中東・アフリカの医療機器パッケージング:市場シェア分析、産業動向、成長予測(2025~2030年)

MEA Medical Devices Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 101 Pages

- 納期

- 2~3営業日

- 商品コード

- 1637880

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

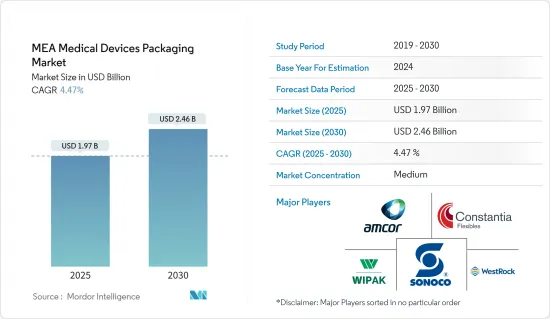

中東・アフリカの医療機器パッケージングの市場規模は2025年に19億7,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは4.47%で、2030年には24億6,000万米ドルに達すると予測されています。

医療機器需要の急増が保護包装の必要性を高めています。中東とアフリカは、過去数十年の間にヘルスケアシステムの開発と人々の健康成果の改善においてかなりの進歩を遂げました。

主なハイライト

- 中東・アフリカのヘルスケア業界では、無菌医療包装の需要が増加しています。プラスチック、紙、板紙には、リサイクル可能、軽量、耐久性などいくつかの利点があります。医療機器パッケージングは、医療機器の安全性と有効性を守る上で不可欠な役割を果たしています。包装は、輸送や保管中の危害、汚染、操作から機器を保護し、ヘルスケアプロバイダーや患者に重要なデータを伝えます。

- パウチ包装は医療機器の効果的な包装方法であることが実証されています。パウチは軽量で持ち運びやすく、保管に便利なだけでなく、製品の無菌性、保護、安全性の維持にも貢献します。医療用パウチ包装の利点を最大化するために、デザイン、素材、バリア保護を特定の用途に合わせることができます。さらに、小型から中型の医療機器、器具、消耗品の使用単位包装における用途の増加は、パウチ包装の需要増加を促進すると思われます。パウチ包装の需要は、二次包装における診断テストパック、プレフィルド吸入器、外科用・歯科用トレーの使用増加の影響を受けると予測されています。

- 糖尿病は、世界的にもこの地域でも死亡原因の第7位を占めています。さらに、糖尿病は身体障害の重大な原因であり、失明、心血管疾患、下肢切断、腎不全のリスク増大と関連しています。国際糖尿病連合によると、アフリカ、中東、北アフリカでは、2021年から2045年の間に糖尿病患者数が世界で最も増加する(134%)。これらの医薬品は汚染のリスクが高いため、こうした事件が無菌包装の需要を高め、無菌医療機器パッケージングの需要を押し上げています。

- さらに、サウジアラビア政府はヘルスケア分野の開拓に多額の投資を行っており、これがヘルスケア市場を押し上げると期待されています。政府は医療サービスの質の向上、先進医療技術の導入、病院やヘルスケアセンターの増加に注力しています。サウジアラビアのFDAは、国内の医薬品や医療機器の登録、評価、承認を担当しています。これは最終的に対象市場の成長に影響を与えます。

- しかし、サウジアラビアの標準化・計量・品質機関(SASO)は、サウジアラビアにおけるプラスチック製品に関する新たな規制を発表しました。プラスチックはOXO生分解性でなければならず、国内に入るすべてのプラスチック製品は、商業用または工業用で使用するためにSASOに登録され、認証を受けなければならないです。そのため、政府の様々な法律が同国における医療機器用プラスチック包装の開発を妨げると予想されます。

中東・アフリカの医療機器パッケージング市場の動向

滅菌パッケージングの需要増加

- 滅菌は医療機器産業における重要な処理工程です。そのため、滅菌パッケージング製品やバリアシステムを使用することが業界でますます重要になってきています。無菌医療包装は再利用不可能であり、微生物感染に対するバリアとして機能します。プラスチックや紙を使用することで、軽量、リサイクル性、耐久性などの利点があります。

