|

市場調査レポート

商品コード

1637922

アジア太平洋地域の医療機器包装:市場シェア分析、産業動向&統計、成長予測(2025年~2030年)Asia-Pacific Medical Devices Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の医療機器包装:市場シェア分析、産業動向&統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

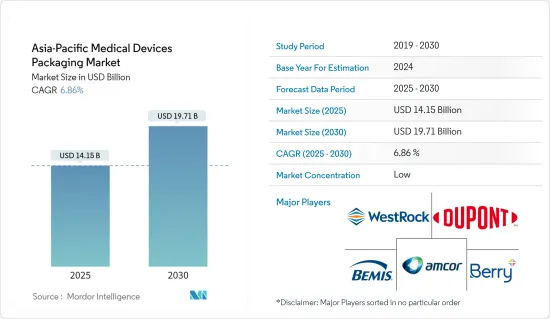

アジア太平洋地域の医療機器包装の市場規模は2025年に141億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.86%で、2030年には197億1,000万米ドルに達すると予測されます。

官民のヘルスケア支出増による医療機器需要の増加と規制強化が、アジア太平洋地域の医療機器包装市場を牽引しています。

主なハイライト

- 効果的な医療機器包装は、流通や保存期間中の機器の保護に極めて重要な役割を果たします。医療製品の開発プロセスでは、包装材料と包装タイプの設計に細心の注意を払うことが最も重要です。適切な包装は、医療機器がエンドユーザーの手元に届くまで、無菌状態を保ち、安全で機能的であることを保証します。これには、様々な環境条件やマテリアルハンドリングプロセスに耐えられる素材を選択することと、ユーザーフレンドリーで規制基準に準拠した包装を設計することが含まれます。

- 医療機器包装は、無菌包装と非無菌包装に大別されます。無菌包装は、物理的損傷に対する保護に加え、器具が汚染から保護されなければならない包装のタイプです。無菌包装は規格に適合し、製造から手術室までのサプライチェーン全体を通して無菌性を保証しなければならないです。

- CTスキャナー、X線装置、手術用ロボット、心臓血管装置、超音波装置など、一部の医療機器は繊細で高価であるため、適切な流通のために適切な包装が必要となります。改ざん防止や小児用耐性を持たせるため、これらの機器の包装にはさらなる技術革新が進んでいます。この業界は、国によって異なる政府の規制の影響を大きく受けやすいです。

- 国連によると、アジア太平洋には世界で最も人口の多い国がいくつかあり、世界の総人口の約60%を占めています。同地域は、医療機器の製造・調達の主要拠点のひとつです。オリンパス、ソニックヘルスケア、ニプロなどの主要な医療機器メーカーが存在することが、この地域における医療機器包装ソリューションの需要を促進しています。

アジア太平洋地域の医療機器包装市場の動向

プラスチックセグメントが大きな市場シェアを占める見込み

- プラスチックは、特に医療産業において、単回使用と多回使用の両方のシナリオに対応し、無数の目的を果たします。医療用プラスチックと呼ばれるこれらの材料は、ヘルスケアにおける重要な機器、消耗品、用具を製造するためのコスト効率の高い手段を提供します。ヘルスケア分野は、様々な医療用プラスチックに大きく依存しており、新しいポリマーや材料の研究を先導しています。このような継続的な研究は、進化し続けるヘルスケア産業の需要に対応できる高度な医療ソリューションの開発にとって極めて重要です。

- 医療用プラスチックはその耐久性とリサイクル性から、注射器やチューブのような使い切りタイプで主流を占めています。しかし、その有用性はそれだけにとどまらず、義肢装具などの用途にも広がっています。汎用性、持続可能性、コスト効率に優れたプラスチックは、現在も医療現場の要であり、革新的な用途が次々と生まれています。これらの技術革新は、医療機器の機能性を高めるだけでなく、患者の転帰を改善し、ヘルスケア施設の運営効率を向上させています。

- 医療機器包装には、防湿、遮光、チャイルドプルーフなどの管理が必要です。医療機器におけるポリマーの成長は、医療機器包装業界に大きな変革をもたらしました。プラスチック製医療機器は、柔軟性が高く手頃な価格といった利点から、ガラス、セラミック、金属といった他の素材に着実に取って代わりつつあります。

- プラスチックは寿命が長く、幅広い用途に使用でき、プラスチック製品を作るための材料費も安いため、製造コストを抑えることができます。プラスチックは腐食や飛散に強く、医療用プラスチックは繰り返しの滅菌にも対応できるように設計できます。これらの利点により、医療機器メーカーは諸経費を大幅に削減することができ、低コストでサービスを提供することで、事業と患者の双方に利益をもたらすことができます。

