|

市場調査レポート

商品コード

1640636

中東・アフリカの受託包装:市場シェア分析、産業動向、成長予測(2025年~2030年)Middle East And Africa Contract Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東・アフリカの受託包装:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 101 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

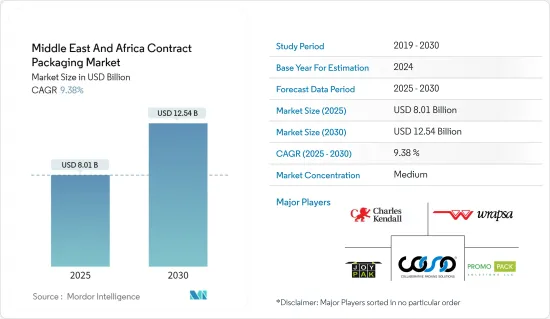

中東・アフリカの受託包装市場規模は2025年に80億1,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは9.38%で、2030年には125億4,000万米ドルに達すると予測されます。

瓶詰め・充填サービスは特に中東・アフリカで有望な成長を遂げています。食品、飲食品、医薬品の需要が増加しているため、多くの企業が安全性を高めるために包装をアウトソーシングしています。

中東とアフリカは世界のeコマース市場の主要企業として台頭しており、成長の大きな可能性を提供しています。この地域の数多くの国々とその第2級都市が、この動向に積極的に参加しています。この急成長の背景には、テクノロジーへのアクセスの向上とインターネット普及率の向上があり、オンライン・ショッピングの可能性を高めています。mFilterItが2023年12月に発表したレポートによると、同地域の小売普及率は約11%から12%で、80%以上の購入者がモバイル機器を利用し、70%がソーシャルメディアを活用して売り手と関わっています。増大する需要に対応するため、企業はオンラインショッピングを好む消費者向けに、包装のエンド・ツー・エンドまたは単体サービスを外注しています。

今後数年間で、注射剤は経口剤など他の投与方法を上回る市場シェアを獲得すると予想されています。その結果、注射剤の受託包装需要は増加すると予想され、大手製薬ベンダーは地域ごとの能力を高めると予想されます。

多くの地域ブランドは、食品の安全性や財務およびビジネスの敏捷性の必要性など、製造オペレーションを構築する代わりに共同包装を選択しています。コ・パッカーは、新規設備への支出を正当化できなかったり、収益性の低い新製品を生産するための設備から生産を切り離したりする可能性のある、この地域の十分な飲食品企業にとって不可欠な役割を果たしています。

しかし、自社包装に対する需要の高まりは、受託包装市場の成長を妨げると予想されます。例えば、外部の受託包装業者を利用する企業は、流通サイクルを最大で7日間延長することができ、その間は製品が見えにくくなります。商品を迅速かつ効果的に流通させたい企業にとっては、これが障壁となる可能性があります。

大半の消費者がオンラインショッピングを好む中、企業は高まる需要に対応するため、包装をエンド・ツー・エンドまたは単体でアウトソーシングしています。

中東・アフリカの受託包装市場動向

eコマース需要の増加が市場を大きく牽引

- eコマースパッケージング企業は、現代技術の重要な採用者であり推進者です。世界のeコマース企業の増加も、顧客のニーズによりよく応えるためのパッケージング・ソリューションに対する業界の需要に拍車をかけています。

- さらに、消費者包装商品(CPG)プロバイダーからの高い変動性要件により、サプライチェーンにおけるスピードとともにカスタマイズは、eコマースを通じて製品を提供する企業にとっての課題を作成し、したがって、柔軟性、敏捷性、臨機応変のために構築されているので、カスタマイズされたeコマースパッケージングソリューションのための受託包装会社からの要件をエスカレートさせる。

- 受託包装業者やフルフィルメント・サービス・プロバイダーは、限られた数量で小規模に事業を展開し、意思決定に携わる人員も少ないです。その結果、eコマース対応のパッケージング・イノベーションをより迅速に実施することができます。さらに、eコマース企業と協力することで、急成長するこのチャネルに最適化されたパッケージングへの道筋を短縮することができます。

