南米の電気自動車用電池製造:市場シェア分析、産業動向、成長予測(2025~2030年)

South America Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636473

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

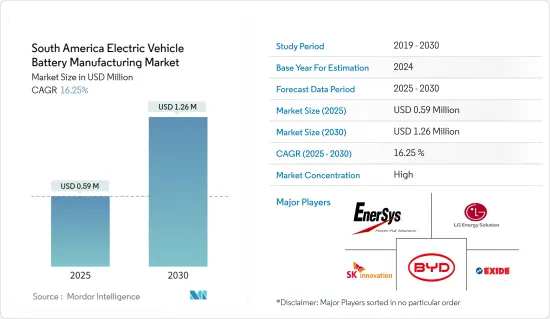

南米の電気自動車用電池製造市場規模は2025年に59万米ドルと推定され、予測期間(2025~2030年)のCAGRは16.25%で、2030年には126万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、同地域における電気自動車の普及拡大や豊富な原料などの要因が、予測期間中の南米の電気自動車用電池製造市場の最も重要な促進要因の1つになると予想されます。

- その一方で、アジア太平洋のような既存の電池市場が競合しています。これは予測期間中、南米の電気自動車用電池製造市場にとって脅威となります。

- 南米諸国間の協力関係やパートナーシップを構築するための継続的な努力は、将来的に市場にいくつかの機会を生み出すと予想されます。

- ブラジルは、電池製造の確立に向けた政府の取り組みが活発化していることと、電気自動車の普及が進んでいることから、市場を独占し、予測期間中に最も高い成長を記録すると予想されます。

南米の電気自動車用電池製造市場動向

リチウムイオン電池が著しい成長を遂げる

- リチウムイオン電池セグメントは、南米における電気自動車(EV)用電池製造市場の要であり、同地域の豊富な天然資源、進化する産業能力、持続可能性への取り組みの高まりがその原動力となっています。南米には、ブラジル、チリ、アルゼンチンを含む「リチウム・トライアングル」があり、これらの国々が世界のリチウム埋蔵量の大部分を占めています。

- 例えば、Energy Institute Statistical Review of World Energyは、2023年に南米のリチウム埋蔵量が7万1,030トンを超えると報告しています。これは2022年から22.82%の大幅な伸びを示し、世界的に最も急成長している地域のひとつに位置づけられています。特筆すべきは、2018~2023年にかけて、南米は38.1%以上のCAGRを誇り、この地域のリチウム埋蔵量と生産能力がエスカレートしていることを裏付けていることです。

- この戦略的優位性により、同地域はリチウムイオン電池の世界のサプライチェーンにおける重要な参入企業として位置づけられています。リチウムイオン電池は、エネルギー密度が高く、サイクル寿命が長く、自己放電率が比較的低いため、電気自動車の動力源として極めて重要です。リチウムの抽出と加工はますます高度化しており、南米諸国は抽出効率と環境の持続可能性を向上させる技術に投資しています。水の使用や採掘作業による環境への影響といった課題があるにもかかわらず、これらの問題を軽減するためのグリーン鉱業技術の進歩が模索されています。

- 2024年5月、Rio Tinto、Eramet、LG Energyは、チリのサラレス・アルトアンディノスで革新的なアプローチを提案しました。このイニシアチブは、単なる増産にとどまらず、リチウム採掘の環境への影響を再定義し、先駆的な持続可能性のベンチマークを確立することを目的としています。

- 直接リチウム抽出法(DLE)として知られるこの方法は、従来の手法からの顕著な飛躍を意味します。南米のリチウムが豊富な地域で一般的な、時間がかかり景観を支配する蒸発池とは異なり、DLE法は化学的、物理的、電気的プロセスを用いてかん水からリチウムを抽出します。これによって効率が高まるだけでなく、環境破壊も最小限に抑えられます。

- 同様に、ブラジルでは、原料の抽出だけでなく、電池セルの製造やリサイクル施設も含めた包括的な電池製造エコシステムの開発に向けた取り組みが進められており、電池の利用を中心とした循環型経済が形成されつつあります。リチウムの埋蔵量が多いアルゼンチンも、原料輸出から付加価値生産への移行を目指し、現地に電池製造施設を設立するための外国投資の誘致に力を入れています。

- こうした開発状況を踏まえると、リチウムイオン電池セクターは今後数年で大きく成長する可能性があります。

市場を独占するブラジル

- ブラジルは、戦略的、経済的、技術的な要因が重なり、南米の電気自動車(EV)用電池製造市場を独占する勢いです。南米最大の経済大国であるブラジルは、強固な産業基盤と確立された自動車産業を有しており、これらは電気自動車用電池製造に進出するための強固な基盤となっています。

