|

市場調査レポート

商品コード

1640539

アジア太平洋地域の接着剤およびシーラント:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Asia-Pacific Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の接着剤およびシーラント:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

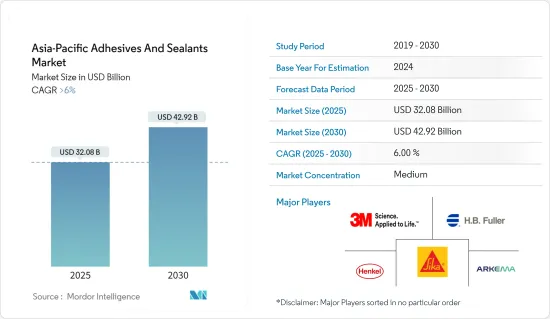

アジア太平洋地域の接着剤およびシーラント市場規模は2025年に320億8,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは6%を超え、2030年には429億2,000万米ドルに達すると予測されます。

この地域はCOVID-19パンデミックの悪影響を受けました。同地域の接着剤およびシーラント市場も同様の状況に直面しました。しかし、現在ではパンデミック以前の水準に達しており、市場は大きなペースで成長すると予想されます。

世界中で拡大する包装産業と建築・建設産業が、予測期間中に接着剤とシーリング剤の需要を牽引すると思われます。

しかし、揮発性有機化合物の使用に関する政府の厳しい環境規制が市場拡大の妨げになると予想されます。

バイオベースの接着剤の技術革新と開発、複合材料の接着へのシフトは、接着剤およびシーラント市場に機会を提供すると思われます。

中国は、自動車、建設、エレクトロニクス、包装などのエンドユーザー産業が消費を牽引する、同地域最大の接着剤およびシーラント市場となります。

アジア太平洋地域の接着剤およびシーラント市場の動向

市場を独占するパッケージングセグメント

- 紙パッケージング製品は、紙器、段ボール箱、紙袋、液体板紙で構成されます。組織小売の大幅な増加に伴い、スーパーマーケットや近代的なショッピングセンターの急増により、紙製包装の需要は増加すると予想されます。

- 工業製品の極めて高い割合が包装されて販売されているが、これは保管や輸送に安定性が要求されるためか、美観上の理由によるものです。現在使用されている包装資材のほとんどは、異なる素材を張り合わせたもので、接着剤を使用する必要があります。

- このセグメントの成長を加速させている重要な要因のひとつに、eコマース・プラットフォームの拡大や、大衆の所得水準の上昇に伴う消費の増加があります。

- 中国はアジア太平洋地域地域の包装産業に大きく貢献している国です。2021年から2025年の「5カ年計画」で、中国はプラスチックのリサイクルと焼却能力を向上させ、「グリーン」プラスチック製品を推進し、包装や農業におけるプラスチックの誤用と闘うと発表しました。新たな5カ年計画では、商店や宅配業者に「不合理な」プラスチック包装を減らすよう働きかけ、都市部でのゴミ焼却率を昨年の58万トンから2025年までに1日あたり約80万トンに引き上げるとしています。このような開発により、リサイクル可能な軟質プラスチック包装の国内需要が増加すると予想されます。予測期間中、アリババのようなeコマース大手の台頭が包装市場に拍車をかけると予想されます。例えば、10日間続いたアリババのショッピングイベント「ダブル11」では、中国の買い物客は約19億件の出荷を受けました。

- インドでは、プラスチック包装は毎年20~25%という著しい成長率で伸びており、680万トンに達しているのに対し、紙包装は760万トンと評価されています。これらの動向は、包装分野における接着剤の消費にプラスの影響を与えました。

- 2022年6月、環境省傘下の連邦機関である中央公害防止委員会(CPCB)は、特定の使い捨てプラスチック製品を非合法化するための措置リストを発表しました。このような措置により、国内での紙製包装の需要が高まることが予想されます。

- さらに、インドのような国では、オンライン食品注文の需要が増加しており、食品包装市場における包装食品箱の利用を後押ししています。例えば、2022年2月、著名な食品宅配会社の1つであるZomatoは、過去5年間で、Zomatoにおける食品宅配レストランの月間平均アクティブ数は6倍、月間平均取引顧客数は13倍に成長したと発表しました。

- オンライン小売ショッピングは、インターネット技術やウェブアプリケーションの台頭とともに高い割合で増加しており、これが主にパッケージ業界の成長を支えています。

- 在韓英国商工会議所によると、韓国の飲食ビジネスは、ハイパーマーケットの優位性とeコマース・プラットフォームを通じた販売の拡大によって定義されています。韓国のF&B市場は、2024年までに761億ポンド(899億8,000万米ドル)に達すると予想されています。

