|

市場調査レポート

商品コード

1637836

中東・アフリカの接着剤およびシーラント:市場シェア分析、産業動向、成長予測(2025~2030年)MEA Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東・アフリカの接着剤およびシーラント:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

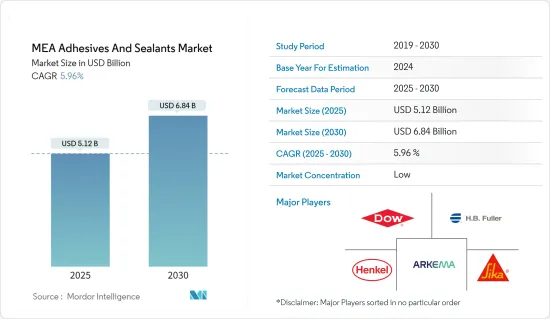

中東・アフリカの接着剤およびシーラント市場規模は2025年に51億2,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.96%で、2030年には68億4,000万米ドルに達すると予測されます。

COVID-19パンデミックは原料供給網を混乱させ、接着剤およびシーラント市場に悪影響を与えました。パンデミック後は、建設、ヘルスケア、包装業界の需要増が接着剤およびシーラント市場を復活させると予想されます。

主なハイライト

- 短期的には、接着剤およびシーラントの需要は、建設業界からの需要増加、ヘルスケアインフラの増加、包装業界における使用量の増加によって大きく牽引されています。

- しかし、化学物質の使用に関する環境問題の高まりが市場成長の妨げになる可能性が高いです。

- バイオベースの接着剤の技術革新と開発、複合材料の接着剤接合へのシフトは、同地域の接着剤およびシーラント市場にチャンスをもたらすと思われます。

- サウジアラビアは同地域最大の接着剤およびシーラント市場で、建設、ヘルスケア、包装などのエンドユーザー産業が消費の主な原動力となっています。

中東・アフリカの接着剤およびシーラント市場動向

包装エンドユーザー産業が市場を独占

- 包装分野は接着剤およびシーラント市場の最大消費者です。包装業界は、飲食品、化粧品、消費財、文房具などのエンドユーザー業界からの強い需要を目の当たりにしています。

- 世界・イノベーション・インデックス(GII)によると、2022年の中東・アフリカの美容・パーソナルケア産業の市場規模は約354億5,000万米ドルでした。

- さらに、人口の増加や高品質な製品に対する需要、都市化、消費者のテクノロジー志向などにより、化粧品や飲食品の需要は伸びると予想されます。したがって、包装業界の需要を煽っています。

- 国際通貨基金(IMF)によると、アラブ首長国連邦の食品とノンアルコール飲料に対する消費者支出は、2023年から2028年の間に99億6,000万米ドル(17.36%増)増加すると予想されています。食品関連支出は2028年には673億米ドルに達すると予想されます。

- カナダ農業・農業食品省によると、アラブ首長国連邦における食品とノンアルコール飲料への1人当たり年間支出額は、2022年には2,337.2米ドルでした。2023年には2,400米ドル以上に上昇すると予想されています。

- さらに、中東とアフリカの高級包装の市場価値は、2025年までに12億米ドル以上に上昇すると予想されています。高級包装とは、高級ブランド品のあらゆる包装を指します。最近の市場開拓には、持続可能な生分解性包装が含まれます。

- したがって、中東・アフリカ地域全体の包装業界のこのような堅調な成長により、接着剤およびシーラント市場の需要も予測期間中に増加すると予想されます。

市場を独占するサウジアラビア

- サウジアラビアは、同地域における接着剤およびシーラントの消費を支配しています。建設活動の成長、自動車生産、ヘルスケアと航空宇宙産業における消費の増加が、同国における接着剤とシーリング剤の消費を促進する主な要因です。