- 医療機器業界では、輸送中の湿気などの環境要因から製品を保護する包装のニーズが高まっています。さらに、効率を高める先進パッケージング機器など、パッケージング技術への投資の高まりが、医療機器や医薬品の完全性と無菌性を保証するパッケージングソリューションへの需要を促進しています。

- パンデミックは、無菌および抗菌パッケージングの選択肢を生み出し、その創出を促進しています。トランスミッションを防止するための無菌医療用包装に対する需要の急増は、パンデミックによって急がれました。感染症やウイルスの増加により、汚染を避けるための無菌医療包装のニーズが高まり、市場成長に寄与しています。

- 患者の安全性を最優先するため、外科手術や医療器具の包装に対する政府の厳しい規制が、このセグメントの無菌包装の需要を押し上げています。無菌包装は外科手術や医療器具にとって、患者を保護し、外科手術中の細菌や病気のトランスミッションを防ぐために極めて重要です。National Institute of Health(国立衛生研究所)のデータによると、2023年には医療機器に関連した感染症が170万件発生しており、これが医療機器向け無菌包装の需要を世界的に高めています。

- 政府はヘルスケアサービスの質の向上に注力しており、ヘルスケア分野への投資を増やす戦略的な計画を立てています。医薬品関連製品や医療機器に対する需要の増加により、無菌・無菌包装に対するニーズが高まっています。これらのパッケージング・ソリューションは、汚染リスクの低減に役立つため、機器の安全な保管と輸送に不可欠です。この地域はヘルスケア分野への投資を続けており、予測される時間枠の中で医療機器パッケージングの需要を煽っています。

- さらに、国連社会経済局によると、この地域の国々は高齢者人口の増加を経験します。サウジアラビアでは2050年までに65歳以上の人口の割合が15.1%に達し、チュニジアとアラブ首長国連邦では2050年までに高齢者人口が21.4%と28%を占めるようになります。このような高齢者人口の増加は医療の成長を促進し、最終的には市場成長に影響を与えると思われます。

サウジアラビアは医療機器生産の増加で著しい成長が見込まれる

- サウジアラビア政府は、石油・ガス収入への依存を減らし、製造業や観光業など、収入を生み出す他のセクターの開発を計画しています。サウジ・ビジョン2030は、国内の他のセクターを発展させるという同じビジョンを持って開始されました。サウジ・ビジョン2030のイニシアチブのひとつには、国内の患者ケアを向上させるためのヘルスケア部門の強化が含まれています。

- さらに政府は、原材料、設備、スペアパーツに対する関税免除や最大10年間の所得税の繰延べ、低水道・電気料金などの追加優遇措置を提供することで、現地化に注力しています。また、国内でヘルスケア製品を流通・販売する機会を提供することで、サプライチェーンの強化も図っています。

- サウジアラビア投資省(MISA)は、高い投資ポテンシャルを持つ分野として、医薬品と医療機器の2つを挙げています。サウジアラビア投資省(MISA)は、国内の医療機器の約90%が輸入品であると指摘。現地生産を支援することで、外国企業への依存度を下げることができます。このことは、同国の医療機器パッケージメーカーの成長に大きな影響を与えると予想されます。

- 医療機器メーカーは、サウジアラビア政府が提供する機会を活用するため、同国での事業展開を模索しています。例えば2024年、ジョンソン・エンド・ジョンソン社の技術会社であるJ&J MedTech KSAが、サウジアラビアでの直接事業開始を発表しました。同社は医療機器や手術機器を提供しており、同国での直接事業はヘルスケア分野の発展を支援する「ビジョン2030」に貢献するものです。

