|

市場調査レポート

商品コード

1940677

スペインの建設市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Spain Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スペインの建設市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

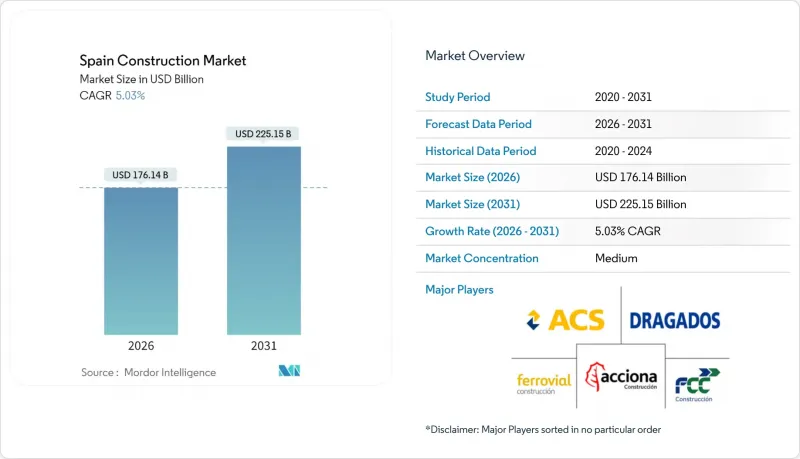

スペインの建設市場は、2025年の1,677億米ドルから2026年には1,761億4,000万米ドルへ成長し、2026年から2031年にかけてCAGR5.03%で推移し、2031年までに2,251億5,000万米ドルに達すると予測されています。

この拡大は、スペインがNextGenerationEU(次世代EU)基金から1,540億米ドルの資金にアクセスできることに後押しされています。この資金の約70%は、インフラ、再生可能エネルギー、建物の改修にまたがる建設関連プログラムに直接投入されます。住宅建設活動の活発化が需要の堅調さを支える一方、前例のない公共部門支出がインフラ投資を牽引し、民間資本の流入を促しています。近代的建設手法の普及拡大、デジタル化推進の義務化、2030年FIFAワールドカップに向けたインフラ整備計画が、さらなる成長機会を創出しています。しかしながら、労働力不足と原材料価格の変動が利益率を圧迫し続けており、企業は自動化、オフサイト製造、戦略的調達活動の加速を迫られています。

スペイン建設市場の動向と展望

EU資金によるインフラ近代化

スペインは765億米ドルの助成金を確保し、欧州委員会から復興計画に対して「優秀」の評価を得ました。主要な鉄道計画には、9億1,960万米ドルを投じるADIFネットワーク更新事業や、33億米ドルを投じる地中海回廊改良事業が含まれます。後者は単線区間の複線化と重要区間の電化を推進します。補完的な欧州接続施設(CEF)資金2億6,510万米ドルは、8地域にわたる22のマルチモーダルプロジェクトを支援します。これらの事業は地域雇用を創出し、鉄鋼・コンクリート需要を刺激するとともに、スペインを大陸の物流ハブとして再位置づけるものです。

再生可能エネルギーの拡大

国家目標では2030年までに62ギガワットの新規再生可能エネルギー容量を求め、広範な建設を促進しています。7億7,000万米ドル規模のテルエル陸上風力発電契約(GEバーノバ製タービン125基)は760メガワットを供給し、ポートフォリオ拡大の好例です。欧州連合(EU)資金の一部支援を受けたイベルドローラ社の5億5,000万米ドル規模のスマートグリッド拡張事業は、年間1万人の雇用創出が見込まれます。バルデカナス揚水発電所改修(1億1,880万米ドル)などのエネルギー貯蔵投資は、送電網の耐障害性を高め、安定したEPC(設計・調達・建設)案件のパイプラインを確保します。

高い人件費と熟練労働者不足

スペインの建設労働力のうち29歳未満はわずか9.2%(2008年は25.2%)であり、EU資金プロジェクトの施工能力を制約しています。職業訓練の登録者数は15年間で45.6%減少し、再生可能エネルギーやデジタル化が専門人材を必要とする中で格差が拡大しています。業界団体は建設労働財団(Fundacion Laboral de la Construccion)によるデュアルトレーニングプログラムの拡充を推進する一方、海外からの人材採用で漸進的な緩和を図っています。マドリードとカタルーニャの逼迫した労働市場は賃金上昇を招き、入札競争力を脅かし固定価格契約に負担をかけています。

