中国の電気自動車用VRLA電池:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

China Electric Vehicle Vrla Batteries - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636516

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

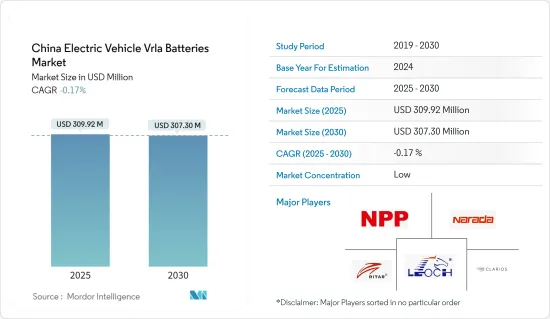

中国の電気自動車用VRLA電池市場規模は、2025年に3億992万米ドルと推定され、2030年には3億730万米ドルに減少すると予測されます。

主要ハイライト

- 今後数年間、電気自動車用VRLA電池の需要は増加すると予測されます。これは、リチウムイオン電池と比較して費用対効果が高いことと、全国的に電気スクーターや電気二輪車の人気が急上昇していることが要因です。

- 逆に、高性能EVの標準となりつつある先進的なリチウムイオン電池への迅速な移行は、電気自動車用VRLA電池市場の成長にとって課題となります。

- しかし、VRLA電池は、特にエネルギー密度よりも信頼性を優先するシナリオでは、電気自動車の補助電源またはバックアップとして依然として価値を保っています。このニッチは近い将来、電気自動車用VRLA電池市場に大きな成長の可能性をもたらします。

中国の電気自動車用VRLA電池市場の動向

吸収ガラスマット電池が大きく成長

- VRLA電池、特に吸収ガラスマット(AGM)タイプは、その費用対効果、信頼性、メンテナンスフリーの性質から、中国の電気自動車産業で頻繁に利用されています。AGM電池はリチウムイオン・電池よりも手頃な価格で、電気自動車にとって魅力的な選択肢です。

- VRLA電池のサブセットであるAGM(Absorbed Glass Mat)電池は、従来の鉛蓄電池を上回る性能で注目を集めています。電解液を吸収するためにガラスマットセパレーターを利用することで、AGM電池は明確な利点を提供し、特定のEVアプリケーション、特に低コストの電気モビリティに特に適しています。

- 中国で二輪車や三輪車の電気自動車が普及するにつれて、このセグメントのAGM電池の需要が急増しています。しかし、二輪車と三輪車の販売が最近落ち込んでいるため、AGM電池部門はピンチを感じています。国際エネルギー機関(IEA)のデータによると、中国の電動二輪車販売台数は減少しており、2021年の1,020万台から590万台に激減しています。今後は、リチウムイオンを筆頭とする代替電池技術の台頭が、AGM市場に課題を突きつけることになります。

- 中国の電気自動車用電池市場は、主に新エネルギー自動車(NEV)の普及によって推進されており、その勢いは政府の義務化によってさらに加速しています。例えば、財務省は2023年6月に、2024年と2025年に購入されるNEVに対して、1台当たり3万人民元(4,170米ドル)の消費税免除を発表しました。この免税措置は、2026~2027年にかけての購入については1万5,000人民元まで縮小されます。さらに、EV販売をさらに刺激するために2020年4月に開始された中国の国家新エネルギー車補助金制度は、当初2020年末に終了する予定だったが、COVID-19の流行により2022年まで延長されました。

- EVのセグメント、特にコストに敏感な地域でAGM電池の重要性が高まっていることは、VRLA技術の持続的な重要性を強調しています。さらに、政府の合意やイニシアティブは、EVの普及を促進し、地域のEVインフラを強化するというコミットメントを強調しています。

- その結果、これらのイニシアチブは同地域のEV生産を後押しするだけでなく、今後数年間でEV用VRLA電池の需要を高めることになります。

新エネルギー車向け充電インフラを対象とする中国の施策

- 中国の電気自動車充電インフラ推進連盟(EVCIPA)によると、2023年8月現在、中国は720万8,000基の充電インフラ(公共と民間)を有しています。このうち、227万2,000台が公共の充電スタンドで、493万6,000台が自家用に指定されています。

- 2024年末の予測では、中国におけるEV充電器の数は958万台に急増し、約84%の大幅な伸びを示します。この上昇軌道は、EV充電器市場に計り知れない可能性と機会があることを強調しています。

