欧州のデータセンター冷却:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1639423

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

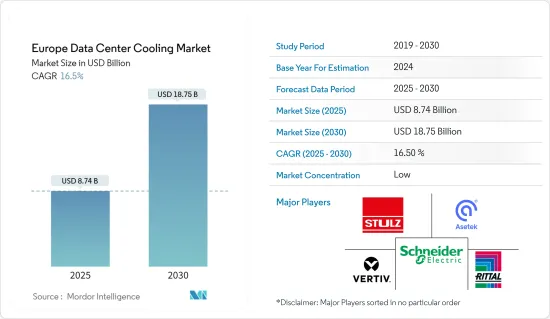

欧州のデータセンター冷却の市場規模は、2025年に87億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは16.5%で、2030年には187億5,000万米ドルに達すると予測されます。

中小企業におけるクラウドコンピューティングの採用拡大、地域のデータセキュリティに関する政府規制、国内企業による投資の拡大などが、同地域におけるデータセンター冷却の需要を促進する主な要因となっています。

主なハイライト

- 冷却技術は通常、データセンターの所在地に基づいて選択されます。企業が定期的にコスト削減を求める中、エネルギー効率の高い冷却方法が従来の冷却方法に代わる潜在的な選択肢として検討されています。また、エッジコンピューティングの採用やIoTデバイスの増加も市場の成長を後押ししています。

- ハンガリー、ギリシャ、ポーランド、トルコなどの新興欧州諸国では、ITインフラの開発により、50MWを超える電力容量を持つハイパースケールデータセンター施設の建設が増加すると予想されます。英国、ドイツ、フランスは欧州全体でデータセンター数が最も多く、市場プレーヤーはこれらの国をターゲットにして新技術に投資することができます。また、市場競争力のある価格で市場要件に対応するため、今後のデータセンター事業者とパートナーシップを結ぶことができ、予測期間中の欧州のデータセンター冷却市場の成長を後押しします。

- 冷却システムは、データセンターの電力消費のほぼ40%を占めています。企業はグリーンデータセンターを設置することで、この問題に取り組もうとしています。情報の保存、管理、配信にグリーン・データセンターを導入する傾向が強まっており、多くのソフトウェア企業がエネルギー消費量と総エネルギー・コストの削減に貢献しています。例えば、AIと組み合わせたImmersion4のようなグリーンテクノロジーは、効率的なエネルギー使用と低カーボンフットプリントを実現することで、データセンターの運用方法をより持続可能なものに変えようとしています。このようなグリーンデータセンターの出現は、この地域における冷却装置の需要を牽引しています。

- データセンター冷却システムは、設置に高額な初期投資を必要とするため、市場が抑制される可能性があります。しかし、多くの現地ベンダーや市場開拓者は、既存のデータセンターを低コストで改造し、新しいユニットの設置コストを削減する革新的なソリューションを開発しています。さらに、二酸化炭素排出量の削減や停電時の冷却問題が市場の成長を妨げる可能性があります。

- COVID-19パンデミックは、新規データセンターの設置や既存データセンターの更新のための施錠、機器不足、サプライチェーンの混乱により市場に影響を与えました。一方、欧州諸国ではデータ量とモバイルデータ利用が大幅に増加しており、欧州全域でデータセンターの設立が促進されると予想されます。これは予測期間中の市場成長を促進すると思われます。また、政府による支援も、予測期間中のデータセンター冷却市場の開拓を後押しすると予測されます。

欧州のデータセンター冷却市場動向

小売セグメントが大きな市場シェアを占める見込み

- 小売分野では、eコマースやオンライン消費におけるユーザー数の増加により、膨大な量のビッグデータが生成され、データストレージ、セキュリティ、レイテンシ低減のニーズが高まると予測されます。これがこの地域の支出とデータセンター数を押し上げています。小売セクターの急速な開発とインダストリー4.0の動向もデータセンターの増加の原因であり、冷却装置の必要性を高めています。

