|

市場調査レポート

商品コード

1642955

タイの商業用不動産:市場シェア分析、産業動向、成長予測(2025年~2030年)Commercial Real Estate In Thailand - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| タイの商業用不動産:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

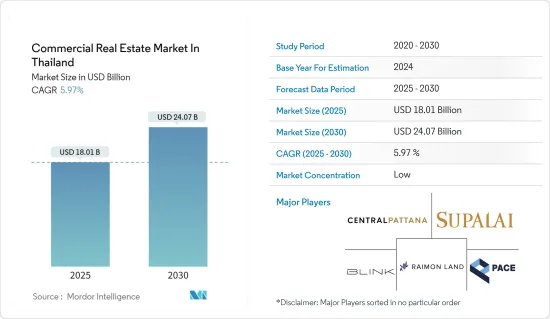

タイの商業用不動産市場2025年の市場規模は180億1,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.97%で、2030年には240億7,000万米ドルに達すると予測されます。

主なハイライト

- タイの商業用不動産市場は、2024年に堅調な業績が見込まれます。この成長の背景には、同国の観光産業の復活、製造業の拡大、優良資産に品質と持続可能性を求める投資家の顕著な動向があります。

- タイの不動産市場は来年、回復力を示すと思われます。この回復力は、さまざまな国内政策と自信に満ちた国内市場により、世界のマクロ経済情勢の不確実性を相殺するものと期待されます。

- 2023年の統計は、タイの不動産の活況を浮き彫りにしました。対象となる製造業への投資は、前年比66%増という驚異的な伸びを示しました。観光客は政府予測を上回る152%増となり、ホスピタリティセクターの回復を裏付けています。また、バンコクのセントラル・ビジネス・エリア(CBA)の一等地のオフィス・スペースに対する需要は、多国籍企業を中心に依然として強いです。

- 2024年、タイと東南アジアの不動産市場は、戦略的なインフラ強化とバンコクのグレードA不動産の質の向上に注力することで、大きな影響を目の当たりにすることになると思われます。

- バンコクの不動産事情は、ワールドクラスの複合施設プロジェクトの数々によって、顕著な変貌を遂げようとしています。10の異なる地区からなるこれらのプロジェクトは、2028年までにバンコクの景観を大幅に向上させると予測されています。具体的には、90万平方メートルを超えるグレードAのオフィススペース、30万平方メートルの商業施設、5400戸の高級コンドミニアム、5900室の高級ホテルがバンコクのセントラル・ビジネス・エリア(CBA)に集中します。このような高級不動産の急増により、バンコクは投資家、多国籍企業(MNC)、優良な機会を求める有能な個人にとって魅力的な目的地となっています。

タイの商業用不動産市場の動向

タイにおける小売スペース需要の高まり

2024年のタイの小売不動産セクターは、消費者心理の顕著な上昇に後押しされ、成長の態勢を整えています。2023年12月、消費者信頼感指数(CCI)は62.0に達し、2020年2月以来の高水準を記録しました。政府の継続的な景気刺激策と観光客の増加が予想されることから、小売セクターはさらなる支援を受けることになると思われます。小売セクターは、開発業者や小売業者が多様な都市に進出するという顕著な変化を目の当たりにしています。ショッピングモールの拡大、特にコミュニティモールや複合用途プロジェクト内の小売スペースの拡大の勢いは、2024年も続くと思われます。

特に繁華街やミッドタウンでは、簡単にアクセスできるショッピング街への意欲が高まっています。郊外でも、人口増加やインフラ整備に後押しされ、ショッピングモールの建設が急増しています。2023年の小売セクターの稼働率は95%と好調で、この動向はさまざまな形態のショッピングモールで維持されています。バンコクの小売業界では、2024年に新規出店やリニューアルが急増すると見られています。しかし、この予想される供給の流入は、このセクターの稼働率に圧力をかける可能性があります。

バンコクのオフィススペースが市場を牽引

厳しい2023年を経て、タイの商業用不動産市場は刺激的な2024年を迎えます。グレードの高いオフィスや商業施設の急増が目前に迫っており、開発業者、投資家、入居者の注目を集めています。

2024年末までには、7件の新規オフィス・プロジェクトにより、バンコクのセントラル・ビジネス・エリア(CBA)におけるプライム・オフィスの総供給量は4,12,600㎡(NLA)に達すると予測されています。この数字は、既存のプライムオフィス・ストックの27.9%に相当し、1999年以降、年間供給量の増加率としては最高となります。こうした開発は、特にCBAサブマーケットにおいて注目すべき課題となっています。プライムオフィスのパイプラインは、2028年末までにCBAサブマーケットに約150万平方メートルを投入すると予想されており、これは既存のプライムオフィスストックを実質的に倍増させることになります。

質への逃避」の傾向が顕著な中、古い商業ビルは安定した賃料と稼働率の維持という課題に直面しています。その結果、ESG認証の取得に重点を置いた改修や強化の取り組みが目立って増えています。こうした努力は、新しい開発にもかかわらずビルの競争力を維持するために極めて重要です。

