先端複合材料:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Advanced Composite Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1641863

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

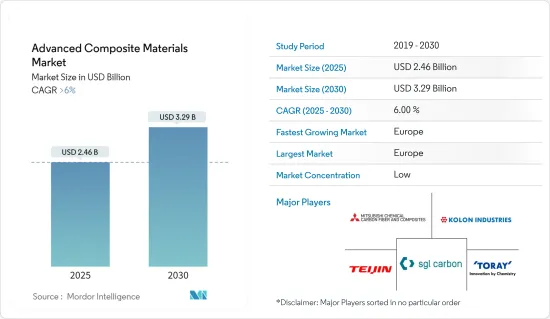

先端複合材料の市場規模は2025年に24億6,000万米ドルと推定され、2030年には32億9,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは6%を超えると予測されています。

COVID-19の大流行は、先端複合材料の市場に悪影響を与えました。全国的な封鎖と厳格な社会的遠ざけ措置により、航空機や自動車の製造施設が閉鎖され、先端複合材料市場に影響を与えました。しかし、COVIDパンデミック後は、規制解除後、市場は順調に回復しました。航空宇宙・防衛、風力エネルギー、自動車エンドユーザー産業における先端複合材料の消費増加により、市場は大幅に回復しました。

航空宇宙・防衛産業における軽量材料の需要増加と、低燃費で軽量な自動車に対する需要の高まりが市場を牽引すると予想されます。

原料価格の上昇が市場成長の妨げになると予想されます。

先進的複合材料のリサイクルとナノ複合材料の需要の増加は、予測期間中に市場に機会をもたらすと予想されます。

北米地域が市場を独占すると予想されます。また、航空宇宙・防衛、風力エネルギー、自動車、海洋の各エンドユーザー産業における先端複合材料の需要増加により、予測期間中に最も高いCAGRで推移することが予想されます。

先端複合材料の市場動向

市場を独占する航空宇宙・防衛エンドユーザー産業

- 複合材料の需要は航空宇宙産業で増加しています。民間輸送機における複合材料の使用は、機体重量の軽減が燃費の向上を可能にし、したがって運航コストの低減を可能にするため、大規模なものとなっています。

- 先進的複合材料には、高強度、高剛性、耐熱性、耐薬品性、電気伝導性、その他さまざまな熱的・化学的特性が含まれます。そのため、航空宇宙・防衛産業では先端複合材料の使用が増加しています。

- 国際航空運送協会(IATA)によると、民間航空会社の世界売上高は2021年に4,720億米ドル、2022年には7,270億米ドルと評価され、前年比43.6%の成長率を記録しました。さらに、2023年末には7,790億米ドルに達すると予想されています。このような要因により、航空宇宙部品製造における先端複合材料の需要は今後数年間で増加すると考えられます。

- 世界最大の航空機メーカーの1つであるBoeingは、2022年に合計480機の航空機を納入したと発表したが、これは2021年の世界全体の合計340機と比較して41%の増加です。このように、新しい航空機の納入が増加することで、先端複合材の需要が促進されると予想されます。

- 米国は北米地域における航空機の製造拠点です。AirbusとBoeingが同国最大の航空機メーカーです。例えば、2022年にAirbusは661機の民間航空機を納入し、年末までに1,078機の新規受注を記録しました。同様に、Boeingも737 Max 8ジェット機を57機受注しており、2025年までの納入が見込まれています。このように、航空機需要の増加は、先端複合材料市場を牽引すると予想されます。

- 欧州では、フランスやドイツなどの国々を中心に航空機の生産が増加しており、先端複合材料の需要を牽引すると予想されます。2023年5月には、航空機メーカーのVoltAeroがフランスにハイブリッド電気航空機の製造施設を建設する計画を発表しました。このように、同地域における新型航空機の生産増加は、同地域における先端複合材料の需要を促進します。

- 多くの国々が、ハードウェアを現地生産する一方で、国内防衛産業の成長に注力しています。これらの要因は、予測期間中に先端複合材料の需要を促進すると予想されます。したがって、上記の要因から、予測期間中は航空宇宙・防衛用途セグメントが市場を独占すると予想されます。

市場を独占する北米地域

- 予測期間中、北米地域が先端複合材料市場を独占すると予想されます。米国、カナダ、メキシコなどの国々では、航空宇宙・防衛、自動車、エレクトロニクス産業で先端複合材料の需要が増加しています。

- 運輸統計局のデータによると、米国の航空会社は2022年に8億5,300万人の旅客を運び、その成長率は2021年の6億7,400万人と比べて30%でした。そのため、複数の航空会社が、増加する航空旅客需要に対応するため、保有機材を拡大し、先進的機能を備えた航空機を調達しています。例えば、2022年2月、American AirlinesはBoeingに737 Max 8を30機発注しました。このように、民間航空機に対する需要の高まりは、現在の研究市場を牽引すると予想されます。