- オンライン・ユーザーの増加により、外資系小売企業はストレージ容量を拡大するために欧州諸国に定期的に投資し、インターネット・トラフィックとデータセンターへの負荷を増大させています。例えば、中国のeコマース大手JD.comは最近、欧州の小売分野への戦略的参入を確認しました。同地域では規制が厳しいため、同地域に投資する外資系企業は、データ保護法に関する移行をスムーズに行うため、データを現地で保管する可能性があります。その結果、データセンター冷却システムの利用が増加し、予測期間中の同地域の市場成長を押し上げると予想されます。

- 特に、eコマース財団によると、欧州のB2C eコマース売上高は、同地域のインターネット普及率の高さにより、約13%拡大し、6,210億米ドルに達する見込みです。ビッグデータ量が増加し、この地域のデータセンターと冷却システムの増加につながる可能性があります。

- Eurostatによると、イタリアとポーランドではeコマース利用者が急増しています。その結果、膨大な量のデータが生成され、ストレージ要件が強化されました。その結果、欧州のデータセンター冷却市場は予測期間中に成長する見込みです。

最大の市場シェアを占める英国

- 英国の企業は新しいデータセンターに積極的に投資しており、これが予測期間中の同地域の市場成長にプラスの影響を与えると予想されます。例えば、欧州のコロケーション・ネットワーキング企業であるInterxionは、ロンドンに3つ目のデータセンターを開設し、消費者向けのキャリアとCDNを拡充しました。この開発により、冷却システムの利用が促進され、市場の成長が促進されると期待されています。

- 同国のファッション小売業H&Mは、ストックホルムに新設するデータセンターに冷却・熱回収システムを組み込む計画です。データセンターから発生する余剰熱は、エネルギー会社Fortum Varmeが市内全域の顧客(全負荷時で2,500戸の近代的住宅アパート)に分配して再利用します。

- 英国は欧州で最もデータセンターの数が多い国です。市場関係者は、これらの国をターゲットにして新技術に投資することができます。また、今後のデータセンター事業者とパートナーシップを結び、市場競争力のある価格で事業者の要求に応えることも可能です。

- グリーン電力、水の再生利用、ゼロウォーター冷却システム、リサイクル、廃棄物管理などのグリーンで再生可能なソリューションは、最も持続可能なデータセンターを構築するために利用されています。英国を含む欧州諸国ではビッグデータ量が増加しており、低遅延・大容量のデータセンターへのニーズが高まることで、冷却システムの利用率が高まると予想されます。サイエンス・ダイレクト社によると、データセンターのエネルギー使用量は予測期間中、世界の電力供給の2.13%を占める可能性があります。

- 企業は各業界で定期的に運用コストの削減を試みており、国内のデータセンター冷却システムに使用されるAI技術を増やしています。例えば、シーメンスはAIベースの熱最適化を導入し、データセンター冷却システムを強化するためにVigilant AI製品を活用しています。

欧州のデータセンター冷却産業の概要

欧州のデータセンター冷却市場は細分化されており、技術によってもたらされるメリットや、データセンターに効率化規制を課すことによる政府からの支援が、データセンター冷却市場の成長を後押しすると期待されています。主な市場プレイヤーとしては、IBM Corporation、富士通株式会社、株式会社日立製作所、ヒューレット・パッカード・エンタープライズ、シュナイダーエレクトリックSEなどが挙げられます。市場の浸透は、既存市場における大手企業の強い存在感とともに拡大しています。技術革新への注目が高まるにつれ、新技術への需要が高まり、それがさらなる開発のための投資を促進しています。

- 2024年5月リタールは、複数のハイパースケールデータセンター事業者と共同で、モジュール式冷却システムを開発しました。このソリューションは、直接水冷により1MWを超える冷却能力を誇る。AIアプリケーションの高電力密度に対応するよう特別に調整されています。

- 2024年1月世界なハイパースケールおよびエンタープライズ顧客向けに、持続可能で革新的、かつ適応性のある規模のデータセンターおよびビルド・トゥ・スケールソリューションを提供する技術インフラ企業であるアラインド・データ・センターズは、人工知能、機械学習、スーパーコンピューターを含む次世代アプリケーションおよびハイパフォーマンス・コンピューティングの高密度計算要件をサポートするために構築された特許出願中のソリューションであるDeltaFlow液冷技術を発表しました。DeltaFlowは、アラインドのExpandOnDemand機能を拡張し、変化するコンピューティング環境をサポートするためにシームレスに拡張し、ピボットする柔軟性を顧客に提供します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要(対象範囲:データセンター冷却に関連する現在の地域動向の詳細な分析を含みます。)