- 国際貿易局によると、サウジアラビアは湾岸協力会議(GCC)諸国の医療費の約60%を占めています。2023年には、ヘルスケアと社会開発への支出が前年比で約504億米ドルを占める。さらに、サウジアラビアの医療機器市場は年率10%で成長しています。サウジアラビアの人々の間で医療に対する関心が高まり、ヘルスケアサービスの消費が増加していることから、医療機器セクターの力強い成長が医療機器パッケージング市場の開拓を後押しすると予想されます。

中東・アフリカの医療機器パッケージング産業の概要

中東・アフリカの医療機器パッケージング市場は半固体化しています。同市場の主要企業には、Amcor Group GmbH、Sonoco Products Company、DS Smith PLC、Wipak Group、Constantia Flexibles GmbH、WestRock Companyなどがあります。各プレイヤーは、この地域でのプレゼンスと製品ポートフォリオを拡大し、市場機会を有利にすることに注力しています。

- 2023年11月-Amcor Group GmbHは新しい単一素材ポリエチレン(PE)ラミネートを発売しました。この新しい単一素材ラミネートは、様々な包装形態に対応できるように設計されています。一般的にドレープや保護材、カテーテルや注射システム、チューブなどに使用される3D熱可塑性プラスチックパッケージの非リサイクル蓋に取って代わることができます。また、創傷ケア材料や手袋の2Dパウチ用途にも適しています。

- 2023年6月-Rose Plastic Medical Packaging GmbHは、デリケートな歯科インプラント用のプラスチックチューブ容器、DentalImplantPackの発売を発表しました。歯科インプラント用の新しいプラスチックチューブ容器は、手術中の取り扱いが容易で、輸送中の安全性も確保されているため、製品が無傷のまま顧客の手元に届きます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 地政学的シナリオが市場に与える影響

第5章 市場力学

- 市場促進要因

- 医療機器用滅菌パッケージングの需要増加

- ヘルスケアセクター開発への多額の投資

- 市場抑制要因

- プラスチック使用に対する政府の規制

第6章 市場セグメンテーション

- 材料別

- プラスチック

- 紙・板紙

- その他の原材料

- 製品タイプ別

- パウチ・袋

- トレイ

- 箱

- クラムシェル

- その他の製品タイプ

- 用途別

- 滅菌パッケージング

- 非滅菌パッケージング

- 国別

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- その他中東とアフリカ

第7章 競合情勢

- 企業プロファイル

- Amcor Group GmbH

- Sonoco Products Company

- DS Smith PLC

- Wipak Group

- Constantia Flexibles GmbH

- WestRock Company

- Rose Plastic Medical Packaging GmbH

- Amber Packaging Industries LLC

- Intermat Flexible Packaging(Pak Holding AS)

- Ispak Esnek Ambalaj Sanayi AS

第8章 投資分析

第9章 市場の将来

目次

The MEA Medical Devices Packaging Market size is estimated at USD 1.97 billion in 2025, and is expected to reach USD 2.46 billion by 2030, at a CAGR of 4.47% during the forecast period (2025-2030).

The surge in demand for medical devices drives the need for protective packaging. The Middle East and Africa made considerable progress in developing healthcare systems and the improvement of health outcomes among their populations over the past few decades.

Key Highlights

- The Middle East and Africa healthcare industry is seeing increased demand for sterile medical packaging. Plastics, paper, and paperboard have several advantages, including recyclability, low weight, and durability. Medical device packaging plays an essential role in safeguarding the safety and effectiveness of medical devices. Packaging protects devices from harm, contamination, and manipulation during transport and storage and conveys critical data to healthcare providers and patients.

- Pouch packaging has been demonstrated to be an effective method of packaging medical devices. Not only are pouches lightweight, portable, and convenient to store, but they also contribute to product sterility, protection, and safety maintenance. The design, materials, and barrier protection can be tailored to the specific application to maximize the benefits of medical pouch packaging. Furthermore, rising applications in the unit-of-use packaging of small to medium-sized medical devices, appliances, and supplies will likely drive increased demand for pouches. Pouch packaging demand is projected to be influenced by the growing usage of diagnostic test packs, prefilled inhalers, and surgical and dental trays in secondary packaging.

