インドのスマートTVとOTT-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

India Smart TV and OTT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1643132

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

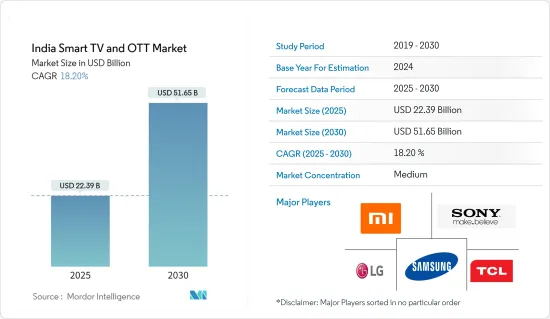

インドのスマートTVとOTT市場規模は2025年に223億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは18.2%で、2030年には516億5,000万米ドルに達すると予測されます。

高速インターネットが簡単に手に入るようになったため、良質なコンテンツを好む視聴者/視聴者は、他のテレビシステムよりもスマートテレビを好むようになりました。また、オーディオビジュアルコンテンツにおけるOTTストリーミングへの憧れの高まりは、インドのスマートTV市場全体に好影響を与えています。

主要ハイライト

- インドのほとんどの地域で高速インターネットが普及し、消費者の嗜好がオンラインコンテンツにシフトしていることが市場成長の原動力となっています。Netflix、Amazon Prime、Hotstarのような動画ストリーミングメディア企業による大規模な投資フローが、有料テレビ加入者の増加につながりました。

- さらに、可処分所得水準の上昇やインターネット普及率の高まりも、スマートTVの販売台数増加に寄与し、市場成長を後押ししています。さらに、IBEFによると、インドのOTTビデオストリーミング市場の市場規模は2023年までに50億米ドルに達すると予測されており、2022年までに8億2,300万米ドルに達し、世界のOTT市場上位10のひとつになると予測されています。

- インドの家庭は転換期にあり、従来のテレビからスマートテレビへの嗜好の変化が見られます。中間所得層のライフスタイルの変化は、所得水準の上昇、意識の向上、新技術の採用、インターネット普及率の上昇に起因します。また、主にTier-IIとTier-III都市における政府の取り組みも、予測期間中のインドスマートTV市場の成長を後押しする主要要因の1つです。

- 一方、オンラインストリーミングに対する需要の高まりは、サービスプロバイダーがOTT領域に進出し、インターネット経由でコンテンツを配信する機会を広げています。Netflix、Amazon、Hotstar、Sony Liv、その他いくつかのストリーミングサービスなどのOTTコンテンツ・参入企業は、DTHやTVケーブルサービスから顧客を引き離して顧客ベースを拡大するため、マーケティングやローカル・コンテンツへの支出を増やしています。また、これらのプラットフォームの多くは、ブロードバンドプロバイダーと提携し、無料のバンドル契約を提供することで、既存のデータユーザーを取り込んでいます。こうした継続的な取り組みが、消費者行動の変化と相まって、同市場の需要拡大を後押ししています。

- COVID-19の発生はディスプレイ産業に悪影響を及ぼし、主要な製造拠点で製造業務が一時的に停止され、生産が大幅に減速しました。Samsung、LG Display、Xiaomiなど、さまざまな主要メーカーが中国、インド、韓国、欧州での製造業務を停止しました。しかし、パンデミック(世界的大流行)の間、人々は長時間自宅に滞在したため、市場は消費者需要の大幅な伸びを目の当たりにしました。さらに、パンデミックによるテレビ視聴傾向の高まりも、引き続き市場に影響を与え、結果として市場の成長につながると予想されます。

インドのスマートテレビとOTT市場の動向

IoTエコシステム全体におけるスマートデバイスの普及が市場成長を牽引

- EricssonのIoT Connections 展望レポートによると、IoT技術によって接続されるデバイスの数は約80%増加し、2021年には3億3,000万台に達します。この成長は、様々なエンドユーザー産業にわたる消費者向けIoT市場の成長を促進した様々なネットワーキング・プロトコルの開発とともに、多くのデバイスやアプリケーションに接続能力が統合されたことに起因しています。

- インターネット普及率の増加も、スマートTVなどIoT対応民生用電子機器のインドにおける普及拡大に寄与しています。Bain and Companyの「Unlocking Digital for Bharat: USD 50 billion Opportunity」によると、インドのアクティブ・インターネットユーザー数は2番目に多く、少なくとも月に1回はウェブを利用する住民は約3億9,000万人にのぼるといいます。さらに、Ericssonの接続展望レポートによると、IoT技術の成長は、4Gと5Gとの大規模なIoT共存を可能にするネットワーク機能の追加によって強化されます。

- さらに、アンビエントインテリジェンスや自動ユーザー支援などの機能により、IoTエコシステムにおけるスマートTVの重要性が高まっていることに加え、インドの人々の可処分所得が増加していることも、市場の成長をさらに後押ししています。

