|

市場調査レポート

商品コード

1699401

植込み型医療機器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Implantable Medical Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 植込み型医療機器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月27日

発行: Global Market Insights Inc.

ページ情報: 英文 155 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

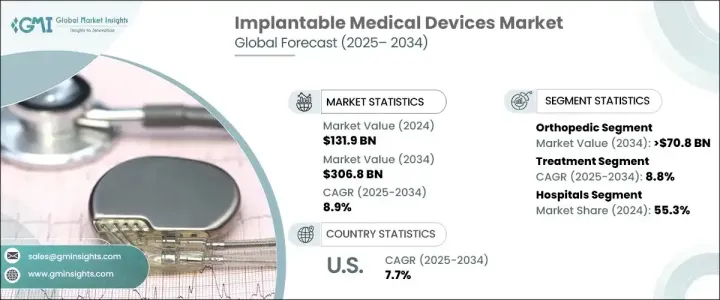

植込み型医療機器の世界市場は、2024年に1,319億米ドルと評価され、2025年から2034年にかけてCAGR 8.9%で成長すると予測されています。

この成長には、心血管疾患、神経疾患、整形外科的問題などの慢性疾患の有病率の増加が寄与しており、これらすべてにおいて高度な埋め込み型ソリューションが必要とされています。世界人口の高齢化に伴い、ペースメーカー、神経刺激装置、整形外科用インプラント、その他の生命維持装置に対する需要が急増し続けています。高齢者層は、加齢に関連した病気や慢性疾患にかかりやすいため、市場拡大の大きな原動力となっています。

生体適合性材料、ワイヤレス技術、スマートインプラントなどの技術革新により、これらの機器の機能性と耐久性が向上しています。低侵襲手術の台頭や、長持ちするソリューションに対する患者の嗜好も採用を後押ししています。人工知能(AI)と医療モノのインターネット(IoMT)の統合が新たな成長の道を開いており、より良い患者管理のためのリアルタイムの健康モニタリングとデータ送信が可能な機器が登場しています。また、3Dプリンターによるインプラントも急増しており、より高度なカスタマイズと手術成績の向上が可能になっています。世界的にヘルスケア支出が増加し、次世代インプラントの規制承認が緩和される中、メーカーはより効率的で患者中心の機器を導入するための研究開発に注力しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,319億米ドル |

| 予測金額 | 3,068億米ドル |

| CAGR | 8.9% |

市場はさまざまなカテゴリーに区分されるが、中でも整形外科用機器は大幅な成長が見込まれます。整形外科分野はCAGR 5.7%で成長し、2034年には708億米ドルに達すると予測されます。骨粗鬆症、変形性関節症、骨折の増加により、整形外科用インプラントの需要が高まっています。特に股関節、膝関節、脊椎インプラントなどの人工関節置換術の増加が、市場の拡大をさらに加速させています。さらに、交通事故やスポーツ関連の災難による外傷の発生率の増加が、世界中で高度な整形外科ソリューションの採用を促進しています。

植込み型医療機器産業はまた、治療機器と診断機器に分けられます。治療目的で使用される機器を含む治療分野は、CAGR 8.8%で成長し、2034年には3,032億米ドルに達すると予測されています。糖尿病や心血管障害などの生活習慣病の増加により、革新的で耐久性のある埋め込み型ソリューションの需要が高まっています。これらの機器は、患者の転帰と生活の質を大幅に向上させるため、広く採用されるようになっています。

米国の植込み型医療機器市場は、2024年に548億米ドルと評価され、2025年から2034年にかけてCAGR 7.7%で拡大すると予想されています。同国は、ワイヤレス充電、小型化、AI駆動型インプラントの革新が業界に革命を起こすなど、技術進歩における世界的リーダーであり続けています。リアルタイムのデータとパーソナライズされた治療オプションを提供するスマートインプラントは、ヘルスケアプロバイダーの間で人気を集めています。さらに、3Dプリンティング技術は、個別化されたインプラントの製造に変革をもたらし、外科手術の精度を向上させています。継続的な研究開発投資と強固なヘルスケア・インフラにより、米国はインプラント医療機器イノベーションの最前線であり続ける態勢を整えています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 世界の慢性疾患の増加

