エンジンオイル-市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Engine Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1640684

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

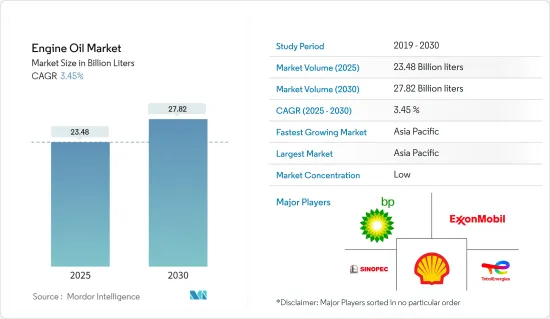

エンジンオイル市場規模は2025年に234億8,000万リットルと推定され、2030年には278億2,000万リットルに達すると予測され、予測期間(2025~2030年)のCAGRは3.45%です。

COVID-19危機は世界の自動車産業に影響を与え、ほとんどの地域で自動車の生産と販売の両方が突然停止しました。こうした作業停止により、世界中で何百万台もの自動車の生産が失われました。エンジンオイルは、エンジン全体の効率を向上させ、排出ガスを削減するために使用されるため、自動車産業はエンジンオイル市場に直接的な影響を与えています。しかし、2021年後半に規制が解除された後、自動車産業の活動が活発化したため、市場の成長は着実に回復し、市場の回復につながりました。

主要ハイライト

- 中期的には、自動車の生産・販売台数の増加と高性能潤滑油の採用拡大が市場の成長を牽引する重要な要因です。

- しかし、ドレイン間隔の延長と電気自動車(EV)のささやかな影響は、予測期間中に対象産業の成長を抑制すると予想される主要因です。

- 中東・アフリカにおける自動車産業の成長と、北米とアジア太平洋における数多くの今後の建設プロジェクトは、間もなく世界市場に有利な成長機会をもたらすと考えられます。

- アジア太平洋が市場を独占し、予測期間中に最も高いCAGRで推移する可能性が高いです。

エンジンオイル市場の動向

自動車産業からの需要の増加

- エンジンオイルは、内燃エンジンの潤滑に広く使用されています。エンジンオイルは75~90%の基油と10~25%の添加剤で構成され、世界中の自動車やその他の輸送セグメントで主に使用されています。

- エンジンオイルを使用する主要利点は、摩耗や損傷の低減、腐食防止、エンジンのスムーズな作動です。エンジンオイルは、可動部品の間に薄い膜を作ることで熱伝達を促進し、部品が接触する際の緊張を緩和します。

- 小型車の生産と販売の増加は、エンジンオイルの消費に直接的な影響を与えると推定されます。その結果、予測期間中にエンジンオイルの需要が増加すると予想されます。

- 国際自動車工業会(OICA)によると、2022年の世界の自動車生産台数は8,501万6,728台に達し、前年比5.9%増となりました。2021年と2022年の自動車生産台数の前年比成長率は6%でした。

- 同様に、OICAによると、2022年の商用車生産台数は5,749万台に達し、2021年の5,644万台と比較して成長を記録しました。

- 一方、米国商務省経済分析局によると、2022年の小型車小売販売台数は1,375万4,300台となり、2021年の1,494万6,900台と比較して最低となりました。

- また、ドイツ自動車工業会(Verband der Automobilindustrie)によると、ドイツの自動車生産台数は2022年に340万台に達し、2021年の310万台と比較して9.6%の伸びを記録しました。

- その結果、上記の要因は、将来的にエンジンオイル市場に大きな有益な影響を与えると予想されます。

市場を独占するアジア太平洋

- アジア太平洋は、主に自動車生産と発電産業の巨大な需要増加により、エンジンオイル市場を独占しています。

- 中国は世界有数の自動車メーカーです。同国の自動車産業は、燃費の向上と排出ガスの削減を目指した自動車の生産に重点を置き、製品の進歩を図っています。

- 中国汽車工業協会(CAAM)によると、2022年には中国で乗用車が約2,356万台、商用車が約330万台販売されました。

- 同様に、India Brand Equity Foundationによると、2022会計年度にはインドの発電能力は約400GWに増加します。これにより、以前からの発電能力の伸びは続いています。1992~2022年の間に、インドの発電能力は5倍に増加しました。