- Diabetes has been identified as the seventh leading cause of death globally and in the region. In addition, diabetes is a significant cause of disability and is associated with an increased risk of blindness, cardiovascular disease, lower limb amputation, and kidney failure. According to the International Diabetes Federation, Africa, the Middle East, and North Africa will have the highest increase in the number of people with diabetes worldwide between 2021 and 2045 (134%). These incidents have increased the demand for sterile packaging as these medicines have a high risk of contamination, boosting the demand for sterile medical device packaging.

- Additionally, the Saudi government is investing heavily in developing the healthcare sector, which is expected to boost the healthcare market. The government is focusing on improving the quality of healthcare services, implementing advanced healthcare technologies, and increasing the number of hospitals and healthcare centers. The Saudi FDA is responsible for registering, evaluating, and approving drugs and medical devices in the country. This will ultimately impact on the growth of the target market.

- However, the Saudi Standardization, Metrology, and Quality Organization (SASO) issued new regulations for plastic items in Saudi Arabia. The plastic must be OXO-biodegradable, and all plastic goods entering the nation must be registered with and certified by SASO for use in commercial or industrial settings. So, it is anticipated that various government laws will impede the development of medical device plastic packaging in the country.

MEA Medical Devices Packaging Market Trends

Increasing Demand for Sterile Packaging

- Sterilization is an important processing step in the medical device industry. Therefore, using sterile packaging products or barrier systems is becoming increasingly important in the industry. Sterile medical packaging is non-reusable and acts as a barrier against microbial infection. Using plastic and paper offers lightweight, recyclability, and durability advantages.

- The medical device industry is experiencing a growing need for packaging to safeguard products from environmental factors like moisture while in transit. Additionally, the rising investments in packaging technologies, including advanced equipment to enhance efficiency, are driving the demand for packaging solutions that guarantee the integrity and sterility of medical devices and pharmaceuticals.

- The pandemic has created avenues and advanced the creation of sterile and anti-microbial packaging options. The surge in demand for sterile medical packaging to prevent transmission was hastened by the pandemic. The rise in infectious diseases and viruses has resulted in a higher need for sterile medical packaging to avoid contamination, contributing to market growth.

- Stringent government regulations for surgical and medical appliance packaging to prioritize patient safety boost the demand for sterile packaging for this segment. Sterile packaging is crucial for surgical and medical appliances to protect patients and prevent transmission of germs or diseases during surgical procedures. According to data from the National Institute of Health, 1.7 million cases were caused by medical device-associated infection in 2023, which enhanced the demand for sterile packaging for medical appliances globally.

- The government focuses on improving the quality of healthcare services and has strategic plans to increase investment in the healthcare sector. The increasing demand for medicine-related products and medical devices has created a greater need for aseptic and sterile packaging. These packaging solutions are essential for the safe storage and transit of devices, as they help to reduce the risk of contamination. The region continues to invest in the healthcare sector, thus fueling the demand for medical device packaging in the projected timeframe.

- Additionally, according to the United Nations Department of Social and Economic Affairs, countries in the region will experience growth in the elderly population. The percentage of the population 65+ in Saudi Arabia will account for 15.1% by 2050, and in Tunisia and the United Arab Emirates, the elderly population will account for 21.4% and 28% by 2050. Such growth of the elderly population will propel the growth of medical care, eventually impacting the market growth.

Saudi Arabia is Expected to Register Significant Growth with the Increasing Production of Medical Devices

- The government in the country is planning to reduce the reliance on oil and gas revenues and develop other sectors to generate income, such as manufacturing and tourism. The Saudi Vision 2030 was initiated with the same vision of developing other sectors in the country. One of the initiatives of Saudi Vision 2030 includes enhancing the healthcare sector to advance patient care in the country.

