|

市場調査レポート

商品コード

1644313

米国のスマートTV:市場シェア分析、産業動向・統計、成長予測(2025~2030年)US Smart TV - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のスマートTV:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

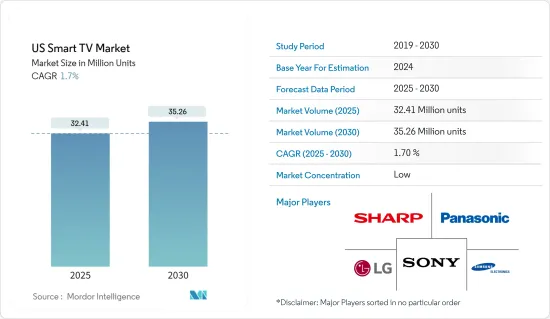

米国のスマートTVの市場規模は2025年に3,241万台と推計され、2030年には3,526万台に達すると予測され、市場推計・予測期間(2025~2030年)のCAGRは1.7%です。

OTTサービスの普及が進み、典型的なストリーミング・エンターテインメント製品としてスマートTVが好まれるようになったこと、米国と中国の貿易紛争により、中国製造に依存しているスマートTVベンダーが安全在庫構築のために出荷を拡大するようになったことが、米国におけるスマートTVの成長を促進する2つの主な要因です。

主なハイライト

- Apple TV、Amazon Fire TV、Google Chromecastなどのストリーミングメディアが消費者の視聴体験を変えつつあります。複数のメーカーがOTT(オーバー・ザ・トップ)コンテンツやデバイスのプロバイダーと提携し、セットトップボックス不要の内蔵機能を提供しています。例えば、TCL CorporationはRoku Inc.と提携し、4K HDR Roku TVを発表しました。

- さらに、高速ブロードバンドアクセスの増加に伴い、オンライン素材の視聴者数は近年劇的に拡大しています。さらに、拡大するエレクトロニクス分野では、音声コマンドや計算知能を含むさまざまな技術的進歩が融合し始め、スマートTVを含むインテリジェント機器への需要が高まっています。

- さらに、大手市場開拓企業による製品開発の増加が、調査期間中のセグメント成長に寄与すると予想されます。例えば、2022年3月-LG Displayは、10日(現地時間)にカリフォルニア州サンノゼで3日間開催されたSociety for Information Display(SID)のDisplay Week 2022で、MLA技術を搭載した77インチ8K OLED TVパネルを初めて発表しました。LGディスプレイの77インチ8K有機ELテレビは、世界で初めてEX技術とMLAを採用しました。

- さらに、拡大し続ける動画ストリーミング・サービスの世界は、それぞれが独占的なテレビ番組や映画を提供し、視聴者を惹きつけています。コンシューマー・テクノロジー協会によると、動画ストリーミング・サービスへの支出は2022年に470億米ドルに達し、2021年比で7%増加しました。

- 例えば、2021年には8Kテレビメーカーが本格的に始動しました。サムスン8KテレビのQN900A、QN800A、QN700Aといったお決まりの8K解像度画面トリオに加え、LGも自社のMini LED技術を搭載した8K対応モデルをいくつか発表しました。TCLの6シリーズ8K QLEDは米国で最も安価な8Kテレビです。

- さらに、超高速インターネットの普及と高効率のネットワーク・インフラは、スマートTVの解像度に好影響を与えると予想されます。例えば、米国連邦政府は2021年までに全国に集中型5G無線ネットワークを構築する計画です。最近、ホワイトハウスは米国における5G確保のための国家戦略を発表し、主に国内外の5Gインフラのアップグレードと安全確保に焦点を当てています。

- COVID-19の大流行は、すべての消費者のライフスタイルや日常に劇的な影響を与えています。避難命令や在宅勤務の義務化によって、家庭内でのビデオ消費はかつてない水準に達しています。新興経済国でのスマートフォンユーザーの増加は、スマートTVにとって重要な起爆剤となっています。

