|

市場調査レポート

商品コード

1907314

欧州のフレキシブル包装市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Europe Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のフレキシブル包装市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

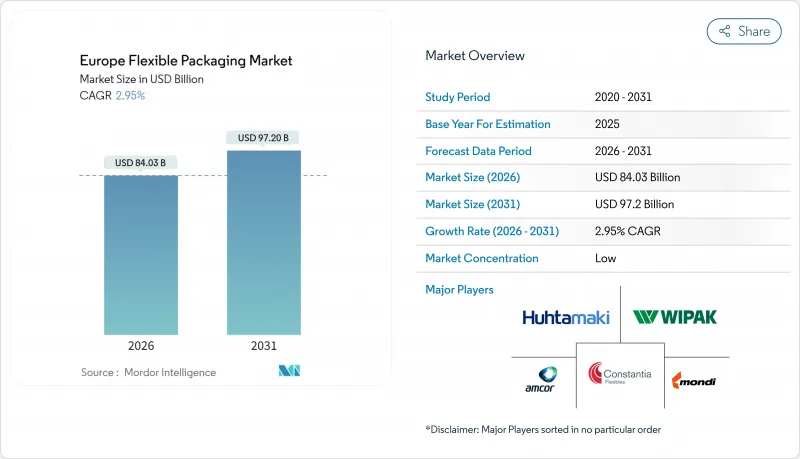

欧州のフレキシブル包装市場規模は、2026年に840億3,000万米ドルと推定され、2025年の816億2,000万米ドルから成長が見込まれます。

2031年の予測では972億米ドルに達し、2026年から2031年にかけてCAGR2.95%で拡大する見通しです。

この成長軌跡は、EUのより厳格なリサイクル義務化、電子商取引の荷物量の拡大、長期保存が必要な便利食品への需要加速に起因します。包装および包装廃棄物規制(PPWR)が2030年までに再生プラスチック30%含有を推進する中、単一素材フィルムの革新が加速しており、生分解性オプションも小規模ながら拡大しています。ブランドオーナーは物流コスト削減のため軽量パウチへの移行を継続していますが、フィルムやラップは食品・工業製品ラインにおける汎用性から、依然として数量ベースで主流を占めています。上位7社のサプライヤーが売上高の約4分の1しか占めていないという中程度の競合環境は、バリア技術やデジタル印刷におけるニッチな機会を地域専門企業が獲得する余地を生み出しています。

欧州フレキシブル包装市場の動向と洞察

EU循環型経済目標が牽引する再生可能単一素材フィルムの需要急増

PPWR(包装廃棄物指令)により、2030年までに欧州で販売される全ての包装はリサイクル可能であることが義務付けられ、コンバーター各社は機械的リサイクル工程を通過する単一素材形式へ多層構造の再設計を迫られています。ネスレ社はペットフード用ポリプロピレンレトルトパウチによりカーボンフットプリントを60%削減したと報告し、サイカフレックス社は2025年までに消費後再生材を組み込んだ完全リサイクル可能な製品群の実現を計画しています。紙は再生材含有率の義務対象外であるため、ケーラーペーパー社のNexPlusバリアラインなど紙ベースの代替品が注目を集めています。多層構造の性能低下を補うため、サプライヤー各社はポリプロピレン基材上で酸素透過率を95%低減するオルモサー(ORMOCER)などの無機コーティングを試験中です。拡大生産者責任制度の費用負担が非再生可能素材に課されることで、採用スケジュールが前倒しされています。

電子商取引の急成長が柔軟な郵送用包装材・保護材の需要を押し上げる

多くのEU市場においてオンライン小売は二桁成長を継続しており、小包あたりの輸送コストを削減する軽量メール袋や保護フィルムの採用を促進しています。HP Indigo 200Kなどのデジタル印刷機は、季節や地域別のプロモーションに合わせて外装グラフィックをパーソナライズ可能であり、フレキソ印刷と比較してセットアップ時の廃棄物を削減します。ウテコのハイブリッドプラットフォーム「サファイアアクア」は、食品接触規制を満たす低移行性水性インクを使用し、150 mpm(分あたりメートル)の速度で1,200×1,200 DPIの印刷を実現します。中小規模のEコマースブランドはフルフィルメント業務を外部委託する傾向が強まっており、自動包装ラインに対応した柔軟なフォーマットを好む間接流通業者を通じた出荷量が増加しています。

EUの厳格なプラスチック・包装廃棄物規制によりコンプライアンスコストが増加

中小コンバーター企業は、リサイクル可能性の認証取得、再生樹脂の統合、調和された表示基準を満たすためのグラフィック再設計に多額の投資を迫られています。非準拠包装に対する拡大生産者責任(EPR)費用は、納入コストを50%以上押し上げる可能性があり、新ラインが稼働するまで利益率を圧迫します。2026年に施行されるPFAS禁止により、食品包装用耐油性コーティングの再配合が迫られる一方、2028年施行の表示規則は数千のSKUにわたるアートワーク変更を促します。

