|

市場調査レポート

商品コード

1851468

欧州の接着剤とシーリング剤:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Europe Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の接着剤とシーリング剤:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

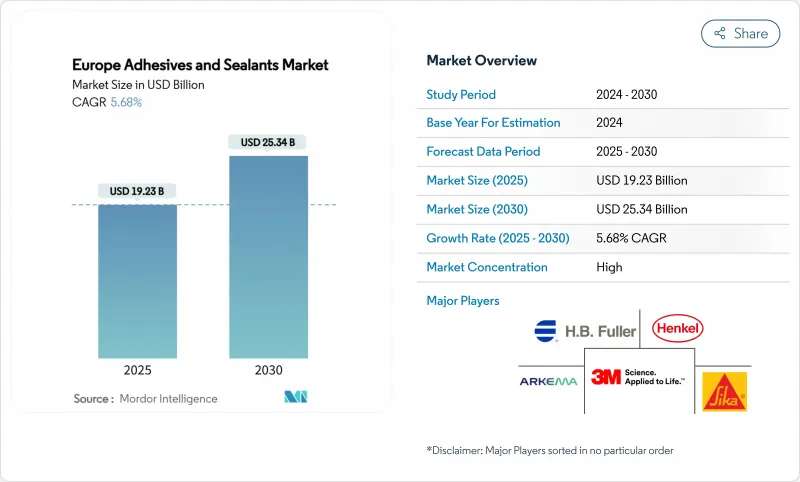

欧州の接着剤とシーリング剤市場規模は2025年に192億3,000万米ドルと推定・予測され、予測期間(2025-2030年)のCAGRは5.68%で、2030年には253億4,000万米ドルに達すると予測されます。

この軌跡は、建設業の回復、自動車の軽量化義務、再生可能エネルギーの拡大を活用しながら、EUの厳しいグリーンディール規制を乗り切る同分野の能力を反映しています。VOC規制が強化されるにつれて水性システムが牽引力を増し、UV硬化型ケミストリーはエレクトロニクスや自動車工場のラインスピードを加速させる。ドイツのインフラ投資は堅調な需要を下支えし、スペインの再生可能エネルギー建設はこの地域で最も急成長している構造用接着ソリューションの買い手となっています。競合の激しさは依然として緩やかで、大手既存企業はバイオベース樹脂にポートフォリオを集中し直し、原料価格の変動と炭素削減コストから利幅を守るために買収主導で能力を拡大しています。

欧州の接着剤とシーリング剤市場動向と洞察

住宅リフォーム需要の高まり

欧州のリフォームは、エネルギー効率の義務化とパンデミック後のライフスタイルの変化により、断熱材、床材、窓の改修への支出が増加し、勢いを増しています。EUのリノベーション・ウェーブは、2030年までに建物の改修率を倍増させることを目標としており、サーマルブリッジを解消する連続接着システムの需要を後押ししています。ドイツの年間500億ユーロ(~584億5,000万米ドル)の改修市場では、ヘンケルのLOCTITE HB S ECOのようなバイオベース製品の採用が増加しています。北欧のサプライヤーは、プレハブのファサード・パネル用の工場塗布型接着剤のパイオニアであり、厳しい室内空気環境基準を満たしながら、現場での迅速な組み立てを可能にしています。このような改修の推進により、欧州の接着剤・シーリング剤市場は2028年まで数量成長を維持するとみられます。

eコマース包装量の急増

小包出荷の増加により、コンバーターはFEICAが発表した紙のリサイクルガイドラインに適合する高速で無溶剤の接着ソリューションの採用を求められています。フレキシブル包装用接着剤は、EUプラスチック戦略の下でリサイクルを簡素化するモノマテリアル設計をサポートしながら、接着強度と脱インキ性のバランスを取る必要があります。ドイツとオランダでは、厳密な粘度管理と素早い硬化を必要とする自動化ラインのアップグレードが進んでいます。こうした動向は、欧州の接着剤・シーラント市場、特に迅速なスループット向けに設計されたホットメルトや水性グレードの市場拡大を支えるものです。

