|

|

市場調査レポート

商品コード

1665045

EV用トラクションインバーター市場の機会、成長促進要因、産業動向分析、2025~2034年の予測EV Traction Inverter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| EV用トラクションインバーター市場の機会、成長促進要因、産業動向分析、2025~2034年の予測 |

|

出版日: 2024年12月10日

発行: Global Market Insights Inc.

ページ情報: 英文 240 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

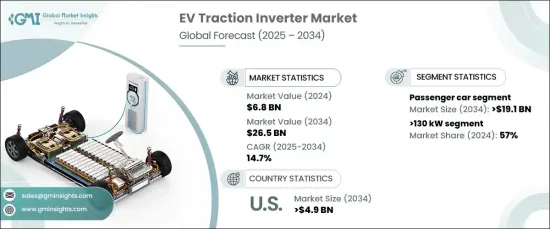

EV用トラクションインバーターの世界市場規模は2024年に68億米ドルとなり、2025年から2034年にかけて14.7%のCAGRで堅調に拡大すると予測されています。

各国政府が内燃機関車(ICE)に代わる、よりクリーンで持続可能な選択肢としてEVを推進しているため、世界中で電気自動車(EV)の導入が急増していることが、この市場成長の主な要因となっています。こうした取り組みは、温室効果ガスの排出を大幅に削減し、気候変動という差し迫った課題に取り組むことを目的としています。

パワーエレクトロニクスの進歩は、トラクション・インバーターの性能と効率に革命をもたらしています。炭化ケイ素や窒化ガリウムのようなワイドバンドギャップ半導体などの画期的な技術革新は、エネルギー効率の向上、熱管理の改善、よりコンパクトな設計を可能にしています。これらの技術は、走行距離の延長、充電時間の短縮、優れた車両性能に対する需要の高まりに対応するために不可欠であり、急速に進化するEV産業において不可欠なものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 68億米ドル |

| 予測金額 | 265億米ドル |

| CAGR | 14.7% |

車種別では、乗用車と商用車に分かれます。2024年には、乗用車セグメントが全体の73%を占めて市場をリードし、2034年には191億米ドルの市場規模になると予測されています。この成長を後押ししているのは、環境意識の高まり、政府のインセンティブ、不安定な燃料価格などが拍車をかけ、個人移動のためのEV利用が増加していることです。乗用車は、市場基盤が大きく生産台数が多いため、商用車よりも速いペースで電動モビリティに移行しています。

EV用トラクションインバーター市場は、出力に基づいて<=130 kW and>130kWセグメントに分類されます。130 kW超セグメントは、高性能EVへの嗜好の高まりと大型商用車の電動化に牽引され、2024年の市場シェアの57%を占めました。高出力インバーターは、卓越したトルク、加速、航続距離の延長を実現し、プレミアムEVや要求の厳しい商用アプリケーションのニーズに応えるために極めて重要です。これらの高度なインバータは、高性能条件下で効率的に動作するように設計されており、信頼性と最適なエネルギー利用を保証します。

米国のEV用トラクションインバーター市場は2024年に83%のシェアを占め、2034年には49億米ドルに達すると予測されています。同国の確立されたEV製造エコシステムと消費者需要の高まりが、この拡大を後押しする主要因となっています。さらに、EV生産やトラクション・インバーターを含む重要部品の開発に多額の投資が行われていることも、市場の成長軌道を後押ししています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 技術プロバイダー

- 部品サプライヤー

- メーカー

- OEMメーカー

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- 電気自動車(EV)の普及拡大

- パワーエレクトロニクス技術の進歩

- 商用車の電動化

- 充電インフラへの投資の増加

- 業界の潜在的リスク&課題

- EVとコンポーネントの初期コストの高さ

- 技術的な複雑さと熱管理

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:推進力別、2021年~2034年

- 主要動向

- BEV

- HEV

- PHEV

第6章 市場推計・予測:出力パワー別、2021~2034年

- 主要動向

- 130 kW以下

- 130 kW超

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- IGBT

- MOSFET

第8章 市場推計・予測:半導体材料別、2021年~2034年

- 主要動向

- GaN

- Si

- SiC

第9章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- 商用車

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- BorgWarner Inc.

- Continental AG

- DENSO Corporation

- Drive System Design Ltd

- Eaton Corporation

- Hitachi Astemo Ltd

- Hyundai Mobis Co. Ltd.

