|

市場調査レポート

商品コード

1636269

ASEAN諸国のプラグインハイブリッド電気自動車用電池:市場シェア分析、産業動向、成長予測(2025~2030年)ASEAN Countries Plug-in Hybrid Electric Vehicle Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ASEAN諸国のプラグインハイブリッド電気自動車用電池:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

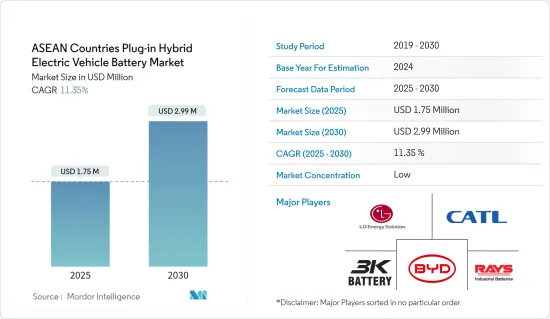

ASEAN諸国のプラグインハイブリッド電気自動車用電池市場規模は、2025年に175万米ドルと推定され、予測期間(2025~2030年)のCAGRは11.35%で、2030年には299万米ドルに達すると予測されます。

主要ハイライト

- 今後数年間、ASEAN諸国のプラグインハイブリッド電気自動車用電池市場は、電気自動車販売の急増とリチウムイオン電池のコスト低下により、大きな影響を受ける展望です。

- しかし市場は、特にプラグインハイブリッド電気自動車用電池の交換コストの高騰という逆風に直面しています。

- しかし、エネルギー容量の向上と航続距離の延長を目指した電池化学の進歩が続いており、市場には多くの機会がもたらされると期待されています。

- 今後数年間は、すべての国の中でインドネシアが市場を独占すると予想されます。

ASEAN諸国のプラグインハイブリッド電気自動車用電池市場動向

乗用車が成長を牽引

- 政府施策、環境問題、技術進歩のミックスに後押しされ、プラグインハイブリッド車(PHEV)電池市場の乗用車セグメントは、ASEAN(東南アジア諸国連合)諸国において顕著な成長を遂げています。

- 急速な都市化と中間層の急増に伴い、ASEAN諸国では自動車需要が急増しています。都市の混雑と汚染が深刻化するなか、各国政府は厳しい排ガス規制と電気自動車やハイブリッド車の導入を促進するインセンティブで対応しています。

- ASEAN Automotive Federationのデータによると、2023年の販売台数はインドネシアが77万9,326台でトップ、マレーシアが71万9,160台でこれに続きます。タイは40万6,501台と好調で、ベトナムは23万706台、フィリピンは11万1,980台です。シンガポールは3万2,511台、ミャンマーは2,832台です。こうした販売台数は、同地域で乗用車に対する購買意欲が高まっていることを裏付けています。

- 補助金、税金の割り戻し、充電インフラの整備など、政府の取り組みがASEAN全域でプラグインハイブリッド車の普及を後押ししています。さらに、地域間の協力や研究開発投資が、ASEANの自動車セグメントにおけるプラグインハイブリッド車用電池市場の重要性を確固たるものにしています。

- 国内のPHEV用電池生産を促進する動きとして、タイ政府は2023年11月に「EV3.5」補助金プログラムを導入しました。これは、2024~2027年まで有効で、生産される電池1台あたり最大2,760米ドルの補助金を提供するものです。

- 主要目的は2つあり、外国からの投資を誘致することと、東南アジアのプラグインハイブリッド車用電池製造の中心的存在としてのタイの地位を確立することです。現在、中国のプラグインハイブリッド車ブランドが優位を占めており、欧州勢の関心も高まっていることから、この戦略的な動きは、急速に進化するプラグインハイブリッド車用電池セクターにおけるタイの軌道を再定義するものです。

- 電池技術の進歩は、ASEANのプラグインハイブリッド車市場を決定的に形成しています。特にリチウムイオン電池の技術革新は、エネルギー密度を高め、ライフサイクルを延ばし、急速充電を可能にすることで、プラグインハイブリッド車の魅力を高めています。

- こうした動きを踏まえると、乗用車セグメントは今後数年間で成長する可能性があります。

インドネシアが市場を独占する展望

- 政府施策、経済成長、消費者行動、技術進歩などの要因に後押しされ、ASEANプラグインハイブリッド車(PHEV)電池市場のインドネシアセグメントは顕著な変貌を遂げつつあります。東南アジア最大の経済大国であるインドネシアの急成長する自動車市場は、プラグインハイブリッド電気自動車セクターにとって大きな可能性を秘めています。

- インドネシア政府は、施策やイニシアティブを通じて、二酸化炭素排出量の削減とサステイナブル輸送の推進に積極的に取り組んでいます。税制優遇措置、補助金、重要なのは充電インフラの開発など、こうした取り組みは、プラグインハイブリッド電気自動車に一般的に関連する高い初期費用を軽減することを目的としています。