- Additionally, the government focuses on localization by offering additional incentives such as customs duty exemption and deferred income tax for up to 10 years on raw materials, equipment, spare parts, and low water and electricity rates. It also offers an enhanced supply chain with opportunities to distribute and sell healthcare products within the country.

- The Ministry of Investment of Saudi Arabia (MISA) has identified two areas with high investment potential: pharmaceutical and medical devices. The Ministry of Investment of Saudi Arabia (MISA) noted that around 90% of the medical devices in the country are imported. Supporting local manufacturing would help the country reduce its dependence on foreign companies. This is expected to significantly impact the growth of medical device packaging manufacturers in the country.

- Medical device manufacturers are seeking to operate in Saudi Arabia to take advantage of the opportunities offered by the government in the country. For instance, in 2024, J&J MedTech KSA, a Johnson & Johnson Company technology firm, announced the launch of direct operations in Saudi Arabia. The company offers medical and surgical equipment, and its direct operation in the country helps contribute to Vision 2030 to support the development of the healthcare sector.

- According to the International Trade Administration, Saudi Arabia accounts for around 60% of the Gulf Cooperation Council (GCC) countries' healthcare expenditure. In 2023, healthcare and social development spending accounts for approximately USD 50.4 billion compared to the previous year. Moreover, the medical device market in Saudi Arabia is growing at 10% annually. The strong growth in the medical device sector, with rising healthcare concerns among the Saudi population and increasing consumption of healthcare services, is anticipated to aid the development of the medical device packaging market.

MEA Medical Devices Packaging Industry Overview

The Middle East and Africa medical devices packaging market is semi-consolidated . Some of the major players in the market are Amcor Group GmbH, Sonoco Products Company, DS Smith PLC, Wipak Group, Constantia Flexibles GmbH, and WestRock Company. The players are focusing on expanding their presence and product portfolio in the region to gain an advantage of the market opportunities.

- November 2023- Amcor Group GmbH launched a new mono-material polyethylene (PE) laminate. The new mono-material laminate is designed to support various packaging formats. It can replace non-recyclable lidding in 3D thermoplastic packages, commonly used in drapes and protective materials, catheters and injection systems, and tubing. It also suits 2D pouch applications for wound care materials and gloves.

- June 2023 - Rose Plastic Medical Packaging GmbH announced the launch of DentalImplantPack, a plastic tube container for delicate dental implants. The new plastic tube container for the dental implant offers easy handling during surgery and safety during transport so that the product reaches the customer intact.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Geopolitical Scenario on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Sterile Packaging for Medical Equipment

- 5.1.2 Investing Heavily in Developing the Healthcare Sector

- 5.2 Market Restraints

- 5.2.1 Government Regulation for Plastic Usage

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Plastic

- 6.1.2 Paper and Paper Board

- 6.1.3 Other Raw Materials

- 6.2 By Product Type

- 6.2.1 Pouches and Bags

- 6.2.2 Trays

- 6.2.3 Boxes

- 6.2.4 Clamshells

- 6.2.5 Other Product Types

- 6.3 By Application

- 6.3.1 Sterile Packaging

- 6.3.2 Non-sterile Packaging

- 6.4 By Country

- 6.4.1 Saudi Arabia

- 6.4.2 United Arab Emirates

- 6.4.3 South Africa

- 6.4.4 Egypt

- 6.4.5 Rest of Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Sonoco Products Company

- 7.1.3 DS Smith PLC

- 7.1.4 Wipak Group

- 7.1.5 Constantia Flexibles GmbH

- 7.1.6 WestRock Company

- 7.1.7 Rose Plastic Medical Packaging GmbH

- 7.1.8 Amber Packaging Industries LLC

- 7.1.9 Intermat Flexible Packaging (Pak Holding AS)

- 7.1.10 Ispak Esnek Ambalaj Sanayi AS

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 101 Pages

- 納期

- 2~3営業日