|

市場調査レポート

商品コード

1537588

スマート植込み型ポンプの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Smart Implantable Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スマート植込み型ポンプの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年08月14日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

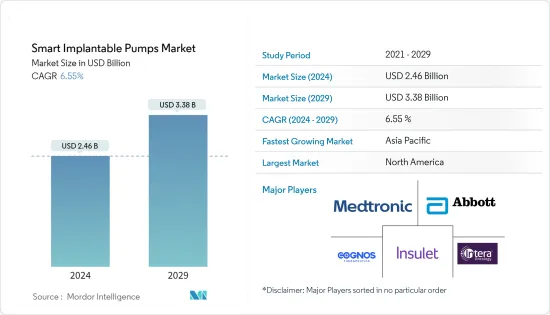

世界のスマート植込み型ポンプの市場規模は、2024年に24億6,000万米ドルと推定され、2029年には33億8,000万米ドルに達し、予測期間中(2024年~2029年)にCAGR6.55%で成長すると予測されています。

スマート植込み型ポンプ市場は、痙縮や慢性疼痛などの慢性疾患の有病率の増加、高齢者人口の増加、ヘルスケア意識の高まり、医療費の増加、有利な償還政策などの主な要因によって大きな成長を遂げています。

痙縮は、多発性硬化症、脳卒中、脳性麻痺などの神経疾患の主な症状です。痙縮は筋肉のこわばりや不随意な筋収縮を引き起こし、可動性や日常生活に影響を及ぼします。近年、痙縮の症例が増加しているため、スマート植込み型ポンプなどの新しい治療法に対する需要が高まっており、市場の成長を促進しています。

例えば、Physicians Group LLCが2023年12月に発表した記事によると、その特定の年には世界中で約1,200万人が痙縮に苦しんでいます。同出典はまた、電子植込み型ポンプや標的ドラッグデリバリーシステムを含む新しい理学療法アプローチは、運動機能を強化し、患者の痙縮を軽減する上で高い効率を示したと述べています。

Merz Therapeuticsが2024年5月に発表した報告書によると、脊髄損傷後、患者の約65%~74%に痙縮が見られ、2023年には患者の35%~45%に厄介な痙縮や問題のある痙縮が見られたと報告されています。同様に米国では、交通事故や職場に起因する外傷性脳損傷の負担が増加しており、痙縮やその他の慢性疼痛の症例が増加する可能性があります。

加齢に伴い、身体は心血管疾患、糖尿病、神経疾患などの慢性疾患にかかりやすくなるため、植込み型ポンプの需要が高まり、市場の成長を後押ししています。例えば、世界保健機関(WHO)が2024年3月に発表した報告書によると、世界の高齢者人口は2030年までに14億人、2050年までに21億人に増加する見通しです。この増加はかつてないペースで起こっており、特に発展途上国では今後数十年で加速すると思われます。このような人口の増加は、スマート植込み型ポンプの需要を増加させ、市場の成長を促進すると予想されます。

結論として、慢性疾患の罹患率の増加、高齢者人口の増加、ヘルスケア意識などの要因が市場の成長を促進すると予想されます。しかし、厳しい規制の枠組みや製品リコールが市場の成長を抑制すると予想されます。

スマート植込み型ポンプの市場動向

心血管セグメントは予測期間中に大幅な成長が見込まれる

心臓補助装置、ドラッグデリバリーポンプ、血行動態モニタリングポンプなどのスマート植込み型ポンプは、さまざまな心血管系疾患を管理するための低侵襲で的を絞ったアプローチを提供します。心血管疾患の有病率の上昇や心血管植込みポンプの技術的進歩などの主な要因は、予測期間中に心血管セグメントの成長を促進すると予想されています。

心血管疾患の高い有病率が、心血管植込み型ポンプセグメントの成長を促進しています。例えば、冠動脈疾患は近年高い割合で増加しています。2023年5月に米国疾病予防管理センターが発表した報告書によると、冠動脈性心疾患は最も発症率の高い心臓病です。2022年には、20歳以上の成人の約5%、つまり20人に1人が冠動脈疾患(CAD)に罹患しています。

