マレーシアの建設:市場シェア分析、産業動向、成長予測(2025年~2030年)

Malaysia Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1642086

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

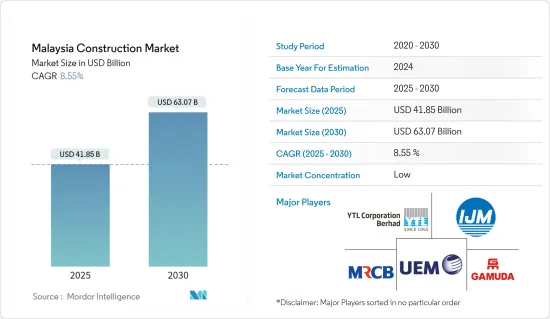

マレーシアの建設市場規模は2025年に418億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは8.55%で、2030年には630億7,000万米ドルに達すると予測されます。

主要ハイライト

- マレーシアの建設産業は2023年も成長を続け、1月から10月の間に実現したプロジェクトの総額は547億1,000万MYR(114億7,000万米ドル)に達しました。

- 民間部門がCOVID-19による停滞からの回復の先頭に立ち、建設成長の主要原動力となりました。この回復に貢献した民間セクターの主要プロジェクトには、複合用途の高層住宅プロジェクト、サプライチェーンの最適化を推進する高速産業プロジェクト、データセンター開発などがあります。

- 民間部門は政府主導のプロジェクトの大半を占めていたが、主に政府の統制と慎重な支出により、時間の経過とともに減速しました。しかし、政府はさまざまな国家インフラプロジェクトを通じて、公共交通の改善と地域の経済開発に向けて大きく前進しました。

- このプロジェクトには、アジア太平洋で拡大するデータセンター需要に対応する5Gネットワークの展開や、建設段階で数千人の雇用創出が見込まれるMRTの延伸などが含まれます。公共交通プロジェクトは、クランバレーや都市間鉄道沿線にトランジット志向のプロジェクトの波を巻き起こし、周辺地域の不動産活性化の起爆剤となっています。

- マレーシア政府が打ち出した新産業マスタープラン(NIMP)2030は、2030年までにマレーシアの製造業を高付加価値で技術ベースの国際競合部門に変革することを目指しています。NIMPは、製造業の発展を促進するため、新たな工業団地の設立やインフラの建設・近代化を求めています。

マレーシアの建設市場の動向

住宅建設が市場を牽引

マレーシアの建設活動は、2023年第2四半期に成長率が鈍化したもの、5四半期連続で増加しています。

- マレーシア統計局(DOSM)のデータによると、2023年4月から6月までの建設部門の工事額は前年同期比8.1%増の324億MYR(70億5,000万米ドル)でした。

- 建設生産高の伸びは、主に住宅部門の工事増加によるもので、住宅部門は前年同期比6.9%増と回復しました。さらに、特殊貿易活動も前年同期比9.8%増と、より速い伸びを記録しました。

- しかし、同部門の生産高で最大の割合を占める土木工学は、前年同期比10.4%増と伸び率が鈍化しました。

- この伸びは過去4四半期で最も鈍いものであったが、これは主に、2023年第2四半期までの3四半期において、工事金額が121億MYR(25億9,000万米ドル)前後とほぼ同額であったため、ベースが高くなったためです。

- プロジェクト所有者別では、総生産高の63.1%を占める民間部門の生産高が17.3%増(2023年第1四半期:10.6%増)と急速に増加した一方、政府傘下の建設プロジェクト開発の進捗はゼロ成長(2023年第1四半期:6.1%増)または2023年第1四半期と横ばいを記録しました。

インフラ建設活動の増加が成長を牽引

マレーシアの建設セクターは劇的に拡大しており、2023年9月時点で9,144件のプロジェクトが開始されています。これらのプロジェクトは630億MYR(132億1,000万米ドル)の民間投資と840億MYR(176億1,000万米ドル)の政府投資に相当します。プロジェクトの91%は地元業者が担当し、マレーシアのインフラ開発における彼らの専門性が実証されました。

マレーシアの2024年度予算によると、政府はペナンLRT、サバ・サラワク・リンク道路、LRT3の復活など、いくつかの大規模プロジェクトの実施を計画しています。これらのプロジェクトは、マレーシアの2024年度開発支出予算900億MYR(188億7,000万米ドル)の一部です。

- ペナン技術パークリチウム電池セパレーター工場プロジェクトは、ペナンに40億平方メートルのリチウム電池セパレーター工場を建設するものです。工場は26.7ヘクタールの土地に建設され、ウェットプロセスとコーティングされたセパレーターの生産能力は年間40億平方メートルとなります。工場の建設は2023年第4四半期に始まり、2025年第3四半期に完成する予定です。このプロジェクトは、同地域におけるポリイミド電池の需要増に対応することを目的としています。操業開始後は、同地域初のプロジェクトのひとつとなり、ASEAN最大の低炭素セパレーター工場となります。