- インドネシア工業省は、電動二輪車を含む電気自動車やハイブリッド車に対する購入補助金を打ち出しています。さらに、従来の内燃機関二輪車を電気二輪車に改造するための補助金も出そうとしています。電池式電気自動車の新規購入には5,130米ドルの補助金が支給されるが、従来のハイブリッド車にはその半額の補助金が支給されます。

- 過去10年間で、電池技術と製造における飛躍的な進歩が、インドネシアのハイブリッド電気自動車におけるリチウムイオン電池の採用を加速させました。こうした進歩により、コスト削減だけでなく性能と信頼性も向上し、リチウムイオン電池はメーカーと消費者の双方にとって好ましい選択肢となっています。

- 最近、リチウムイオン電池とセルパックの価格は下落傾向にあり、エンドユーザー産業にアピールしています。2022年にわずかに上昇した後、2023年には価格下落が再開し、リチウムイオン電池パックは歴史的安値の139米ドル/kWhを記録し、14%の下落を示しました。

- さらに、プラグインハイブリッド電気自動車用電池の現地製造施設の台頭は、製造コストを押し下げる構えです。その結果、プラグインハイブリッド電気自動車は消費者にとってより身近なものになると考えられます。政府の奨励策や技術的進歩も相まって、手頃な価格でサステイナブル輸送手段へのこの経済的軸足は、インドネシアのプラグインハイブリッド電気自動車市場の大幅な成長に拍車をかけることになります。

- 例えば、2023年6月、インドネシアはHapco Neta、Wuling、Chery、Xiaokangの中国の著名な自動車メーカー4社と重要な合意に調印し、インドネシアを潜在的な電気自動車輸出ハブに位置づけた。Chery Automobileとの協議では、プラグインハイブリッド電気自動車(PHEV)を国内で製造するための調査の道を探るという明確な意図があります。従来のハイブリッド車よりも燃費が向上したプラグインハイブリッド電気自動車は、中国ではすでに人気があります。奇瑞は野心的な計画を持っており、2030年までに10万台の電気自動車の展開を目標としています。

- こうした新興国市場の開拓を踏まえると、インドネシアは今後数年で市場をリードする態勢を整えています。

ASEAN諸国のプラグインハイブリッド電気自動車用電池産業概要

ASEAN諸国のプラグインハイブリッド電気自動車用電池市場は半分断構造です。この市場の主要企業(順不同)には、LG Energy Solution、Contemporary Amperex Technology、BYD Company、HDS Global Pte Ltd、3K Batteryなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車販売の成長

- リチウムイオン電池の価格低下

- 抑制要因

- 高い電池交換コスト

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 電池タイプ

- リチウムイオン電池

- 鉛蓄電池

- ナトリウムイオン電池

- その他

- 車種

- 乗用車

- 商用車

- 地域

- シンガポール

- フィリピン

- ベトナム

- タイ

- マレーシア

- インドネシア

- その他のASEAN諸国

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- LG Energy Solution

- Contemporary Amperex Technology Co Ltd.

- BYD Company

- Panasonic Holdings Corporation

- Toshiba Corporation

- Enersys Sarl

- Exide Industries Ltd

- HDS Global Pte Ltd

- 3K Battery

- Clarios, LLC

- その他の著名な企業一覧

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 新しい電池化学の研究開発の継続

The ASEAN Countries Plug-in Hybrid Electric Vehicle Battery Market size is estimated at USD 1.75 million in 2025, and is expected to reach USD 2.99 million by 2030, at a CAGR of 11.35% during the forecast period (2025-2030).

Key Highlights

- In the coming years, the ASEAN Countries Plug-in Hybrid Electric Vehicle Battery Market is poised to be significantly influenced by surging electric vehicle sales and the plummeting costs of lithium-ion batteries.

- However, the market faces headwinds, notably from the steep replacement costs associated with plug-in hybrid electric vehicle batteries.

- Yet, ongoing advancements in battery chemistries, aimed at enhancing energy capacity and extending driving range, promise to unlock numerous opportunities for the market.

- Among all the countries, Indonesia is expected to dominate the market during the upcoming years.

ASEAN Countries Plug-in Hybrid Electric Vehicle Battery Market Trends

Passenger Vehicles to Witness Growth

- Driven by a mix of government policies, environmental concerns, and technological advancements, the passenger vehicle segment of the plug-in hybrid electric vehicle (PHEV) battery market is experiencing notable growth in ASEAN (Association of Southeast Asian Nations) countries.

- With rapid urbanization and a burgeoning middle class, ASEAN nations are witnessing a surge in vehicle demand. As urban congestion and pollution escalate, governments are responding with stringent emission regulations and incentives to promote electric and hybrid vehicle adoption.

- Data from the ASEAN Automotive Federation highlights Indonesia's lead in 2023 with 779,326 units sold, trailed by Malaysia at 719,160 units. Thailand's market stands robust at 406,501 units, while Vietnam and the Philippines report 230,706 and 111,980 units, respectively. Singapore and Myanmar round out the figures with 32,511 and 2,832 units. Such sales figures underscore the growing appetite for passenger vehicles in the region.