- 中国は、EV充電市場を強化するために、以下の重要な日付で一連の的を絞った施策を導入しています。

- 2023年6月(施策文書:高品質の充電インフラシステムのさらなる構築に関する指導意見):この施策は、都市部、高速道路、農村部にわたる統一された充電ネットワークの確立を目指しています。標準化、規制、市場モニタリングの必要性を強調し、2030年までに世界の充電技術を支配するというビジョンを掲げています。

- 2023年5月(施策文書:地方における新エネルギー自動車の普及と地方活性化をよりよく支援するための充電インフラ開発の加速化):このイニシアティブは、県レベルでの公共充電ネットワークの設置において地方自治体を支援し、商業ビル、交通拠点、高速道路のパーキングエリアへの充電ポイントの設置を促進します。

- 2023年1月(施策文書:エネルギーエレクトロニクス産業の開発促進に関する指導意見):5G基地局や新エネルギー自動車充電ステーションなど、新興設備におけるエネルギーエレクトロニクス製品の応用を促進することに重点を置く。

- 2022年12月(施策文書:第14次5カ年計画における内需拡大実施計画):駐車場、充電ステーション、電池交換ステーション、水素充填ステーションなどの支援施設の強化を強調。

- 例えば、第14次5ヵ年計画に沿った北京市都市管理開発計画では、2025年までに累計70万台の電気自動車充電器を目標としています。

- このような政府の取り組みは、単なる数ではなく、充電設備の安全性、インテリジェンス、接続性を高めることに重点を置いています。このような進歩はEV産業を前進させ、今後数年間の電池市場を強化する可能性があります。

中国の電気自動車用VRLA電池産業概要

中国の電気自動車用VRLA電池市場は適度にセグメント化されています。主要企業(順不同)には、NPP Power Group、Vision Battery Group、Zhejiang Narada Power Source、LEOCH Battery Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- VRLA電池の費用対効果

- 電動スクーターと電動二輪車の成長

- 抑制要因

- 代替電池技術の利用可能性

- 促進要因

- サプライチェーン分析

- 産業の魅力-PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- タイプ別

- 吸収ガラスマット電池

- ゲル電池

- 車種別

- 二輪車

- 低速EV

- 産業用EV

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- LEOCH Battery Corporation

- Zhejiang Narada Power Source Co., Ltd.

- NPP Power Group

- C&D Technologies

- Shenzhen Ritar Power Co Ltd

- Clarious LLC

- Ritar Power

- GS Yuasa Battery Ltd.

- JYC Battery Manufacturer Co. Ltd.

- Chilwee Battery

- その他の著名な企業一覧

- 市場ランキング/シェア分析

第7章 市場機会と今後の動向

- バックアップと補助アプリケーション

目次

Product Code: 50003869

The China Electric Vehicle Vrla Batteries Market size is estimated at USD 309.92 million in 2025, and is expected to decline to USD 307.30 million by 2030.

Key Highlights

- In the coming years, the demand for electric vehicle VRLA batteries is projected to rise, driven by their cost-effectiveness compared to lithium-ion batteries and the surging popularity of electric scooters and bikes nationwide.

- Conversely, the swift transition to advanced lithium-ion batteries, which are becoming the standard for high-performance EVs, poses a challenge to the growth of the electric vehicle VRLA batteries market.

- However, VRLA batteries still hold value as auxiliary power sources or backups in electric vehicles, especially in scenarios prioritizing reliability over energy density. This niche presents substantial growth potential for the electric vehicle VRLA batteries market in the near future.

China Electric Vehicle Vrla Batteries Market Trends

Absorbed Glass Mat Battery Witness Significant Growth

- Due to their cost-effectiveness, reliability, and maintenance-free nature, VRLA batteries, particularly Absorbed Glass Mat (AGM) types, are frequently utilized in China's EV industry. AGM batteries, being more affordable than lithium-ion counterparts, present an attractive option for electric vehicles.

- AGM (Absorbed Glass Mat) batteries, a subset of VRLA batteries, have garnered attention for outperforming traditional lead-acid variants. By utilizing a glass mat separator to absorb the electrolyte, AGM batteries offer distinct advantages, making them particularly suited for certain EV applications, especially in budget-friendly electric mobility.

- As two and three-wheeler electric vehicles gain traction in China, the demand for AGM batteries in this segment has surged. Yet, with a recent downturn in two and three-wheeler sales, the AGM battery sector is feeling the pinch. Data from the International Energy Agency (IEA) reveals a drop in electric two-wheeler sales in China, plummeting from 10.2 million in 2021 to 5.9 million. Looking ahead, the rise of alternative battery technologies, notably lithium-ion, poses a challenge to the AGM market.