セグメント分析

2025年時点で欧州フレキシブル包装市場におけるプラスチックのシェアは61.88%を占め、食品・EC向けラインにおけるポリエチレンのコストパフォーマンス優位性が牽引しています。石油由来基材は現在も主導権を握るもの、ブランドオーナーがPPWR(生産者責任拡大制度)への適合を追求する中、欧州フレキシブル包装市場ではバイオベース・堆肥化可能フィルムへの関心が高まっており、CAGR5.66%で拡大中です。紙・板紙は再生材含有率の義務付け対象外となっており、ケーラーペーパー社などのサプライヤーはバリアコーティングを施したグレードで81.5%の再生利用率を達成し、進展を見せております。金属化構造は絶対的なバリア性が求められる医薬品や高級食品分野で依然として使用されていますが、ニッチな需要により数量変動の影響を大きく受けずに済んでおります。PETの化学的リサイクル技術(脱重合によるバージン原料相当の原料化を含む)は、2027年までに食品グレード樹脂の安定供給を目指す取り組みであり、リサイクル率目標の上昇の中でPETの地位を安定させる重要な節目となり得ます。

欧州のフレキシブル包装市場では、従来型ポリオレフィン層と生分解性コーティングを組み合わせたハイブリッドラミネートの試験が進められています。これにより、保存期間中のシール性能を維持しつつ、土壌分解を加速させることが可能です。透明スナックフィルムの主力素材は依然としてBOPPですが、レトルト対応蓋材にはシール性に優れたCPPが好まれています。バイオプラスチックは現在、総生産量のごく一部に過ぎませんが、堆肥化可能な買い物袋から、PLA、PBAT、澱粉をブレンドした高バリア構造へと進化しています。コンバーター各社は、原料のスケールアップと需要を喚起する規制が整う2028年以降でなければ、化石由来グレードとのコスト競争力達成は難しいと予測しています。

フィルムおよびラップは、ベーカリー製品、チーズ、工業用部品など大量消費カテゴリーに対応するため、2025年時点で欧州フレキシブル包装市場の43.92%を占めました。しかしながら、レトルト対応ペットフード包装や電子レンジ対応レトルト食品など、外出先での消費ライフスタイルに適した製品に支えられ、パウチは2031年までCAGR6.55%で拡大を続けています。スタンドアップ形式は棚スペースの有効活用とブランド認知度向上に寄与し、小売業者から優遇された陳列位置を獲得しています。ネスレ社のリサイクル可能なレトルトパウチは、従来構造と比較して性能を維持しながらカーボンフットプリントを60%削減できる事例を示しています(Packaging Digest)。

袋形式は、重量制限により薄肉代替品の採用が難しい農業用種子・肥料・DIY市場で引き続き主流です。デジタル印刷技術の普及により、コンバーターは5,000単位未満の小ロットでもSKU単位のカスタマイズを提供可能となり、単位経済性を損なわずにニッチなグルメブランドがライフサイクル早期からパウチ包装を採用する動きを促進しています。オーバーラップ包装やシュリンクスリーブは、飲料や医薬品分野における改ざん防止ソリューションとして依然重要ですが、リサイクル可能性については厳しい視線が向けられています。欧州におけるペット飼育率の二桁成長は、製品の鮮度と香りの保護を保証するレトルトパウチやスタンドアップパウチの需要をさらに後押ししています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- EU循環型経済目標を背景とした再生可能単一素材フィルムの需要急増

- 欧州における電子商取引の加速的成長が、フレキシブルメーラー及び保護包装フォーマットの需要を押し上げております

- 消費者の利便性と分量管理製品への志向が柔軟性のあるパウチの採用を促進

- 高バリア共押出技術の発展によるレトルト食品の保存期間延長

- デジタル印刷およびハイブリッド印刷の普及拡大により、小ロット生産と大量カスタマイズが可能に

- レトルト加工・スタンドアップパウチを用いた欧州ペットフード産業の急速な拡大

- 市場抑制要因

- EUの厳格なプラスチック・包装廃棄物規制によりコンプライアンスコストが増加

- 多層フィルムのリサイクルインフラが限られていることが循環性目標の達成を妨げております

- エネルギー危機後のポリオレフィン及びアルミ箔価格の変動が利益率に影響

- 持続可能性を重視するブランド間における硬質リサイクル代替品からの競合圧力

- サプライチェーン分析

- 規制の見通し

- テクノロジーの展望

- 投資分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 素材タイプ別

- プラスチック

- ポリエチレン(PE)

- 二軸延伸ポリプロピレン(BOPP)

- キャストポリプロピレン(CPP)

- ポリエチレンテレフタレート(PET)

- ポリスチレン(PS)および発泡ポリスチレン(EPS)

- その他のプラスチック種類

- 紙および板紙

- 金属

- 生分解性および堆肥化可能な素材

- プラスチック

- 製品タイプ別

- パウチ

- バッグ

- フィルムおよびラップ

- その他の製品タイプ

- エンドユーザー業界別

- 食品

- 飲料

- 医療・医薬品

- 化粧品・パーソナルケア

- 産業用

- その他の最終用途産業

- 流通形態別

- 直接販売

- 間接販売

- 国別

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Amcor PLC

- Mondi Group

- Huhtamaki Oyj

- Constantia Flexibles GmbH

- Sealed Air Corporation

- Coveris Management GmbH

- ProAmpac LLC

- Novolex Holdings Inc.

- Sonoco Products Company

- Bischof+Klein SE & Co. KG

- Wipak Oy

- Schur International A/S

- Gualapack SpA

- ePac Holdings LLC

- Danaflex Group

- Cellografica Gerosa SpA

- Di Mauro Officine Grafiche SpA

- Bak Ambalaj Sanayi ve Ticaret AS

- Flextrus AB

- Sipospack Kft.

- Clondalkin Flexible Packaging

- Innovia Films Ltd.

- AR Packaging Group AB

- RKW Group

- Plastopil Hazorea Co. Ltd.

- Schur Flexibles Group

- Glenroy Inc.

- Leefung ASG Europe