|

|

市場調査レポート

商品コード

1687081

タイの接着剤とシーリング剤:市場シェア分析、産業動向、成長予測(2025~2030年)Thailand Adhesives and Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| タイの接着剤とシーリング剤:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

タイの接着剤とシーリング剤市場は予測期間中にCAGR 6.02%を記録する見込み。

この地域におけるCOVID-19の蔓延は、同国における長期の操業停止と原料不足により、同国の自動車セクターに影響を与えました。

主要ハイライト

- 短期的には、同国における包装産業からの需要の増加と複合材料の接着へのシフトが市場を牽引する主要要因です。

- その反面、VOC排出に関する厳しい環境規制とCOVID-19の悪影響が市場の成長を妨げています。

- バイオベースの接着剤に対する需要の増加は、予測期間を通じて市場の成長にさまざまな機会を提供すると期待されます。

タイの接着剤とシーリング剤の市場動向

紙、板紙、包装セグメントが市場を独占

- 包装産業は接着剤の最大のエンドユーザーの一つです。その用途には、袋、タバコ、フィルター、カートンのサイドシームとクロージャー、複合容器とチューブ、使い捨て品、封筒、軟包装、製品、ラベル/サイン/シール、特殊包装、段ボールなどがあります。板紙印刷会社は、書籍用の接着剤を使用しています。

- タイには約2,000の印刷会社があり、そのほとんどが中小規模です。大規模な事業所は全体の1%にも満たないです。数千の事業所が包装産業に携わっています。

- 食品加工部門は軟包装の最大のユーザーであり、総需要の50%以上を占めています。

- 国内で段ボール包装の需要が伸びているのは、主に包装食品と飲食品の需要が継続的に増加しているためです。

- export.govによると、タイの美容・パーソナルケア製品市場は2022年までに80億米ドルに達すると予想されています。export.govによると、タイの美容とパーソナルケア製品市場は、2022年までに80億米ドルに達すると予想されています。美容と化粧品産業から、高価な包装に使用される接着剤の需要のこのような成長は、研究市場を牽引しています。

- 全体として、包装産業からの接着剤の需要の伸びは、予測期間中に中程度から高いと予想されています。

シリコーンセグメントがシーリング剤市場を独占する

- シリコーンは汎用性の高いポリマーです。これらは、ガラス、金属、石などの表面に永久的と一時的な接着を提供するように設計されています。シリコーンシーリング剤の最適な接着にはプライマーが必要だが、プライマーは不要な場合も多いです。

- シリコーンシーリング剤は、広い温度範囲で、摩耗を伴う状況で、気候の変化の下で過酷な環境で効果的に動作します。そのため、耐水性、耐薬品性、耐熱性、柔軟性に優れ、優れた性能を発揮します。

- これらのシーリング剤の主要エンドユーザー産業は、電子・電気、自動車、航空宇宙、建築・建設です。シリコーン接着剤の最も一般的な用途のいくつかは、家の周りの基本的な修理のためです。

- シリコーンは、ケーブルやセンサを所定の位置に密封するために使用され、極端な温度に耐える特性により、これらのシーリング剤の需要は、電子自動車セグメント、建設、電子機器での増加が見込まれています。さらに、建築・建設セグメントでは、シリコーンシーリング剤は極端な気象条件下でも使用できるため、使用量が増加しています。

- このように、上記の要因から、シリコーンシーリング剤の需要は予測期間中に成長すると予想されます。

タイの接着剤とシーリング剤産業概要

タイの接着剤とシーリング剤市場は収益面で統合されています。上位5社の合計シェアは約70%で、市場競争は激しいです。しかし、その他の地元企業の存在が市場に競争環境をもたらしています。主要企業には、Henkel(Thailand)Ltd、Selic Corp Public Company Limited、Covestro AG、Bostik(Arkem Group)、H.B. Fuller(Thailand)などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 包装産業からの需要の増加

- 複合材料の接着へのシフト

- 抑制要因

- VOC排出に関する厳しい環境規制

- COVID-19の影響

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 接着剤

- 技術セグメント

- 水性

- アクリル系

- ポリ酢酸ビニル(PVA)エマルジョン

- エチレンビニルアセテート(EVA)エマルジョン

- その他の水性接着剤

- 溶剤系

- スチレンブタジエンゴム(SBR)

- クロロプレンゴム

- ポリアクリレート(PA)