- China's electric vehicle battery market is primarily propelled by the uptake of new energy vehicles (NEVs), a momentum further fueled by government mandates. For example, in June 2023, The Ministry of Finance announced a sales tax exemption of CNY 30,000 (USD 4,170) per vehicle for NEVs purchased in 2024 and 2025. This exemption will taper to CNY 15,000 for purchases made between 2026 and 2027. Additionally, China's national New Energy Vehicle Subsidy Program, initiated in April 2020 to further stimulate EV sales, was originally set to conclude at the end of 2020 but received an extension until 2022 due to the COVID-19 pandemic.

- The growing prominence of AGM batteries in the EV domain, especially in cost-sensitive regions, underscores the sustained significance of VRLA technology. Furthermore, government agreements and initiatives underscore a commitment to bolster EV adoption and enhance the region's EV infrastructure.

- Consequently, these initiatives are poised to not only boost EV production in the region but also elevate the demand for EV VRLA batteries in the coming years.

Chinese Policies Targeting Charging Infrastructure for New Energy Vehicles

- As of August 2023, China boasted 7,208,000 charging infrastructure units (both public and private), according to the China Electric Vehicle Charging Infrastructure Promotion Alliance (EVCIPA). Out of these, 2,272,000 were public charging stands, while 4,936,000 were designated for private use.

- Projections for the end of 2024 suggest that the number of EV chargers in China will surge to 9.58 million units, representing a substantial growth rate of approximately 84 percent. This upward trajectory underscores the immense potential and opportunities within the EV charging market.

- China has introduced a series of targeted policies to strengthen its EV charging market, with the following key dates:

- June 2023 (Policy Document: Guiding Opinions on Further Constructing a High-Quality Charging Infrastructure System): The policy aims to establish a unified charging network across urban, highway, and rural areas. It emphasizes the need for standardization, regulation, and market oversight, with a vision to dominate global charging technologies by 2030.

- May 2023 (Policy Document: Accelerating the Development of Charging Infrastructure to Better Support the Deployment of New Energy Vehicles in Rural Areas and Rural Revitalization): This initiative supports local governments in setting up public charging networks at the county level and facilitates the installation of charging points in commercial buildings, traffic hubs, and highway parking areas.

- January 2023 (Policy Document: Guiding Opinions on Promoting the Development of Energy Electronics Industry): Focuses on boosting the application of energy electronic products in emerging facilities, including 5G base stations and new energy vehicle charging stations.

- December 2022 (Policy Document: Implementation Plan for Expanding Domestic Demand in the 14th Five-Year Plan): Emphasizes the enhancement of supporting facilities like parking lots, charging stations, battery swapping stations, and hydrogen refueling stations.

- For example, the Beijing Urban Management Development Plan, aligned with the 14th Five-Year Plan, targets a cumulative total of 700,000 electric vehicle chargers by 2025.

- These governmental efforts are not just about numbers; they focus on elevating the safety, intelligence, and connectivity of charging facilities. Such advancements are poised to propel the EV industry forward, potentially bolstering the battery market in the coming years.

China Electric Vehicle Vrla Batteries Industry Overview

The China Electric Vehicle VRLA Batteries market is moderately fragmented. Some of the key players (not in particular order) are NPP Power Group., Vision Battery Group, Zhejiang Narada Power Source Co., Ltd., and LEOCH Battery Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Cost-Effectiveness of VRLA batteries

- 4.5.1.2 Growth in Electric Scooters and Bikes

- 4.5.2 Restraints

- 4.5.2.1 Availability of Alternate Battery Technology

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Absorbed Glass Mat Battery

- 5.1.2 Gel Battery

- 5.2 By Vehicle Type

- 5.2.1 Two-Wheelers

- 5.2.2 Low-Speed EVs

- 5.2.3 Industrial Evs

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 LEOCH Battery Corporation

- 6.3.2 Zhejiang Narada Power Source Co., Ltd.

- 6.3.3 NPP Power Group

- 6.3.4 C&D Technologies

- 6.3.5 Shenzhen Ritar Power Co Ltd

- 6.3.6 Clarious LLC

- 6.3.7 Ritar Power

- 6.3.8 GS Yuasa Battery Ltd.

- 6.3.9 JYC Battery Manufacturer Co. Ltd.

- 6.3.10 Chilwee Battery

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Backup and Auxiliary Applications

中国の電気自動車用VRLA電池:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日