|

市場調査レポート

商品コード

1639361

北米のIoTセキュリティ-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)North America IoT Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のIoTセキュリティ-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

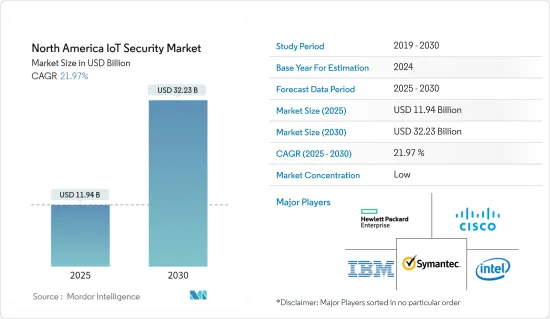

北米のIoTセキュリティ市場規模は、2025年に119億4,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは21.97%で、2030年には322億3,000万米ドルに達すると予測されます。

主要ハイライト

- 新たなビジネスモデルと用途は、デバイスコストの削減と相まって、IoTの採用を促進し、その結果、コネクテッドマシン、ウェアラブル、自動車、メーター、民生用電子機器製品などのコネクテッドデバイスの数が増加しています。

- 消費者向けIoTデバイスへの攻撃は蔓延しており、製造業や類似の産業における混乱の可能性が脅威をより深刻なものにしています。米国とカナダの様々なエンドユーザー産業では、過去数年間にかなりのセキュリティ攻撃に直面しています。IoTセキュリティは、企業、消費者、規制当局にとって重要な注目セグメントとなりつつあります。このような注目の高まりを受けて、世界中でIoTベースのソリューションを提供している企業は、これらのソリューションのセキュリティ面に多額の投資を行っています。

- 例えば、2022年10月、クラウド用途のモニタリングセキュリティプラットフォームを提供するDatadog, Inc.は、Cloud Security Managementの一般提供を宣言しました。この製品は、クラウドセキュリティポスチャ・マネジメント(CSPM)、クラウドワークロードセキュリティ(CWS)、アラート、インシデント管理、レポーティングの機能を単一のプラットフォームに統合したもので、DevOpsチームとセキュリティチームが設定ミスを特定し、脅威を検出し、クラウドネイティブ用途を保護できるようにします。

- さらに、コネクテッドデバイスへの依存度の高まりにより、コネクテッドデバイスの安全性を維持する必要性が生じています。この大きな成長は、コネクテッドエコシステムの展開に産業が注力するようになったことや、3GPPセルラーIoT技術の標準化によってもたらされると予想されます。

- インターネットに接続されるデバイスの増加に伴い、サイバー世界では新たな脅威や攻撃の発生や出現が大幅に増加すると予想されます。IoTデバイスは、データ盗難、なりすまし、フィッシング攻撃、DDoS攻撃(サービス拒否攻撃)など、さまざまなネットワーク攻撃に対して特に脆弱です。これらは、ランサムウェア攻撃やその他の深刻なデータ漏えいなど、さまざまなサイバーセキュリティ関連の脅威につながる可能性があり、企業は復旧に多大な費用と労力を費やすことになります。

- しかし、デバイス間の複雑化は、ユビキタス法の欠如と相まって、予測期間を通じて市場全体の成長を制限する可能性のある主要な懸念事項である可能性があります。

- COVID-19が始まって以来、IoT攻撃が増加しているため、世界各国はいくつかの予防策を実施しています。地域社会が自宅待機を求められ、学校が閉鎖される中、複数の組織が従業員の自宅勤務を認める方法を見出しました。その結果、ビデオ・コミュニケーションプラットフォームの導入が増加しました。さらに、COVID-19以降の期間には、特に主要な市場参入企業によるコスト効率の高いクラウドベースとハイブリッドのさまざまなソリューションの導入により、市場は大きな成長機会を目の当たりにすると予想されます。