- 内閣府の発表によると、2022年の国内メーカーからの重電受注額は約2兆2,500億円(約152億2,000万米ドル)で、前年の約2兆1,500億円(約145億5,000万米ドル)から増加します。

- その結果、上記の要因は、今後数年間、同地域のエンジンオイル市場に大きな影響を与えると予測されます。

エンジンオイル産業概要

エンジンオイル市場は細分化されています。主要参入企業は、Total Energies、Exxon Mobile Corporation、BP p.l.c.、Shell PLC、China Petrochemical Corporationなどです(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 自動車生産・販売の増加

- 高性能潤滑油の採用増加

- 抑制要因

- ドレイン間隔の延長

- 電気自動車(EV)の将来的な影響はわずか

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 規制施策分析

第5章 市場セグメンテーション(市場規模(数量ベース))

- エンドユーザー産業

- 発電

- 自動車とその他の輸送機器

- 重機

- 冶金・金属加工

- 化学製造

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- フィリピン

- インドネシア

- マレーシア

- タイ

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- メキシコ

- カナダ

- その他の北米地域

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- スペイン

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- カタール

- アラブ首長国連邦

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AMSOIL INC

- Bharat Petroleum Corporation Limited

- BP p.l.c

- Chevron Corporation

- China Petrochemical Corporation

- Eni SPA

- Exxon Mobil Corporation

- FUCHS

- Gazpromneft-Lubricants, Ltd

- Gulf Oil International

- Hindustan Petroleum Corporation Limited

- Idemitsu Kosan Co.,Ltd

- Illinois Tool Works Inc.

- Indian Oil Corporation Ltd

- JX Nippon Oil & Gas Exploration Corporation

- LUKOIL

- Motul

- Petrobras

- PETRONAS Lubricants International

- Phillips 66 Company

- PT Pertamina Lubricants

- Repsol

- Shell PLC

- SK Enmove CO., Ltd

- Tide Water Oil Co. (India) Ltd

- TotalEnergies

- Valvoline Cummins Pvt. Ltd.

第7章 市場機会と今後の動向

- 中東・アフリカにおける自動車産業の成長

- 北米とアジア太平洋における数多くの建設プロジェクト

目次

The Engine Oil Market size is estimated at 23.48 billion liters in 2025, and is expected to reach 27.82 billion liters by 2030, at a CAGR of 3.45% during the forecast period (2025-2030).

The COVID-19 crisis impacted the global automotive industry, as both the production and sales of motor vehicles came to a sudden halt in most regions. These work stoppages led to a loss in the production of millions of vehicles across the world. The automobile industry has a direct effect on the engine oil market as it is used to improve the overall efficiency of an engine and reduce emissions. However, the market growth picked up steadily, owing to increased automotive activities after the lifting of restrictions in the second half of 2021, leading to market recovery.

Key Highlights

- Over the medium term, the increasing automotive production and sales and the increasing adoption of high-performance lubricants are significant factors driving the growth of the market studied.

- However, extended drain intervals and the modest impact of electric vehicles (EVs) are key factors anticipated to restrain the growth of the target industry over the forecast period.

- Nevertheless, the growing automotive industry in the Middle East and Africa and numerous upcoming construction projects in North America and APAC are likely to create lucrative growth opportunities for the global market soon.

- Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Engine Oil Market Trends

Increasing Demand from Automotive Industry

- Engine oils are widely used to lubricate internal combustion engines. They are composed of 75-90% base oils and 10-25% additives and are mostly used in automotive and other transport segments across the world.

- The major advantages of using engine oils are wear and tear reduction, corrosion protection, and the engine's smooth operation. They function by creating a thin film between the moving parts for enhancing heat transfer and reducing tension during the contact of parts.

- The increasing production and sales of light-duty vehicles are estimated with a direct impact on engine oil consumption. It, in turn, is anticipated to drive the demand for engine oil during the forecast period.

- According to the International Organization of Motor Vehicle Manufacturers (OICA), global motor vehicle production reached 85,016,728 units in 2022, and the production increased by 5.9% when compared to the previous year's data. Motor vehicle production growth year-on-year between the 2021 and 2022 markets was at 6%.

- Similarly, as per OICA, commercial vehicle production reached 57.49 million units in 2022 and registered growth when compared to 56.44 in 2021.

