北米の電気自動車用電池負極:市場シェア分析、産業動向、成長予測(2025~2030年)

North America Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636448

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

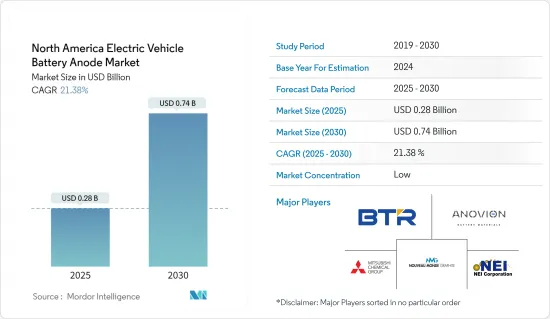

北米の電気自動車用電池負極市場規模は、2025年に2億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは21.38%で、2030年には7億4,000万米ドルに達すると予測されます。

主要ハイライト

- 予測期間中、電気自動車の普及拡大、政府の支援策、リチウムイオン電池の価格下落が市場の成長を後押しします。

- 逆に、電池部品の国内生産が限られているため、市場は課題に直面する可能性があります。

- しかし、現在進行中の負極材料と効率的な電解質の研究と進歩は、市場拡大の有望な機会をもたらします。

- 自動車セクターからの需要が増加している米国は、負極材料の用途拡大によって市場をリードすることになると考えられます。

北米の電気自動車用電池負極市場動向

リチウムイオン電池タイプが大きなシェアを占める見込み

- 歴史的に、リチウムイオン電池は携帯電話からパソコンに至るまで、民生用電子機器に電力を供給してきました。しかし、その役割は拡大し、北米ではハイブリッド車や完全電気自動車(EV)の電源として好まれるようになっています。この変化は主に、CO2や窒素酸化物などの温室効果ガスを排出しないEVの環境上の利点によるものです。

- 北米では、リチウムイオン電池は、その有利な容量対重量比により、他のタイプの電池を凌いで普及しています。リチウムイオン電池の採用は、優れた性能、長寿命、コストの低下によってさらに加速しています。高いエネルギー密度と長いサイクル寿命により、リチウムイオン電池はEVメーカーにとって最適な選択肢となっています。北米諸国がEV生産を拡大するにつれて、リチウムイオン技術に合わせた先進的製造装置への需要が高まり、電池負極材の需要を牽引しています。

- 北米におけるリチウムイオン電池の市場優位性の重要な要因は、価格の低下です。過去10年間、技術の進歩、規模の経済、洗練された製造プロセスにより、リチウムイオン電池のコストは大幅に低下しました。

- 2023年には、リチウムイオン電池パックの価格は前年比14%下落し、139米ドル/kWhとなります。電池価格の下落に伴い、EVはより手頃な価格となり、電気自動車の普及と市場シェアの拡大につながります。このような需要の急増は、負極を含む電池部品の消費量の増加を促し、電池性能を向上させるための技術進歩を促進します。

- 今後、同地域では負極材や正極材などのリチウムイオン電池製造部品の生産増強が重視されるため、リチウムイオン電池負極市場は予測期間中に成長すると予測されます。

- 例えば、2024年4月には、オーストラリアを拠点とするSicona Battery Technologiesが、米国南東部にシリコン-炭素負極材の初回生産施設を設立する予定です。シリコン-炭素負極は、電気自動車(EV)電池の製造にますます使用されるようになっています。従来のリチウムイオン電池は通常、黒鉛負極を使用しているが、シリコン-炭素負極は、特にエネルギー密度の点でいくつかの利点があります。同社は2030年までに、米国での生産量を年間2万6,500トンに拡大する計画です。

- このように、電気自動車におけるリチウムイオン電池の使用の増加と価格の低下により、リチウムイオン電池負極セグメントは予測期間中に大きく成長すると予想されます。

米国が市場を独占する見込み

- 近年、米国のEV用電池負極市場は、電気自動車の普及と最先端電池技術への需要の高まりに後押しされ、急速に拡大しています。

- 米国で電気自動車の販売が急増するにつれ、電池メーカーは国内生産への投資を増やし、EVバッテリー用負極の需要を押し上げています。国際エネルギー機関(IEA)の報告によると、米国の電気自動車販売台数は2023年に139万台に達し、2022年の99万台から顕著に増加しました。