米国のスマートTV市場動向

55インチ以上の画面サイズへの需要の高まり

- 米国では、小型・中型テレビ画面から大型テレビ画面へのシフトが見られます。これは主に一人当たりの所得が増加していることに加え、高級品や贅沢品への買い替えが進んでいることが背景にあります。米国商務省によると、米国の一人当たり個人所得は昨年6万3,444米ドルで、前年より増加しました。

- さらに、オンライン・ストリーミング・アプリの需要は、オーディオとビデオの品質における没入体験という動向に消費者の焦点を移し、これが大画面スマートTVの大きな原動力となっています。

- さらに、サウンドバー、ストリーミング・プレーヤー、マウントが2桁の伸びを示したように、テレビはパンデミックの間、人々の隠れ家として機能してきました。大型ディスプレイの販売を手がけるロサンゼルスのVideo &Audio Center店舗では、98インチのサムスン製8Kテレビが予想を上回る売れ行きを示しました。6月にサンタモニカ店で6万米ドルの8Kディスプレイの販売を開始したところ、すぐに3台売れました。それ以来、同チェーンはロサンゼルス地域の他の4店舗にも販売を拡大しています。

- サムスン電子アメリカによると、75インチ以上のスクリーンは市場で最も急成長しているセグメントのひとつとなっています。消費者が自宅で過ごす時間を増やし、自宅で仕事をし、さらには子供に教えるようになったため、自宅をより快適で楽しいものにするための住宅設備投資により力を入れるようになった。

- 業界各社も、競争力を維持するためにストリーミング・サービスを提供しています。例えば、ディズニーはDisney+にHuluとESPN+をバンドルして月額12.99米ドル(月額5米ドル割引)で利用できるオプションを消費者に提供しています。CBSはShowtimeとCBS All Accessをバンドルして月額14.99米ドルから提供している(月額2米ドル割引)。上記のすべての要因が、この地域におけるスマートTVの需要と普及を高めています。

- 55インチ以上の画面のスマートTVの需要は以前からあったが、COVID-19の大流行の発生により、より大きな画面のスマートTVの必要性へとシナリオが変化しました。春には、米国全土で州や地域の規制により自宅待機が推奨されたため、消費者は通常ホリデーシーズンに見られる水準でテレビを購入しました。

著しい成長を遂げるOLEDセグメント

- テレビ業界は最近、OLEDディスプレイの使用を拡大しています。OLEDがディスプレイ市場の将来展望となり、ほとんどあらゆる場所で最良の方法で使用されるようになったため、テレビメーカーはOLEDディスプレイをテレビに採用するようになっています。テレビ業界における採用の増加は、地域のスマートテレビ市場におけるOLEDパネルの成長をさらに増大させると思われます。

- Consumer Technology Associationによると、米国のOLED TV工場の売上は2021年の29億8,000万米ドルから2022年には33億米ドルに11%増加し、市場成長をさらに促進しています。

- 超高精細(UHD)スマートテレビに量子ドットLED(QLED)などの革新的な技術が採用されたことで、予測期間中の同分野の需要に拍車がかかると予想されます。このレンジのテレビは、他と比べて普及率が高いです。例えば、2021年6月、LG Electronicsは米国で世界初の83インチOLEDテレビを発表しました。83C1は4K OLEDテレビ業界で最も巨大な製品でもあります。

- さらに、OLEDテレビの価格引き下げは、収益性の高い拡大展望を生み出す可能性があります。米国エネルギー省によると、米国における有機発光ダイオード(OLED)パネル製造の人件費は、2025年までにOLEDパネル生産1平方メートル当たり5米ドルまで低下すると予想されています。

- 次年度のOLED技術革新の改善と原材料コストの低下により、OLEDテレビのコストは低下し、当面の業界を牽引する可能性が高いです。さらに、新たな業界参加者の出現とOLEDテレビの大量生産は、OLEDテレビの価格を引き下げ、OLEDディスプレイの需要を促進します。さらに、2021年12月、サムスンは量子ドット/OLED技術(通称QD-OLED)を採用したハイブリッドTVに賭けた。サムスン電子はLGディスプレイからパネルを購入しているが、社内のディスプレイ部門が量子ドット/OLED(QD-OLED)TVパネルを製造する計画を明らかにしました。