- PET、HDPE、PP、ビニルは、医療機器包装に使用される最も一般的なプラスチックです。医療機器パッケージング・プロバイダーは、需要の高まりと厳しい規制により、持続可能なパッケージング・ソリューション開発への投資を増やしています。アジア太平洋で事業を展開する主要な包装業者も、医療機器向けの持続可能な包装ソリューションの需要増に対応するため、同様のアプローチを採用すると予想されます。

- インド・ブランド・エクイティ財団によると、インドの医療機器輸出は2022-23年に33億9,000万米ドルと評価され、2025年までに100億米ドルに急増すると予測されています。こうした輸出を強化するため、保健家族福祉省(MOHFW)と中央医薬品標準管理機関(CDSCO)は戦略的な取り組みを展開しています。こうした取り組みは、医療機器セクターにおける先進パッケージング・ソリューションの需要を押し上げる構えです。

中国が最大市場シェアを占める可能性が高い

- 中国は世界有数の医療機器メーカーです。伝統的に、中国の医療機器市場は、ローエンドの消耗品や機械治療機器で知られてきました。ハイエンドの医療機器の調達は外国からの輸入に大きく依存していました。しかし、最近では「メイド・イン・チャイナ」などの政府の後押しにより、高価値でリスクの高い医療機器は国産化される傾向にあります。

- ヘルスケア・セクターの基盤拡大とともに、中国の医療機器市場は大きなペースで開拓されています。中国におけるハイエンド医療機器の需要増加の原動力のひとつは、人口の高齢化です。

- 国連開発計画(UNDP)は、中国を世界で最も急速に高齢化が進んでいる国のひとつに挙げています。2023年には、65歳以上の高齢者が2億1,680万人となり、人口の15.4%を占める。ITAの予測によると、2025年までに中国の60歳以上の人口は3億人を突破するといいます。さらに、医療保険の適用範囲が拡大したことで、神経系や心臓血管系のインプラント需要が高まっており、特にこれらの分野は高価な消耗品の輸入に大きく依存しています。

- また、同国はさまざまな地域にわたって、国内で製造された医療機器の大部分を輸出しており、これが同国の医療機器包装の需要を高めています。

- 医療機器の輸出量と国内消費量の両方が増加することが予想されるため、予測期間中、同国の医療機器包装市場は促進されることになります。プラスチックの使用がしばしば批判されるヘルスケア分野は、使い捨ての医療用プラスチック製品から発生する大量の廃棄物という顕著な課題に直面しています。

- 地域のメーカーは医療廃棄物を抑制する方法を積極的に模索しており、よりリサイクル可能な使い捨てアイテムの設計に注力しています。注射針や薬剤のような物品を二次汚染の可能性から保護する必要があることから、医療用プラスチックが包装の有力な選択肢として浮上してきました。プラスチック製パウチは密封できるため、使い捨ての物品を保護し、使用前の滅菌の必要性をなくすことができます。さらに、プラスチックボトルや容器は、紫外線、湿気、その他の有害要素から処方箋を保護するのに長けています。

アジア太平洋地域の医療機器包装産業の概要

アジア太平洋地域の医療機器包装市場は細分化されており、多くの企業が地域全体で様々な医療機器包装製品を製造しています。同時に、業界では価格引き下げ圧力による包装メーカーの合併・買収・統合が起きています。この地域で事業を展開している主要企業には、Amcor PLC、Bemis Manufacturing Company、Berry Global Inc.、三菱ケミカルホールディングスなどがあります。

- 2024年2月、韓国に本社を置くSKケミカルズは、循環型リサイクルイニシアチブの立ち上げにより、医療用包装市場に参入する計画を発表しました。MD&Mは米国で開催される医療機器・製造分野の著名な展示会であり、医療機器の設計・製造における新技術や新製品を発表する場となっています。MD&MにおいてSKケミカルズは、PPEや医療機器パッケージなどの医療必需品によく見られる従来のポリエステルを展示するだけでなく、循環型リサイクルの原則を取り入れた「スカイペットCR」や「エコトリアCR」などの最新素材も紹介します。

- 2024年5月、オリバーヘルスケア・パッケージングはマレーシアのジョホール州に最初の製造工場の建設を開始し、アジア太平洋における大幅な拡大を示しました。この施設は同社にとってアジア最大となる予定で、この地域へのコミットメントを強調しています。主に革新的なフレキシブル・パッケージングに焦点を当てたこの工場は、マレーシアの急成長する医薬品・医療機器部門を強化することを目的としています。2024年末の完成が見込まれる同工場は、同地域のサプライチェーンにおいて極めて重要な役割を果たすことになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 産業政策

第5章 市場力学

- 市場促進要因

- 医療機器市場の成長

- より良い包装に対する人々の意識の高まり

- 市場抑制要因

- コスト削減に対する市場の圧力

- COVID-19の市場への影響評価

第6章 市場セグメンテーション

- 包装タイプ別

- プラスチック容器

- ガラス容器

- 蓋

- パウチ

- ラップフィルム

- 紙缶

- その他の包装タイプ

- 地域別

- 中国

- 日本

- インド

- オーストラリア

第7章 競合情勢

- 企業プロファイル

- Amcor PLC

- Bemis Manufacturing Company

- Berry Global Inc.