- 政府の強力な支援を受けて、電池メーカーは米国に電気自動車(EV)用の新工場を設立しています。この拡大により、EVの生産に使用される材料、特に電池・アノードの需要が大幅に上昇することになります。例えば、米国エネルギー省は2024年1月、EV用電池と充電システムの研究開発を推進するプロジェクトに1億3,100万米ドルを割り当てた。

- 今後、EVの普及が進むにつれて、電池負極市場は、電池技術における国の研究開発努力に後押しされ、成長する態勢が整っています。特に、従来の黒鉛負極よりも高いエネルギー密度を約束する革新的なシリコン-炭素複合負極は、EVの航続距離を延ばすために極めて重要です。パナソニックやLG Energy Solutionのような大手企業は、Sila Nanotechnologiesのような新興企業とともに、負極の性能と安定性を高めるための研究開発に資源を投入しています。

- さらに、Nouveau Monde Graphiteは、カナダのケベック州で、急成長するリチウムイオン電池と燃料電池市場を対象に、カーボンニュートラル電池負極材の開発で先駆的な役割を果たしています。

- EVの普及と技術進歩の軌跡を考えると、予測期間中、米国が市場をリードすることになります。

北米の電気自動車用電池負極産業概要

北米の電気自動車用電池負極市場は半分裂状態です。同市場の主要企業(順不同)には、BTR New Material Group、Mitsubishi Chemical Group Corporation、Anovion LLC、Nouveau Monde Graphite Inc、NEI Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電池製造に向けた政府の施策と投資

- 電池原料コストの低下

- 抑制要因

- 電池部品の国内製造の制限

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 電池タイプ

- リチウムイオン

- 鉛-酸

- その他

- 材料

- リチウム

- 黒鉛

- シリコン

- その他

- 地域

- 米国

- カナダ

- その他の北米地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

BTR新材料グループ

- Anovion LLC

- Mitsubishi Chemical Group Corporation

- Nouveau Monde Graphite Inc

- NEI Corporation

- Targray Industries Inc.

- Nexeon Lid.

- LG Chem Ltd

- Tokai Carbon Co., Ltd.

- Nippon Carbon Co., Ltd.

- 市場ランキング分析

- その他の有力企業一覧

第7章 市場機会と今後の動向

- その他の電池化学の研究開発の増加

目次

The North America Electric Vehicle Battery Anode Market size is estimated at USD 0.28 billion in 2025, and is expected to reach USD 0.74 billion by 2030, at a CAGR of 21.38% during the forecast period (2025-2030).

Key Highlights

- In the forecast period, the market is poised for growth, driven by the rising adoption of electric vehicles, supportive government initiatives, and declining prices of lithium-ion batteries.

- Conversely, the market may face challenges due to the limited domestic manufacturing of battery components.

- However, ongoing research and advancements in anode materials and efficient electrolytes present promising opportunities for market expansion.

- With increasing demand from the automotive sector, the United States is set to lead the market, bolstered by its growing application of anode materials.

North America Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Type is Expected to Have a Major Share

- Historically, lithium-ion batteries powered consumer electronics, from mobile phones to personal computers. However, their role has expanded, becoming the preferred power source for hybrid and fully electric vehicles (EVs) in North America. This shift is primarily attributed to the environmental benefits of EVs, which produce no CO2, nitrogen oxides, or other greenhouse gases.

- In North America, lithium-ion batteries are outpacing other battery types in popularity due to their favorable capacity-to-weight ratio. Their adoption is further fueled by superior performance, extended shelf life, and declining costs. With high energy density and long cycle life, lithium-ion batteries have become the go-to choice for EV manufacturers. As countries in North America ramp up EV production, there's a growing demand for advanced manufacturing equipment tailored to lithium-ion technology, thereby driving the demand for battery anode material.