米国のスマートTV産業の概要

米国のスマートTV市場は複数のプレーヤーで構成されています。この業界は、消費者の関心が非常に高いため、有利な投資機会と見られています。各社は将来の技術に投資し、実質的な専門知識を得て持続可能な競争優位性を獲得しています。

- 2022年1月- シャープ・ホーム・エレクトロニクス・カンパニー・オブ・アメリカは、シンプルでカスタマイズ可能なホーム画面、数千のストリーミング・チャンネルへのアクセス、200以上のライブTVチャンネルを含むプレミアム・ホーム・エンターテイメント体験を提供するTV専用ストリーミング・プラットフォームであるRoku TVと協業しました。この協業は、シャープのホームエンタテインメント革新の長い歴史に基づくものです。

- 2021年8月- 日立製作所は、大画面量子ドット(QLED)Android TVTM OS搭載のQシリーズを発表しました。フレームレスの4K HDRテレビで、画面サイズは65インチ/55インチ/50インチ/43インチ。ドルビービジョンHDRや内蔵スピーカーなどの機能によりオーディオビジュアル性能を強化し、より没入感のあるホームエンターテインメント体験を提供します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 業界バリューチェーン分析

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 新興国における可処分所得の増加

- ビデオオンデマンドサービスの動向上昇

- 市場の課題

- 新興経済諸国における高速インターネットの普及不足

第6章 市場セグメンテーション

- スクリーンサイズ(対角)別

- 30~45インチ

- 45~55インチ

- 55インチ以上

- 解像度タイプ別

- 4K UHDテレビ

- フルHDテレビ

- ハイビジョンテレビ

- パネルタイプ別

- LCD

- LED

- 有機EL

- QLED

- 価格帯別

- 1,000米ドル未満

- 1,000~2,000米ドル

- 2,000~3,000米ドル

- 3,000米ドル以上

- オペレーティングセグメント別

- Android

- Tizen

- WebOS

- Roku

- その他のOS

第7章 競合情勢

- 企業プロファイル

- LG Electronics Inc.

- Samsung Electronics Co. Ltd

- Sony Corporation

- Panasonic Corporation

- Sharp Corporation

- VIZIO Inc.

- Hisense Group Co. Ltd

- Koninklijke Philips NV

- Insignia Systems Inc.

- Haier Group Corporation

- Hitachi Ltd

- Westinghouse Electric Corporation

- TCL Technology

第8章 ベンダー市場ランキング分析

第9章 投資分析

第10章 市場の将来

The US Smart TV Market size is estimated at 32.41 million units in 2025, and is expected to reach 35.26 million units by 2030, at a CAGR of 1.7% during the forecast period (2025-2030).

The increasing adoption of OTT services leading to the preference of smart TVs as a typical streaming entertainment product and the Us-China trade dispute prompting smart TV vendors dependent on Chinese manufacturing to expand shipments for building safety stocks are the two major factors driving the growth of smart TV in the United States.

Key Highlights

- Streaming media such as Apple TV, Amazon Fire TV, and Google Chromecast are changing the consumers' viewing experience. Several manufacturers are teaming up with OTT (over-the-top) content and device providers to provide built-in features with no further requirement of a set-top box. For instance, TCL Corporation has teamed up with Roku Inc. and introduced a 4K HDR Roku TV.

- Furthermore, viewership of online material has expanded dramatically in recent years as high-speed broadband access has increased. Furthermore, the expanding electronics sector has started merging different technical advancements, including voice command and computational intelligence, with growing demand for intelligent gadgets, including smart TVs.