- 民生用電子機器メーカーのSamsung Indiaは最近、LEDテレビセグメントで25%近い成長を見込んでいると発表しました。同社は、適切な提案と新技術を備えた製品を提供することで、テレビ市場全体の約36%のシェアを獲得することを目指しています。このため、同社は2022年4月、インドで超高級2022 Neo QLED 8KとNeo QLED TVを発売しました。

- さらに、シャオミは最近、スマートフォンとスマートTVの新たなパートナー3社を加え、インドでの製造を拡大しました。新たな提携により、Mi Indiaのインドでの製造能力はさらに向上すると予想されます。このような大手ベンダーの開発は、予測期間中の市場成長を押し上げると予想されます。

インターネット・プロトコル・テレビ(IPTV)が市場成長を押し上げる

- ビデオ・オン・デマンド(VOD)はIPTVが提供するダイナミックな機能のひとつです。ビデオデータはリアルタイムストリーミング・プロトコルで伝送されます。VODはここ最近、大きな人気を博しています。その結果、スマートTVの普及率が高まっています。さらに、スマートフォンの普及が進み、データ通信料が安くなったことで、OTTプラットフォームを通じたVoDサービスはインドで有望な成長を示しています。

- OTTとIPTVは、この地域におけるブロードバンド普及率の上昇とコンテンツ消費行動の変化によって牽引力を増しています。この効果は、2021年度のGDP成長率が8.9%だったインドのようなアジア諸国で顕著に見られます。この地域の急速な都市化(インドでは35.39%)と消費力の増加は、家庭でのIPTV導入に重要な役割を果たしています。

- さらに、ケーブルTVやDTH(Direct-to-Home)サービスのデジタル化など、デジタル変革に向けたインド政府の取り組みも、同国におけるIPTVの普及を後押ししています。インドにおけるIPTVのシナリオは、ネットワークサービスプロバイダーの登場によって変化しており、同社はIPTVのライブ配信を無料で顧客に提供しています。他の企業もこれに追随しており、この地域ではモバイルベースのIPTVサービスの需要が増加すると予想されます。

- 市場競合を維持するために、さまざまなベンダーが戦略的な投資を行っています。例えば、2022年7月、インド政府はSony Pictures Networks IndiaとZee Entertainmentの合併承認を発表しました。

インドのスマートTVとOTT産業概要

インドのスマートTVとOTT市場は複数の参入企業で構成されています。この産業は、最近の消費者の関心の高さから、有利な投資機会と見られています。各社は将来的な技術に投資し、実質的な専門知識を得ることで、サステイナブル競争優位性を獲得しています。

- 2022年3月:インドの公共放送局DD Indiaは、テレビ視聴者のゲートウェイであるOTTプラットフォームYupp TVと、DD Indiaチャネルの世界のリーチを拡大するためのMoUを締結しました。情報放送省によると、これは世界のプラットフォームで様々な国際情勢に対するインドの視点を打ち出し、インドの文化や価値観を世界に発表する試みです。

- 2022年1月:Sony Electronicsは、MASTERシリーズ Z9K 8K、X95K 4K Mini LEDモデル、MASTERシリーズ A95K、MASTERシリーズ A90K、A80K 4K OLEDモデル、X90K 4K LEDモデルなど、ブラビアXRテレビシリーズを発表。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査の成果

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- インドの世帯数の多さと相対的に低い普及レベル

- OTT需要を押し上げる消費力の増大とスマートフォン普及率の伸び

- 単価の低下と地域参入企業の参入によるバイヤーの交渉力強化

- 市場抑制要因

- メーカーは税制上の課題と比較的高い買い替え率に直面

第6章 世界のスマートテレビ市場スナップショット(出荷台数予測、主要ベンダーの成長戦略、市場展望、インド市場の主要指標)

第7章 市場セグメンテーション

- OSタイプ(Tizen、WebOS、Android TVなど)

- 価格帯

第8章 インドのOTT事情分析

- 歴史的背景と現在の市場シナリオ

- 市場の分類-放送事業者(HotstarとZEE)、独立系(Alt BalajiとViu)、国際的参入企業(NetflixとAmazon Prime)、通信事業者(Jio、Airtel、Vodafone Play)

- 主要OTT参入企業の加入者ベース(単位:10万人)

- OTT参入企業が採用した主要戦略-コンテンツのローカライズ、手頃な価格設定、戦略的提携、パーソナライゼーション、視聴エンゲージメントのためのデジタルトランスフォーメーションの活用