北米のIoTセキュリティ市場動向

データ漏洩件数の増加が市場を牽引すると予測

- インターネットに接続されるデバイスの増加に伴い、サイバー世界では新たな脅威や攻撃の発生・出現が増加すると予想されています。このことは、過去数年間における北米地域のさまざまなエンドユーザー業種におけるデータ侵害の増加からも明らかです。このような攻撃は、ビジネスシステムや個人を直接標的とするものであり、莫大な金銭的・個人的損失につながる可能性があります。そのため、データ侵害の影響を受けやすい消費者向けデバイスに対するIoTセキュリティの必要性が高まっている

- さらに、医療、製造業、BFSI、自動車など、さまざまなエンドユーザー産業におけるデータ漏洩の増加が、サイバー攻撃から接続デバイスを保護するIoTセキュリティソリューションの必要性を高めています。例えば、Identity Theft Resource CenterによるITRC 2022 Annual Data Breach Reportによると、米国における2022年のデータ漏洩件数は1802件でした。米国におけるデータ漏洩件数は、2005年の157件から2022年には1802件へと大幅に増加しています。

- さらに、クラウドサービスは、IoTの需要に起因する高い採用率を経験しています。このように、さまざまな業種でクラウドシステムの利用が増加しているため、データ漏洩に対するシステムの脆弱性が高まっています。多くのプロバイダーが複数のソリューションを提供しているため、統一されたセキュリティプラットフォームに対するニーズが高まっています。IoTセキュリティは、デバイスと通信、データストレージ、ライフサイクルソリューションに展開できます。

- さらに、サイバー攻撃から企業を保護するための政府の取り組みが増加していることから、市場はさらに成長すると予想されています。例えば、バイデン政権は2023年7月、インターネット接続機器に関連する無数のセキュリティリスクから米国人を守るため、モノのインターネット(IoT)サイバーセキュリティ表示プログラムを開始しました。このプログラム「米国サイバートラストマーク」は、米国人がサイバー攻撃に対する強力なサイバーセキュリティ保護を含むインターネット接続機器を確実に購入できるようにすることを目的としています。

米国が市場を独占する見込み

- 米米のIoTセキュリティ市場の成長の主要重要要因は、先進技術の採用率の高さ、サイバー攻撃の増加、同国における接続デバイス数の増加です。同国は、IoT展開において支配的な地域の1つです。その他の要因としては、同地域におけるデジタル化とIoTセキュリティ支出の増加が挙げられます。

- さらに、この地域には、Symantec Corporation、IBM Corporation、FireEye Inc.、Palo Alto Networks Inc.など、重要なIoTセキュリティベンダーが存在します。ベンダー各社は製品イノベーションを強化することで、製品ポートフォリオと市場での存在感を高めています。例えば、2022年3月、ネットワークファイアウォールのプロバイダーであるPalo Alto Networksは、Amazon Web Servicesと提携し、新しいPalo Alto Networks Cloud NGFW for AWSを発表したことを明らかにしました。

- また、2022年5月には、エレクトロニクス用途のあらゆるセグメントで顧客にサービスを提供する世界の半導体プロバイダーであるSTMicroelectronicsが、ST認定パートナーであるMicrosoftとの協業の詳細を明らかにしました。その目的は、新たなInternet-of-Things用途のセキュリティを強化することです。STは、超低消費電力のSTM32U5マイコンとMicrosoft Azure RTOS &IoT Middlewareを組み合わせるとともに、特に組込みシステム向けに、Arm Trusted Firmware-M(TF-M)セキュアサービスの認定セキュア実装を行います。

- さらに、米国ではサイバー脅威が増加しています。Identity Theft Resource Centerによると、同国の平均侵害件数は過去数年間でわずかに増加しています。2022年10月、バイデン-ハリス政権は米国のサイバー防衛の改善に大きな焦点を当て、国家のサイバーセキュリティを強化し保護するための積極的な行動を取るための包括的なアプローチを構築しました。