- セデナックJH1データセンター・キャンパスプロジェクトは、JB(ジョホールバル)の12.5haの土地に150MWのデータセンター・キャンパスを開発するものです。建設は2023年第4四半期に開始され、2025年第4四半期に完成する予定です。完成すれば、データセンター(DC)キャンパスは東南アジア最大級のデータセンター・キャンパスとなり、同地域の顧客のインフラ要件を満たすことになります。

- 中国通信建設公司(CCCC)は、マレーシア最大のインフラ事業である東海岸鉄道リンクの陣頭指揮を執っています。CCCCは中国の最先端技術を活用し、従来の3倍のスピードで線路を敷設し、新たなペースを築いています。

マレーシアの建設産業概要

マレーシアの建設市場は、国際的な大手企業が市場全体の大きなシェアを占めているため、競合は少ないです。さらに、住宅建設と運輸建設部門は予測期間中に大きな成長の可能性を秘めており、これが他の市場参入企業の成長機会を刺激しています。マレーシアの建設市場における主要企業には、YTL Corporation Berhad、IJM Corporation Berhad、Gamuda Berhad、UEM Group Berhad、Malaysian Resources Corporation Berhadなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 市場の範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の経済と建設市場のシナリオ

- 建設セグメントにおける技術革新

- 政府の規制と取り組みが建設産業に与える影響

- マレーシアビジョン2020概要と解説

- マレーシアの主要産業指標と他ASEAN諸国との比較

- マレーシアと他のASEAN諸国との建設コスト指標の比較

- COVID-19の市場への影響

- 市場力学

- 市場促進要因

- 住宅需要の増加

- インフラプロジェクトの増加

- 市場抑制要因

- 原料コストの上昇

- 市場機会

- 市場促進要因

- バリューチェーン/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- セクター別

- 商業用建設

- 住宅建設

- 産業建設

- インフラ(交通)建設

- エネルギー公益事業建設

- 建設タイプ別

- 増築

- 解体・新築

第6章 競合情勢

- 市場概要

- 企業プロファイル

- YTL Corporation Berhad

- IJM Corporation Berhad

- Gamuda Berhad

- UEM Group Berhad

- Malaysian Resources Corporation Berhad

- WCT Holdings Berhad

- WCE Holdings Berhad

- Hock Seng Lee Berhad

- Mudajaya Group Berhad

- Muhibbah Engineering(M)Bhd*

第7章 市場の将来

第8章 付録

目次

The Malaysia Construction Market size is estimated at USD 41.85 billion in 2025, and is expected to reach USD 63.07 billion by 2030, at a CAGR of 8.55% during the forecast period (2025-2030).

Key Highlights

- The construction industry in Malaysia continued to grow in 2023, with the total value of projects realized amounting to MYR 54.71 billion (USD 11.47 billion) between January and October.

- The private sector spearheaded the recovery from COVID-19 lockdowns and became the main driver of construction growth. Some key private sector projects that contributed to this recovery were high-rise residential projects with mixed-use ideas, supply chain optimization-driven fast-track industrial projects, and data center developments.

- While the civil sector accounted for the majority of government-initiated projects, it slowed down over time, mainly due to government control and prudent spending. However, the government has made significant strides toward improving public transportation and economic development in the region through various national infrastructure projects.

- The projects include the 5G network roll-out, which will cater to the growing demand for data centers across the Asia-Pacific region, and the MRT extension, which is projected to create thousands of jobs during the construction phase. Public transportation projects have sparked a wave of transit-oriented projects in Klang Valley, as well as along the intercity railway links, catalyzing real estate revitalization in the surrounding areas.

- The New Industrial Master Plan (NIMP) 2030 launched by the Government of Malaysia aims to transform Malaysia's manufacturing industry into a high value, technology-based and globally competitive sector by 2030. The NIMP calls for the establishment of new industrial parks and the construction and modernisation of infrastructure to facilitate the development of the manufacturing sector.

Malaysia Construction Market Trends

Residential Construction Driving the Market

Construction activity in Malaysia has increased for the fifth consecutive quarter, although the growth rate has slowed in the second quarter of 2023.

- According to data from the Department of Statistics Malaysia (DOSM), the value of work done in the construction sector rose by 8.1% year-on-year to MYR 32.4 billion (USD 7.05 billion) from April to June 2023.

- The growth in construction output was primarily driven by increased work in the residential sector, which saw a rebound and a 6.9% year-on-year expansion. Additionally, special trade activities experienced a faster rise of 9.8% year-on-year.

- However, civil engineering, which makes up the largest proportion of the sector's output, grew at a slower rate of 10.4% year-on-year.

- The growth was the slowest in four quarters, mainly because of the higher base due to the value of work done being more or less the same, hovering around MYR 12.1 billion (USD 2.59 billion) in the three quarters to Q2-2023.