- インドにおけるOTTとDTHのユーザーベースの比較研究

- 主要ベンダーの主要顧客獲得戦略

- サービスのバンドル化と通信事業者との提携

- プレミアム化とコンテンツ重視のプログラム

- 若年層を対象とした手頃な加入プラン

- 現在のOTTベンダーから判明したその他の主要戦略テーマ

- 地域コンテンツへの旺盛な需要に支えられ、地場参入企業の台頭が期待される

第9章 ベンダー市場シェア分析-INDIA SMART TV(Xiaomi、Samsung、LG、Sonyなど)

第10章 競合情勢

- 企業プロファイル

- Xiaomi Corporation

- Samsung Electronics

- LG Corporation

- Sony Corporation

- TCL Technology

- Vu Technologies

- Honor

- Panasonic Corporation

- Haier

- OnePlus

- Sansui

第11章 投資の展望

第12章 市場展望市場展望

目次

The India Smart TV and OTT Market size is estimated at USD 22.39 billion in 2025, and is expected to reach USD 51.65 billion by 2030, at a CAGR of 18.2% during the forecast period (2025-2030).

As high-speed internet has become easily affordable, viewers/audiences that prefer good quality content prefer smart TVs over other television systems. Also, the increasing admiration for OTT streaming in audiovisual content is impacting the overall smart TV market in a positive manner in India.

Key Highlights

- The shifting consumer preferences toward online content due to the increasing proliferation of high-speed internet in most parts of India provides an impetus to market growth. Substantial investment flows by video streaming media companies, like Netflix, Amazon Prime, and Hotstar, led to an increase in Pay-TV subscribers.

- Furthermore, a rise in disposable income levels and growing internet penetration in the country also contribute to an increase in sales of smart TVs and hence fuelling the market growth. Moreover, according to IBEF, the market size of the OTT video streaming market of India is forecasted to reach USD 5 billion by 2023, and India is projected to become one of the top 10 global OTT markets to reach USD 823 million by 2022.

- Households in India are at a cusp of transition, and a shift in preference has been witnessed from conventional TV sets to smart TV sets. Changing the lifestyle of the middle-income population is attributed to rising income levels, increasing awareness, adoption of new technology, and growing internet penetration. Additionally, government initiatives, primarily in tier-II and tier-III cities, are some of the key factors likely to bolster the growth of the Indian smart TV market during the forecast period.

- On the other hand, the growing demand for online streaming has opened opportunities for service providers to venture into the OTT space and distribute content via the internet. OTT content players, such as Netflix, Amazon, Hotstar, Sony Liv, and several other streaming services, are increasing their spending on marketing and local content to expand their customer base by luring them away from DTH and TV Cable services. Many of these platforms also partner with broadband providers to get the existing data users onboard by offering free bundled subscriptions. These continued efforts, coupled with changing consumer behavior, are driving the increased demand for the market.

- The COVID-19 outbreak affected the display industry negatively, with manufacturing operations temporarily suspended across major manufacturing hubs, leading to a substantial slowdown in production. Various key manufacturers, including Samsung, LG Display, and Xiaomi, suspended their manufacturing operations in China, India, South Korea, and Europe. However, the market has witnessed considerable growth in consumer demand during the pandemic as people stayed at their homes for extended periods. Further, the increased tendency to watch television due to the pandemic is also expected to continue impacting the market, resulting in its growth.

India Smart TV & OTT Market Trends

Increasing Adoption of Smart Devices Across IoT Ecosystem to Drive the Market Growth

- According to Ericsson's IoT Connections Outlook report, the number of devices connected by IoT technologies increased by approximately 80% and reached 330 million in 2021. The growth can be attributed to the integration of connectivity competence in many devices and applications, along with the development of various networking protocols that have advanced the growth of the consumer IoT market across various end-user industries.

- Increasing internet penetration can also contribute to India's widespread expansion of IoT-enabled consumer electronics, such as smart TV. According to Bain and Company's, Unlocking Digital for Bharat: USD 50 billion Opportunity, the report stated India has the second-highest number of active internet users, with about 390 million residents who use the web at least once a month. Further, the Ericsson connection outlook report stated that the growth of IoT technologies is enhanced by an added network capability that enables massive IoT co-existence with 4G and 5G.

- Additionally, the increasing significance of smart TV in the IoT ecosystem, due to the features like ambient intelligence and automatic user assistance, along with the rising disposable income of the people in India, is further boosting the market growth.

- Samsung India, a consumer electronics firm, has recently announced that it expects a nearly 25% growth in the LED TV segment. The company aims to capture around 36% share of the overall TV market by bringing products with the right proposition and new technologies. Owing to this, the company, in April 2022, launched its ultra-premium 2022 Neo QLED 8K and Neo QLED TVs in India.

- Moreover, recently, Xiaomi expanded its manufacturing in India by adding three new partners for smartphones and smart TVs. The new partnerships are expected further to increase Mi India's manufacturing capacity in India. Such developments by the major vendors are expected to boost market growth over the forecast period.