- Additionally, the increasing product development by major market players is expected to contribute to segment growth over the study period. For instance, in March 2022 - LG Display first introduced a 77-inch 8K OLED TV panel with MLA technology at the Society for Information Display's (SID) Display Week 2022, which was held in San Jose, California, on the 10th (local time) for three days. LG Display's 77-inch 8K OLED TV was the first in the world to use EX technology and MLA.

- Further, an ever-expanding universe of video streaming services, each with its exclusive TV shows and movies, is attracting a growing audience. According to the Consumer Technology Association, spending on video streaming services reached USD 47 billion in 2022, a 7% increase over 2021.

- For instance, 2021 saw 8K TV makers get into gear. Alongside the usual trio of 8K resolution screens from Samsung 8K TV, such as QN900A, QN800A, and QN700A, LG also brought several 8K-capable models that feature their Mini LED technology. Other brands are also launching, such as TCL's 6-Series 8K QLED, proving the cheapest 8K TV in the United States.

- Moreover, the increasing penetration of ultra-high-speed internet and highly efficient network infrastructure are expected to favorably impact the Smart TV Resolutions. For instance, the US federal government plans to build a centralized 5G wireless network nationwide by 2021. Recently, the White House released its National Strategy to Secure 5G in the US, mainly focusing on upgrading and securing 5G infrastructure at home and abroad.

- The COVID-19 pandemic has drastically impacted the lifestyles and routines of all consumers. Shelter-in-place orders and work-at-home mandates have driven in-home video consumption to unprecedented levels. The growing number of smartphone users in emerging economies has acted as a significant catalyst for smart TV as users look to continue their streaming content consumption on more giant screens when at home.

US Smart TV Market Trends

Boosting Demand for 55 Inches and above Screen Size

- The United States has seen a shift from small- and medium-sized TV screens to big screens. This is mainly driven by the increasing per capita income, followed by the growing change for premium and luxurious products. According to the US Department of Commerce, per capita, personal income in the United States was USD 63,444 last year, an increase from the previous year.

- Moreover, the demand for online streaming apps has shifted the consumers' focus toward the trend of an immersive experience in audio and video quality, which has been a significant driver for smart TVs with larger screens.

- Furthermore, TVs have served as a retreat for people during the pandemic, as the market witnessed a double-digit increase in soundbars, streaming players, and mounts. At Video & Audio Center stores in Los Angeles, a retail store carrying the sale of larger displays, a 98-inch Samsung 8K TV exceeded expectations. When the retailer began selling the USD 60,000 8K display at its Santa Monica store in June, it sold three quickly. Since then, the chain has expanded sales of the display to its other four LA-area stores.

- According to Samsung Electronics America, screens larger than 75 inches have become one of the market's fastest-growing segments. As consumers started spending more time at home, working from home, and even teaching their kids, they increased their focus on investing more in home improvement projects to make their homes more comfortable and enjoyable.

- The industry players are also offering streaming services to remain competitive. For instance, Disney gives consumers the option to bundle Disney+ with Hulu and ESPN+ for USD 12.99 per month (a USD 5 per month discount). CBS offers a bundle of Showtime and CBS All Access starting at USD 14.99 per month (a USD 2 per month discount). All the above factors are increasing the demand and adoption of Smart TVs in the region.

- Though the demand for smart TVs with 55 inches above-sized screens was present before, the outbreak of the COVID-19 pandemic transformed the scenario into a need for smart TVs with much bigger screens. During the spring, as state and local regulations across the United States recommended people stay at home, consumers purchased televisions at levels usually seen during the holiday season.

OLED Segment to Witness Significant Growth

- The television industry has ramped up its use of OLED displays recently. With OLED becoming the future of the display market and being used almost everywhere in the best possible ways, television manufacturers are increasingly using OLED displays for televisions. The increasing adoption in the television industry will further augment the OLED panel's growth in the regional smart tv market.

- According to the Consumer Technology Association, US OLED TV factory revenue increased by 11% to USD 3.3 billion in 2022 from USD 2.98 billion in 2021, further driving the market growth.