- ブラジルの豊富な天然資源、特にニッケル、コバルト、リチウムなどの鉱物は、リチウムイオン電池の生産に不可欠であり、重要な原料の国内調達に大きな可能性を提供しています。ブラジルの地理的な位置と開発されたインフラは、大陸内の輸出入の物流ハブとしての可能性をさらに高め、効率的な物資の移動を促進し、国際貿易関係を促進します。

- さらに、ブラジル政府はサステイナブルエネルギーソリューションへの移行と二酸化炭素排出量の削減に向けた確固としたコミットメントを示しており、世界の動向と一致し、電気自動車販売と関連電池技術に対する国内市場の成長展望を強化しています。

- 国際エネルギー機関(IEA)によると、ブラジルの電気自動車販売台数は2023年に急増し、1万9,000台に達しました。これは、2022年から123.5%増という顕著な伸びを示しました。印象的なことに、過去5年間で販売台数は急増しており、100倍以上に成長しています。

- ブラジル政府は、再生可能エネルギーの開発と電気自動車の導入にインセンティブを与える施策を積極的に推進しており、その結果、国産電池の需要が刺激されています。減税、補助金、研究開発への投資といったイニシアチブは、国内外からの投資を電池製造部門に呼び込むためのものです。これらの施策措置は、ブラジルの広大な市場ポテンシャルと熟練労働力の活用を熱望する国際的な技術企業との提携によって補完されています。

- 例えば、BYDは2023年7月、ブラジルのFord工場跡地に3つの生産施設を建設する予定です。1つは電気自動車とハイブリッド車の生産用、1つは電気バスとトラックのシャーシ用、3つ目は電気自動車用電池市場向けにリチウムとリン酸鉄を加工する施設です。BYDは、ブラジルのバイーア州にあるカマカリ工業団地の敷地を転用するために、最大6億1,700万米ドルを投じる用意があります。

- このようなシナリオにより、予測期間中、ブラジルが市場を独占することが予想されます。

南米の電気自動車用電池製造産業概要

南米の電気自動車用電池製造市場は半固体化しています。この市場の主要企業(順不同)は、BYD、SK innovation、EnerSys、LG Chem Ltd、Exide Industriesです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の普及拡大

- 豊富な原料

- 抑制要因

- 既存市場との競合

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 電池

- リチウムイオン

- 鉛蓄電池

- ニッケル水素電池

- その他

- 電池形態

- 角型

- 袋型

- 円筒形

- 車両

- 乗用車

- 商用車

- その他

- 推進

- 電池電気自動車

- ハイブリッド電気自動車

- プラグインハイブリッド電気自動車

- 地域

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- BYD Co. Ltd

- SK innovation Co., Ltd.

- EnerSys

- LG Chem Ltd

- Exide Industries

- Panasonic Corporation

- その他の著名な企業一覧

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 地域コラボレーション

目次

Product Code: 50003740

The South America Electric Vehicle Battery Manufacturing Market size is estimated at USD 0.59 million in 2025, and is expected to reach USD 1.26 million by 2030, at a CAGR of 16.25% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the increasing adoption of electric vehicles in the region coupled with the abundance of raw materials in the region are expected to be among the most significant drivers for the South American electric Vehicle Battery Manufacturing Market during the forecast period.

- On the other hand, established battery markets such as Asia Pacific are competing. This poses a threat to the South American electric Vehicle Battery Manufacturing Market during the forecast period.

- Nevertheless, continued efforts to create collaborations and partnerships between South American countries are expected to create several opportunities for the market in the future.

- Brazil is expected to dominate the market and will likely register the highest growth during the forecast period due to the government's rising efforts to establish battery manufacturing and the growing adoption of electric vehicles.

South America Electric Vehicle Battery Manufacturing Market Trends

Lithium-ion Battery to Witness Significant Growth

- The lithium-ion battery segment is a cornerstone of the electric vehicle (EV) battery manufacturing market in South America, driven by the region's abundant natural resources, evolving industrial capabilities, and increasing commitment to sustainability. South America is home to the "Lithium Triangle," encompassing Brazil, Chile, and Argentina, which collectively hold over a significant share of the world's known lithium reserves.

- For instance, the Energy Institute Statistical Review of World Energy reported that South America's lithium reserves exceeded 71.03 thousand tonnes of lithium content in 2023. This marked a substantial growth of 22.82% from 2022, positioning it as one of the fastest-growing regions globally. Notably, from 2018 to 2023, South America boasted an impressive annual average growth rate of over 38.1%, underscoring the region's escalating lithium reserves and production capacity.

