|

市場調査レポート

商品コード

1636483

中東・アフリカの電気自動車用電池負極の市場シェア分析、産業動向、成長予測(2025~2030年)Middle-East And Africa Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東・アフリカの電気自動車用電池負極の市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

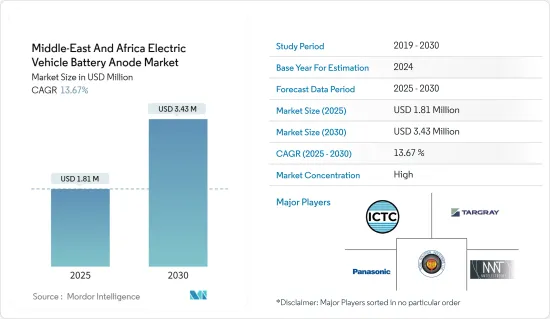

中東・アフリカの電気自動車用電池負極市場規模は、2025年に181万米ドルと推定され、予測期間(2025~2030年)のCAGRは13.67%で、2030年には343万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、政府の施策と投資が電気自動車の普及を促進し、市場を牽引するとみられます。

- 逆に、この地域では負極製造に携わる企業が限られているため、市場の成長が阻害される可能性があります。

- 負極材料の研究開発は現在進行中であり、市場にとって有望な成長機会となります。

- 調査対象期間中、アラブ首長国連邦が中東・アフリカの電気自動車用電池負極市場を独占すると予測されます。

中東・アフリカの電気自動車用電池負極市場動向

リチウムイオン電池が市場を独占

- リチウムは電気自動車(EV)用電池の製造において重要な役割を果たしています。充電可能なリチウムイオン電池の主要成分であるリチウムの高いエネルギー密度は、走行距離の延長を容易にします。最近、中東・アフリカでは、特に負極のような電池部品のリチウムイオン製造装置が急増しています。

- 例えば、NextSource Materialsは2024年7月、サウジアラビアに電気自動車セグメントに特化した黒鉛負極の新工場を建設する計画を発表しました。投資額は2億8,000万米ドルを超え、このベンチャーは同社の世界の拡大戦略を浮き彫りにしています。この工場では、リチウムイオン電池に特化した黒鉛負極活物質を年間2万トン生産し、同地域の電気自動車用電池負極市場を強化することを目指しています。

- 同様に、中東・アフリカでリチウムイオン製造装置が普及するにつれ、負極の需要も増加します。2024年3月には、Saudi AramcoとAbu Dhabi National Oil Companyが油田かん水からリチウムを抽出するために提携し、湾岸諸国が電気自動車生産と負極需要の拡大に意欲を示しています。

- 2023年12月、SHENZEN LEMI Technology Development Companyがナイジェリア連邦電力省と中国生態環境省の監督を受け、ナイジェリアで1億5,000万米ドルのリチウムイオン電池プラントの契約を獲得しました。このプロジェクトは、アフリカにおける「一帯一路」構想の目標や、気候変動技術の進展に向けた世界の取り組みに沿ったものです。

- 歴史的に見ると、リチウムイオン電池の価格が急落するにつれ、負極などの関連部品の需要が急増しています。Bloomberg NEFによると、2023年のリチウムイオン電池の平均価格は139米ドル/kWhで、2014年から5倍も下落しています。この価格下落は、負極市場が将来的に活況を呈することを示唆しています。

- さらに、アラブ首長国連邦と南アフリカでは電気自動車の普及が進んでいます。国際エネルギー機関(IEA)は、2023年のこれらの国の電気自動車販売台数が前年比53.5%増の2万9,980台に達したと指摘しています。他の地域諸国もEV需要で追随する可能性が高く、負極市場は恩恵を受けることになります。

- リチウムイオン電池と負極の生産動向を考えると、中東・アフリカの電気自動車用電池負極市場は成長する態勢が整っています。

アラブ首長国連邦が最大市場

- アラブ首長国連邦は、交通部門からの二酸化炭素排出を抑制することを目的とした政府の取り組みに後押しされ、e-モビリティの急速な普及を目の当たりにしています。2030年までに4万2,000台の電気自動車(EV)を走らせるという政府の野心的な目標は、このコミットメントを強調しています。