環境問題の高まり

2023年8月発効のREACHジイソシアネート規制は、ポリウレタンシステムの改質または作業員訓練の義務付けを迫り、2026年8月発効のホルムアルデヒド排出規制は、超低排出グレードへのシフトを促します。オクタメチルトリシロキサンを含む247のSVHCが追加され、規制の不確実性が拡大します。持続可能性への投資ニーズは、欧州の化学セクター全体で年間資本支出を70%増加させ、利幅を縮小させるが、バイオベース原料の長期的な技術革新に拍車をかける。

セグメント分析

アクリル樹脂は、汎用性と多様な基材への接着性により、2024年の欧州接着剤・シーラント市場で37.16%の売上シェアを維持。バイオベースのイノベーションを含むその他の樹脂は、炭素削減の義務付けが強化されるにつれて2030年までのCAGRが6.96%拡大すると予測されます。欧州の接着剤とシーリング剤バイオベースグレードの市場規模は、BASFの再生可能なエチルアクリレートがロールアウトし、キシランホットメルトが再利用可能なまま30MPaのラップシアーを実証するにつれて拡大すると予測されます。シアノアクリレートはエレクトロニクスの小型化で支持を集め、ポリウレタン成形メーカーはジイソシアネート・トレーニングをバイパスする湿気硬化システムを追求します。シリコーン樹脂は高温分野で成長し、VAE/EVAはコスト重視のニッチを維持しています。

水性プラットフォームは2024年の売上ベースの43.19%を占め、これは定着した生産ラインとVOCキャップとの整合性を反映しています。しかし、UV硬化システムは、組立工場がインスタント・ボンド加工を求めるため、2030年までのCAGRは6.54%となります。Panacolの黒色UVエポキシは、より厚い層で硬化するためシャドウエリアをなくし、現在ではEVモーターワイヤーの応力緩和ジョイントに指定されています。

反応性ホットメルトは、迅速な硬化と強力な最終接着を併せ持ち、高速パッケージングラインに役立っています。長いオープンタイムが重要な航空宇宙分野では、溶剤を使用する需要が持続しているが、高固形分バージョンは、厳しくなる排ガス規制を満たすのに役立っています。LED-UVランプへの設備アップグレードはエネルギー使用量を削減し、欧州の接着剤・シーラント市場における技術転換をさらに促進します。

欧州の接着剤とシーリング剤レポートは、接着剤樹脂(アクリル、シアノアクリレート、エポキシ、その他)、接着技術(ホットメルト、反応性、溶剤ベース、その他)、シーラント樹脂(ポリウレタン、エポキシ、アクリル、その他)、エンドユーザー産業(航空宇宙、自動車、建築・建設、その他)、地域(ドイツ、英国、フランス、イタリア、スペイン、ロシア、北欧諸国、その他欧州)で区分されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 住宅リフォーム需要の高まり

- eコマース包装量の急増

- 加速する欧州自動車産業の軽量化

- 急成長する風力タービンブレード接着市場

- プレハブ・モジュラー建築の普及

- 市場抑制要因

- 高まる環境問題

- 不安定な原料価格

- ロボット接着剤塗布労働力におけるスキルギャップ

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 接着樹脂別

- アクリル

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE/EVA

- その他の樹脂(シラン変性ポリマー(SMP)、バイオベース樹脂など)

- 接着技術別

- ホットメルト

- 反応性

- 溶剤系

- UV硬化型

- 水性

- シーラント樹脂別

- ポリウレタン

- エポキシ

- アクリル

- シリコーン

- その他の樹脂(ポリサルファイド、SMPハイブリッドなど)

- エンドユーザー業界別

- 航空宇宙

- 自動車

- 建築・建設

- 履物および皮革

- ヘルスケア

- 包装

- 木工および建具

- その他のエンドユーザー産業(再生可能エネルギー、エレクトロニクスとアプライアンスなど)

- 地域別

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- 3M

- Akzo Nobel N.V.

- Arkema

- Avery Dennison Corporation

- BASF

- Dow

- Dymax

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC.

- Jowat

- Mapei S.p.A

- Momentive

- Munzing

- PPG Industries, Inc.

- Sika AG

- Soudal Group

- Wacker Chemie AG