- Infineon Technologies AG

- John Deere Electronic Solutions

- Lear Corporation

- LG Magna e-Powertrain

- Marelli Corporation

- Meidensha Corporation

- Mitsubishi Electric Corporation

- Robert Bosch GmbH

- Tesla, Inc.

- Toyota Industries Corporation

- Valeo SA

- Vitesco Technologies

- ZF Friedrichshafen AG

The Global EV Traction Inverter Market was valued at USD 6.8 billion in 2024 and is projected to expand at a robust CAGR of 14.7% from 2025 to 2034. The surging adoption of electric vehicles (EVs) worldwide is a key driver of this market growth, as governments promote EVs as a cleaner and more sustainable alternative to internal combustion engine (ICE) vehicles. These efforts aim to significantly reduce greenhouse gas emissions and tackle the pressing challenges of climate change.

Advancements in power electronics are revolutionizing traction inverter performance and efficiency. Breakthrough innovations, such as wide-bandgap semiconductors like silicon carbide and gallium nitride, are enabling greater energy efficiency, improved thermal management, and more compact designs. These technologies are critical for addressing the growing demand for extended driving ranges, faster charging times, and superior vehicle performance, making them indispensable in the rapidly evolving EV industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.8 Billion |

| Forecast Value | $26.5 Billion |

| CAGR | 14.7% |

By vehicle type, the market is divided into passenger cars and commercial vehicles. In 2024, the passenger car segment led the market, accounting for 73% of the total share, and is projected to generate USD 19.1 billion by 2034. This growth is propelled by the increasing use of EVs for personal transportation, spurred by heightened environmental consciousness, government incentives, and volatile fuel prices. Passenger cars are transitioning to electric mobility at a faster pace than commercial vehicles, thanks to their larger market base and higher production volumes.

Based on output power, the EV traction inverter market is categorized into <=130 kW and >130 kW segments. The >130 kW segment held 57% of the market share in 2024, driven by the rising preference for high-performance EVs and the electrification of heavy-duty commercial fleets. High-powered inverters are crucial for delivering exceptional torque, acceleration, and extended range, catering to the needs of premium EVs and demanding commercial applications. These advanced inverters are engineered to operate efficiently under high-performance conditions, ensuring reliability and optimal energy utilization.

The U.S. EV traction inverter market dominated with an 83% share in 2024 and is projected to reach USD 4.9 billion by 2034. The country's well-established EV manufacturing ecosystem and growing consumer demand are key factors fueling this expansion. Additionally, significant investments in EV production and the development of critical components, including traction inverters, are bolstering the market growth trajectory.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Technology providers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 OEMs

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Growing adoption of electric vehicles (EV)

- 3.7.1.2 Advancements in power electronics technology

- 3.7.1.3 Electrification of commercial vehicles

- 3.7.1.4 Increasing investments in charging infrastructure

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High initial costs of EV and components

- 3.7.2.2 Technical complexity and thermal management

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 BEV

- 5.3 HEV

- 5.4 PHEV

Chapter 6 Market Estimates & Forecast, By Output Power, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 <=130 kW

- 6.3 >130 kW

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 IGBT

- 7.3 MOSFET

Chapter 8 Market Estimates & Forecast, By Semiconductor Material, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 GaN

- 8.3 Si

- 8.4 SiC

Chapter 9 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Passenger car

- 9.3 Commercial vehicle

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 BorgWarner Inc.

- 11.2 Continental AG

- 11.3 DENSO Corporation

- 11.4 Drive System Design Ltd

- 11.5 Eaton Corporation

- 11.6 Hitachi Astemo Ltd

- 11.7 Hyundai Mobis Co. Ltd.

- 11.8 Infineon Technologies AG

- 11.9 John Deere Electronic Solutions

- 11.10 Lear Corporation

- 11.11 LG Magna e-Powertrain

- 11.12 Marelli Corporation

- 11.13 Meidensha Corporation

- 11.14 Mitsubishi Electric Corporation

- 11.15 Robert Bosch GmbH

- 11.16 Tesla, Inc.

- 11.17 Toyota Industries Corporation

- 11.18 Valeo SA

- 11.19 Vitesco Technologies

- 11.20 ZF Friedrichshafen AG