|

市場調査レポート

商品コード

1644451

ASEANのeコマースロジスティクス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)ASEAN E-commerce Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ASEANのeコマースロジスティクス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

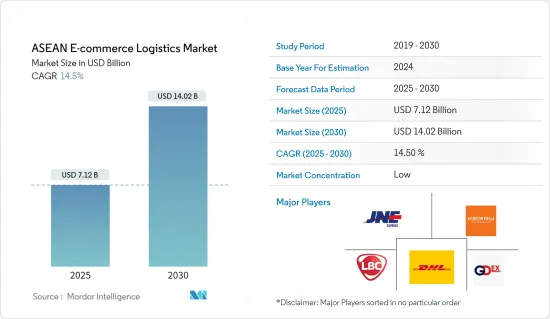

ASEANのeコマースロジスティクス市場規模は2025年に71億2,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは14.5%で、2030年には140億2,000万米ドルに達すると予測されます。

COVID-19が東南アジア全域でeコマースの急増を引き起こしたとき、宅配業者は成功を維持・拡大するために奮闘しました。東南アジアのインターネット小売額は4,950億米ドルから推定5億8,100万米ドルに増加しました。倉庫の広さは通常1,000平方メートルだが、1万平方メートルや1万5,000平方メートルの立体倉庫の需要があった。

東南アジアはeコマースで急成長を遂げようとしています。東南アジアの5カ国は、世界で最も急成長しているeコマース市場のひとつであり、上位10カ国の半分を占めています。東南アジアは以前はeコマースの後塵を拝し、中国や日本の影に隠れていました。しかし、今ではほぼすべての国がモバイル機器を持ち、その結果インターネットにアクセスできるようになった。5カ国のモバイル普及率はいずれも100%に近いです。

業界筋によると、マレーシアの人口は3,280万人。基準年のeコマース売上高は、前年比15%増の63億米ドル。最も人気のあるマーケットプレースはShopeeで、JDと提携するローカルプラットフォームPGMallがこれに続く。最も人気のあるマーケットプレースはJD、Shopee、Lazadaです。主な商品カテゴリーは電子機器とパーソナルケアです。

eコマースの急成長がこの市場の物流開拓を後押ししているとはいえ、東南アジアの複雑な地形を持ついくつかの国々にとっては、これは依然として課題です。ロジスティクスの運営管理はeコマース・ビジネスの課題です。世界の大流行から経済が回復し、所得水準が上昇するにつれて、アジア域内市場は拡大し、それに伴い、eコマース分野の隆盛に後押しされたエクスプレス・ロジスティクス・サービスの需要も増加すると予想されます。

ASEANのeコマースロジスティクス市場の動向

eコマースの成長が市場を牽引

東南アジアではeコマースが急増しています。同地域の消費動向は、デジタル決済分野の大幅な成長により、拡大を目指すオンライン小売業者にとって刺激的な機会を生み出しています。商品カテゴリーの中で、この地域で最も人気があるのは電子機器です。テレビ、スマートフォン、ノートパソコン、USBメモリー、パワーバンクなどがこのカテゴリーのベストセラーです。

一方、衣料品、ファッション小物、ベビー用品、家具も遠く及ばず、東南アジア市場ではこれらの分野の売上が過去最高を記録しています。eコマース・プラットフォームのライブストリーミングは、東南アジア市場で急速に拡大しています。統計によると、マレーシアとシンガポールでは、eコマース・プラットフォームでのライブ・ストリーミングの視聴時間が200%増加しました。この動向はフィリピンにも波及し、60%のブランドが店舗への集客を増やすためにライブ販売を利用しています。

ソーシャル・コマースの支援、インターネットの普及、一部の製品カテゴリーに対する需要が、ASEAN諸国におけるeコマースの成長を牽引しています。オンライン・チャネルは、各国の国内小売企業にとって、大きなビジネスチャンスとなっています。これらの国々は、インフラやロジスティクス・サービスで遅れをとっているにもかかわらず、このチャネルを通じた製品に対する需要が、投資家を市場に深く飛び込むよう誘い込んでいます。

