|

市場調査レポート

商品コード

1928935

電気自動車用バッテリー試験市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Electric Vehicle Battery Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 電気自動車用バッテリー試験市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月12日

発行: Global Market Insights Inc.

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

概要

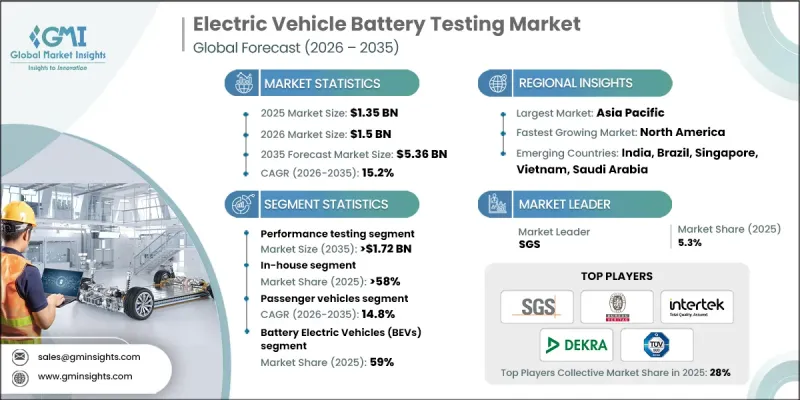

世界の電気自動車用バッテリー試験市場は、2025年に13億5,000万米ドルと評価され、2035年までにCAGR 15.2%で成長し、53億6,000万米ドルに達すると予測されています。

市場拡大は、世界の電気自動車生産の加速と密接に関連しており、これによりバッテリーメーカーやサプライヤーは安全性、信頼性、性能を確認するための先進的な試験ソリューションの導入を迫られています。バッテリー設計が高エネルギー密度、コンパクトな形状、新たな化学組成へと進化するにつれ、故障に伴う財務的・安全上のリスクは引き続き高まっています。メーカーは量産時の製品の一貫性を確保するため、複数の動作条件にわたる包括的な検証を優先しています。さらに、セル、モジュール、パックの各レベルにおける長期耐久性、劣化挙動、過酷条件耐性、熱安定性の評価ニーズが試験需要を後押ししています。バッテリー交換コストが高止まりする中、バッテリー試験はリスク管理戦略の必須要素となりました。かつては規制順守を目的とした活動でしたが、現在では電気モビリティエコシステム全体において、ブランド評価の保護、保証リスクの低減、製品品質全体の向上を図る戦略的投資と位置付けられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 13億5,000万米ドル |

| 予測金額 | 53億6,000万米ドル |

| CAGR | 15.2% |

性能試験セグメントは2025年に38%のシェアを占め、2035年までに17億2,000万米ドルに達すると予測されています。このセグメントは、様々な負荷条件や動作環境下でバッテリーが電力を効率的に供給する方法を評価することに重点を置いています。ライフサイクル評価は、基本的な充電サイクルを超えて、加速劣化試験、予測劣化分析、高度なバッテリー健全性モデリングを含むようになり、車両のより長い使用期待を支えています。

乗用車セグメントは2034年までCAGR 14.8%で成長すると予測されています。電気乗用車の普及拡大に伴い、航続距離、充電性能、耐久性、安全性に関する厳しい要件を満たすバッテリーの需要が増加し続けています。メーカーは一貫した性能を確保し、信頼性に対する消費者の期待に応えるため、広範な試験プロトコルに依存しています。

米国電気自動車用バッテリー試験市場は、2025年に2億3,220万米ドルと評価され、2026年から2035年にかけて堅調な成長が見込まれています。安全性検証と規制順守への重視の高まりが、高度な試験サービスの需要を牽引しています。メーカー各社は、技術的課題やコンプライアンス対応の増大を管理しつつ、迅速な商品化を支援するため、社内および外部委託の試験能力を拡大しています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 世界の電気自動車生産の成長