- さらに、持続可能な包装に対する政府の取り組みが、紙製包装製品の採用を義務付けています。例えば、韓国の2050年カーボンニュートラル目標の一環として、韓国環境省は2022年6月10日からチェーンカフェやファーストフード店の使い捨てカップに300ウォン(0.25米ドル)のデポジットを義務付けると発表しました。この規制は、100以上の支店と38,000以上の店舗を持つチェーン店に適用されます。

- したがって、紙、板紙、包装業界における広範な用途と、主にeコマース業界の成長による包装資材の需要増加により、この分野における接着剤とシーリング剤の消費は、予測期間中にこの地域でさらに増加すると予想されます。

アジア太平洋地域では中国が優位を占める

- アジア太平洋地域の接着剤およびシーラントの消費は中国が支配的です。建設活動の成長、包装産業での消費の増加、国際市場での需要を支えるエレクトロニクス生産は、同国の接着剤およびシーラント市場の消費を促進する主な要因の一部です。

- 中国の成長は、主に住宅および商業建築部門の急速な拡大と同国の経済拡大によって後押しされています。中国は継続的な都市化プロセスを奨励し、それに耐えており、その割合は2030年までに70%に達すると予測されています。その結果、中国のような国々における建築活動の活発化が、この地域の接着剤産業に拍車をかけると予測されています。すべてのそのような要因は、地域全体の接着剤の需要を増加させる傾向があります。

- 中国国家統計局によると、建設生産額は2021年の29兆3,100億人民元(4兆2,000億米ドル)から増加し、2022年には31兆2,000億人民元(4兆5,000億米ドル)を占める。さらに、住宅・都市・農村開発省の予測によると、中国の建設部門は2025年までGDPの6%を維持すると予想されています。

- 中国の乗用車用電気自動車(EV)市場は目覚ましい成長を続けており、2022年のEV販売台数は前年比87%増となります。BYD、Wuling、Chery、Changan、GACは、EV市場を独占する中国のトップブランドであり、地元ブランドが81%を占めています。さらに、BYDは2022年に市場シェアを前年比11%以上拡大し、中国市場におけるEVモデル上位10車種のうち6車種がBYDブランドによるものです。

- さらに、中国政府は2025年までに電気自動車の普及率が20%になると予測しています。そのため、自動車用電池の生産と消費が増加し、接着剤とシーリング剤の需要が高まると予想されます。

- さらに、中国は世界最大級のエレクトロニクス生産拠点を有しており、韓国、シンガポール、台湾といった既存の川上メーカーに厳しい競合を提供しています。スマートフォン、OLEDテレビ、タブレット端末などの電子製品は、市場のコンシューマーエレクトロニクス・セグメントにおいて需要の成長率が最も高いです。

- 中国では、中国から電子製品を輸入している国々における電子製品需要の高まりと、中間層の可処分所得の増加に伴い、電子製品の生産が伸びると予測されています。

- したがって、エンドユーザー産業におけるこのような動向はすべて、予測期間にわたって同国の接着剤およびシーラント市場の成長を促進すると予想されます。

アジア太平洋地域の接着剤およびシーラント産業の概要

アジア太平洋地域の接着剤およびシーラント市場は、その性質上、部分的に統合されています。主要企業(順不同)には、3M、アルケマ、シーカAG、H.B.フラー・カンパニー、ヘンケルAG &Co.KGaAです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 東南アジア諸国における包装産業の成長

- 建設セクターにおける需要の高まり

- その他の促進要因

- 抑制要因

- VOC排出に関する厳しい環境規制

- 原材料価格の高騰

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 接着剤樹脂別

- ポリウレタン

- エポキシ

- アクリル

- シリコーン

- シアノアクリレート

- VAE・EVA

- その他樹脂(ポリエステル、ゴムなど)

- 接着技術別

- 溶剤系

- 反応性

- ホットメルト

- UV硬化型接着剤

- 水性

- シーラント樹脂別

- シリコーン

- ポリウレタン

- アクリル系

- エポキシ

- その他の樹脂(瀝青、ポリサルファイドUV硬化型など)

- エンドユーザー産業別

- 航空宇宙

- 自動車

- 建築・建設

- 履物・皮革

- ヘルスケア

- 包装

- 木工・建具

- その他エンドユーザー産業(エレクトロニクス、コンシューマー/DIYなど)

- 地域別

- 中国

- インド

- 日本

- 韓国

- インドネシア

- マレーシア

- タイ

- ベトナム

- その他アジア太平洋地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Arkema

- Ashland

- Avery Dennison Corporation

- Beardow Adams

- Dow

- DuPont

- Dymax Corporation

- Franklin International

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers(Illinois Tool Works Inc.)