セグメント分析

2025年時点で住宅建設はスペイン建設市場シェアの36.80%を占め、未充足の都市住宅需要と活発な外国人購入者層に支えられています。最も成長率の高いインフラ部門は、復興計画の資金が交通・エネルギー分野の近代化に先行投入されるため、2031年までCAGR6.78%が見込まれます。マドリード地下鉄路線延伸、地中海回廊鉄道複線化、イベルドローラ社による送電網拡張が相まって、建設業者の受注残高は重土木工事へシフトしています。一方、2030年FIFAワールドカップ開催に伴う主要スタジアム建設や都市交通プロジェクトが、インフラ分野の成長をさらに加速させる見込みです。

インフラの急成長にもかかわらず、土地不足と政策インセンティブが垂直開発を促進するマドリード、バルセロナ、バレンシアでは住宅建設のパイプラインが堅調です。省エネ建築基準がヒートポンプ設置や高性能外皮の需要を喚起し、専門下請け業者の需要を刺激しています。商業用不動産は観光需要の回復を活かし、工業用スペースはニアショアリングとEC物流の波に乗り、セクターの多様な成長エンジンを浮き彫りにしています。

2025年のスペイン建設市場規模において、新規建設が67.05%を占め主導的立場にあります。これは新規鉄道・高速道路・公益事業メガプロジェクトに支えられたものです。一方、改修市場はCAGR5.55%で拡大しており、2026年までに51万戸の住宅改修を目標とするEU補助金38億米ドルが後押ししています。対象費用の最大80%をカバーし、30%のエネルギー使用量削減を義務付ける補助金制度が、住宅所有者の導入意欲を高めています。カタルーニャ州は300以上の補助金制度で主導的役割を果たし、499自治体にわたる597の公共建築物では別途改修資金が確保されています。

改修ブームは、建物の3分の2が築40年以上というスペインの老朽化したストック問題に対応しています。BIMベースのエネルギー監査とデジタル建築許可により、承認プロセスが効率化され、工事の統合が促進され、単価が削減されています。請負業者は、外壁断熱、太陽光対応屋根、アクセシビリティ向上に注力し、中小企業専門業者にニッチな機会を創出しています。光熱費の上昇に伴い、投資回収期間が短縮され、補助金期間終了後も持続的な改修ブームを支えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要(マクロ経済と建設活動)

- 市場促進要因

- 有利な住宅ローン金利に支えられた住宅需要の回復

- EU資金によるインフラ近代化(NextGenerationEU)

- 再生可能エネルギーの拡大(風力・太陽光及び送電網)

- 観光主導型商業不動産の回復

- 公共入札におけるモジュール式/工業化建設の導入状況

- 水不足適応プロジェクト(海水淡水化、水の再利用)

- 市場抑制要因

- 高い労働コストと熟練労働者の不足

- 変動するセメント及び鉄鋼価格

- 厳格な生物多様性影響評価

- 気候リスク保険の保険料上昇

- バリュー/サプライチェーン分析

- 概要

- 不動産開発業者および建設業者- 主要な定量的・定性的洞察

- 建築・エンジニアリング企業- 主要な定量的・定性的洞察

- 建材・建設機械メーカー- 主要定量的・定性的洞察

- 政府の取り組みとビジョン

- 規制情勢

- テクノロジーの展望

- 業界の魅力度- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 建設資材の価格設定および建設コスト(資材、労務、設備)分析

- スペインと他国の主要産業指標の比較

- 主要な今後の/進行中のプロジェクト(特に大型プロジェクトに焦点を当てて)

第5章 市場規模と成長予測(金額、単位:10億米ドル)

- セクター別

- 住宅用

- アパートメント/分譲マンション

- 戸建て住宅

- 商業用

- オフィス

- 小売り

- 産業・物流施設

- その他

- インフラストラクチャー

- 交通インフラ(道路、鉄道、航空、その他)

- エネルギー・公益事業

- その他

- 住宅用

- 建設タイプ別

- 新築

- 改修

- 施工方法別

- 従来型現場施工

- 近代的建築手法(プレハブ、モジュラーなど)

- 投資源別

- 公共

- 民間

- 地域別

- アンダルシア

- カタルーニャ

- マドリード

- バレンシア

- その他の地域

第6章 競合情勢

- 市場集中と戦略的動き

- 市場シェア分析

- 企業プロファイル

- ACS, Actividades de Construccion y Servicios, S.A.

- Dragados S.A.

- Acciona Construccion S.A.

- Ferrovial Construccion S.A.

- FCC Construccion S.A.

- Sacyr Construccion S.A.

- Elecnor S.A.

- Cobra Instalaciones y Servicios S.A.

- TSK Electronica y Electricidad S.A.

- Administrador de Infraestructuras Ferroviarias(ADIF)

- ADIF Alta Velocidad

- Obrascon Huarte Lain(OHLA)S.A.

- Grupo SANJOSE S.A.

- Aldesa Construcciones S.A.

- Vias y Construcciones S.A.

- COMSA Corporacion

- Copasa

- Grupo Ortiz

- Sorigue

- Rover Grupo