- By project owners, private sector output, which accounted for 63.1% of total output, rose faster by 17.3% (Q1 2023: +10.6%), while the progress of construction project developments under the government recorded zero growth (1Q 2023: +6.1%) or unchanged from Q1 of 2023.

Increase in Infrastructure Construction Activities Driving Growth

The construction sector in Malaysia has seen a dramatic expansion, with 9,144 projects launched as of September 2023. The projects represent MYR 63 billion (USD 13.21 billion) of private investment and MYR 84 billion (USD 17.61 billion) of government investment. 91% of the projects were handled by local contractors, demonstrating their expertise in developing Malaysia's infrastructure.

According to budget-2024 Malaysia, the government plans to implement several large-scale projects such as Penang LRT, Sabah and Sarawak Link Road, and the reinstatement of LRT 3. These projects are part of Malaysia's MYR 90 billion (USD 18.87 billion) development expenditure budget for 2024.

- The Penang Technology Park Lithium Battery Separator Plant project consists of the construction of a 4 billion square meter (4 billion sq. m) lithium battery separators plant in Penang. The plant will be located on 26.7 hectares of land and will have a production capacity of 4 billion square meters per annum of wet-process and coated separators. The construction of the plant began in the fourth quarter of 2023 and is planned to be completed in the third quarter of 2025. This project is intended to meet the increasing demand for polyimide batteries in the region. Once operational, the project will be one of the first in the region and will be the largest low-carbon separator plant in ASEAN.

- Sedenak JH1 Data Center Campus project consists of the development of a 150 MW data center campus located on a 12.5 ha plot of land in JB (Johor Bahru). The construction started in the 4th quarter of 2023 and will be finished in the 4th quarter of 2025. Once completed, the Data Center (DC) campus will become one of Southeast Asia's largest data center campuses to meet the infrastructure requirements of customers in the region.

- The China Communication Construction Company (CCCC) is spearheading Malaysia's largest infrastructure endeavor, the East Coast Rail Link. Leveraging cutting-edge Chinese technology, CCCC is setting a new pace, laying tracks at a rate three times faster than traditional methods.

Malaysia Construction Industry Overview

The Malaysian construction market is less competitive due to major international players holding a large share of the total market. Furthermore, the residential and transport construction sectors have a huge potential for growth during the forecasted period, which stimulates opportunities for other market players. Some of the major players in Malaysia's Construction Market are YTL Corporation Berhad, IJM Corporation Berhad, Gamuda Berhad, UEM Group Berhad, and Malaysian Resources Corporation Berhad.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Market

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Economic and Construction Market Scenario

- 4.2 Technological Innovations in the Construction Sector

- 4.3 Impact of Government Regulations and Initiatives on the Industry

- 4.4 Review and Commentary on the Extent of Malaysia Vision 2020

- 4.5 Comparison of Key Industry Metrics of Malaysia with Other ASEAN Countries

- 4.6 Comparison of Construction Cost Metrics of Malaysia with Other ASEAN Countries

- 4.7 Impact of COVID-19 on the Market

- 4.8 Market Dynamics

- 4.8.1 Market Drivers

- 4.8.1.1 Rise in Demand for Residential Property

- 4.8.1.2 Increase in Infrastructure Projects

- 4.8.2 Market Restraints

- 4.8.2.1 Increase in Cost of Raw Materials

- 4.8.3 Market Oppurtunities

- 4.8.1 Market Drivers

- 4.9 Value Chain/Supply Chain Analysis

- 4.10 Industry Attractiveness - Porter's Five Forces Analysis

- 4.10.1 Bargaining Power of Suppliers

- 4.10.2 Bargaining Power of Buyers/Consumers

- 4.10.3 Threat of New Entrants

- 4.10.4 Threat of Substitute Products

- 4.10.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Sector

- 5.1.1 Commercial Construction

- 5.1.2 Residential Construction

- 5.1.3 Industrial Construction

- 5.1.4 Infrastructure (Transportation) Construction

- 5.1.5 Energy and Utilities Construction

- 5.2 By Construction Type

- 5.2.1 Additions

- 5.2.2 Demolition and New Construction

6 COMPETITIVE LANDSCAPE

- 6.1 Market Overview

- 6.2 Company Profiles

- 6.2.1 YTL Corporation Berhad

- 6.2.2 IJM Corporation Berhad

- 6.2.3 Gamuda Berhad

- 6.2.4 UEM Group Berhad

- 6.2.5 Malaysian Resources Corporation Berhad

- 6.2.6 WCT Holdings Berhad

- 6.2.7 WCE Holdings Berhad

- 6.2.8 Hock Seng Lee Berhad

- 6.2.9 Mudajaya Group Berhad

- 6.2.10 Muhibbah Engineering (M) Bhd*

7 FUTURE OF THE MARKET

8 APPENDIX

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日