- The adoption of innovative technologies, such as Quantum dot LEDs (QLEDs) across Ultra-high-definition (UHD) Smart TVs, is expected to fuel the segment demand over the forecast period. Televisions in this range have high penetration rates compared to the others. For instance, in June 2021, LG Electronics introduced the first global 83-inch OLED television in the United States. The 83C1 is also the most giant 4K OLED TV industry.

- Furthermore, price reductions in OLED TVs may create profitable expansion prospects. According to the US Department of Energy, labor costs for organic light-emitting diode (OLED) panel fabrication in the United States is expected to fall to USD 5 per square meter of OLED panel produced by 2025.

- Improvements in OLED innovation in the following years, as well as lower raw material costs, are likely to lower the expense of OLED TVs, propelling the industry in the foreseeable future. Additionally, the emergence of new industry participants and the mass manufacturing of OLED TVs will help reduce OLED TV prices, driving the demand for OLED displays. In addition, in December 2021, Samsung placed its bets on hybrid TVs featuring quantum dot/OLED technology, commonly called QD-OLED. Although Samsung Electronics purchases panels from LG Display, the company revealed plans for its in-house display division to manufacture the quantum dot/OLED (QD-OLED) TV panels.

US Smart TV Industry Overview

The United States smart TV market consists of several players. This industry is viewed as a lucrative investment opportunity due to enormous consumer interest. The companies are investing in future technologies to gain substantial expertise and achieve sustainable competitive advantage.

- January 2022 - Sharp Home Electronics Company of America collaborated with Roku TV, a TV-specific streaming platform that provides a premium home entertainment experience that includes a simple, customizable home screen, access to thousands of streaming channels, and over 200 live TV channels. This collaboration builds on Sharp's long history of home entertainment innovation.

- August 2021 - Hitachi introduced the Q series of large-screen Quantum Dot (QLED) Android TVTM OS devices. The frameless 4K HDR TVs, available in 65"/55"/50"/43" screen sizes, bring the user closer to the on-screen action while delivering higher levels of color accuracy and detail thanks to QLED technology. They enhance the audio-visual performance with features such as Dolby Vision HDR and integrated speakers to provide a more immersive home entertainment experience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Disposable Income across Emerging Economies

- 5.1.2 Rising Trend of Video-on-demand Service

- 5.2 Market Challenges

- 5.2.1 Lack of High-speed Internet Penetration in Developing Economies

6 MARKET SEGMENTATION

- 6.1 By Screen Size (Diagonal)

- 6.1.1 30-45 Inches

- 6.1.2 45-55 Inches

- 6.1.3 55 Inches and above

- 6.2 By Resolution Type

- 6.2.1 4K UHD TV

- 6.2.2 Full HD TV

- 6.2.3 HDTV

- 6.3 By Panel Type

- 6.3.1 LCD

- 6.3.2 LED

- 6.3.3 OLED

- 6.3.4 QLED

- 6.4 By Pricing Range

- 6.4.1 Under USD 1,000

- 6.4.2 USD 1,000 to USD 2,000

- 6.4.3 USD 2,000 to USD 3,000

- 6.4.4 USD 3,000 and Above

- 6.5 By Operating Segment

- 6.5.1 Android

- 6.5.2 Tizen

- 6.5.3 WebOS

- 6.5.4 Roku

- 6.5.5 Other Operating Systems

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 LG Electronics Inc.

- 7.1.2 Samsung Electronics Co. Ltd

- 7.1.3 Sony Corporation

- 7.1.4 Panasonic Corporation

- 7.1.5 Sharp Corporation

- 7.1.6 VIZIO Inc.

- 7.1.7 Hisense Group Co. Ltd

- 7.1.8 Koninklijke Philips NV

- 7.1.9 Insignia Systems Inc.

- 7.1.10 Haier Group Corporation

- 7.1.11 Hitachi Ltd

- 7.1.12 Westinghouse Electric Corporation

- 7.1.13 TCL Technology