市場を支える東南アジアのインフラ開発

東南アジアのインフラニーズに対する世界の関心の高まりは、発展途上国にとって刺激的であると同時に懸念材料でもあります。G7は米国主導の「Build Back Better World」(B3W)イニシアチブを2021年に支持すると発表し、欧州連合(EU)は「Globally Connected Europe」と名付けられたインフラ戦略を発表しました。

これらの構想は、開発途上国の40兆米ドルにのぼるインフラ格差に対処することを目的としているが、中国の「一帯一路構想」と競合するように見えることから、地政学的な懸念も生じています。東南アジア諸国政府は、投資決定をめぐる地政学的な対立に巻き込まれることを望んでいないです。莫大な資本が必要なことは別として、発展途上の東南アジア諸国のインフラは、貧困や常に存在する気候変動の脅威のために、より多くの問題を抱えています。インフラは改善されたとはいえ、さらに多くのことが必要とされています。人口の大半は、電気、安全な飲料水、安全な道路を利用できないです。

計画が不十分で交通渋滞の多い都市では、それだけで日々の生産性の低下、燃料の浪費、ストレスの増大などの犠牲を強いられています。さらに、国際通貨基金(IMF)は、非効率のために各国がインフラ支出のおよそ3分の1を無駄にしていることを発見しました。

一方、2023年、東南アジアではインフラ分野への投資が増加しています。例えば、2023年3月、アジアインフラ投資銀行(AIIB)は、セラヤ東南アジアエネルギー転換・デジタルインフラ基金(基金)に1億2,000万米ドル以上を供与しました。この投資は、同地域のグリーン・エネルギーへの移行とテクノロジーを活用したインフラ開発を強化することを目的としており、アジア域内の国境を越えたデジタル接続の改善も期待されています。さらに、A.P.モラー・グループは2023年2月、南アジアと東南アジアのさまざまなインフラ・プラットフォームに7億5,000万米ドル以上の投資を計画しています。このように、同地域におけるインフラ部門の成長は、eコマースロジスティクス・サービス・プロバイダーにとって大きなビジネスチャンスを生み出すと期待されています。

ASEANのeコマースロジスティクス業界の概要

ASEANのeコマースロジスティクス市場情勢は、地域全体でロジスティクス・サービスに対する需要が急拡大しているため断片化されており、各社はこの機会を捉えようと競争力を高めています。その結果、国際的なプレーヤーは、新しい物流センターやスマート倉庫の開設など、地域の物流ネットワークを確立するための戦略的投資を行っています。大手企業には、JNEエクスプレス、LBCエクスプレス、GDエクスプレス、ケリーエクスプレス、ニンジャバン、ベストエクスプレスなどがあります。コスト競争力を維持するため、オンライン事業を展開する企業は、社内で配送スタッフを雇用する代わりに、サードパーティーの宅配業者と協力することを好みます。その結果、世界企業はこの地域の成長機会を狙って積極的に投資しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析方法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学

- 現在の市場シナリオ

- 市場力学

- 促進要因

- eコマース分野の成長

- 抑制要因

- 複雑な製品返品

- 機会

- デジタルインフラへの投資の増加

- 促進要因

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 技術動向と自動化への洞察

- 政府の規制と取り組み

- サプライチェーン/バリューチェーン分析

- eコマース市場の洞察

- スポットライト-eコマースロジスティクスの主要拠点

- リバース/リターン・ロジスティクスへの洞察

- COVID-19の市場への影響

第5章 市場セグメンテーション

- サービス別

- 輸送

- 倉庫・在庫管理

- 付加価値サービス(ラベリング、パッケージングなど)

- ビジネス別

- B2B(企業間取引)

- B2C(企業対消費者)

- 仕向地別

- 国内

- 国際/クロスボーダー

- 商品別

- ファッション・アパレル

- 家電

- 家電製品

- 家具

- 美容・パーソナルケア製品

- その他(玩具、食品など)

- 国別

- シンガポール

- タイ

- ベトナム

- インドネシア

- マレーシア

- フィリピン

- その他のASEAN諸国

第6章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- Deutsche Post DHL Group