同出典によると、米国では毎年約85万人が心臓発作を起こしています。このうち60万5,000人が初めて心臓発作を起こし、20万人以上がすでに心臓発作を起こしています。心不全管理、肺高血圧症、慢性狭心症の緩和やモニタリングなどの治療処置に使用されるこれらのポンプに対する需要が心血管植込み型ポンプ分野の成長に寄与しているため、これは植込み型ポンプにとって大きな市場機会となります。

また、同市場の主要企業は、心血管疾患の症例増加に対処するため、新技術の導入に取り組んでいます。例えば、2022年4月、Abiomedは、心臓ポンプの米国食品医薬品局(FDA)の早期実現可能性試験(EFS)の一環として、Impella Bridge-to-Recovery(BTR)が移植されたことを通知しました。この移植は、ノースウェスタン医学部ブルーム心臓血管研究所のDuc Thinh Pham医学博士とJane Wilcox医学博士によって行われました。

結論として、心血管疾患患者の増加と市場における最近の技術的進歩が、予測期間中の同分野の成長を促進すると予想されます。

予測期間中、北米が市場で大きなシェアを占める見込み

北米は、確立されたヘルスケアインフラ、より良い規制枠組み、政府支援、大手企業の存在により、スマート植込み型ポンプ市場で急成長が見込まれています。また、慢性疾患の増加や新しい治療法に対する需要の高まりが、同国の市場成長を後押しすると期待されています。

同地域では近年、糖尿病の有病率が劇的に増加しています。例えば、国立糖尿病・消化器腎臓病研究所が2024年1月に発表した報告書によると、2022年には国内で全年齢の糖尿病患者が3,840万人(人口の11.6%)に上りました。このうち、3,810万人が18歳以上の成人でした。さらに、2,970万人(人口の8.9%)以上の全年齢層が糖尿病と診断されています。

同出典によると、米国では9,760万人以上の成人が糖尿病予備軍と診断されており、これは成人総人口の約3分の1に相当します。人口における糖尿病および糖尿病予備軍の顕著な有病率は、グルコースレベルのモニタリングおよび管理に対する需要の増加により、植込み型ポンプ市場の成長を促進すると予想されます。

同様に、米国糖尿病協会が2023年11月に発表した報告書によると、米国では毎年約120万人が糖尿病と診断されています。同国は低年齢の糖尿病人口も多く、2024年には20歳未満の米国人が35万2,000人以上が糖尿病と診断されると推定されています。植込み型ポンプは、糖尿病患者が定期的に血糖値をモニターし、安定させるために不可欠です。したがって、糖尿病患者の増加は、植込み型ポンプ市場の成長を促進しています。

同市場の主要企業は、同地域でより大きな市場シェアを獲得するため、製品の発売や承認など、さまざまな成長戦略に取り組んでいます。例えば、2023年4月、米国食品医薬品局(FDA)は、SmartGuard技術でありながらフィンガースティックが不要なGuardian 4センサーを搭載したMedtronicのMiniMed 780Gシステムを承認しました。

結論として、慢性疾患患者の増加と主要企業が採用する製品発売の増加が、予測期間中の北米における植込み型ポンプ市場の成長を促進すると予想されます。

スマート植込み型ポンプ産業の概要

スマート植込み型ポンプ市場は中程度の競争であり、複数の大手企業で構成されています。ヘルスケア分野における様々な組織の統合や製品リコールの増加により、将来的には主要企業間の競争間の敵対関係が生じると予想されます。同市場の主要企業には、Medtronic、Abbott Laboratories、Cognos Therapeutics、Insulet Corporation、Intera Oncologyなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 痙縮や慢性疼痛などの慢性疾患の高い有病率と発生率

- 高齢者人口の増加

- ヘルスケア意識の高まり、医療費の増加、有利な償還政策

- 市場抑制要因

- 厳しい規制枠組と製品回収

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模:金額)

- ポンプタイプ別

- 灌流ポンプ

- マイクロポンプ

- 用途別

- 疼痛

- 痙縮

- 心血管

- その他

- エンドユーザー別

- 病院

- 外来手術センター

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Medtronic

- Abbott Laboratories

- Cognos Therapeutics, Inc.