- 米国農務省海外農業局によると、アラブ首長国連邦における2023年の小売eコマースの売上税別小売額は、前年の56億米ドルから約62億米ドルに達します。小売売上高が増加すると、一般的に包装商品の需要が高まり、主要企業は包装のニーズを包装請負会社に委託するようになります。このような需要の急増は、包装請負業者にとってのビジネスチャンスの拡大につながる可能性があり、小売業者の増大するニーズに対応するため、事業の拡大や新技術への投資を促す可能性があります。

著しい成長を遂げる飲料業界

- 加工に不可欠なインフラへの需要が高まる中、飲料メーカーやジュースメーカーは、より中核的な活動に力を入れ始めています。メーカーは、衛生的な加工基準を念頭に置きながら、適切な技術的専門知識とタイムリーで費用対効果の高いソリューションを提供することで、原料を保管する専用エリアを持つパッケージング・ベンダーに期待を寄せており、これがこの地域における飲料パッケージング受託サービスの需要を高めています。

- 新時代の飲料の多くは、流通は広範に及んでいるが販売量は限られているため、工場の関与が正当化されるにはあまりにも少量であるにもかかわらず、複数の製造拠点が必要とされています。ホットフィル製品への需要が高いため、有名ブランドを持つ大企業は、生産要件を満たすために受託包装業者を利用しています。

- 2024年2月の南アフリカ統計局のデータによると、南アフリカの消費者物価指数(CPI)は、食品とノンアルコール飲料に関して113.9ポイントと測定されました。製造業者が競争力のある価格設定を維持しながら消費者の需要を満たすために効率的でコスト効率の高いソリューションを求めているため、国内では受託包装サービスの需要が増加しています。

- 受託製造業者はまた、缶、ボトル、瓶、カートンなどの瓶詰めや充填、パレット陳列、販促用パッケージング、製品陳列、カスタム組立、手作業によるパッケージングなどのバンドル・サービスも提供しています。食品、飲食品、製薬業界は、一次包装を最も多く採用している業界のひとつです。そのため、これらの業界の生産能力全体の伸びは、地域全体で一次請負包装サービスの採用を促進すると予想されます。

- 受託包装企業の専門知識とインフラを活用することで、メーカーは効率的で柔軟な包装ソリューションの恩恵を受けながら、製品開発やマーケティングといった中核業務に集中することができます。この動向は、ダイナミックなビジネス環境においてサプライチェーン・オペレーションを最適化し、市場対応力を強化する上で、受託包装会社が提供するバリュー・プロポジションに対する認識の高まりを反映しています。

中東・アフリカの受託包装産業の概要

中東・アフリカのコントラクトパッケージング市場は半固体化しています。地域市場の開拓と海外直接投資における現地プレイヤーのシェア拡大が、この細分化を促進する主な要因となっています。

- 2023年9月- 医薬品の製造、包装、社内ラボを提供する南アフリカの第三者医薬品製造・包装会社であるWrapsaは、さらなる現地化に注力する計画を明らかにしました。同社は、錠剤、シロップ剤、軟膏剤、粉末剤、発泡剤、グミなど、あらゆる医薬品フォーマットと包装に対応できます。

- 2023年1月-StrongPack社は、2023年初頭にナイジェリアの高速PET水ラインの一部としてSidel社のブロー成形機を設置すると発表しました。StrongPackはナイジェリアのノンアルコール飲料の共同パッカーのひとつです。新しい毎時8万6,000本の高速ラインはアフリカ最速となり、StrongPack社がスティルウォーターのコ・パッキング市場に参入することを示しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力度-ポーターの5フォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場力学

- 市場促進要因

- 急速な技術の進歩

- 小売チェーンの開発

- 市場抑制要因

- 原材料と包装製品のコスト上昇

第6章 市場セグメンテーション

- サービスタイプ別

- 一次包装

- 二次包装

- 三次包装

- 業界別

- 飲料

- 食品

- 医薬品

- ホーム&ファブリックケア

- ビューティーケア

- 国別

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- エジプト

- ナイジェリア

第7章 競合情勢

- 企業プロファイル

- Joypak(Pty)Ltd.

