推計・予測:健康アプリ別、2021~2034年

- 主要動向

- 消化器系の健康

- 過敏性腸症候群(IBS)

- 炎症性腸疾患(IBD)

- 抗生物質関連下痢

- その他

- 免疫の健康

- 女性の健康

- 体重管理

- 脳の健康

- 口腔の健康

- その他

第10章 市場推計・予測:流通チャネル別、2021~2034年

- 主要動向

- 小売薬局

- 健康・ウェルネスストア

- スーパーマーケットとハイパーマーケット

- オンライン小売

- eコマースプラットフォーム

- ブランドウェブサイト

- オンライン薬局

- 直接販売

- その他

第11章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第12章 企業プロファイル

- Chr. Hansen Holding A/S

- Danone S.A.(Activia, Actimel)

- Yakult Honsha Co., Ltd.

- Nestle S.A.(Garden of Life)

- Probi AB

- BioGaia AB

- Probiotics International Ltd(Protexin)

- Lallemand Inc.

- DuPont(IFF)

- Lifeway Foods, Inc.

- Morinaga Milk Industry Co., Ltd.

- Bifodan A/S

- Culturelle(i-Health, Inc.)

- Jarrow Formulas, Inc.

- NOW Foods

The Global Probiotics Based Dietary Supplement Market was valued at USD 8.4 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 17.4 billion by 2034. These supplements, crafted with live strains like Lactobacillus, Bifidobacterium, and Saccharomyces, support digestive balance, bolster immunity, and enhance gut-brain health. Rising awareness around digestive wellness, preventive health, and allergen-free options is spurring demand. Today's consumers are opting for high-CFU, multi-strain formulations, as well as convenient formats like gummies and sachets. Broadening use among infants, seniors, and health-conscious adults-especially across North America and Asia-Pacific-is creating space for innovations in clinical validation, delivery systems, and clean-label offerings.

The shift toward dairy-free, transparency-focused products and sustainable sourcing reflects a wider trend in health-conscious and eco-minded nutrition, positioning probiotics as a central pillar of preventive wellness. Consumers are increasingly scrutinizing ingredient lists, demanding clean-label formulations that align with ethical values and dietary restrictions. This behavioral shift is accelerating the demand for plant-based and allergen-free probiotic supplements, pushing brands to innovate with non-dairy carriers, natural flavorings, and biodegradable packaging. As awareness grows around the gut's role in immunity, mood, and overall vitality, probiotics are no longer viewed as niche supplements but rather as daily essentials. This evolution is transforming how manufacturers approach product development, with traceability, environmental responsibility, and personalized health outcomes tailored to modern lifestyles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $17.4 Billion |

| CAGR | 7.5% |

The capsule segment dominated the market with a 35.7% share, totaling USD 3 billion in 2024. Their success is due to precise dosage, long shelf-life, and ease of use. Vegetarian, gelatin, and delayed-release versions cater to diverse consumer needs, ensuring probiotics survive stomach acid to reach the gut. High-CFU capsule options tailored for digestion, immunity, and mental health are particularly sought after amid growing interest in personalized gut health regimens.

Lactobacillus strains segment made up 30.4% share, worth USD 2.6 billion in 2024. These clinically backed strains-such as L.acidophilus, L.rhamnosus, and L.plantarum-are known for improving gut flora, strengthening immunity, and aiding lactose intolerance. Their resilience against stomach acid and adaptability in both single- and multi-strain blends make them popular in dairy-free and vegan probiotic products, especially prevalent in North American and Asian markets.

Asia-Pacific Probiotics Based Dietary Supplement Market held a 38.6% share in 2024. Growth in this region is driven by increasing digestive and immune health awareness, higher lactose intolerance rates, urbanization, and rising demand for functional foods. Local and international brands are expanding their retail presence and R&D to meet consumer needs, offering lactose-free, plant-based probiotic options. Government-led wellness campaigns, a growing middle class, and the regional popularity of fermented foods are contributing to mass adoption.