- This strategic advantage positions the region as a vital player in the global supply chain for lithium-ion batteries, which are pivotal in powering electric vehicles due to their high energy density, long cycle life, and relatively low self-discharge rates. The extraction and processing of lithium have become increasingly sophisticated, with South American countries investing in technology to improve extraction efficiency and environmental sustainability. Despite challenges such as water usage and the environmental impact of mining operations, advancements in green mining techniques are being explored to mitigate these issues.

- In May 2024, Rio Tinto, Eramet, and LG Energy proposed an innovative approach in Chile's Salares Altoandinos: a new lithium extraction technology. This initiative goes beyond mere production increases; it aims to redefine lithium mining's environmental impact, establishing pioneering sustainability benchmarks.

- Known as Direct Lithium Extraction (DLE), this method marks a notable leap from conventional practices. Unlike the slow and landscape-dominating evaporation ponds typical in South America's lithium-rich areas, DLE methods employ chemical, physical, or electrical processes to extract lithium from brine. This not only enhances efficiency but also minimizes environmental disturbances.

- Similarly, in Brazil, initiatives are underway to develop a comprehensive battery manufacturing ecosystem that includes not only raw material extraction but also the production of battery cells and recycling facilities, thus creating a circular economy around battery use. Argentina, with its significant lithium reserves, is also focusing on attracting foreign investment to establish local battery manufacturing facilities, aiming to move beyond raw material exportation to value-added production.

- Given these developments, the lithium-ion battery sector is poised for significant growth in the coming years.

Brazil to Dominate the Market

- Brazil is poised to dominate the South American electric vehicle (EV) battery manufacturing market due to a confluence of strategic, economic, and technological factors that favor its development as a regional powerhouse in this burgeoning sector. As the largest economy in South America, Brazil offers a robust industrial base and a well-established automotive industry, which collectively provide a solid foundation for expanding into electric vehicle battery manufacturing.

- Brazil's extensive natural resources, particularly minerals such as nickel, cobalt, and lithium, are crucial for lithium-ion battery production and offer significant potential for domestic sourcing of critical raw materials. Brazil's geographical location and developed infrastructure further enhance its potential as a logistical hub for both import and export within the continent, facilitating the efficient movement of goods and fostering international trade relationships.

- In addition, Brazil's government has demonstrated a solid commitment to transitioning toward sustainable energy solutions and reducing carbon emissions, aligning with global trends and reinforcing the domestic market's growth prospects for electric vehicle sales and related battery technologies.

- According to the International Energy Agency, Brazil witnessed a surge in electric vehicle sales in 2023, reaching 19,000 units. This marked a notable 123.5% increase from 2022. Impressively, over the last five years, sales have skyrocketed, growing by over 100 times, underscoring the escalating demand for electric vehicles in the nation.

- The Brazilian government is actively promoting policies to incentivize the development of renewable energy and the adoption of electric vehicles, which in turn is stimulating demand for locally manufactured batteries. Initiatives such as tax breaks, subsidies, and investment in research and development are designed to attract both domestic and foreign investment into the battery manufacturing sector. These policy measures are complemented by partnerships with international technology firms, which are eager to leverage Brazil's vast market potential and skilled labor force.

- For instance, in July 2023, BYD is planning to build three production facilities on a former Ford industrial site in Brazil: one for the production of electric and hybrid cars, one for chassis for electric buses and trucks, and a third that will process lithium and iron phosphate for the electric vehicle battery market. To convert the site in the Camacari industrial park in the Brazilian state of Bahia, BYD is ready to spend up to USD 617 million.

- Thus, such a scenario is expected to Brazil the dominating player in the market during the forecast period.

South America Electric Vehicle Battery Manufacturing Industry Overview

The South America Electric Vehicle Battery Manufacturing Market is semi-consolidated. Some of the key players in this market (in no particular order) are BYD Co. Ltd, SK innovation Co., Ltd., EnerSys, LG Chem Ltd, and Exide Industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Abundance of Raw Materials

- 4.5.2 Restraints

- 4.5.2.1 Competition From Established Markets

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Nickel Metal Hydride Battery

- 5.1.4 Others

- 5.2 Battery Form

- 5.2.1 Prismatic

- 5.2.2 Pouch

- 5.2.3 Cylindrical

- 5.3 Vehicle

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.3.3 Others

- 5.4 Propulsion

- 5.4.1 Battery Electric Vehicle

- 5.4.2 Hybrid Electric Vehicle

- 5.4.3 Plug-in Hybrid Electric Vehicle

- 5.5 Geography

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Colombia

- 5.5.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd

- 6.3.2 SK innovation Co., Ltd.

- 6.3.3 EnerSys

- 6.3.4 LG Chem Ltd

- 6.3.5 Exide Industries

- 6.3.6 Panasonic Corporation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Regional Collaboration

南米の電気自動車用電池製造:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日