- 冷却に関する主要コストの考察

- DCクーリングに注目したDC運用に関連する主要コスト諸経費の分析

- データセンター冷却における主な技術革新と発展

- データセンターで採用されている主なエネルギー効率化手法

第5章 市場力学

- 市場促進要因(エネルギー消費重視の高まり、グリーンソリューションへの移行などの主要要因を、今後5~7年間の相対的影響に基づいてマッピング)

- 市場力学(規制のダイナミックな性質、顧客ニーズの進化などの主要因を、今後5~7年間の相対的影響に基づいてマッピング)

- 市場機会

- 封じ込め付きレイズドフロアと封じ込めなしレイズドフロアの比較

- 産業エコシステム分析

第6章 地域別データセンターのフットプリントの現状分析

- データセンターのIT負荷容量と面積フットプリントの地域分析(2017年~2030年の期間)

- 欧州地域における確立されたDC市場と新興DCホットスポットの地域分析(主要な確立されたDC市場と新興DC市場にハイライトを当てることで網羅性を持たせます)

- DC冷却に関する規制枠組みの地域分析

第7章 データセンター冷却市場のセグメンテーション

- 冷却技術別(主要動向、2022~2029年の市場規模推計・予測、将来展望)

- エアベース冷却

- CRAH

- チラーとエコノマイザー

- 冷却塔(直接冷却、間接冷却、2段階冷却をカバー)

- その他

- 液体ベース冷却

- 液浸冷却

- 直接チップ冷却

- リアドア式熱交換器

- エアベース冷却

- 業界別

- IT&テレコム

- 小売・消費財

- ヘルスケア

- メディア&エンターテインメント

- 連邦政府機関

- その他のエンドユーザー

- 国別

- 英国

- ドイツ

- ロシア

- デンマーク

- ノルウェー

- オランダ

- スペイン

- ポーランド

- スイス

- オーストリア

- ベルギー

- フランス

- イタリア

- アイルランド

- スウェーデン

第8章 競合情勢

- 企業プロファイル

- Vertiv Group Corp.

- Stulz GmbH

- Schneider Electric SE

- Rittal GmbH & Co. KG

- Asetek A/S

- Alfa Laval AB

- Iceotope Technologies Limited

- Green Revolution Cooling Inc.

- Chilldyne Inc.

- Airedale International Air Conditioning Ltd

第9章 投資分析

第10章 市場機会と今後の動向

目次

The Europe Data Center Cooling Market size is estimated at USD 8.74 billion in 2025, and is expected to reach USD 18.75 billion by 2030, at a CAGR of 16.5% during the forecast period (2025-2030).

The growing adoption of cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data center cooling in the region.

Key Highlights

- Cooling technologies are usually selected based on the data centers' geographical location. As companies regularly seek to mitigate costs, energy-efficient cooling methods are being considered the potential alternatives to traditional cooling methods. The market's growth is also fueled by edge computing adoption and the increase in IoT devices.

- Developments in IT Infrastructure in emerging European countries such as Hungary, Greece, Poland, and Turkey are expected to increase the construction of hyperscale data center facilities with over 50 MW power capacity. The United Kingdom, Germany, and France had the highest number of data centers across Europe, and market players can target these countries to invest in their new technologies. Also, they can form partnerships with upcoming data center organizations to cater to market requirements at a competitive price, aiding the growth of the European data center cooling market over the forecast period.

- The cooling systems are responsible for almost 40% of the data center power consumption. Companies are trying to tackle this issue by setting up green data centers. The growing trends toward deploying green data centers for storing, managing, and distributing information have helped many software companies reduce energy consumption and total energy costs. For example, green technologies, such as Immersion4 in combination with AI, are changing how data centers operate to make them more sustainable with efficient energy usage and low carbon footprint. Such green data centers' emergence drives the demand for cooling units in the region.