- United Parcel Service

- FedEx Corporation

- Pos Indonesia

- PT Jalur Nugraha Ekakurir(JNE Express)

- PT Global Jet Express(J&T Express)

- J&T Express

- Flash Express

- Best Express

- Kerry Express

- PT Citra Van Titipan Kilat(TIKI)

- Giao Hang Nhanh

- Ninja Van

- LBC Express

- GD Express Sdn Bhd*

- その他の企業

第7章 市場の将来

第8章 付録

- マクロ経済指標(活動別GDP分布、運輸・宅配業界の経済貢献度)

- 貿易統計-製品別、原産国・仕向国別の輸出入統計

The ASEAN E-commerce Logistics Market size is estimated at USD 7.12 billion in 2025, and is expected to reach USD 14.02 billion by 2030, at a CAGR of 14.5% during the forecast period (2025-2030).

When COVID-19 caused a surge in e-commerce throughout Southeast Asia, delivery companies struggled to sustain and expand their success. Southeast Asia's internet retail value increased from USD 495 billion to an estimated USD 581 million. Warehouses were typically 1,000 sq. mt. in size, but demand was for multi-level warehouses that could be 10,000 or 15,000 sq. mt.

Southeast Asia is poised for rapid growth in e-commerce. Five Southeast Asian countries are among the world's fastest-growing e-commerce markets, accounting for half of the top ten. Southeast Asia was previously an e-commerce laggard, digitally overshadowed by China and Japan. However, nearly all of them now have mobile devices and, as a result, internet access. The five countries' mobile penetration rates are all close to 100%.

According to industry sources, Malaysia has a population of 32.8 million people. E-commerce sales in the base year were USD 6.3 billion, up 15% from the previous year. Shopee is the most popular marketplace, followed by PGMall, a local platform that collaborates with JD. The most popular marketplaces are JD, Shopee, and Lazada. The main product categories are electronics and personal care.

Even though the rapid growth of e-commerce is driving logistics development in this market, this remains a challenge for a few countries with complex topography in Southeast Asia. Logistics operation management is a challenge for e-commerce businesses. As economies recover from the global pandemic and income levels rise, the intra-Asian market is expected to expand, with a corresponding increase in demand for express logistics services propelled by the thriving e-commerce sector.

ASEAN E-commerce Logistics Market Trends

E-commerce growth is driving the market

Southeast Asia is experiencing a surge in e-commerce. Consumer trends in the region are creating exciting opportunities for online retailers looking to expand due to massive growth in the digital payments sector. Among product categories, electronics are the most popular in the region. TVs, smartphones, laptops, USB drives, power banks, and other items are among the best-sellers in this category.

On the other hand, clothing, fashion accessories, baby products, and furniture are not far behind, with Southeast Asian markets experiencing higher-than-ever sales in these segments. Live streaming for e-commerce platforms is rapidly expanding in the Southeast Asian market. Statistics show live streaming hours on e-commerce platforms increased by 200% in Malaysia and Singapore. The trend spread to the Philippines, where 60% of brands use live selling to attract more customers to their stores.

The support of social commerce, internet penetration, and demand for some product categories drives the growth of e-commerce in ASEAN countries. The online channel has created a huge opportunity for domestic retailers in various countries. Even though these countries lag in infrastructure and logistics services, the demand for products through the channel is luring investors to dive deeply into the market.

Infrastructure development in south-east Asia supporting the market

The growing global interest in Southeast Asia's infrastructure needs has been exciting and concerning for developing countries. The G7 announced its support for the US-led 'Build Back Better World' (B3W) initiative in 2021, while the European Union unveiled its infrastructure strategy, dubbed 'Globally Connected Europe.'

These initiatives aim to address developing countries' USD 40 trillion infrastructure gap, but they also raise geopolitical concerns by appearing to compete with China's Belt and Road Initiative. Southeast Asian governments do not want to be caught in a geopolitical crossfire over investment decisions. Apart from the massive amounts of capital required, infrastructure in developing Southeast Asian countries suffers more due to poverty and the ever-present threat of climate change. While the infrastructure has improved, more is needed. The majority of the population lacks access to electricity, safe drinking water, and safe roads.