- GSMA Intelligenceによると、北米における産業用と消費者用のモノのインターネット接続総数は、2025年末までに約54億に増加すると予測されています。2019年、北米のIoT接続総数は28億接続に達しました。同地域内の産業用と民生用モノのインターネット接続の総数がこのように大幅に増加することで、市場全体の成長機会が大きく促進されると予測されます。

北米のIoTセキュリティ産業概要

北米のIoTセキュリティ市場の競合情勢は、この地域全体に多数の地域参入企業が存在するため、セグメント化が特徴となっています。これらの市場参入企業は、さまざまな産業に対応する革新的なソリューションを導入する動きを強めています。さらに、同市場では、市場での存在感を高めることを目的とした提携や買収が顕著に増加しています。

2022年12月、サイバーセキュリティソリューション・プロバイダーのCheck Point Software Technologies Ltd.(Check Point Software Technologies Ltd.)は、Check Point Quantumサイバーセキュリティプラットフォームの機能強化版であるCheck Point Quantum Titanを発表しました。Quantum Titanは、ディープラーニングと人工知能(AI)のパワーを活用した3つのソフトウェアブレードを組み込んだもので、先進的DNS(Domain Name System Exploits)やフィッシング攻撃に対する先進的脅威防御を実現するほか、自律的なIoTセキュリティも記載しています。チェック・ポイントのQuantum Titanは、IoTデバイスの検出機能と、IoTデバイスを保護するためのゼロトラスト脅威防御プロファイルの自動適用機能を備えています。

Palo Alto Networksは2022年12月、医療機器向けに設計された包括的なゼロ・トラストセキュリティソリューションであるMedical IoT Securityを発表しました。このソリューションにより、医療組織は新しいコネクテッド技術を安全かつ迅速に導入・管理できるようになります。サイバーセキュリティに対するゼロトラストのアプローチは、すべてのユーザーとデバイスを継続的に検証することに重点を置いており、これにより組織のセキュリティフレームワーク内の暗黙の信頼を排除します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- データ漏えいの増加

- スマートシティの出現

- 市場抑制要因

- デバイス間の複雑化とユビキタス法制の欠如

第6章 市場セグメンテーション

- セキュリティタイプ

- ネットワークセキュリティ

- エンドポイントセキュリティ

- ソリューション

- ソフトウェア

- サービス

- エンドユーザー産業

- 自動車

- 医療

- 政府機関

- 製造業

- エネルギー・電力

- 小売業

- BFSI

- その他

- 地域

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Symantec Corporation

- IBM Corporation

- Check Point Software Technologies Ltd.

- Intel Corporation

- Hewlett Packard Enterprise Company

- Cisco Systems Inc.

- Fortinet Inc.

- Trustwave Holdings

- AT&T Inc.

- Palo Alto Networks Inc.

第8章 投資分析

第9章 市場機会と今後の動向

The North America IoT Security Market size is estimated at USD 11.94 billion in 2025, and is expected to reach USD 32.23 billion by 2030, at a CAGR of 21.97% during the forecast period (2025-2030).

Key Highlights

- The emerging business models and applications, coupled with the reducing device costs, have been instrumental in driving the adoption of IoT, consequently, the number of connected devices, such as connected machines, wearables, cars, meters, and consumer electronics.

- Attacks on consumer IoT devices are prevalent, and the overall possibility of disruption in manufacturing and similar industries makes the threat more serious. Various end-user industries in the United States and Canada have faced considerable security attacks in various industries in the past few years. IoT security is becoming a significant focus area for businesses, consumers, and regulators. Following such increasing prominence, enterprises that are offering IoT-based solutions worldwide are investing heavily in the security aspect of these solutions.