- Data center cooling systems require a high initial investment to set up, which could restrain the market. However, many local vendors and market players are developing innovative solutions by modifying the existing data centers at a low cost to reduce the cost of setting up a new unit. Additionally, reduced carbon emission and cooling issues during power outages could hamper the growth of the market.

- The COVID-19 pandemic impacted the market owing to lockdowns, shortage of devices, and supply chain disruptions to set up new data centers and update the existing data centers. On the other hand, there is a massive rise in data volume and mobile data usage in European countries, which is anticipated to boost the setup of data centers across Europe. This will propel the market growth over the forecast period. Also, government support is projected to boost the development of the data center cooling market over the forecast period.

Europe Data Center Cooling Market Trends

The Retail Segment is Expected to Hold a Significant Market Share

- In the retail segment, the increasing number of users in e-commerce and online spending is creating an enormous volume of Big Data, which is expected to propel the need for data storage, security, and reduced latency. This boosts the region's expenditure and the number of data centers. Rapid development in the retail sector and Industry 4.0 trends are also responsible for the rise of data centers, enhancing the need for cooling devices.

- Due to the increasing number of online users, foreign retail companies regularly invest in European countries to expand their storage capacity, increasing internet traffic and the load on data centers. For instance, JD.com, a Chinese e-commerce giant, recently confirmed a strategic entry into the European retail sphere. Due to stringent regulations in the region, foreign companies investing in the area may store their data locally for smooth transitions regarding the data protection law. As a result, the usage of data center cooling systems is expected to increase, thereby boosting the market growth in the region over the forecast period.

- Notably, according to the E-commerce Foundation, the European B2C e-commerce turnover is expected to expand by approximately 13% to reach USD 621 billion due to the high internet penetration in the region. It may increase the Big Data volume, leading to more data centers and cooling systems in the area.

- According to Eurostat, Italy and Poland witnessed tremendous growth in e-commerce users. It led to the generation of a vast amount of data, thereby strengthening storage requirements. As a result, the European data center cooling market is expected to grow over the forecast period.

The United Kingdom Accounts For the Largest Market Share

- Companies in the UK are rigorously investing in new data centers, and this is expected to positively impact the market growth in the region over the forecast period. For instance, Interxion, a European colocation and networking company, commenced its third data center in London, expanding carriers and CDNs for consumers. This development is expected to propel cooling system utilization and foster market growth.

- H&M, a fashion retailer in the country, plans to integrate a cooling and heat recovery system in its new data center in Stockholm. The excess heat generated from the data center is reused by Fortum Varme, an energy company, by distributing it to customers (2,500 modern residential apartments at full load) throughout the city.

- The UK recorded the highest number of data centers across Europe. Market players can target these countries to invest in their new technologies. Also, they can form partnerships with upcoming data center organizations to cater to their requirements at a competitive price, which may aid the growth of the European data center cooling market over the forecast period.

- Green and renewable solutions, such as green electricity, water reclamation, zero water cooling systems, recycling, and waste management, are being used to build the most sustainable data centers. Growth in Big Data volume across European countries, including the United Kingdom, is expected to increase the need for low-latency and high-capacity data centers, thereby boosting cooling system utilization. According to Science Direct, data center energy use might account for 2.13% of worldwide electricity supply over the forecast period.

- Companies are regularly trying to reduce their operational cost across their verticals, increasing the AI technology used in data center cooling systems in the country. For instance, Siemens introduced AI-based thermal optimization, wherein the company utilizes Vigilant AI products to enhance cooling systems in data centers.

Europe Data Center Cooling Industry Overview

The European data center cooling market is fragmented as the benefits offered by the technology and support from the government by imposing efficiency regulations on data centers are expected to help the growth of the data center cooling market. Some major market players are IBM Corporation, Fujitsu Ltd, Hitachi Ltd, Hewlett-Packard Enterprise, and Schneider Electric SE. Market penetration is growing with a strong presence of major players in established markets. With the increasing focus on innovation, the demand for new technologies is growing, which, in turn, is driving investments for further developments.