- Insulet Corporation

- Tandem Diabetes

- Intera Oncology

- i2o Therapeutics, Inc.

- OrphaCare GmbH

第7章 市場機会と今後の動向

The Smart Implantable Pumps Market size is estimated at USD 2.46 billion in 2024, and is expected to reach USD 3.38 billion by 2029, growing at a CAGR of 6.55% during the forecast period (2024-2029).

The smart implantable pumps market is experiencing significant growth owing to major factors such as the growing prevalence of chronic diseases such as spasticity and chronic pain, the growing geriatric population, growing healthcare consciousness, rising healthcare expenditure, and favorable reimbursement policies.

Spasticity can be a major symptom of neurological conditions like multiple sclerosis, stroke, and cerebral palsy; spasticity causes muscle stiffness and involuntary muscle contractions, impacting mobility and daily activities. Rising cases of spasticity in recent years are increasing the demand for novel treatment methods, such as smart implantable pumps, thereby propelling the market's growth.

For instance, as per an article published by Physicians Group LLC in December 2023, around 12.0 million people worldwide suffered from spasticity in that particular year. The same source also stated that novel physical therapy approaches, including electronic implantable pumps and targeted drug delivery systems, showcased high efficiency in enhancing motor function and reducing patient spasticity.

According to a report published by Merz Therapeutics in May 2024, after spinal cord injury, about 65% to 74% of patients were reported to have spasticity, while 35% to 45% of patients had troublesome or problematic spasticity in 2023. Similarly, in the United States, there is a growing burden of traumatic brain injury caused by road accidents or workplace-related injuries, which can lead to a rise in cases of spasticity or other chronic pains.

As individuals age, their bodies become more susceptible to chronic diseases such as cardiovascular diseases, diabetes, and neurological diseases, creating a demand for implantable pumps and boosting the market's growth. For instance, according to a report published by the World Health Organization in March 2024, the geriatric population worldwide is poised to increase to 1.4 billion by 2030 and 2.1 billion by 2050. This increase is occurring at an unprecedented pace and would accelerate in the coming decades, particularly in developing countries. This rising population is expected to increase the demand for smart implantable pumps, thereby propelling the market's growth.

In conclusion, factors such as increasing incidence of chronic diseases, rising geriatric population, and healthcare awareness are expected to propel the market's growth. However, stringent regulatory frameworks and product recalls are expected to restrain the market's growth.

Smart Implantable Pumps Market Trends

Cardiovascular Segment is Expected to Witness a Significant Growth Over the Forecast Period

Smart implantable pumps, such as cardiac assist devices, drug delivery pumps, and hemodynamic monitoring pumps, offer a minimally invasive and targeted approach to managing various cardiovascular conditions. Major factors such as the rising prevalence of cardiovascular diseases and technological advancements of cardiovascular implantable pumps are expected to propel the growth of the cardiovascular segment during the forecast period.

The high prevalence of cardiovascular diseases is propelling the growth of the cardiovascular implantable pumps segment. For instance, coronary artery disease has risen at a high rate in recent years. As per a report published by the Centers for Disease Control and Prevention in May 2023, coronary heart disease is the most highly occurring form of heart disease. Approximately 5% of adults aged 20 and older, or 1 in 20, were affected by Coronary Artery Disease (CAD) in 2022.

According to the same source, about 850,000 people in the United States have a heart attack every year. Among these, 605,000 have had their first heart attack, and over 200,000 people have already had one. This presents a substantial market opportunity for implantable pumps, as the demand for these pumps used in treatment procedures such as heart failure management, pulmonary hypertension, and chronic angina relief and monitoring contributes to the growth of the cardiovascular implantable pumps segment.