- A significant driver of lithium-ion batteries' market dominance in North America is their decreasing prices. Over the last decade, technological advancements, economies of scale, and refined manufacturing processes have led to a significant drop in lithium-ion battery costs.

- In 2023, the price of lithium-ion battery packs decreased by 14% compared to the previous year to USD139/kWh. As battery prices drop, EVs become more affordable, leading to increased adoption and a larger market share for electric vehicles. This surge in demand will drive higher consumption of battery components, including the anode, and encourage technological advancements to improve battery performance.

- In the future, due to the region's heightened emphasis on boosting the production of lithium-ion battery manufacturing components, such as anode and cathode materials, the market for lithium-ion battery anodes is projected to grow during the forecast period.

- For instance, in April 2024, Sicona Battery Technologies, based in Australia, is set to establish its inaugural production facility for silicon-carbon anode materials in the Southeastern United States. Silicon-carbon anodes are increasingly being used in the manufacturing of electric vehicle (EV) batteries. Traditional lithium-ion batteries typically use graphite anodes, but silicon-carbon anodes offer several advantages, particularly in terms of energy density. By 2030, the company plans to expand its U.S. production to a total output of 26,500 tons annually.

- Thus, owing to the increasing use of lithium-ion batteries in electric vehicles and decreasing prices, the lithium-ion battery anode segment is expected to grow significantly in the forecast period.

United States of America is Expected to Dominate the Market

- In recent years, the United States EV battery anode market has rapidly expanded, fueled by the rising adoption of electric vehicles and the demand for cutting-edge battery technologies.

- As electric vehicle sales surge in the United States, battery manufacturers are increasingly investing in domestic production, thereby driving up demand for EV battery anodes. The International Energy Agency reported that U.S. EV car sales reached 1.39 million units in 2023, a notable rise from 0.99 million in 2022.

- With strong government support, battery manufacturers are setting up new plants for electric vehicles (EVs) in the United States. This expansion is set to significantly elevate the demand for materials, especially battery anodes, used in EV production. For example, in January 2024, the U.S. Department of Energy allocated USD 131 million to projects aimed at advancing research and development in EV batteries and charging systems.

- Looking ahead, as EV adoption continues to rise, the battery anode market is poised for growth, bolstered by the nation's R&D efforts in battery technology. Notably, the innovative silicon-carbon composite anodes, which promise higher energy density than traditional graphite anodes, are pivotal for extending the EV range. Major players like Panasonic and LG Energy Solution, alongside newcomers like Sila Nanotechnologies, are pouring resources into R&D to boost anode performance and stability.

- Moreover, Nouveau Monde Graphite is pioneering the development of a carbon-neutral battery anode material in Quebec, Canada, targeting the burgeoning lithium-ion and fuel cell markets.

- Given the trajectory of EV adoption and technological advancements, the U.S. is poised to lead the market during the forecast period.

North America Electric Vehicle Battery Anode Industry Overview

The North America electric vehicle battery anode market is semi-fragmented. Some of the major players in the market (in no particular order) include BTR New Material Group Co., Ltd., Mitsubishi Chemical Group Corporation, Anovion LLC, Nouveau Monde Graphite Inc, and NEI Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Policies and Investments towards battery manufacturing

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 Limited Domestic Manufacturing of Battery Components

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Other Battery Types

- 5.2 Material

- 5.2.1 Lithium

- 5.2.2 Graphite

- 5.2.3 Silicon

- 5.2.4 Others

- 5.3 Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1

BTR New Material Group Co., Ltd

- 6.3.2 Anovion LLC

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 Nouveau Monde Graphite Inc

- 6.3.5 NEI Corporation

- 6.3.6 Targray Industries Inc.

- 6.3.7 Nexeon Lid.

- 6.3.8 LG Chem Ltd

- 6.3.9 Tokai Carbon Co., Ltd.

- 6.3.10 Nippon Carbon Co., Ltd.

- 6.4 Market Ranking Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Increasing Research and Development of Other Battery Chemistries

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日