Cities with poor planning and traffic congestion alone cost them a daily loss of productivity, wasted fuel, and increased stress. In addition, the International Monetary Fund (IMF) discovered that countries waste roughly one-third of their infrastructure spending due to inefficiencies.

Meanwhile, in 2023, Southeast Asia witnessed an increasing number of investments in the infrastructure sector. For instance, in March 2023, the Asian Infrastructure Investment Bank (AIIB) granted more than USD120 million to the Seraya Southeast Asia Energy Transition and Digital Infrastructure Fund (the Fund). This investment is aimed at enhancing the region's transition to green energy and technology-enabled infrastructure development, which is also expected to improve cross-border digital connectivity within Asia. Moreover, in February 2023, A.P. Moller Group planned to invest more than USD 750 million in various infrastructure platforms in South and Southeast Asia. Thus, the growing infrastructure sector in the region is expected to create a huge opportunity for e-commerce logistics service providers.

ASEAN E-commerce Logistics Industry Overview

The ASEAN e-commerce logistics market landscape is fragmented as the demand for logistics services is growing rapidly across the region, and companies are becoming more competitive to capture this opportunity. As a result, international players are making strategic investments to establish a regional logistics network, such as opening new distribution centers and smart warehouses. Some leading players include JNE Express, LBC Express, GD Express, Kerry Express, Ninja Van, and Best Express. To maintain cost competitiveness, companies that operate online prefer to work with third-party courier providers instead of hiring in-house delivery staff. As a result, global companies are actively investing in targeting growth opportunities in the region.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Method

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Growing E-commerce Sector

- 4.2.2 Restraints

- 4.2.2.1 Complicated Product Returns

- 4.2.3 Opportunities

- 4.2.3.1 Increasing Investments in Digital Infrastructure

- 4.2.1 Drivers

- 4.3 Value Chain / Supply Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Insights into Technological Trends and Automation

- 4.6 Government Regulations and Initiatives

- 4.7 Supply Chain/Value Chain Analysis

- 4.8 Insights into the E-commerce Market

- 4.9 Spotlight - Key Hubs for E-commerce Logistics

- 4.10 Insights into Reverse/Return Logistics

- 4.11 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.2 Warehousing and Inventory Management

- 5.1.3 Value-added Services (Labeling, Packaging, etc.)

- 5.2 By Business

- 5.2.1 B2B (Business-to-Business)

- 5.2.2 B2C (Business-to-Consumer)

- 5.3 By Destination

- 5.3.1 Domestic

- 5.3.2 International/Cross-border

- 5.4 By Product

- 5.4.1 Fashion and Apparel

- 5.4.2 Consumer Electronics

- 5.4.3 Home Appliances

- 5.4.4 Furniture

- 5.4.5 Beauty and Personal Care Products

- 5.4.6 Other Products (Toys, Food Products, etc.)

- 5.5 By Country

- 5.5.1 Singapore

- 5.5.2 Thailand

- 5.5.3 Vietnam

- 5.5.4 Indonesia

- 5.5.5 Malaysia

- 5.5.6 Philippines

- 5.5.7 Rest of the ASEAN

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Deutsche Post DHL Group

- 6.2.2 United Parcel Service

- 6.2.3 FedEx Corporation

- 6.2.4 Pos Indonesia

- 6.2.5 PT Jalur Nugraha Ekakurir (JNE Express)

- 6.2.6 PT Global Jet Express (J&T Express)

- 6.2.7 J&T Express

- 6.2.8 Flash Express

- 6.2.9 Best Express

- 6.2.10 Kerry Express

- 6.2.11 PT Citra Van Titipan Kilat (TIKI)

- 6.2.12 Giao Hang Nhanh

- 6.2.13 Ninja Van

- 6.2.14 LBC Express

- 6.2.15 GD Express Sdn Bhd*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution by Activity, Contribution of Transport/Courier Industry to Economy)

- 8.2 Trade Statistics - Export and Import Statistics by product and by country of origin/destination