- May 2024: Rittal, in collaboration with multiple hyperscale data center operators, developed a modular cooling system. This solution boasts a cooling capacity exceeding 1 MW, achieved through direct water cooling. It is specifically tailored to cater to the high-power densities of AI applications.

- January 2024: Aligned Data Centers, the technology infrastructure company providing sustainable, innovative, and adaptive scale data centers and build-to-scale solutions for global hyperscale and enterprise customers, introduced its DeltaFlow liquid cooling technology, a patent-pending solution built to support the high-density compute requirements of next-generation applications and high-performance computing, including artificial intelligence, machine learning, and supercomputers. DeltaFlow extended Aligned's ExpandOnDemand capabilities, providing customers the flexibility to seamlessly scale and pivot to support shifting computing environments.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview (Coverage: A detailed analysis of the current regional trends related to Data Center Cooling are included in this section)

- 4.2 Key cost considerations for Cooling

- 4.2.1 Analysis of the key cost overheads related to DC operations with an eye on DC Cooling

- 4.2.2 Key innovations and developments in Data Center Cooling

- 4.2.3 Key energy efficiency practices adopted in Data Centers

5 MARKET DYNAMICS

- 5.1 Market Drivers (Key factors such as the increased emphasis on energy consumption, move towards green solutions are mapped based on their relative impact over the next 5-7 years)

- 5.2 Market Challenges (Key factors such as the dynamic nature of regulations, evolving customer needs are mapped based on their relative impact over the next 5-7 years)

- 5.3 Market Opportunities

- 5.4 Comparison of raised floor with containment & raised floor without commitment

- 5.5 Industry Ecosystem Analysis

6 ANALYSIS OF THE CURRENT REGIONAL DATA CENTER FOOTPRINT

- 6.1 Regional Analysis of IT Load Capacity & Area Footprint of Data Centers (for the period of 2017-2030)

- 6.2 Regional Analysis of the Established DC Markets and Emerging DC Hotspots in Europe region (we will include coverage by highlighting major established and emerging DC markets)

- 6.3 Regional Analysis of Regulatory Framework On DC Cooling

7 DATA CENTER COOLING MARKET SEGMENTATION

- 7.1 By Cooling Technology (Key trends, market size estimates & projections for the period of 2022-2029 and future outlook)

- 7.1.1 Air-based Cooling

- 7.1.1.1 CRAH

- 7.1.1.2 Chiller and Economizer

- 7.1.1.3 Cooling Tower (covers direct, indirect & two-stage cooling)

- 7.1.1.4 Others

- 7.1.2 Liquid-based Cooling

- 7.1.2.1 Immersion Cooling

- 7.1.2.2 Direct-to-Chip Cooling

- 7.1.2.3 Rear-Door Heat Exchanger

- 7.1.1 Air-based Cooling

- 7.2 By End-user Vertical

- 7.2.1 IT & Telecom

- 7.2.2 Retail & Consumer Goods

- 7.2.3 Healthcare

- 7.2.4 Media & Entertainment

- 7.2.5 Federal & Institutional agencies

- 7.2.6 Other End Users

- 7.3 By Country

- 7.3.1 United Kingdom

- 7.3.2 Germany

- 7.3.3 Russia

- 7.3.4 Denmark

- 7.3.5 Norway

- 7.3.6 Netherlands

- 7.3.7 Spain

- 7.3.8 Poland

- 7.3.9 Switzerland

- 7.3.10 Austria

- 7.3.11 Belgium

- 7.3.12 France

- 7.3.13 Italy

- 7.3.14 Ireland

- 7.3.15 Sweden

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Vertiv Group Corp.

- 8.1.2 Stulz GmbH

- 8.1.3 Schneider Electric SE

- 8.1.4 Rittal GmbH & Co. KG

- 8.1.5 Asetek A/S

- 8.1.6 Alfa Laval AB

- 8.1.7 Iceotope Technologies Limited

- 8.1.8 Green Revolution Cooling Inc.

- 8.1.9 Chilldyne Inc.

- 8.1.10 Airedale International Air Conditioning Ltd

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日