- 北米、特に米国では、エレクトロニクス産業は緩やかな成長が見込まれています。新しい技術製品への需要の増加が、今後の市場拡大に貢献すると予想されます。

- 米国では、エレクトロニクス産業における技術の進歩や研究開発活動において、技術革新のペースが速いため、より新しく高速なエレクトロニクス製品への需要が高まっています。消費者技術協会(Consumer Technology Association)によると、米国の民生用電子機器技術販売による小売売上高は、2021年の4,610億米ドルに対し、2022年には5,050億米ドルになると推定されています。

- 先進医療技術協会(AMTA)によると、アメリカの医療技術企業は、患者の診断と質の高い治療法の提供、治療成績の向上、医療コストの削減、経済成長の推進において重要な役割を果たしています。米国は世界最大の医療機器市場であり、世界の医療機器市場の40%以上を占めています。

- OICAによると、米国の自動車生産台数は2021年の915万台に対し、2022年には1,006万台に達し、成長率は9%です。したがって、自動車生産台数の増加は、同地域の先端複合材料市場を牽引すると考えられます。

- このような要因から、同地域の先端複合材料市場は予測期間中に成長率を記録すると予想されます。

先端複合材料産業概要

先端複合材料市場は細分化されています。市場の主要企業には、Toray Industries Inc.、Kolon Industries Inc.、SGL Carbon、Mitsubishi Chemical Carbon Fiber and Composites Inc.、TEIJIN LIMITEDなどがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 航空宇宙・防衛産業における軽量材料の需要増加

- 低燃費で軽量な自動車に対する需要の高まり

- その他の促進要因

- 抑制要因

- 原料価格の上昇

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 複合材料タイプ

- セラミックマトリックス複合材料(CMC)

- 金属マトリックス複合材料(MMC)

- ポリマーマトリクス複合材料(PMC)

- 芯材

- 繊維タイプ

- アラミド繊維

- ガラス繊維

- 炭素繊維

- エンドユーザー産業

- 航空宇宙・防衛

- 風力エネルギー

- 運輸

- 海洋

- 消費財

- その他のエンドユーザー産業(医療、エレクトロニクスなど)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- ノルディック

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3B-the fibreglass company

- Dow

- Henkel Corporation

- Hexcel Corporation

- HYOSUNG ADVANCED MATERIALS

- Kolon Industries Inc.

- Mitsubishi Chemical Carbon Fiber and Composites Inc.

- Owens Corning

- SGL Carbon

- Solvay

- TEIJIN LIMITED

- Toray Industries Inc.

- Yantai Tayho Advanced Materials Co. Ltd

第7章 市場機会と今後の動向

- 先進複合材料のリサイクル

- ナノ複合材料の需要増加

目次

The Advanced Composite Materials Market size is estimated at USD 2.46 billion in 2025, and is expected to reach USD 3.29 billion by 2030, at a CAGR of greater than 6% during the forecast period (2025-2030).

The COVID-19 pandemic had negatively impacted the market for advanced composite materials. The nationwide lockdowns and strict social distancing measures resulted in the closure of airplane and automotive manufacturing facilities, thereby affecting the market for advanced composite materials. However, post-COVID pandemic, the market recovered well after the restrictions were lifted. The market recovered significantly, owing to the rise in consumption of advanced composite materials in aerospace and defense, wind energy, and automotive end-user industries.

The increasing demand for lightweight materials in the aerospace and defense industries and the rising demand for fuel-efficient and lightweight vehicles are expected to drive the market.

The increasing prices of raw materials are expected to hinder the market's growth.

The recycling of advanced composites and the increasing demand for nanocomposites are expected to create opportunities for the market during the forecast period.

The North American region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period due to rising demand for advanced composite materials in aerospace and defense, wind energy, automotive, and marine end-user industries.

Advanced Composite Materials Market Trends

Aerospace and Defense End-user Industry to Dominate the Market

- The demand for composite materials is increasing in the aerospace industry. The use of composite materials in commercial transport aircraft is massive because reduced airframe weight enables better fuel economy and, therefore, lowers operating costs.

- The advanced composite materials include high strength, stiffness, heat and chemical resistivity, electrical conductivity, and various other thermal and chemical properties. Thus, the usage of advanced composites is increasing in the aerospace and defense industry.

- According to the International Air Transport Association (IATA), the global revenue for commercial airlines was valued at USD 472 billion in 2021 and USD 727 billion in 2022, registering a growth rate of 43.6% Y-o-Y. Furthermore, the revenue is expected to reach USD 779 billion by the end of 2023. Such factors are likely to increase the demand for advanced composite materials from aerospace parts manufacturing in the years to come.

- Boeing, one of the largest global aircraft manufacturers, announced it delivered a total of 480 aircraft in 2022, which is an increase of 41% compared to the total of 340 aircraft across the world in 2021. Thus, the increasing deliveries of new aircraft are expected to drive the demand for advanced composites.