- StrongPack Ltd.

- Collaborative Packing Solutions

- Charles Kendall Group

- Promo Pack Solutions LLC

- Al Bustan Co-Packing LLC

- Al Sharaf Repacking Services

- Gulf Trading and Refrigerating LLC(GULFCO)

- Wrapsa(Pty)Ltd.

- PackMan Packaging

第8章 投資分析

第9章 市場の将来展望

The Middle East And Africa Contract Packaging Market size is estimated at USD 8.01 billion in 2025, and is expected to reach USD 12.54 billion by 2030, at a CAGR of 9.38% during the forecast period (2025-2030).

Bottling and filling services have particularly experienced promising growth in the Middle East and Africa. Owing to the increased demand for food, beverage, and pharmaceutical needs, many businesses have outsourced their packaging for increased safety.

The Middle East and Africa have emerged as key players in the global e-commerce market, offering substantial potential for growth. Numerous countries in the region and their tier-two cities are actively participating in this trend. This surge is driven by increased accessibility to technology and higher internet penetration rates, amplifying online shopping prospects. According to a report published by mFilterIt in December 2023, retail penetration in the region stands at approximately 11% to 12%, with over 80% of buyers utilizing mobile devices and 70% leveraging social media to engage with sellers, creating opportunities for contract packaging services. To keep up with the growing demand, businesses outsource their packaging end-to-end or standalone services to consumers who prefer to shop online.

Over the upcoming years, injectables are anticipated to gain a market share that surpasses that of other administration methods, such as oral. As a result, contract packaging demand for injectable solutions is expected to rise, and significant pharmaceutical vendors are anticipated to increase their regional capabilities.

Many regional brands opt for co-packing instead of building their manufacturing operations, including food safety and the need for financial and business agility. Co-packers play an essential role for ample food and beverage companies in the region that may be unable to justify spending on new equipment or divert production from equipment to produce new and less profitable products.

However, the growing demand for in-house packaging is anticipated to hinder the market growth for contract packaging. For instance, businesses that use outside contract packagers can extend their distribution cycle by up to seven days, during which their product is less visible. Companies looking to distribute their goods quickly and effectively may find this a barrier.

With most consumers prefer online shopping channels, companies have been outsourcing their packaging end-to-end or standalone services to meet the growing demand.

Middle East And Africa Contract Packaging Market Trends

Increasing Demand in E-Commerce will Significantly Drive the Market

- E-commerce packaging companies are significant adopters and drivers of modern technology. The increasing number of global e-commerce companies is also fueling the industry's demand for packaging solutions to better cater to customers' needs.

- Additionally, with high variability requirements from Consumer-packaged goods (CPG) providers, customization along with speed in the supply chain creates a challenge for product offering companies via e-commerce, thus escalating the requirements from contract packaging companies for a customized e-commerce packaging solution, as they are built for flexibility, agility, and resourcefulness.

- Contract packers and fulfillment service providers operate on a smaller scale with limited volumes and fewer people involved in decision-making. As a result, they can implement e-commerce-ready packaging innovations more quickly. Furthermore, collaborating with e-commerce companies can shorten the path to optimized packaging for this rapidly growing channel.

- According to the USDA Foreign Agricultural Service, in 2023, the retail value, excluding sales tax of retail e-commerce in the United Arab Emirates, reached around USD 6.2 billion, up from USD 5.6 billion in the previous year. As retail sales increase, there is typically a higher demand for packaged goods, leading companies to outsource their packaging needs to contract packaging firms. This surge in demand can lead to increased opportunities for contract packaging providers, potentially prompting them to expand their operations or invest in new technologies to meet the growing needs of retailers.