築10年未満のオフィスビルは、2023年第3四半期にはCBA全体の平均より平均22.5%高い賃料プレミアムを獲得しました。10年以上経過した物件でも、大幅な改修が行われ、競争力が維持され、平均をわずかに上回るプレミアムがついた。一方、築10年以上経過し、目立った改修が施されていないオフィスビルのディスカウント率は平均を8.8%下回り、この差は拡大すると予想されます。こうした動向は、オフィス市場における先行者優位の台頭を示しています。

タイの商業用不動産業界の概要

タイの商業用不動産市場は、プレーヤーが多いため細分化されています。市場の主要な不動産プレーヤーとしては、セントラル・パタナPLC、サンシリ・パブリック、ペース・デベロップメント・コーポレーションPLC、ライモン・ランドPCLなどが挙げられます。

同市場は、経済成長の継続と大都市における商業用不動産需要の増加により、予測期間中の成長が見込まれています。オフィススペースの需要や観光客の増加など、その他の要因も市場を牽引する可能性があります。工業用不動産開発業者は今後、投資に注力したり、新しいフェーズやプロジェクトを開発したりする可能性が高いです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場を牽引する全体的な経済成長

- 市場を牽引するビジネスと産業の成長

- 市場抑制要因

- 市場の成長を妨げる不安定な経済状況

- 土地の所有権や賃借権の難しさが市場に影響

- 市場機会

- 市場を牽引するeコマース分野の台頭

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 現在の市場シナリオ

- バリューチェーン/サプライチェーン分析

- 商業用不動産セクターに対する政府の取り組みと規制面

- 既存および今後のプロジェクトに関する洞察

- 一般経済と不動産融資の金利レジームに関する洞察

- 商業用不動産セグメントの賃貸利回りに関する洞察

- 商業用不動産における資本市場の浸透とREITの存在に関する洞察

- 商業用不動産における官民パートナーシップに関する洞察

- 不動産セグメントで活躍する不動産テックおよび新興企業に関する洞察(ブローキング、ソーシャル・メディア、施設管理、不動産管理)

- COVID-19が市場に与える影響

第5章 市場セグメンテーション

- タイプ別

- オフィス

- 小売

- 産業・物流

- ホスピタリティ

- その他

- 主要都市別

- バンコク

- チェンマイ

- ホアヒン

- サムイ島

- その他のタイ

第6章 競合情勢

- 市場集中

- 企業プロファイル

- ディベロッパー

- Central Pattana PLC

- Supalai Company Limited

- Pace Development Corporation PLC

- Raimon Land PCL

- Blink Design Group*

- 不動産会社

- CBRE Thailand

- Savills

- Colliers International Thailand

- RE/MAX Thailand

- JLL Thailand

- Knight Frank Thailand*

- その他の企業(新興企業、団体)

- Property Perfect

- Hipflat

- DDProperty

- Dot Property*

- ディベロッパー

第7章 市場の将来

第8章 付録

The Commercial Real Estate Market In Thailand Market size is estimated at USD 18.01 billion in 2025, and is expected to reach USD 24.07 billion by 2030, at a CAGR of 5.97% during the forecast period (2025-2030).

Key Highlights

- The Thai commercial real estate market has been set for a robust performance in 2024. This growth can be attributed to the revival of the country's tourism industry, expanding manufacturing sectors, and a notable trend of investors seeking quality and sustainability in prime assets.

- The Thai real estate market will exhibit resilience in the coming year. This resilience is expected to counterbalance the uncertainties of the global macroeconomic landscape, owing to a range of domestic policy initiatives and a confident domestic market.

- Statistics from 2023 underscored the vibrancy of Thailand's real estate landscape. Investments in targeted manufacturing industries surged by an impressive 66% Y-o-Y. Tourist arrivals, surpassing the government's projections, soared by 152%, underscoring a robust rebound in the hoslity sector. Also, the demand for prime office spaces in Bangkok's Central Business Area (CBA) remains strong, particularly among multinational corporations.

- In 2024, the Thai and Southeast Asian real estate market will witness a significant impact from strategic infrastructure enhancements and a focus on elevating the quality of Grade A real estate in Bangkok.

- The real estate landscape in Bangkok is poised for a notable transformation, driven by a slew of world-class mixed-use projects. These projects, comprising 10 distinct precincts, are projected to add to the city's landscape by 2028 substantially. Specifically, they will contribute over 900,000 sq. m of Grade A office space, 300,000 sq. m of retail centers, 5,400 luxury condominium units, and 5,900 luxury hotel rooms, all concentrated in Bangkok's Central Business Area (CBA). This surge in premium real estate offerings makes Bangkok an attractive destination for investors, multinational corporations (MNCs), and talented individuals seeking prime opportunities.

Thailand Commercial Real Estate Market Trends

Growing Demand for Retail Spaces in Thailand

The Thai retail estate sector in 2024 is poised for growth, buoyed by a notable increase in consumer sentiment. In December 2023, the Consumer Confidence Index (CCI) reached 62.0, marking its highest level since February 2020. With ongoing government stimulus initiatives and a projected rise in tourist arrivals, the retail sector is set to receive further support. The retail sector is witnessing a notable shift, with developers and retailers venturing into diverse city locales. The momentum behind shopping mall expansions, particularly community malls and retail spaces within mixed-use projects, is set to persist in 2024.