- For instance, in October 2022, Datadog, Inc., the monitoring and security platform for cloud applications, declared the general availability of Cloud Security Management. This product brings together capabilities from Cloud Security Posture Management (CSPM), Cloud Workload Security (CWS), alerting, incident management, and reporting in a single platform to enable DevOps and Security teams to identify misconfigurations, detect threats, and secure cloud-native applications.

- Moreover, the increasing dependency on connected devices is creating the need to keep the connected devices secure. This significant growth is anticipated to be driven by the growing industry focus on deploying a connected ecosystem as well as the standardization of 3GPP cellular IoT technologies.

- With the growing number of devices connected to the Internet, the cyber world is anticipated to witness a significant rise in the occurrence and emergence of new threats and attacks. IoT devices are particularly vulnerable to various network attacks, such as data theft, spoofing, phishing attacks, and DDoS attacks (denial of service attacks). These can lead to various cybersecurity-related threats like ransomware attacks and other serious data breaches that can take businesses a lot of money and effort to recover from.

- However, the growing complexity among devices, coupled with the lack of ubiquitous legislation, could be a major matter of concern that can limit the overall market's growth throughout the forecast period.

- Since the beginning of COVID-19, there has been an increase in IoT attacks, and hence, countries worldwide have implemented several preventive measures. With communities being asked to stay at home and schools being closed, multiple organizations have found a way to allow their employees to work from their homes. This has resulted in a rise in the adoption of video communication platforms. Moreover, during the post-COVID-19 period, the market is expected to witness significant growth opportunities, especially due to the introduction of various cost-effective cloud-based and hybrid solutions by the leading major market participants.

North America IoT Security Market Trends

Increasing Number of Data Breaches is Anticipated to Drive the Market

- With the increase in the number of devices connected to the Internet, the cyber world is expected to witness a rise in the occurrence and emergence of new threats and attacks. This is evident by the growth in data breaches across the North America region in various end-user verticals over the past few years. These attacks, which directly target business systems and individuals, may potentially lead to enormous financial and personal losses. Thus fueling the need for IoT security for consumer devices that are highly susceptible to data breaches.

- Moreover, the growth in data breaches across the region in various end-user industries, such as healthcare, manufacturing, BFSI, automotive, etc., is driving the need for IoT security solutions to protect their connected devices from cyberattacks. For instance, according to the ITRC 2022 Annual Data Breach Report by Identity Theft Resource Center, the number of data compromises in the United States was 1802 cases in 2022. The number of data compromises in the United States significantly increased from 157 cases in 2005 to 1802 cases in 2022.

- Further, cloud services are experiencing high adoption rates owing to the demand for IoT. This increasing use of cloud systems across various verticals has increased the vulnerabilities of these systems to data breaches. With many providers offering multiple solutions, the need for a uniform security platform is rising. IoT security can be deployed for devices and communication, data storage, and lifecycle solutions.

- Additionally, the market is further expected to grow due to the increasing government initiatives to protect businesses from cyberattacks. For instance, in July 2023, The Biden administration launched an Internet of Things (IoT) cybersecurity labeling program to protect Americans against the myriad security risks associated with internet-connected devices. The program, "U.S. Cyber Trust Mark," aims to help Americans ensure they are buying internet-connected devices that include strong cybersecurity protections against cyberattacks.

United States is Expected to Dominate the Market

- The major crucial factors for the growth of the IoT security market in the United States are the high adoption of advanced technologies, increasing cyberattacks, and a growing number of connected devices in the country. The country is one of the dominant regions for IoT deployment. Other factors include the growth in digitalization and IoT security spending in the region.

- Moreover, the region houses significant IoT Security vendors, including Symantec Corporation, IBM Corporation, FireEye Inc., and Palo Alto Networks Inc., among others. The vendors are strengthening their product portfolio and market presence by boosting their product innovation. For instance, in March 2022, Palo Alto Networks, a provider of network firewalls, declared that it has teamed up with Amazon Web Services to unveil the new Palo Alto Networks Cloud NGFW for AWS, a managed Next-Generation Firewall (NGFW) service designed to simplify securing AWS deployments, allowing organizations to speed their pace of innovation while remaining highly secure.