- Jowat AG

- Mapei Inc.

- Tesa SE(A Beiersdorf Company)

- Pidilite Industries Ltd.

- Sika AG

- Wacker Chemie AG

第7章 市場機会と今後の動向

- バイオベース接着剤の革新と開発

- 複合材料の接着へのシフト

The Asia-Pacific Adhesives And Sealants Market size is estimated at USD 32.08 billion in 2025, and is expected to reach USD 42.92 billion by 2030, at a CAGR of greater than 6% during the forecast period (2025-2030).

The region was negatively affected by the COVID-19 pandemic. The adhesives and sealants market in the region also faced a similar situation. However, the market has now reached pre-pandemic levels, and it is expected to grow at a significant pace.

Expanding packaging and building and construction industries around the globe are likely to drive demand for adhesives and sealants during the forecast period.

However, strict environmental regulations set by the government on the use of volatile organic compounds are anticipated to hamper market expansion.

The innovation and development of bio-based adhesives and shifting focus toward adhesive bonding for composite materials are likely to offer opportunities for the adhesives and sealants market.

China stands to be the largest market for adhesives and sealants in the region, where the consumption is driven by the end-user industries, such as automotive, construction, electronics, and packaging.

APAC Sealants & Adhesives Market Trends

Packaging Segment to Dominate the Market

- Packaging products in paper packaging comprises folding cartons, corrugated boxes, paper bags, and liquid paperboard. With the considerable increase in organized retail, the demand for paper packaging is anticipated to increase due to the rapid increase in supermarkets and modern shopping centers.

- An extremely high proportion of industrial products are sold in packages, either due to stability requirements for storage and transport or aesthetic reasons. Most packaging materials presently used are different materials laminated together, which require the use of adhesives.

- One of the critical factors that have been accelerating the growth of the segment includes a growing e-commerce platform and increasing consumption with the rise in income levels of the masses.

- China is a major contributing country in the APAC region for the packaging industry. In a 2021-2025 "five-year plan," China announced it would improve its plastic recycling and incineration capacities, promote "green" plastic products, and combat the misuse of plastic in packaging and agriculture. The new five-year plan would push merchants and delivery companies to reduce "unreasonable" plastic wrapping and increase garbage incineration rates in cities to about 800,000 tons per day by 2025, up from 580,000 tons last year. Such developments are expected to increase the country's demand for recyclable flexible plastic packaging. Over the projection period, the rise of e-commerce giants like Alibaba is expected to fuel the packaging market. For example, Chinese shoppers received approximately 1.9 billion shipments during Alibaba's Double 11 shopping event, which lasted 10 days.

- In India, plastic packaging is growing at a significant rate of 20-25% annually and has reached 6.8 million tons, whereas paper packaging is valued at 7.6 million tons. These trends positively impacted the consumption of adhesives in the packaging sector.

- In June 2022, the Central Pollution Control Board (CPCB), a federal agency under the Ministry of the Environment, released a list of steps to outlaw specific single-use plastic products by June 2022. Such measures are anticipated to drive the demand for paper packaging in the country.

- Moreover, in a country such as India, the growing demand for online food ordering is increasing, pushing the usage of packaged food boxes in the food packaging market. For instance, in February 2022, Zomato, one of the prominent food delivery companies, said that the average monthly active food delivery restaurants have grown by 6x, and average monthly transacting customers have grown by 13x on Zomato over the past five years.

- Online retail shopping is increasing at a higher rate with the rising internet technologies and web applications, which have primarily supported the packaging industry's growth.

- According to the British Chamber of Commerce in Korea, South Korea's F&B business is defined by hypermarket dominance and expanding sales through e-commerce platforms. The F&B market in South Korea is expected to reach GBP 76.1 billion (USD 89.98 billion) by 2024.

- Furthermore, the government initiatives for sustainable packaging are mandating the adoption of paper packaging products. For instance, as part of South Korea's 2050 carbon neutrality goal, the South Korean Ministry of Environment has announced that disposable cups from chain cafes and fast-food restaurants will require a 300 KRW (USD 0.25) deposit starting on June 10, 2022. This regulation applies to chains with more than 100 branches and 38,000 stores.

- Therefore, with extensive application in the paper, board, and packaging industry and increased demand for packaging materials mainly due to the growing e-commerce industry, the consumption of adhesives and sealants in this segment is expected to increase further in the region over the forecast period.