Major players in the market are also working on introducing novel technologies to address the rising cases of cardiovascular diseases. For instance, in April 2022, Abiomed informed that the Impella Bridge-to-Recovery (BTR) was implanted as part of the heart pump's US Food and Drug Administration (FDA) Early Feasibility Study (EFS). The implant was done by Duc Thinh Pham, MD, and Jane Wilcox, MD, at the Northwestern Medicine Bluhm Cardiovascular Institute.

In conclusion, the rising cases of cardiovascular diseases and recent technological advancements in the market are expected to propel the segment's growth during the forecast period.

North America is Expected to Hold a Significant Share in the Market Over the Forecast Period

North America is expected to grow rapidly in the smart implantable pumps market due to its well-established healthcare infrastructure, better regulatory framework, government support, and major player presence. In addition, the increasing number of chronic diseases and rising demand for novel treatment methods are expected to boost the market's growth in the country.

The prevalence of diabetes has increased dramatically in the region in recent years. For instance, according to a report published by the National Institute of Diabetes and Digestive and Kidney Diseases in January 2024, in 2022, 38.4 million people of all ages had diabetes (11.6% of the population) in the country. Among these, 38.1 million were adults ages 18 years or older. Moreover, over 29.7 million people of all ages have been diagnosed with diabetes (8.9% of the population).

According to the same source, over 97.6 million adults in the United States were diagnosed with prediabetes, representing approximately one-third of the total adult population. The significant prevalence of diabetes and prediabetes in the population is expected to drive growth in the implantable pumps market due to increased demand for monitoring and managing glucose levels.

Similarly, according to a report published by the American Diabetes Association in November 2023, about 1.2 million US citizens are diagnosed with diabetes every year. The country also has a high under-age diabetic population, with over 352,000 Americans under age 20 estimated to have been diagnosed with diabetes in 2024. Implantable pumps are vital for diabetic patients to monitor and stabilize their blood glucose levels regularly; thus, the rising number of diabetic patients is propelling the growth of the implantable pumps market.

Key players in the market are working on various growth strategies, such as product launches and approvals, to acquire a larger market share in the region. For instance, in April 2023, the United States Food and Drug Administration (FDA) approved Medtronic's MiniMed 780G system with the Guardian 4 sensor, which requires no fingersticks while in SmartGuard technology.

In conclusion, the increasing cases of chronic diseases and the increasing product launches adopted by key players are expected to propel the growth of the implantable pumps market in North America during the forecast period.

Smart Implantable Pumps Industry Overview

The smart implantable pumps market is moderately competitive and consists of several major players. The increasing consolidations of various organizations and product recalls in the healthcare sector are expected to generate competitive rivalry among the key players in the future. Some of the major players in the market are Medtronic, Abbott Laboratories, Cognos Therapeutics Inc., Insulet Corporation, and Intera Oncology.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Prevalence and Incidence of Chronic Diseases such as Spasticity & Chronic Pain

- 4.2.2 Growing Geriatric Population

- 4.2.3 Growing Healthcare Consciousness, Rising Healthcare Expenditure and Favorable Reimbursement Policies

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Framework and Product Recalls

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Pump Type

- 5.1.1 Perfusion Pumps

- 5.1.2 Micro Pumps

- 5.2 By Application

- 5.2.1 Pain

- 5.2.2 Spasticity

- 5.2.3 Cardiovascular

- 5.2.4 Others

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Medtronic

- 6.1.2 Abbott Laboratories

- 6.1.3 Cognos Therapeutics, Inc.

- 6.1.4 Insulet Corporation

- 6.1.5 Tandem Diabetes

- 6.1.6 Intera Oncology

- 6.1.7 i2o Therapeutics, Inc.

- 6.1.8 OrphaCare GmbH