- DuPont de Nemours Inc.

- WestRock Company

- SDG Pharma

- Sonoco Products Company

- Mitsubishi Chemical Holdings

- 3M

- Technipaq Inc.

- Steripack Group

- CCL Industries Inc.

第8章 投資分析

第9章 市場の将来

The Asia-Pacific Medical Devices Packaging Market size is estimated at USD 14.15 billion in 2025, and is expected to reach USD 19.71 billion by 2030, at a CAGR of 6.86% during the forecast period (2025-2030).

The growing demand for medical devices due to increased healthcare expenditure in the public and private sectors and the stricter regulations are driving the Asia-Pacific medical devices packaging market.

Key Highlights

- Effective medical device packaging plays a pivotal role in safeguarding devices during distribution and their shelf life. Meticulous attention to the design of both the packaging material and type is paramount in the medical product development process. Proper packaging ensures that medical devices remain sterile, secure, and functional until they reach the end user. This involves selecting materials that can withstand various environmental conditions and handling processes, as well as designing packaging that is user-friendly and compliant with regulatory standards.

- The packaging for medical devices is broadly categorized into sterile packaging and non-sterile packaging. Sterile packaging is the type of packaging wherein the devices must also protect against contamination, in addition to protection against physical damage. Sterilization packaging must conform to standards and must guarantee sterility throughout the whole supply chain from production through to the operation room.

- Some medical devices, such as CT scanners, X-ray machines, surgical robots, cardiovascular equipment, and ultrasound devices, are sensitive and costly, thereby requiring appropriate packaging for proper distribution. More innovations are coming up in the packaging of these devices to make them tamper-evident and child-resistant. The industry is highly susceptible to government regulations, which vary with country.

- According to the United Nations, Asia-Pacific is home to some of the world's most populous countries and approximately 60% of the world's total population. The region is among the prime locations for the manufacturing and sourcing of medical devices. The presence of some of the key medical device manufacturers, such as Olympus, Sonic Healthcare, and Nipro, among others, is driving the demand for medical device packaging solutions in the region.

Asia-Pacific Medical Devices Packaging Market Trends

Plastic Segment Expected to Hold Significant Market Share

- Plastics, especially in the medical industry, serve a myriad of purposes, catering to both single-use and multi-use scenarios. Referred to as medical plastics, these materials offer a cost-effective avenue for producing crucial equipment, supplies, and tools in healthcare. The healthcare sector heavily leans on various medical-grade plastics, spearheading research into novel polymers and materials. This ongoing research is crucial for developing advanced medical solutions that can meet the ever-evolving demands of the healthcare industry.

- Given its durability and recyclability, medical plastics dominate in single-use items like syringes and tubes. Yet, their utility extends far beyond, encompassing applications such as prosthetics. Plastic, being versatile, sustainable, and cost-efficient, remains a cornerstone of the medical landscape, witnessing ongoing innovative applications. These innovations are not only enhancing the functionality of medical devices but also improving patient outcomes and operational efficiencies within healthcare facilities.

- Medical device packaging requires control over moisture, light barriers, and childproofing. The growth of polymers in medical devices has brought a considerable transformation to the medical device packaging industry. Plastic medical devices are steadily replacing other materials, such as glass, ceramics, and metals, owing to benefits such as greater flexibility and affordable price.

- Plastic has a long life and can be used for a wide range of applications, and the cost of the material used to make plastic products is less, thereby reducing the cost of manufacturing. Plastics are resistant to corrosion and shattering, and medical-grade plastics can be designed to handle repeated sterilizations. All these advantages allow the medical device manufacturers to significantly reduce their overhead costs, benefiting both the operations and the patients by offering services at a lower cost.

- PET, HDPE, PP, and vinyl are the most common plastics used in packaging medical devices. Medical device packaging providers are increasing their investments in developing sustainable packaging solutions due to the growing demand and stringent regulations. A similar approach is expected to be adopted by major packaging providers operating in Asia-Pacific to fulfill the growing demand for sustainable packaging solutions for medical devices.