- Government initiatives, including subsidies, tax rebates, and charging infrastructure development, are propelling the adoption of plug-in hybrid vehicles across ASEAN. Furthermore, regional collaborations and R&D investments are solidifying the plug-in hybrid vehicle battery market's significance in the ASEAN automotive arena.

- In a move to boost domestic PHEV battery production, the Thai government, in November 2023, introduced the "EV3.5" subsidy program. This initiative offers a subsidy of up to USD 2,760 per battery produced, valid from 2024 to 2027.

- The primary objective is two fold: to entice foreign investments and cement Thailand's stature as a pivotal player in the Southeast Asian plug-in hybrid vehicle battery manufacturing landscape. Given the current dominance of Chinese plug-in hybrid vehicle brands and the growing interest from European counterparts, this strategic move is poised to redefine Thailand's trajectory in the swiftly evolving plug-in hybrid vehicle battery sector.

- Battery technology advancements are crucially shaping the plug-in hybrid vehicle market in ASEAN. Innovations, especially in lithium-ion batteries, are boosting energy density, extending life cycles, and enabling faster charging, thereby enhancing the allure of plug-in hybrids.

- Given these dynamics, the passenger vehicle segment is poised for growth in the coming years.

Indonesia is Expected to Dominate the Market

- Driven by factors such as government policies, economic growth, consumer behavior, and technological advancements, the Indonesian segment of the ASEAN plug-in hybrid electric vehicle (PHEV) battery market is undergoing a notable transformation. As Southeast Asia's largest economy, Indonesia's burgeoning automotive market holds immense promise for the plug-in hybrid electric vehicle sector.

- Through policies and initiatives, the Indonesian government is actively working to reduce carbon emissions and champion sustainable transportation. These efforts, including tax incentives, subsidies, and crucially, the development of charging infrastructure, aim to alleviate the higher upfront costs typically associated with plug-in hybrid electric vehicles.

- The Indonesian Ministry of Industry has rolled out purchase subsidies for electric and hybrid vehicles, including electric motorbikes. Furthermore, there's a push to subsidize converting traditional combustion-engine motorbikes to electric. New battery-electric vehicle purchases can benefit from a generous subsidy of USD 5,130, while conventional hybrids enjoy a subsidy that's half that amount.

- Over the past decade, breakthroughs in battery technology and manufacturing have accelerated the adoption of lithium-ion batteries in Indonesia's hybrid electric vehicle landscape. These advancements have not only reduced costs but also enhanced performance and reliability, making lithium-ion batteries a favored choice for both manufacturers and consumers.

- Recently, lithium-ion battery and cell pack prices have been on a downward trajectory, appealing to end-user industries. After a minor uptick in 2022, prices resumed their decline in 2023, with lithium-ion battery packs hitting a historic low at USD 139/kWh, marking a 14% decrease.

- Moreover, the rise of local manufacturing facilities for plug-in hybrid electric vehicle batteries is poised to drive down production costs. This, in turn, is set to make plug-in hybrid electric vehicles more accessible to consumers. Coupled with government incentives and technological strides, this economic pivot towards affordable and sustainable transportation is primed to spur substantial growth in Indonesia's plug-in hybrid electric vehicle market.

- For example, in June 2023, Indonesia sealed a significant agreement with four prominent Chinese automakers - Hapco Neta, Wuling, Chery, and Xiaokang - positioning Indonesia as a potential electric vehicle export hub. In talks with Chery Automobile, there's a clear intent to explore research avenues for manufacturing plug-in hybrid electric vehicles (PHEVs) domestically. Given their enhanced fuel efficiency over traditional hybrids, plug-in hybrid electric vehicles are already popular in China. Chery has ambitious plans, targeting a rollout of 100,000 electric vehicles by 2030.

- Given these developments, Indonesia is poised to lead the market in the coming years.

ASEAN Countries Plug-in Hybrid Electric Vehicle Battery Industry Overview

The ASEAN Countries Plug-in Plug-in Hybrid Electric Vehicle Battery Market is semi-fragmented. Some of the key players in this market (in no particular order) are LG Energy Solution, Contemporary Amperex Technology Co Ltd., BYD Company, HDS Global Pte Ltd, and 3K Battery

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Decreasing Lithium-ion Battery Price

- 4.5.2 Restraints

- 4.5.2.1 High Battery Replacment Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Sodium-ion Battery

- 5.1.4 Others

- 5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 Geography

- 5.3.1 Singapore

- 5.3.2 Philippines

- 5.3.3 Vietnam

- 5.3.4 Thailand

- 5.3.5 Malaysia

- 5.3.6 Indonesia

- 5.3.7 Rest of ASEAN Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 LG Energy Solution

- 6.3.2 Contemporary Amperex Technology Co Ltd.

- 6.3.3 BYD Company

- 6.3.4 Panasonic Holdings Corporation

- 6.3.5 Toshiba Corporation

- 6.3.6 Enersys Sarl

- 6.3.7 Exide Industries Ltd

- 6.3.8 HDS Global Pte Ltd

- 6.3.9 3K Battery

- 6.3.10 Clarios, LLC

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Continued Research and Development In New Battery Chemistries