There is a rising appetite for easily accessible shopping avenues, particularly in downtown and midtown regions. Even suburban areas are witnessing a surge in shopping mall constructions, buoyed by population upswings and enhanced infrastructure. In 2023, the retail sector boasted a robust 95% occupancy rate, a trend that held across various shopping mall formats. Bangkok's retail scene is set to witness a surge in new and revamped establishments in 2024. However, this anticipated influx of supply may exert pressure on the sector's occupancy rates.

Bangkok's Office Space Driving the Market

After a challenging 2023, the Thai commercial real estate market is poised for an exciting 2024. The imminent surge in prime-grade office and retail offerings is set to grab the attention of developers, investors, and occupiers.

By the close of 2024, with seven new office projects, the total prime office supply in Bangkok's Central Business Area (CBA) is projected to hit 4,12,600 sq. m (NLA). This figure represents 27.9% of the existing prime stock, marking the highest annual supply increase since 1999. These developments pose notable challenges, particularly within the CBA submarket. The prime office pipeline is expected to inject roughly 1.5 million sq. m into the CBA submarket by the end of 2028, effectively doubling the existing prime office stock.

Amid a pronounced "flight-to-quality" trend, older commercial buildings face mounting challenges in maintaining steady rental and occupancy levels. Consequently, there is a noticeable increase in renovation and enhancement initiatives, with a growing emphasis on securing ESG certifications. These endeavors are crucial for the buildings to remain competitive despite newer developments.

Office buildings with less than a decade of age fetched a significant rental premium, averaging 22.5% higher than the CBA-wide average in Q3 of 2023. Over 10 years, even older assets underwent substantial renovations, maintaining their competitiveness and commanding a premium slightly above the average. On the other hand, office properties aged over a decade, without notable renovations, faced a discount of 8.8% below the average, with this gap expected to widen. These trends indicate the emergence of a first-mover advantage in the office market.

Thailand Commercial Real Estate Industry Overview

The Thai commercial real estate market is fragmented due to the country's many players. Some of the major real estate players in the market are Central Pattana PLC, Sansiri Public Co. Ltd, Pace Development Corporation PLC, and Raimon Land PCL.

The market is expected to grow during the forecast period due to continued economic growth and increased demand for commercial real estate in metropolitan cities. Other factors like demand for office spaces and tourism growth may also drive the market. Industrial estate developers are more likely to focus on investments or develop new phases or projects in the future.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Overall economic growth driving the market

- 4.1.2 The growth of business and industries driving the market

- 4.2 Market Restraints

- 4.2.1 Fluctuating economic conditions hindering the growth of the market

- 4.2.2 Difficulty in landownership and leasing rights affecting the market

- 4.3 Market Opportunities

- 4.3.1 The rise in ecommerce sector driving the market

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Current Market Scenario

- 4.6 Value Chain/Supply Chain Analysis

- 4.7 Government Initiatives and Regulatory Aspects for the Commercial Real Estate Sector

- 4.8 Insights on Existing and Upcoming Projects

- 4.9 Insights on Interest Rate Regime for General Economy and Real Estate Lending

- 4.10 Insights on Rental Yields in the Commercial Real Estate Segment

- 4.11 Insights on Capital Market Penetration and REIT Presence in Commercial Real Estate

- 4.12 Insights on Public-private Partnerships in Commercial Real Estate

- 4.13 Insights on Real Estate Tech and Start-ups Active in the Real Estate Segment (Broking, Social Media, Facility Management, Property Management)

- 4.14 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Office

- 5.1.2 Retail

- 5.1.3 Industrial and Logistics

- 5.1.4 Hospitality

- 5.1.5 Others

- 5.2 By Key Cities

- 5.2.1 Bangkok

- 5.2.2 Chiang Mai

- 5.2.3 Hua Hin

- 5.2.4 Koh Samui

- 5.2.5 Rest of Thailand

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Company Profiles

- 6.2.1 Developers

- 6.2.1.1 Central Pattana PLC

- 6.2.1.2 Supalai Company Limited

- 6.2.1.3 Pace Development Corporation PLC

- 6.2.1.4 Raimon Land PCL

- 6.2.1.5 Blink Design Group*

- 6.2.2 Real Estate Agencies

- 6.2.2.1 CBRE Thailand

- 6.2.2.2 Savills

- 6.2.2.3 Colliers International Thailand

- 6.2.2.4 RE/MAX Thailand

- 6.2.2.5 JLL Thailand

- 6.2.2.6 Knight Frank Thailand*

- 6.2.3 Other Companies (Start-ups, Associations)

- 6.2.3.1 Property Perfect

- 6.2.3.2 Hipflat

- 6.2.3.3 DDProperty

- 6.2.3.4 Dot Property*

- 6.2.1 Developers