- India's medical device exports, valued at USD 3.39 billion in 2022-23, are projected to surge to USD 10 billion by 2025, as per the India Brand Equity Foundation. To bolster these exports, the Ministry of Health and Family Welfare (MOHFW) and the Central Drugs Standard Control Organisation (CDSCO) have rolled out strategic initiatives. These efforts are poised to drive up the demand for advanced packaging solutions within the medical devices sector.

China is Likely to Occupy Maximum Market Share

- China is among the leading medical device manufacturers in the world. Traditionally, the Chinese medical devices market has been known for low-end consumables and mechanotherapy devices. The country was largely dependent on foreign imports to procure high-end medical devices. However, there has been a shift toward more domestically made high-value, high-risk devices in the country lately, owing to government-backed initiatives such as 'Made in China.'

- Along with the expanding base of the healthcare sector, China's medical devices market is developing at a significant pace. One of the driving factors for the increase in demand for high-end medical devices in China is the aging population.

- The United Nations Development Programme (UNDP) highlights China as one of the world's fastest-aging nations. In 2023, the country boasted 216.8 million individuals aged 65 or older, constituting 15.4% of its population. Projections from the ITA suggest that by 2025, China's population aged 60 and above will surpass 300 million. Moreover, the broadened medical insurance coverage has bolstered the demand for neurology and cardiovascular implants, especially as these sectors heavily rely on imported high-value consumables.

- The country also exports a major share of its locally manufactured devices across various regions, which is augmenting the demand for medical devices packaging in the country.

- Anticipated growth in both export volume and domestic consumption of medical devices is set to propel the country's medical device packaging market during the forecast period. The healthcare sector, often criticized for its plastic usage, faces a notable challenge with the substantial waste generated by single-use medical plastic items.

- Regional manufacturers are actively seeking ways to curb medical waste, focusing on designing single-use items that are more recyclable. Given the imperative to shield items like needles and medications from potential cross-contamination, medical plastics have emerged as the go-to choice for packaging. Plastic pouches can be hermetically sealed, offering protection to single-use items and negating the need for pre-use sterilization. Moreover, plastic bottles and containers are adept at safeguarding prescriptions from UV rays, humidity, and other damaging elements.

Asia-Pacific Medical Devices Packaging Industry Overview

The Asia-Pacific medical devices packaging market is fragmented, with a large number of players manufacturing varieties of packaging products for medical devices across the region. At the same time, the industry is witnessing mergers and acquisitions/consolidation of packaging players due to pressure on companies to reduce prices. Some of the major players operating in the region include Amcor PLC, Bemis Manufacturing Company, Berry Global Inc., and Mitsubishi Chemical Holdings.

- In February 2024, SK Chemicals, headquartered in South Korea, announced plans to enter the medical packaging market with the launch of a circular recycling initiative. MD&M, a prominent US exhibition for the medical device and manufacturing sector, serves as a platform for unveiling new technologies and products in medical device design and production. At MD&M, SK Chemicals will not only exhibit its traditional polyester, commonly found in medical essentials like PPE and medical device packaging, but will also showcase its latest materials, including SKYPET CR and ECOTRIA CR, which incorporate circular recycling principles.

- In May 2024, Oliver Healthcare Packaging began constructing its inaugural manufacturing plant in Johor, Malaysia, marking a significant expansion in the Asia-Pacific. This facility, set to become the company's largest in Asia, underscores its commitment to the region. Primarily focusing on innovative, flexible packaging, the plant aims to bolster Malaysia's burgeoning pharmaceutical and medical device sector. With an anticipated completion by the end of 2024, the facility is poised to play a pivotal role in the region's supply chain.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Industry Policies

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Medical Devices Market

- 5.1.2 Increasing Awareness Among the People About Better Packaging

- 5.2 Market Restraints

- 5.2.1 Market Pressure to Reduce Costs

- 5.3 Assessment of COVID-19 Impact on the Market

6 MARKET SEGMENTATION

- 6.1 By Packaging Type

- 6.1.1 Plastic Containers

- 6.1.2 Glass Containers

- 6.1.3 Lids

- 6.1.4 Pouches

- 6.1.5 Wrap Films

- 6.1.6 Paper Cans

- 6.1.7 Other Packaging Types

- 6.2 By Geography

- 6.2.1 China

- 6.2.2 Japan

- 6.2.3 India

- 6.2.4 Australia

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 Bemis Manufacturing Company

- 7.1.3 Berry Global Inc.

- 7.1.4 DuPont de Nemours Inc.

- 7.1.5 WestRock Company

- 7.1.6 SDG Pharma

- 7.1.7 Sonoco Products Company

- 7.1.8 Mitsubishi Chemical Holdings

- 7.1.9 3M

- 7.1.10 Technipaq Inc.

- 7.1.11 Steripack Group

- 7.1.12 CCL Industries Inc.