China to Dominate in the Asia-Pacific Region

- China dominates the region's consumption of adhesives and sealants. Growing construction activities, increasing consumption in the packaging industry, and electronics production to support demand in the international market are some of the key factors driving the consumption of the adhesives and sealants market in the country.

- China's growth is fueled mainly by rapid expansion in the residential and commercial building sectors and the country's expanding economy. China is encouraging and enduring a continuous urbanization process, with a projected rate of 70% by 2030. As a result, increased building activity in nations like China is projected to fuel the region's adhesive industry. All such factors tend to increase the demand for adhesives across the region.

- According to the National Bureau of Statistics of China, the value of construction output accounted for CNY 31.2 trillion (USD 4.5 trillion) in 2022, up from CNY 29.31 trillion (USD 4.2 trillion) in 2021. Moreover, as per the forecast given by the Ministry of Housing and Urban-Rural Development, China's construction sector is expected to maintain a 6% share of the country's GDP going into 2025.

- China's passenger electric vehicle (EV) market continues to grow at an impressive rate, with EV sales rising by 87% YoY in 2022. BYD, Wuling, Chery, Changan, and GAC are some of the top Chinese brands that dominate the EV market, with local brands commanding 81%. Additionally, in 2022, BYD increased its market share by over 11% Y-o-Y, with six out of the top 10 EV models in the Chinese market coming from the brand.

- Moreover, the Chinese government estimates a 20% penetration rate of electric vehicle production by 2025. Hence, this is anticipated to increase the production and consumption of vehicle batteries, thus increasing demand for adhesives and sealants in the market.

- Furthermore, China has one of the world's largest electronics production bases and offers tough competition to the existing upstream producers, such as South Korea, Singapore, and Taiwan. Electronic products, such as smartphones, OLED TVs, and tablets, have the highest growth rates in the consumer electronics segment of the market in terms of demand.

- In China, electronics production is projected to grow with the rising demand for electronic products in countries importing electronic products from China and the increase in the disposable income of the middle-class population.

- Hence, all such trends in the end-user industries are expected to drive the growth of the adhesives and sealants market in the country over the forecast period.

APAC Sealants & Adhesives Industry Overview

The Asia-Pacific adhesives and sealants market is partially consolidated in nature. The major players (not in any particular order) include 3M, Arkema, Sika AG, H.B. Fuller Company, and Henkel AG & Co. KGaA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Packaging Industry in South-East Asia Countries

- 4.1.2 Growing Demand in Construction Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Regarding VOC Emissions

- 4.2.2 High Fluctuations in Raw Material Pricing

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Adhesives Resin

- 5.1.1 Polyurethane

- 5.1.2 Epoxy

- 5.1.3 Acrylic

- 5.1.4 Silicone

- 5.1.5 Cyanoacrylate

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins (Polyester, Rubber, etc.)

- 5.2 Adhesives Technology

- 5.2.1 Solvent-borne

- 5.2.2 Reactive

- 5.2.3 Hot Melt

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Sealants Resin

- 5.3.1 Silicone

- 5.3.2 Polyurethane

- 5.3.3 Acrylic

- 5.3.4 Epoxy

- 5.3.5 Other Resins (Bituminous, Polysulfide UV-Curable, etc.)

- 5.4 End-User Industry

- 5.4.1 Aerospace

- 5.4.2 Automotive

- 5.4.3 Building and Construction

- 5.4.4 Footwear and Leather

- 5.4.5 Healthcare

- 5.4.6 Packaging

- 5.4.7 Woodworking And Joinery

- 5.4.8 Other End-user Industries (Electronics, Consumer/DIY, etc.)

- 5.5 Geography

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 South Korea

- 5.5.5 Indonesia

- 5.5.6 Malaysia

- 5.5.7 Thailand

- 5.5.8 Vietnam

- 5.5.9 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 Avery Dennison Corporation

- 6.4.5 Beardow Adams

- 6.4.6 Dow

- 6.4.7 DuPont

- 6.4.8 Dymax Corporation

- 6.4.9 Franklin International

- 6.4.10 H.B. Fuller Company

- 6.4.11 Henkel AG & Co. KGaA

- 6.4.12 Huntsman International LLC

- 6.4.13 ITW Performance Polymers (Illinois Tool Works Inc.)

- 6.4.14 Jowat AG

- 6.4.15 Mapei Inc.

- 6.4.16 Tesa SE (A Beiersdorf Company)

- 6.4.17 Pidilite Industries Ltd.

- 6.4.18 Sika AG

- 6.4.19 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation and Development of Bio-based Adhesives

- 7.2 Shifting Focus Toward Adhesive Bonding for Composite Materials