- 厳格な電池安全基準および規制基準

- 電池エネルギー密度の向上とシステム複雑性の増加

- OEMにおける品質保証と保証リスク低減への注力

- 世界の電池製造能力の拡大

- 業界の潜在的リスク&課題

- 高度な試験インフラの高額な資本コスト

- 長い試験サイクルと市場投入までの時間的プレッシャー

- 市場機会

- 第三者によるバッテリー試験サービスの成長

- デジタルおよび自動化試験技術の進歩

- 次世代電池化学の台頭

- 電池ライフサイクルの拡大とセカンドライフ応用

- 成長可能性分析

- 規制情勢

- 北米

- 米国:NHTSA自動車サイバーセキュリティベストプラクティス

- カナダ:カナダ自動車安全基準(CMVSS)

- 欧州

- 英国:UNECE規則第13号車両制動・安定性システム

- ドイツ:ISO 26262道路車両における電気電子システムの機能安全

- フランス:UNECE規則第79号ステアリング及び車両制御システム

- イタリア:ISO 21434道路車両サイバーセキュリティ工学

- スペイン:ISO 14001環境マネジメントシステム

- アジア太平洋地域

- 中国:GB/T 38628電気自動車用電池試験及びOTA更新セキュリティ要件

- 日本:ISO 26262道路車両の電気電子システムの機能安全

- インド:AIS 155自動車ソフトウェア向けサイバーセキュリティ及びOTA要件

- ラテンアメリカ

- ブラジル:ABNT NBR ISO 26262道路車両の機能安全

- メキシコ:NOM-194-SCFI車両安全性能基準

- アルゼンチン:ISO 9001品質マネジメントシステム

- 中東・アフリカ

- UAE:UNECE規則第155号サイバーセキュリティ及びサイバーセキュリティ管理システム

- 南アフリカ:ISO 26262道路車両における電気電子システムの機能安全

- サウジアラビア:SASO自動車技術規制サイバーセキュリティとソフトウェア

- 北米

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- コスト内訳分析

- 特許分析

- 持続可能性と環境面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- 試験基準とプロトコル

- 電池試験基準とプロトコル

- 認証試験と検証試験と型式承認試験の比較

- 必須試験要件とOEM固有の試験要件

- 電池化学種別試験

- 電池化学種別の試験要件

- 化学組成別熱暴走及び乱用試験の進化

- ライフサイクル段階に基づく試験

- デジタル、AI及びシミュレーションベースの試験

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協力関係

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:試験別、2022-2035

- 性能テスト

- 安全性試験

- ライフサイクル試験

- その他

第6章 市場推計・予測:調達方法別、2022-2035

- 自社調達

- アウトソーシング

第7章 市場推計・予測:車両別、2022-2035

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第8章 市場推計・予測:推進力別、2022-2035

- バッテリー式電気自動車(BEV)

- プラグインハイブリッド電気自動車(PHEV)

- ハイブリッド電気自動車(HEV)

第9章 市場推計・予測:コンポーネント別、2022-2035

- 電池セル

- バッテリーモジュール

- バッテリーパック

- バッテリー管理システム(BMS)

第10章 市場推計・予測:最終用途別、2022-2035

- 自動車メーカー

- 電池メーカー

- 研究開発機関

- 第三者試験サービス提供事業者

第11章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- ポルトガル

- クロアチア

- ベネルクス

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- タイ

- インドネシア

- ベトナム

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

第12章 企業プロファイル

- 世界プレイヤー

- ALS

- Applus+

- Bureau Veritas

- DEKRA

- DNV

- Element Materials Technology

- Eurofins

- Intertek

- SGS

- TUV SUD

- UL Solutions

- 地域プレイヤー

- AVL

- CSA

- FEV

- Instron

- KEMA Labs

- Nemko

- NTS(National Technical Systems)

- Tektronix

- VDE Testing and Certification

- Emerging/Disruptor Players

- Arbin Instruments

- AVILOO

- Bitrode

- Chroma ATE

- Digatron

- Espec

- Hioki

- Keysight Technologies

- Maccor

- Weiss Technik