- サウジアラビア政府は、5,000億米ドルの未来型メガシティ「Neom」プロジェクトや、2022年完成予定の紅海プロジェクト第1期のような様々な建設プロジェクトを含んでいます。また、5つの島に3,000室を有する14の高級・超高級ホテルや、2つの内陸リゾート、キディヤ・エンターテインメント・シティ、超高級ウェルネス観光地アマアラ、アル・ウラにあるジャン・ヌーベルのシャルマン・リゾート、住宅省のサカイ・ホームズ、ジェッダ・タワーなども含まれています。このようなプロジェクトは、予測期間中、様々な建設セクターの用途から接着剤需要を牽引すると思われます。

- WHOによると、サウジアラビアのヘルスケア支出は2022年に607億米ドルで、2027年には771億米ドルになると予想されています。

- サウジアラビアは電気自動車に2億2,000万米ドル以上を投資しており、今後数年間で自動車用接着剤の需要を増加させる可能性のある3つの工場を運営しています。例えば、自動車生産台数は2021年の9,800台から2028年には1万2,800台に達すると予想されています。同国の接着剤およびシーラント市場を牽引することが期待されます。

- 統計総局(サウジアラビア)によると、2022年のサウジアラビアの「建築物建設」産業の売上高は約288億7,000万米ドルでした。

- したがって、このような動向はすべて、予測期間にわたって同国の接着剤およびシーラント市場の成長を促進すると予想されます。

中東・アフリカの接着剤およびシーラント産業の概観

中東・アフリカの接着剤およびシーラント市場は断片的な市場です。同市場の主要企業(順不同)には、Arkema、Henkel AG &Co.KGaA、Sika AG、H.B. Fuller Company、Dowなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- サウジアラビアの建設業界からの需要増加

- 包装業界における用途の拡大

- その他の促進要因

- 抑制要因

- 環境問題の高まり

- その他の抑制要因

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 接着剤:樹脂別

- アクリル系

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE・EVA

- その他の樹脂

- 接着剤:技術別

- ホットメルト

- 反応性

- 溶剤系

- UV硬化型

- 水性

- シーラント:樹脂別

- ポリウレタン

- エポキシ

- アクリル

- シリコーン

- その他の樹脂

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 履物および皮革

- ヘルスケア

- 包装

- 木工・建具

- その他エンドユーザー産業

- 地域

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Arkema

- AVERY DENNISON CORPORATION

- Dow

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Huntsman International LLC

- Illinois Tool Works Inc.

- MAPEI S.p.A

- Permoseal(Pty)Ltd

- Sika AG

- The Industrial Group Ltd

第7章 市場機会と今後の動向

- バイオベース接着剤の革新と開発

- 複合材料の接着へのシフト

The MEA Adhesives And Sealants Market size is estimated at USD 5.12 billion in 2025, and is expected to reach USD 6.84 billion by 2030, at a CAGR of 5.96% during the forecast period (2025-2030).

The COVID-19 pandemic disrupted the raw materials supply chain network, negatively affecting the adhesives and sealants market. Post-pandemic, the rising demand for construction, healthcare, and packaging industries is excepted to revive the market for adhesives and sealants.

Key Highlights

- Over the short term, the demand for adhesives and sealants is extensively driven by the growing demand from the construction industry, increasing healthcare infrastructure, and growing usage in the packaging industry.

- However, the market growth is likely to be hindered by the rising environmental concerns regarding the usage of chemicals.

- The innovation and development of bio-based adhesives and shifting focus toward adhesive bonding for composite materials will likely offer opportunities for the adhesives and sealants market in the region.

- Saudi Arabia is the region's largest market for adhesives and sealants, where the end-user industries, such as construction, healthcare, and packaging, majorly drive consumption.

MEA Adhesives and Sealants Market Trends

Packaging End User Industry to Dominate the Market

- The packaging segment is the largest consumer of the adhesives and sealants market. The packaging industry is witnessing strong demand from end-user industries, such as food and beverages, cosmetics, consumer goods, stationery, and others.

- According to the Global Innovation Index (GII), the beauty and personal care industry in Africa and the Middle East in 2022 was worth around USD 35.45 billion.

- Moreover, the demand for cosmetics and food and beverage products is expected to grow due to the growing population and demand for quality products, urbanization, and consumers inclining toward technology. Hence, fueling the demand for the packaging industry.