Internet Protocol Television (IPTV) to Boost the Market Growth

- Video on demand (VOD) is one of the dynamic features offered by IPTV. The video data is transmitted via Real-Time Streaming Protocol. VOD has gained a tremendous amount of popularity in the recent past. This has resulted in the increased adoption rates of Smart TVs. Moreover, with growing smartphone penetration and lower data tariffs, VoD services through OTT platforms show promising growth in India.

- OTT and IPTV are gaining traction driven by increasing broadband penetration and changing content consumption behaviors in the region. The effect can be significantly observed in Asian countries, like India, which represented an 8.9% GDP growth rate in FY 2021. Rapid urbanization in the region, standing at 35.39% in India, and the increase in spending power play a significant role in adopting IPTV in households.

- Moreover, the Government of India's initiatives toward digital transformation, such as digitization of cable TV and direct-to-home (DTH) services, are also favoring the adoption of IPTV in the country. The IPTV scenario in India is witnessing change owing to the advent of the network services provider, with the company providing free IPTV live subscriptions to its customers. With other companies following suit, the demand for mobile-based IPTV services is expected to increase in the region.

- The market is witnessing strategic investments from various vendors to remain competitive. For instance, in July 2022, the Government of India announced the approval of the merger between Sony Pictures Networks India and Zee Entertainment.

India Smart TV & OTT Industry Overview

The Indian smart TV and OTT market consists of several players. This industry is viewed as a lucrative investment opportunity due to the recent huge consumer interest. The companies are investing in future technologies to gain substantial expertise, enabling them to achieve sustainable competitive advantage.

- March 2022: India's public broadcaster, DD India, signed an MoU with Yupp TV, an OTT platform that is a gateway for television viewers, to expand the global reach of the DD India channel. According to the Ministry of Information and Broadcasting, this is an attempt to put forth India's perspective on various international developments on global platforms and to showcase India's culture and values to the world.

- January 2022: Sony Electronics announced a Bravia XR television series, including MASTER Series Z9K 8K and X95K 4K Mini LED models, MASTER Series A95K, MASTER Series A90K and A80K 4K OLED models, and X90K 4K LED model.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Study Deliverables

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the market

- 4.4 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Large Volume of the Indian Households and Relative Less Levels of Penetration

- 5.1.2 Growing Spending Power and Growth in Smartphone Adoption to boost OTT Demand

- 5.1.3 Declining Unit Prices Coupled with Entry of Several Regional Players to Drive Bargaining Leverage of Buyers

- 5.2 Market Restraints

- 5.2.1 Manufacturers Faced with Taxation Challenges and Relatively Higher Replacement Rate

6 GLOBAL SMART TV MARKET SNAPSHOT (Unit Shipment Forecasts, Growth Strategies Adopted by Key Vendors, Market Outlook, and Major Cues for the Indian Market)

7 MARKET SEGMENTATION

- 7.1 OS Type (Tizen, WebOS, Android TV, etc.)

- 7.2 Price Range

8 ANALYSIS OF THE OTT LANDSCAPE IN INDIA

- 8.1 Historical Context and Current Market Scenario

- 8.2 Market Categorization - Broadcaster (Hotstar and ZEE), Independent (Alt Balaji and Viu), International Players (Netflix and Amazon Prime), and Telco (Jio, Airtel, and Vodafone Play)

- 8.3 Subscriber Base of Key OTT Players (in million)

- 8.4 Key strategies adopted by OTT players -Localization of Content, Affordable Pricing, Strategic Collaborations, Personalization and Use of Digital Transformation for View Engagement

- 8.5 A comparative Study of OTT and DTH User Base in India

- 8.6 Key Customer Acquisition Strategies of Major Vendors

- 8.6.1 Bundling of Services and collaboration with Telcos

- 8.6.2 Premiumization and Emphasis on Content-driven Programs

- 8.6.3 Affordable Subscription Plans Targeted at Young Populace

- 8.6.4 Other Key Strategic Themes Identified from the Current OTT Vendors

- 8.7 Local Players expected to Catch Ground Aided by Strong Demand for Regional Content

9 VENDOR MARKET SHARE ANALYSIS - INDIA SMART TV (Xiaomi, Samsung, LG, Sony, etc.)

10 COMPETITIVE LANDSCAPE

- 10.1 Company Profiles

- 10.1.1 Xiaomi Corporation

- 10.1.2 Samsung Electronics

- 10.1.3 LG Corporation

- 10.1.4 Sony Corporation

- 10.1.5 TCL Technology

- 10.1.6 Vu Technologies

- 10.1.7 Honor

- 10.1.8 Panasonic Corporation

- 10.1.9 Haier

- 10.1.10 OnePlus

- 10.1.11 Sansui

11 INVESTMENT OUTLOOK

12 MARKET OUTLOOK

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日