- その他の溶剤型接着剤

- 反応性

- エポキシ

- シアノアクリレート

- シリコーン

- ポリウレタン

- その他の反応性接着剤

- ホットメルト

- 熱可塑性ポリウレタン

- エチレン酢酸ビニル

- スチレン-ブタジエン共重合体

- その他のホットメルト接着剤

- その他の接着技術

- エンドユーザー産業

- 建築・建設

- 紙・板紙包装

- 輸送

- フットウェアと皮革

- 医療

- 電気・電子

- その他

- 技術セグメント

- シーリング剤

- 製品タイプ

- シリコーン

- ポリウレタン

- アクリル

- その他のシーリング剤製品タイプ

- エンドユーザー産業

- 建築・建設

- 輸送

- 医療

- 電気・電子

- その他

- 製品タイプ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Anabond Limited

- AVERY DENNISON CORPORATION

- Beardow Adams

- Bond Chemicals Company Limited

- Bostik

- CEMEDINE Co. Ltd

- Covestro AG

- Dow

- DUNLOP ADHESIVES(THAILAND)CO. LTD

- H.B. Fuller(Thailand)Co. Ltd

- Henkel(Thailand)Ltd

- Huntsman International LLC

- Jowat(Thailand)Co. Ltd

- Lord Corporation(Parker Hannifin Corp)

- MORESCO(THAILAND)CO. LTD

- Selic Corp. Public Company Limited

- Siam Industry Adhesive Tapes Co. Ltd

- Sika Thailand

- Star Bond(Thailand)Company Limited

- Thai Mitsui Specialty Chemicals Co. Ltd

- TOAGOSEI(THAILAND)CO. LTD

- Wacker Chemie AG

第7章 市場機会と今後の動向

- バイオベース接着剤への需要の高まり

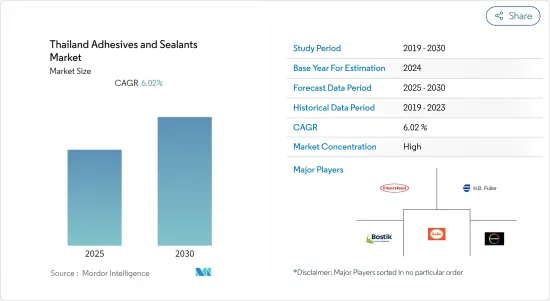

The Thailand Adhesives and Sealants Market is expected to register a CAGR of 6.02% during the forecast period.

The spread of covid-19 in the region impacted the automotive sector of the country due to long lockdowns and the shortage of raw materials in the country.

Key Highlights

- Over the short term, major factors driving the market studied are increasing demand from the packaging industry and shifting focus towards adhesive bonding for composite materials in the country.

- On the flip side, stringent environmental regulations regarding VOC emissions and the negative impact of COVID-19 are hindering the market's growth.

- Increasing demand for bio-based adhesives is expected to offer various opportunities for the market's growth over the forecast period.

Thailand Adhesives and Sealants Market Trends

Paper, Board, and Packaging Segment to Dominate the Market

- The packaging industry is one of the largest end-users of adhesives. Some of the applications include bags, cigarettes and filters, cartons' side seams and closures, composite containers and tubes, disposables, envelopes, flexible packaging, products, labels/signs/decals, specialty packaging, and corrugated boards, among others. Paper board printing houses use adhesives for books.

- There are around 2,000 printing houses in Thailand, most of which are small- to medium-scale. Large-scale establishments account for less than 1% of the total number. Thousands of establishments are involved in the packaging industry.

- The food processing sector is the largest user of flexible packaging, accounting for more than 50% of the total demand.

- The growing demand for corrugated packaging in the country is mainly due to the continued and increasing demand for packaged food and beverages.

- Additionally, there is a considerable increase in the demand for small-scale folding cartons and packaging from the beauty and personal care industry.According to export.gov, Thailand's beauty and personal care products market is expected to reach USD 8.0 billion by 2022. Such growth in the demand for adhesives used in expensive packaging, from beauty and cosmetics industry, is driving the studied market.

- Overall, the demand growth for adhesives from the packaging industry is expected to be moderate to high during the forecast period

Silicone Segment to Dominate the Sealants Market

- Silicones are versatile polymers. These are designed to provide permanent and temporary bonding to surfaces, such as glass, metal, and stone. Primers are required for the optimal adhesion of silicone sealants, although primers are often not necessary.

- The silicone sealants work effectively in harsh environments, across a wide temperature range, in situations involving abrasion, and under climatic changes. Hence, they are water-, chemical-, and temperature-resistant, flexible, and deliver outstanding performance.