- 臓器提供者の不足

- 先進国における技術進歩

- 先進諸国における埋め込み型医療機器に対する政府資金の増加

- マイクロエレクトロニクスと埋め込み型センサーの開発への注目の高まり

- 生体適合性と治療成績の向上を目的とした生体材料の採用増加

- 業界の潜在的リスク&課題

- 機器の高コスト

- 積極的植込み型医療機器に対する厳しい規制

- 処置後の合併症発生率の高さ

- 埋め込み型医療機器のリコール件数の多さ

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- ギャップ分析

- ポーター分析

- PESTEL分析

- 今後の市場動向

- バリューチェーン分析

- 植込み型医療機器のセキュリティの概要

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 整形外科

- 関節再建

- 脊椎器具

- 外傷固定器具

- その他の整形外科製品

- 心臓血管

- ステント

- 植込み型心臓除細動器(ICD)

- ペースメーカー

- 心臓再同期療法(CRT)

- 補助人工心臓

- 植込み型心臓モニター(ICM)

- その他の心臓血管関連製品

- 歯科

- クラウンおよびアバットメント

- 歯科インプラント

- その他の歯科製品

- 神経

- 脳深部刺激装置

- その他神経製品

- 眼科

- 眼内レンズおよび緑内障インプラント

- その他の眼科製品

- 形成外科

- 乳房インプラント

- 臀部インプラント

- その他の製品

第6章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 治療

- 診断用

第7章 市場予測:タイプ別市場推計・予測:デバイス別、2021年~2034年

- 主要動向

- スタティック/ノンアクティブ/パッシブ

- アクティブ

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- マルチスペシャリティセンター

- 診療所

- その他の最終用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Abbott

- Advanced Bionics

- Alcon

- Allergan

- BAUSCH+LOMB

- BIOTRONIK

- Boston Scientific

- Cochlear

- Demant

- GORE

- HENRY SCHEIN

- Johnson &Johnson

- MED-EL

- Medtronic

- MicroPort

- mindray

- POLYTECH

- smith &nephew

- stryker

- ZIMMER BIOMET

The Global Implantable Medical Devices Market was valued at USD 131.9 billion in 2024 and is projected to grow at a CAGR of 8.9% between 2025 and 2034. This growth is fueled by the increasing prevalence of chronic conditions such as cardiovascular diseases, neurological disorders, and orthopedic issues, all of which require advanced implantable solutions. As the global population ages, the demand for pacemakers, neurostimulators, orthopedic implants, and other life-enhancing devices continues to surge. The elderly demographic remains a significant driver of market expansion, given their higher susceptibility to age-related ailments and chronic conditions.

Technological advancements are further reshaping the implantable medical devices industry, with innovations in biocompatible materials, wireless technology, and smart implants enhancing the functionality and durability of these devices. The rise of minimally invasive procedures and patient preference for long-lasting solutions are also propelling adoption. The integration of artificial intelligence (AI) and the Internet of Medical Things (IoMT) is creating new growth avenues, with devices now capable of real-time health monitoring and data transmission for better patient management. The market is also seeing a surge in 3D-printed implants, allowing for greater customization and improved surgical outcomes. With healthcare spending increasing globally and regulatory approvals easing for next-generation implants, manufacturers are focusing on research and development to introduce more efficient and patient-centric devices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $131.9 Billion |

| Forecast Value | $ 306.8 Billion |

| CAGR | 8.9% |

The market is segmented into various categories, with orthopedic devices expected to witness substantial growth. The orthopedic segment is projected to grow at a CAGR of 5.7%, reaching USD 70.8 billion by 2034. Rising cases of osteoporosis, osteoarthritis, and fractures are contributing to the higher demand for orthopedic implants. The increasing number of joint replacement surgeries, particularly hip, knee, and spinal implants, is further accelerating market expansion. Additionally, the growing incidence of traumatic injuries due to road accidents and sports-related mishaps is driving the adoption of advanced orthopedic solutions worldwide.