- Meanwhile, as per the Bureau of Economic Analysis of the United States Department of Commerce, light vehicle retail sales reached 13,754.3 thousand units, registering the lowest production when compared to 14,946.9 thousand units in 2021.

- Further, according to the German Association of the Automotive Industry (Verband der Automobilindustrie), automobile production in Germany reached 3.4 million in 2022 and registered a growth of 9.6% when compared to 3.1 million in 2021.

- As a result, the factors above are anticipated with a substantial beneficial influence on the engine oil market in the future years.

The Asia-Pacific Region to Dominate the Market

- Asia-Pacific dominated the engine oil market primarily due to the huge growing demand for automotive production and power generation industries.

- China holds the title of the world's leading automobile manufacturer. The nation's automotive industry is poised for product advancement, emphasizing the production of vehicles aimed at enhancing fuel efficiency and reducing emissions, addressing escalating environmental concerns attributed to increasing pollution levels in the country

- According to the China Association of Automobile Manufacturers(CAAM), in 2022, approximately 23.56 million passenger cars and 3.3 million commercial vehicles were sold in China.

- Similarly, according to the India Brand Equity Foundation, in the financial year 2022, India's power generation capacity rose to nearly 400 GW. Thereby, the growth in generation capacity from the previous years continues. Between 1992 and 2022, the country's electricity capacity experienced a five-fold increase.

- As per Cabinet Office Japan, in 2022, the order value for heavy electrical machinery from manufacturers in Japan amounted to approximately JPY 2.25 trillion (~USD 15.22 billion), increasing from around JPY 2.15 trillion (~USD 14.55 billion) in the previous year.

- As a result, the factors above are projected to have a substantial influence on the engine oil market in the region in the coming years.

Engine Oil Industry Overview

The engine oil market is fragmented in nature. The major players include (not in particular order) Total Energies, Exxon Mobile Corporation, BP p.l.c., Shell PLC, and China Petrochemical Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Automotive Production and Sales

- 4.1.2 Increasing Adoption of High-performance Lubricants

- 4.2 Restraints

- 4.2.1 Extended Drain Intervals

- 4.2.2 Modest Impact of Electric Vehicles (EVs) in the Future

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 End-user Industry

- 5.1.1 Power Generation

- 5.1.2 Automotive and Other Transportation

- 5.1.3 Heavy Equipment

- 5.1.4 Metallurgy and Metalworking

- 5.1.5 Chemical Manufacturing

- 5.1.6 Other End-user Industries

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Philippines

- 5.2.1.6 Indonesia

- 5.2.1.7 Malaysia

- 5.2.1.8 Thailand

- 5.2.1.9 Vietnam

- 5.2.1.10 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Mexico

- 5.2.2.3 Canada

- 5.2.2.4 Rest of North America

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Russia

- 5.2.3.6 Spain

- 5.2.3.7 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Qatar

- 5.2.5.4 United Arab Emirates

- 5.2.5.5 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AMSOIL INC

- 6.4.2 Bharat Petroleum Corporation Limited

- 6.4.3 BP p.l.c

- 6.4.4 Chevron Corporation

- 6.4.5 China Petrochemical Corporation

- 6.4.6 Eni SPA

- 6.4.7 Exxon Mobil Corporation

- 6.4.8 FUCHS

- 6.4.9 Gazpromneft - Lubricants, Ltd

- 6.4.10 Gulf Oil International

- 6.4.11 Hindustan Petroleum Corporation Limited

- 6.4.12 Idemitsu Kosan Co.,Ltd

- 6.4.13 Illinois Tool Works Inc.

- 6.4.14 Indian Oil Corporation Ltd

- 6.4.15 JX Nippon Oil & Gas Exploration Corporation

- 6.4.16 LUKOIL

- 6.4.17 Motul

- 6.4.18 Petrobras

- 6.4.19 PETRONAS Lubricants International

- 6.4.20 Phillips 66 Company

- 6.4.21 PT Pertamina Lubricants

- 6.4.22 Repsol

- 6.4.23 Shell PLC

- 6.4.24 SK Enmove CO., Ltd

- 6.4.25 Tide Water Oil Co. (India) Ltd

- 6.4.26 TotalEnergies

- 6.4.27 Valvoline Cummins Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Automotive Industry in Middle East and Africa

- 7.2 Numerous Upcoming Construction Projects In North America and APAC

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日