- The major end-user industries for these sealants are electronics and electrical, automotive, aerospace, and building and construction. Some of the most common uses of silicone adhesives are for basic repairs around the house.

- The demand for these sealants is expected to increase in the electronic automotive sector, construction, and electronic devices, as silicone is used to seal cables and sensors into place, and due to its property to withstand extreme temperatures. Furthermore, in the building and construction sector, its usage is increasing as silicone sealants can be used even in extreme weather conditions.

- Thus, from the factors mentioned above, the demand for silicone sealants are expected to grow over the forecast period.

Thailand Adhesives and Sealants Industry Overview

Thailand adhesives and sealants market is consolidated in terms of revenue. The top five players account for a combined share of around 70%, making the market highly competitive. However, the presence of other local players is creating a competitive environment in the market. The major companies include Henkel (Thailand) Ltd, Selic Corp Public Company Limited, Covestro AG, Bostik (Arkem Group), and H.B. Fuller (Thailand) Co. Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Packaging Industry

- 4.1.2 Shifting Focus Towards Adhesive Bonding for Composite Materials

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Regarding VOC Emissions

- 4.2.2 COVID-19 Impact

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Adhesives

- 5.1.1 Technology

- 5.1.1.1 Water-borne

- 5.1.1.1.1 Acrylics

- 5.1.1.1.2 Polyvinyl Acetate (PVA) Emulsion

- 5.1.1.1.3 Ethylene Vinyl Acetate (EVA) Emulsion

- 5.1.1.1.4 Other Water-borne Adhesives

- 5.1.1.2 Solvent-borne

- 5.1.1.2.1 Styrene-butadiene Rubber (SBR)

- 5.1.1.2.2 Chloroprene Rubber

- 5.1.1.2.3 Poly Acrylate (PA)

- 5.1.1.2.4 Other Solvent-borne Adhesives

- 5.1.1.3 Reactive

- 5.1.1.3.1 Epoxy

- 5.1.1.3.2 Cyanoacrylate

- 5.1.1.3.3 Silicone

- 5.1.1.3.4 Polyurethane

- 5.1.1.3.5 Other Reactive Adhesives

- 5.1.1.4 Hot-Melt

- 5.1.1.4.1 Thermoplastic Polyurethane

- 5.1.1.4.2 Ethylene Vinyl Acetate

- 5.1.1.4.3 Styrenic-butadiene Copolymers

- 5.1.1.4.4 Other Hot-melt Adhesives

- 5.1.1.5 Other Adhesive Technologies

- 5.1.2 End-user Industry

- 5.1.2.1 Buildings and Construction

- 5.1.2.2 Paper, Board, and Packaging

- 5.1.2.3 Transportation

- 5.1.2.4 Footwear and Leather

- 5.1.2.5 Healthcare

- 5.1.2.6 Electrical and Electronics

- 5.1.2.7 Other End-user Industries

- 5.1.1 Technology

- 5.2 Sealants

- 5.2.1 Product Type

- 5.2.1.1 Silicone

- 5.2.1.2 Polyurethane

- 5.2.1.3 Acrylic

- 5.2.1.4 Other Sealant Product Types

- 5.2.2 End-user Industry

- 5.2.2.1 Buildings and Construction

- 5.2.2.2 Transportation

- 5.2.2.3 Healthcare

- 5.2.2.4 Electrical and Electronics

- 5.2.2.5 Other End-user Industries

- 5.2.1 Product Type

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Anabond Limited

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 Beardow Adams

- 6.4.5 Bond Chemicals Company Limited

- 6.4.6 Bostik

- 6.4.7 CEMEDINE Co. Ltd

- 6.4.8 Covestro AG

- 6.4.9 Dow

- 6.4.10 DUNLOP ADHESIVES (THAILAND) CO. LTD

- 6.4.11 H.B. Fuller (Thailand) Co. Ltd

- 6.4.12 Henkel (Thailand) Ltd

- 6.4.13 Huntsman International LLC

- 6.4.14 Jowat (Thailand) Co. Ltd

- 6.4.15 Lord Corporation (Parker Hannifin Corp)

- 6.4.16 MORESCO (THAILAND) CO. LTD

- 6.4.17 Selic Corp. Public Company Limited

- 6.4.18 Siam Industry Adhesive Tapes Co. Ltd

- 6.4.19 Sika Thailand

- 6.4.20 Star Bond (Thailand) Company Limited

- 6.4.21 Thai Mitsui Specialty Chemicals Co. Ltd

- 6.4.22 TOAGOSEI (THAILAND) CO. LTD

- 6.4.23 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing demand for Bio-based Adhesives