Beverage Industry to Witness Significant Growth

- With the increasing demand for essential infrastructure to process, beverage, and juice manufacturers have started focusing more on core activities. Manufacturers are looking forward to packaging vendors with a dedicated area to store the raw material by providing the right technical expertise and timely and cost-effective solutions while keeping in mind hygienic processing standards, which has given rise to the demand for contract beverage packaging services in the region.

- Many new-age beverages have widespread distribution but limited volume, necessitating multiple manufacturing locations for volumes far too small to justify plant involvement. Due to the high demand for hot-fill products, large corporations with well-known brands have turned to contract packers to meet their production requirements.

- As per Statistics South Africa data in February 2024, the Consumer Price Index (CPI) in South Africa was measured at 113.9 points regarding food and non-alcoholic beverages. There is an uptick in demand for contract packaging services in the country as manufacturers seek efficient and cost-efficient solutions to meet consumer demand while maintaining competitive pricing.

- Contract manufacturers also provide bundling services such as bottling and filling, pallet displays, promotional packaging, product displays, custom assembly, manual packaging, etc., for cans, bottles, jars, cartons, etc. The food, beverage, and pharmaceutical industries are some of the biggest adopters of primary packaging. Therefore, the growth in the overall production capacity of these industries is expected to drive the adoption of primary contract packaging services across the region.

- By leveraging the expertise and infrastructure of contract packaging firms, manufacturers can focus on their core competencies, such as product development and marketing, while benefitting from efficient and flexible packaging solutions. This trend reflects a growing recognition of the value proposition offered by contract packaging companies in optimizing supply chain operations and enhancing market responsiveness in a dynamic business environment.

Middle East And Africa Contract Packaging Industry Overview

The Middle East and Africa contract packaging market is semi-consolidated. The development of regional markets and the increasing shares of local players in foreign direct investments are the major factors promoting this fragmentation.

- September 2023 - Wrapsa, a South African third-party pharmaceutical manufacturing and packaging company offering pharma manufacturing, packing, and an in-house laboratory, revealed its plan to focus on more localization. The company can cater to all medicine formats and packaging, including tablets, syrups, ointments, powders, effervescent, or gummies.

- January 2023 - StrongPack announced the installation of a blow-molder from Sidel as part of a high-speed PET water line in Nigeria in early 2023. StrongPack is one of Nigeria's co-packers of non-alcoholic beverages. The new 86,000 bottles per hour (bph) high-speed line is set to be the fastest in Africa, indicating StrongPack's entry into the still water co-packing market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industrial Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's 5 Force Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Technology Advancements

- 5.1.2 Development in the Retail Chain

- 5.2 Market Restraints

- 5.2.1 Increasing cost of Raw material and Packaging products

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Primary Packaging

- 6.1.2 Secondary Packaging

- 6.1.3 Tertiary Packaging

- 6.2 By End-User Vertical

- 6.2.1 Beverages

- 6.2.2 Food

- 6.2.3 Pharmaceuticals

- 6.2.4 Home and Fabric Care

- 6.2.5 Beauty Care

- 6.3 By Country

- 6.3.1 United Arab Emirates

- 6.3.2 Saudi Arabia

- 6.3.3 South Africa

- 6.3.4 Egypt

- 6.3.5 Nigeria

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Joypak (Pty) Ltd.

- 7.1.2 StrongPack Ltd.

- 7.1.3 Collaborative Packing Solutions

- 7.1.4 Charles Kendall Group

- 7.1.5 Promo Pack Solutions LLC

- 7.1.6 Al Bustan Co- Packing LLC

- 7.1.7 Al Sharaf Repacking Services

- 7.1.8 Gulf Trading and Refrigerating LLC (GULFCO)

- 7.1.9 Wrapsa (Pty) Ltd.

- 7.1.10 PackMan Packaging