The implantable medical devices industry is also divided into treatment and diagnostic devices. The treatment segment, which encompasses devices used for therapeutic purposes, is anticipated to grow at a CAGR of 8.8%, reaching USD 303.2 billion by 2034. The increasing prevalence of lifestyle-related diseases, such as diabetes and cardiovascular disorders, is driving demand for innovative and durable implantable solutions. These devices significantly enhance patient outcomes and quality of life, leading to widespread adoption.

U.S. Implantable Medical Devices Market, valued at USD 54.8 billion in 2024, is expected to expand at a CAGR of 7.7% from 2025 to 2034. The country remains a global leader in technological advancements, with innovations in wireless charging, miniaturization, and AI-driven implants revolutionizing the industry. Smart implants that provide real-time data and personalized treatment options are gaining traction among healthcare providers. Furthermore, 3D printing technology is transforming the production of personalized implants, improving precision in surgical procedures. With continuous R&D investments and a robust healthcare infrastructure, the U.S. is poised to remain at the forefront of implantable medical device innovations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of chronic diseases across the globe

- 3.2.1.2 Scarcity of organ donors

- 3.2.1.3 Technological advancement in developed nations

- 3.2.1.4 Rising government funding for implantable medical devices in developed countries

- 3.2.1.5 Increasing focus on the development of microelectronics and implantable sensors

- 3.2.1.6 Growing adoption of biomaterials for better biocompatibility and outcomes

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices

- 3.2.2.2 Stringent regulations for active implantable medical devices

- 3.2.2.3 Considerable rate of post-procedural complications

- 3.2.2.4 High number of recalls of implantable medical devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Value chain analysis

- 3.11 Overview on implantable medical device security

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Orthopedic

- 5.2.1 Joint reconstruction

- 5.2.2 Spinal devices

- 5.2.3 Trauma fixation devices

- 5.2.4 Other orthopedic products

- 5.3 Cardiovascular

- 5.3.1 Stents

- 5.3.2 Implantable cardiac defibrillators (ICDs)

- 5.3.3 Pacemaker

- 5.3.4 Cardiac resynchronization therapy (CRT)

- 5.3.5 Ventricular assist devices

- 5.3.6 Implantable cardiac monitors (ICM)

- 5.3.7 Other cardiovascular products

- 5.4 Dental

- 5.4.1 Dental crowns and abutment

- 5.4.2 Dental implants

- 5.4.3 Other dental products

- 5.5 Neurology

- 5.5.1 Deep brain stimulators

- 5.5.2 Other neurology products

- 5.6 Ophthalmology

- 5.6.1 Intraocular lenses and glaucoma implants

- 5.6.2 Other ophthalmology products

- 5.7 Plastic surgery

- 5.7.1 Breast implants

- 5.7.2 Gluteal implants

- 5.8 Other products

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Treatment

- 6.3 Diagnostic

Chapter 7 Market Estimates and Forecast, By Nature of Device, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Static/Non-active/Passive

- 7.3 Active

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Multi-specialty centers

- 8.5 Clinics

- 8.6 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott

- 10.2 Advanced Bionics

- 10.3 Alcon

- 10.4 Allergan

- 10.5 BAUSCH + LOMB

- 10.6 BIOTRONIK

- 10.7 Boston Scientific

- 10.8 Cochlear

- 10.9 Demant

- 10.10 GORE

- 10.11 HENRY SCHEIN

- 10.12 Johnson & Johnson

- 10.13 MED-EL

- 10.14 Medtronic

- 10.15 MicroPort

- 10.16 mindray

- 10.17 POLYTECH

- 10.18 smith & nephew

- 10.19 stryker

- 10.20 ZIMMER BIOMET