- The United States is the manufacturing hub for airplanes in the North American region. Airbus and Boeing are the largest manufacturers of airplanes in the country. For instance, in 2022, Airbus delivered 661 commercial aircraft, registering 1,078 gross new orders by the end of the year. Similarly, Boeing Aeroplane OEM company received orders for 57 of the 737 Max 8 jets, with delivery expected through 2025. Thus, the increasing demand for airplanes is expected to drive the market for advanced composite materials.

- In Europe, the rising production of aircraft, mainly in countries such as France and Germany, is expected to drive the demand for advanced composite materials. In May 2023, VoltAero, an aircraft manufacturer, announced plans to build a manufacturing facility for hybrid-electric aircraft in France. Thus, the increasing production of new aircraft in the region will drive the demand for advanced composites in the region.

- Many countries are focusing on growing a domestic defense industry while manufacturing hardware locally. These factors are expected to drive the demand for advanced composite materials during the forecast period. Hence, owing to the factors mentioned above, the aerospace and defense application segment is expected to dominate the market during the forecast period.

North America Region to Dominate the Market

- The North American region is expected to dominate the market for advanced composite materials during the forecast period. The demand for advanced composite materials is increasing in aerospace and defense, automotive, and electronics industries in countries like the United States, Canada, and Mexico.

- According to data from the Bureau of Transportation Statistics, airlines in the United States carried 853 million passengers in 2022 at a growth rate of 30% compared to 674 million passengers in 2021. Thus, several airline companies are expanding their fleet and procuring aircraft with advanced capabilities to cater to the increasing demand for air passengers. For instance, in February 2022, American Airlines ordered 30 new 737 Max 8 jets from Boeing. Thus, the rising demand for commercial airplanes is expected to drive the current studied market.

- In North America, especially in the United States, the electronics industry is expected to grow at a moderate rate. An increase in the demand for new technological products is expected to help the market expansion in the future.

- In the United States, the rapid pace of innovation in terms of the advancement of technologies and R&D activities in the electronics industry is driving the demand for newer and faster electronic products. According to the Consumer Technology Association, the retail revenue from consumer electronics and technology sales in the United States was estimated at USD 505 billion in 2022, compared to USD 461 billion in 2021.

- According to the Advanced Medical Technology Association (AMTA), America's medical technology companies play a crucial role in diagnosing and providing patients with quality treatment options, improving outcomes, reducing healthcare costs, and driving economic growth. The United States is the world's largest medical device market, accounting for over 40% of the global medical device market.

- According to OICA, in 2022, the United States automotive vehicle production reached 10.06 million compared to 9.15 million units manufactured in 2021, at a growth rate of 9%. Thus, the rise in vehicle production will drive the market for advanced composite materials in the region.

- Due to all such factors, the market for advanced composite materials in the region is expected to register a growth rate during the forecast period.

Advanced Composite Materials Industry Overview

The advanced composite materials market is fragmented in nature. Some of the major players in the market include (not in any particular order) TORAY INDUSTRIES INC., Kolon Industries Inc., SGL Carbon, Mitsubishi Chemical Carbon Fiber and Composites Inc., and TEIJIN LIMITED.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Lightweight Materials in the Aerospace and Defense Industry

- 4.1.2 Rising Demand for Fuel Efficient and Lightweight Vehicles

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Increasing Prices of Raw Materials

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Composite Type

- 5.1.1 Ceramic Matrix Composites (CMCs)

- 5.1.2 Metal Matrix Composites (MMCs)

- 5.1.3 Polymer Matrix Composites (PMCs)

- 5.1.4 Core Materials

- 5.2 Fiber Type

- 5.2.1 Aramid Fiber

- 5.2.2 Glass Fiber

- 5.2.3 Carbon Fiber

- 5.3 End-user Industry

- 5.3.1 Aerospace and Defense

- 5.3.2 Wind Energy

- 5.3.3 Transportation

- 5.3.4 Marine

- 5.3.5 Consumer Goods

- 5.3.6 Other End-user Industries (Medical, Electronics, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 UAE

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3B - the fibreglass company

- 6.4.2 Dow

- 6.4.3 Henkel Corporation

- 6.4.4 Hexcel Corporation

- 6.4.5 HYOSUNG ADVANCED MATERIALS

- 6.4.6 Kolon Industries Inc.

- 6.4.7 Mitsubishi Chemical Carbon Fiber and Composites Inc.

- 6.4.8 Owens Corning

- 6.4.9 SGL Carbon

- 6.4.10 Solvay

- 6.4.11 TEIJIN LIMITED

- 6.4.12 Toray Industries Inc.

- 6.4.13 Yantai Tayho Advanced Materials Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Recycling Advanced Composites

- 7.2 Increasing Demand for Nano Composites

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日