- 2024年8月、米国を拠点とするMullen Automotiveは、アラブ首長国連邦のボルト・モビリティ社と約2億1,000万米ドル相当の契約を締結しました。この契約により、アラブ首長国連邦は2025年末までにクラス1とクラス3の電気自動車を3,000台購入することになっています。このような電気自動車の増加により、電池や陽極のような部品に対する需要が高まり、市場の成長に拍車がかかるものと考えられます。

- 2024年6月、アラブ首長国連邦に全電気自動車のライドヘイリングプラットフォームであるBluSmartが参入しました。この動きにより、BluSmartはアラブ首長国連邦初の100%電気自動車によるプレミアムリムジンサービスとなり、サステイナブル輸送に対する国のコミットメントが強調されました。電気自動車の普及が予想されることから、電池や陽極のような必須部品の需要が高まっている

- 2024年5月、Al Ghurair Motorsは、欧州メーカーのTAM-Europeと電気商用車を中心としたディーラー提携を結びました。この提携は、アラブ首長国連邦の2050年ネット・ゼロ・エミッション目標に対するAl Ghurair Motorsのコミットメントを強調するだけでなく、より環境に優しい輸送風景と電気自動車用電池負極の盛況な市場の到来を告げるものでもあります。

- アラブ首長国連邦における電気自動車の販売は増加傾向にあります。国際エネルギー機関のデータによると、2023年にはアラブ首長国連邦で2万8,900台の電気自動車が販売され、前年比53%増という驚異的な伸びを示しました。この勢いを考えると、電気自動車の需要、ひいては電気自動車用電池負極市場は大きく成長する可能性があります。

- このような発展により、電気自動車用電池負極市場は今後数年間で大きく成長することが予想されます。

中東・アフリカの電気自動車用電池負極産業概要

中東・アフリカの電気自動車用電池負極市場は半固体化しています。主要企業(順不同)には、ICTC Egypt、Total Solution Industries LLC、Panasonic Holdings Corp、Targray、NMT Electrodesなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の導入を支援する政府の施策

- リチウムイオン電池の価格低下

- 抑制要因

- 同地域における限られた参入企業の存在

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 電池タイプ

- 鉛蓄電池

- リチウムイオン電池

- その他の電池タイプ

- 材料

- リチウム

- 黒鉛

- シリコン

- その他

- 地域

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- ナイジェリア

- エジプト

- カタール

- その他の中東・アフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- ICTC Egypt

- NMT Electrodes

- Panasonic Holdings Corp

- Total Solution Industries LLC

- Gamma Anode

- Zinc Egypt

- TAQAT Development

- NextSource

- Emirates Global Aluminium

- Targray

- その他の著名な企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- 負極材料の研究開発

目次

Product Code: 50003752

The Middle-East And Africa Electric Vehicle Battery Anode Market size is estimated at USD 1.81 million in 2025, and is expected to reach USD 3.43 million by 2030, at a CAGR of 13.67% during the forecast period (2025-2030).

Key Highlights

- In the medium term, government policies and investments are likely to boost the adoption of electric vehicles, subsequently driving the market.

- Conversely, the market's growth may be stunted by the limited involvement of companies in anode manufacturing within the region.

- Ongoing research and development in anode materials present promising growth opportunities for the market.

- During the study's focus period, the United Arab Emirates is projected to dominate the electric vehicle battery anode market in the Middle East and Africa.

Middle-East And Africa Electric Vehicle Battery Anode Market Trends

Lithium-ion Batteries to Dominate the Market

- Lithium plays a crucial role in manufacturing batteries for electric vehicles (EVs). As the key ingredient in rechargeable lithium-ion batteries, lithium's high energy density facilitates extended driving ranges. Recently, the Middle East and Africa have seen a surge in lithium-ion manufacturing units, particularly for battery components like anodes.

- For example, in July 2024, NextSource Materials announced plans for a new graphite anode plant in Saudi Arabia, focusing on the electric vehicle sector. With an investment exceeding USD 280 million, this venture highlights the company's global expansion strategy. The plant aims to produce 20,000 tonnes of graphite anode active material annually, specifically for lithium-ion batteries, bolstering the region's electric vehicle battery anode market.

- Similarly, as lithium-ion manufacturing units proliferate in the Middle East and Africa, the demand for anodes is set to rise. In March 2024, Saudi Aramco and the Abu Dhabi National Oil Company teamed up to extract lithium from oilfield brine, signaling Gulf states' ambitions in electric vehicle production and the growing anode demand.