- Also, in May 2022, STMicroelectronics, a global semiconductor provider serving customers across the spectrum of electronics applications, revealed the details of its collaboration with Microsoft, an ST-authorized partner. The aim was to strengthen the security of emerging Internet-of-things applications. ST is combining its ultra-low-power STM32U5 microcontrollers with Microsoft Azure RTOS & IoT Middleware as well as a certified secure implementation of the Arm Trusted Firmware -M (TF-M) secure services, especially for embedded systems.

- Moreover, the United States is experiencing an increasing number of cyber threats. According to the Identity Theft Resource Center, the average number of breaches in the country has increased marginally over the past few years. In October 2022, The Biden-Harris Administration brought a significant focus to improving the United States' cyber defenses, building a comprehensive approach to take aggressive action to strengthen and safeguard the nation's cybersecurity.

- As per GSMA Intelligence, the total number of industrial and consumer Internet of Things connections in North America is forecast to grow to around 5.4 billion by the end of the year 2025. In 2019, the total number of IoT connections in North America amounted to 2.8 billion connections. Such a significant rise in the overall count of the industrial and consumer Internet of Things connections within the region is expected to propel the market's overall growth opportunities significantly.

North America IoT Security Industry Overview

The competitive landscape of the North American IoT Security Market is characterized by fragmentation due to the presence of numerous regional players across the region. These market participants are increasingly introducing innovative solutions to cater to various industries. Furthermore, the market is experiencing a notable increase in collaborations and acquisitions aimed at enhancing its market presence.

In December 2022, Check Point Software Technologies Ltd., a cybersecurity solutions provider, unveiled Check Point Quantum Titan, an enhancement to the Check Point Quantum cyber security platform. The Quantum Titan release incorporates three software blades that harness the power of deep learning and artificial intelligence (AI) to offer advanced threat prevention against sophisticated domain name system exploits (DNS) and phishing attacks, as well as autonomous IoT security. With Check Point Quantum Titan, the platform now includes IoT device discovery and the automatic application of zero-trust threat prevention profiles to safeguard IoT devices.

In December 2022, Palo Alto Networks introduced Medical IoT Security, a comprehensive Zero Trust security solution designed for medical devices. This solution enables healthcare organizations to securely and rapidly deploy and manage new connected technologies. The zero-trust approach to cybersecurity focuses on continuously verifying every user and device, thereby eliminating implicit trust within the organization's security framework.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of Covid-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Number of Data Breaches

- 5.1.2 Emergence of Smart Cities

- 5.2 Market Restraints

- 5.2.1 Growing Complexity among Devices, coupled with the Lack of Ubiquitous Legislation

6 MARKET SEGMENTATION

- 6.1 Type of Security

- 6.1.1 Network Security

- 6.1.2 End-point Security

- 6.2 Solution

- 6.2.1 Software

- 6.2.2 Services

- 6.3 End-user Industry

- 6.3.1 Automotive

- 6.3.2 Healthcare

- 6.3.3 Government

- 6.3.4 Manufacturing

- 6.3.5 Energy and Power

- 6.3.6 Retail

- 6.3.7 BFSI

- 6.3.8 Others End-user Industries

- 6.4 Geography

- 6.4.1 United States

- 6.4.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Symantec Corporation

- 7.1.2 IBM Corporation

- 7.1.3 Check Point Software Technologies Ltd.

- 7.1.4 Intel Corporation

- 7.1.5 Hewlett Packard Enterprise Company

- 7.1.6 Cisco Systems Inc.

- 7.1.7 Fortinet Inc.

- 7.1.8 Trustwave Holdings

- 7.1.9 AT&T Inc.

- 7.1.10 Palo Alto Networks Inc.