- According to the International Monetary Fund, overall consumer expenditure on food and non-alcoholic drinks in the United Arab Emirates is expected to rise by USD 9.96 billion (+17.36%) between 2023 and 2028. Food-related spending is expected to reach USD 67.3 billion in 2028.

- According to Agriculture and Agri-Food Canada, the annual per capita expenditure in the United Arab Emirates on food and non-alcoholic beverages was USD 2,337.2 in 2022. It was expected to rise to over USD 2.4 thousand by 2023.

- Additionally, the market value of luxury packaging in the Middle East and Africa is expected to rise to over USD 1.2 billion by 2025. Luxury packaging refers to any packaging for luxury brand items. Recent market developments include sustainable and biodegradable packaging.

- Hence, with such robust growth of the packaging industry across the Middle East and Africa region, the demand in the adhesives and sealants market is also expected to increase during the forecast period.

Saudi Arabia to Dominate the Market

- Saudi Arabia dominates the consumption of adhesives and sealants in the region. Growing construction activities, automotive vehicle production, and increasing consumption in the healthcare and aerospace industries are the key factors driving the consumption of adhesives and sealants in the country.

- The Saudi Arabian government includes various construction projects, like a USD 500 billion futuristic mega-city 'Neom' project, the Red Sea Project - Phase 1, due to be completed in 2022. It also includes 14 luxury and hyper-luxury hotels that may comprise 3,000 rooms across five islands, and two inland resorts, Qiddiya Entertainment City, Amaala - the uber-luxury wellness tourism destination, Jean Nouvel's Sharman resort in Al-Ula, Ministry of Housing's Sakai homes, and Jeddah Tower. Such projects will likely drive the demand for adhesives from various construction sector applications over the forecast period.

- According to the WHO, Saudi Arabia's healthcare spending was USD 60.7 billion in 2022 and is expected to be USD 77.1 billion in 2027.

- Saudi Arabia is investing more than USD 220 million in electric vehicles by operating three potential factories to increase automotive adhesives demand over the coming years. For instance, automotive production is expected to reach 12.8 thousand units by 2028 from 9.8 thousand units in 2021. It is expected to drive the market for adhesives and sealants in the country.

- According to the General Authority for Statistics (Saudi Arabia), in 2022, the revenue of the industry "construction of buildings" in Saudi Arabia was around USD 28.87 billion.

- Hence, all such trends are expected to drive the growth of the adhesives and sealants market in the country over the forecast period.

MEA Adhesives and Sealants Industry Overview

The Middle East and Africa Adhesives and Sealants Market is a fragmented market. Some of the key players in the market (not in any particular order) include Arkema, Henkel AG & Co. KGaA, Sika AG, H.B. Fuller Company, and Dow.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand from the Construction Industry in Saudi Arabia

- 4.1.2 Growing Usage in the Packaging Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Growing Environmental Concerns

- 4.2.2 Other Restrains

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Adhesives by Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 Adhesives by Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured

- 5.2.5 Water-borne

- 5.3 Sealants by Resin

- 5.3.1 Polyurethane

- 5.3.2 Epoxy

- 5.3.3 Acrylic

- 5.3.4 Silicone

- 5.3.5 Other Resins

- 5.4 End-user Industry

- 5.4.1 Aerospace

- 5.4.2 Automotive

- 5.4.3 Building and Construction

- 5.4.4 Footwear and Leather

- 5.4.5 Healthcare

- 5.4.6 Packaging

- 5.4.7 Woodworking and Joinery

- 5.4.8 Other End-user Industries

- 5.5 Geography

- 5.5.1 Saudi Arabia

- 5.5.2 South Africa

- 5.5.3 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema

- 6.4.2 AVERY DENNISON CORPORATION

- 6.4.3 Dow

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 H.B. Fuller Company

- 6.4.6 Huntsman International LLC

- 6.4.7 Illinois Tool Works Inc.

- 6.4.8 MAPEI S.p.A

- 6.4.9 Permoseal (Pty) Ltd

- 6.4.10 Sika AG

- 6.4.11 The Industrial Group Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation and Development of Bio-based Adhesives

- 7.2 Shifting Focus Toward Adhesive Bonding for Composite Materials