Key global innovators and distributors include Yakult Honsha Co., Ltd., BioGaia AB, Nestle S.A., Danone S.A., and Chr. Hansen Holding A/S. Leading firms are sharpening their competitive edge through strain diversification and transparent labeling, appealing to health-conscious and allergen-sensitive consumers. They're also investing in clinical trials to validate gut-brain, immune, and digestive health claims. Format innovation-with vegan capsules, delayed-release options, gummies, and powders-is broadening access across demographics. Companies are expanding e-commerce channels and direct-to-consumer models while forming partnerships with healthcare professionals and food brands to boost credibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Format, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Capsules

- 5.2.1 Vegetarian capsules

- 5.2.2 Gelatin capsules

- 5.2.3 Delayed-release capsules

- 5.2.4 Others

- 5.3 Tablets

- 5.3.1 Chewable tablets

- 5.3.2 Enteric-coated tablets

- 5.3.3 Others

- 5.4 Powders

- 5.4.1 Single-serve sachets

- 5.4.2 Bulk containers

- 5.4.3 Others

- 5.5 Liquids

- 5.5.1 Shots

- 5.5.2 Drops

- 5.5.3 Others

- 5.6 Gummies

- 5.6.1 Gelatin-based

- 5.6.2 Pectin-based

- 5.6.3 Others

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Probiotic Strain, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Lactobacillus

- 6.2.1 L. acidophilus

- 6.2.2 L. rhamnosus

- 6.2.3 L. plantarum

- 6.2.4 L. casei

- 6.2.5 L. reuteri

- 6.2.6 Others

- 6.3 Bifidobacterium

- 6.3.1 B. bifidum

- 6.3.2 B. longum

- 6.3.3 B. lactis

- 6.3.4 B. breve

- 6.3.5 Others

- 6.4 Streptococcus

- 6.4.1 S. thermophilus

- 6.4.2 Others

- 6.5 Bacillus

- 6.5.1 B. coagulans

- 6.5.2 B. subtilis

- 6.5.3 Others

- 6.6 Saccharomyces

- 6.6.1 S. boulardii

- 6.6.2 Others

- 6.7 Multi-strain formulations

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By CFU Count, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Below 1 billion CFU

- 7.3 1-10 billion CFU

- 7.4 10-50 billion CFU

- 7.5 Above 50 billion CFU

Chapter 8 Market Estimates and Forecast, By Consumer Demographics, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Adults

- 8.2.1 18-34 Years

- 8.2.2 35-54 Years

- 8.2.3 55+ Years

- 8.3 Children

- 8.3.1 Infants (0-2 Years)

- 8.3.2 Children (3-12 Years)

- 8.3.3 Adolescents (13-17 Years)

Chapter 9 Market Estimates and Forecast, By Health Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Digestive health

- 9.2.1 Irritable bowel syndrome (IBS)

- 9.2.2 Inflammatory bowel disease (IBD)

- 9.2.3 Antibiotic-associated diarrhea

- 9.2.4 Others

- 9.3 Immune health

- 9.4 Women's health

- 9.5 Weight management

- 9.6 Brain health

- 9.7 Oral health

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 Retail pharmacies

- 10.3 Health & wellness stores

- 10.4 Supermarkets & hypermarkets

- 10.5 Online retail

- 10.5.1 E-commerce platforms

- 10.5.2 Brand websites

- 10.5.3 Online pharmacies

- 10.6 Direct selling

- 10.7 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Chr. Hansen Holding A/S

- 12.2 Danone S.A. (Activia, Actimel)

- 12.3 Yakult Honsha Co., Ltd.

- 12.4 Nestle S.A. (Garden of Life)

- 12.5 Probi AB

- 12.6 BioGaia AB

- 12.7 Probiotics International Ltd (Protexin)

- 12.8 Lallemand Inc.

- 12.9 DuPont (IFF)

- 12.10 Lifeway Foods, Inc.

- 12.11 Morinaga Milk Industry Co., Ltd.

- 12.12 Bifodan A/S

- 12.13 Culturelle (i-Health, Inc.)

- 12.14 Jarrow Formulas, Inc.

- 12.15 NOW Foods