- In December 2023, SHENZEN LEMI Technology Development Company, with oversight from Nigeria's Federal Ministry of Power and China's Ministry of Ecology and Environment, secured a deal for a USD 150 million lithium-ion battery plant in Nigeria. This project aligns with the Belt and Road Initiative's goals in Africa and global efforts to advance climate technology.

- Historically, as lithium-ion battery prices have plummeted, the demand for related components like anodes has surged. Bloomberg NEF reported the average lithium-ion battery price in 2023 at USD 139 USD/kWh, marking a fivefold drop since 2014. This price decline suggests a buoyant future for the anode market.

- Furthermore, electric vehicle adoption has been on the rise in the United Arab Emirates and South Africa. The International Energy Agency noted that 2023 saw electric car sales in these nations hit 29,980 units, a 53.5% leap from the prior year. With other regional countries likely to follow suit in EV demand, the anode market stands to benefit.

- Given the trends in lithium-ion batteries and anode production, the electric vehicle battery anode market in the Middle East and Africa is poised for growth.

United Arab Emirates to be the Largest Market

- The United Arab Emirates (UAE) is witnessing a swift embrace of e-mobility, bolstered by government initiatives aimed at curbing carbon emissions from the transportation sector. The government's ambitious goal of having 42,000 electric vehicles (EVs) on the roads by 2030 underscores this commitment.

- In August 2024, Mullen Automotive, a US-based firm, sealed a deal worth around USD 210 million with UAE's Volt Mobility. As per the agreement, the UAE is set to purchase 3,000 Class 1 and Class 3 electric vehicles by the end of 2025. This uptick in electric vehicles is poised to drive demand for batteries and components like anodes, fueling the market growth.

- In June 2024, BluSmart, an all-electric ride-hailing platform, made its entry into the UAE. This move establishes BluSmart as the UAE's first-ever 100% electric, premium limousine service, highlighting the nation's commitment to sustainable transport. The anticipated rise in electric vehicle adoption will drive demand for batteries and essential components like anodes.

- In May 2024, Al Ghurair Motors forged a dealership partnership with European manufacturer TAM-Europe, centering on electric commercial vehicles. This alliance not only emphasizes Al Ghurair Motors' commitment to the UAE's 2050 net-zero emissions goal but also heralds a greener transportation landscape and a thriving market for electric vehicle battery anodes.

- Electric vehicle sales in the UAE have been on an upward trajectory. Data from the International Energy Agency reveals that 2023 saw sales of 28,900 electric cars in the UAE, marking a staggering 53% jump from the prior year. Given this momentum, the demand for electric vehicles-and by extension, the electric vehicle battery anode market-is poised for significant growth.

- Given these developments, the electric vehicle battery anode market is set for a robust surge in the coming years.

Middle-East And Africa Electric Vehicle Battery Anode Industry Overview

The Middle East and Africa Electric Vehicle battery anode market is semi-consolidated. Some of the major players (not in particular order) include ICTC Egypt, Total Solution Industries LLC, Panasonic Holdings Corp, Targray, and NMT Electrodes.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government policies supporting adoption of electric vehicles

- 4.5.1.2 Declining Lithium-ion Battery Prices

- 4.5.2 Restraints

- 4.5.2.1 Presence of limited players in the Region

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lead Acid Batteries

- 5.1.2 Lithium-ion Batteries

- 5.1.3 Other Battery Types

- 5.2 Material

- 5.2.1 Lithium

- 5.2.2 Graphite

- 5.2.3 Silicon

- 5.2.4 Others

- 5.3 Geography

- 5.3.1 Saudi Arabia

- 5.3.2 South Africa

- 5.3.3 United Arab Emirates

- 5.3.4 Nigeria

- 5.3.5 Egypt

- 5.3.6 Qatar

- 5.3.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ICTC Egypt

- 6.3.2 NMT Electrodes

- 6.3.3 Panasonic Holdings Corp

- 6.3.4 Total Solution Industries LLC

- 6.3.5 Gamma Anode

- 6.3.6 Zinc Egypt

- 6.3.7 TAQAT Development

- 6.3.8 NextSource

- 6.3.9 Emirates Global Aluminium

- 6.3.10 Targray

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Research & Development in anode material