北米の不動産仲介:市場シェア分析、産業動向、成長予測(2025年~2030年)

North America Real Estate Brokerage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636189

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

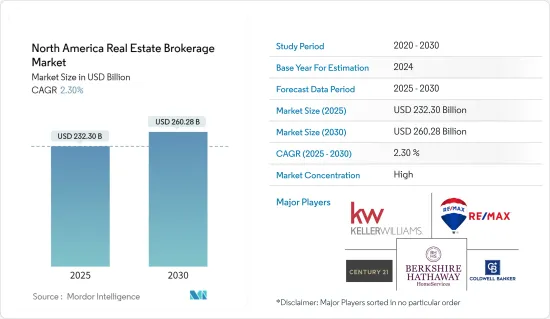

北米の不動産仲介市場規模は2025年に2,323億米ドルと推定され、予測期間(2025~2030年)のCAGRは2.3%で、2030年には2,602億8,000万米ドルに達すると予測されます。

主要ハイライト

- 北米の不動産仲介市場は、主に都市化と住宅用不動産需要の増加が牽引しています。

- 同地域の人口拡大が住宅とインフラの必要性を煽り、不動産市場を後押ししています。人口の増加に伴い、住宅、商業施設、オフィススペースなど、さまざまなインフラに対する需要が顕著に急増しています。

- この急増は、不動産開発業者や投資家にとって有利な機会となります。このような人口動態の変化を理解することで、不動産利害関係者は、投資、物件タイプ、地域の需要に対応するためのカスタマイズ提供について、戦略的な意思決定を行うことができます。国勢調査局によると、米国の人口は2080年までに約3億7,000万人でピークを迎え、その後徐々に減少して2100年には約3億6,600万人になると予測されています。

- 国勢調査局の人口時計によると、米国は中国とインドに次いで世界で3番目に人口の多い国です。インドネシアとパキスタンが上位5を占めます。従って、都市化が進むにつれ、仲介市場は大きく成長する態勢にあります。

- 弱含みの集合住宅市場では、価格が最大6%下落すると予想されます。しかし、新規開発が大幅に減少し、建設リードタイムが長くなっているため、2025年後半までには力強い回復が実現する可能性があります。工業用不動産の価格は底堅く推移すると考えられます。特に中西部、東海岸、メキシコ湾岸の各州では、総額33億米ドルに上る新たな連邦補助金がインフラ強化の起爆剤となり、工業・物流セクターを後押ししています。

- オフィス価格は、2024年には7~10%の下落が予測されるもの、安定化に向かっています。その後、プライム物件とセカンダリー物件の間に顕著なパフォーマンスの乖離が生じることが予想されます。小売セクターでは、ストリップ小売の供給不足が楽観的な見方を助長している一方で、貯蓄の減少やクレジットカード債務の増大が懸念され、個人消費が抑制される可能性があります。

北米の不動産仲介市場の動向

産業用賃貸の成長は、力学が変化する中で課題に直面

2023年、産業用賃貸の成長軌道は、いくつかの大型物件の竣工により課題に直面すると予測されました。典型的な10万平方フィート以下の小規模物件は需要が高まり、1桁台の堅調な賃料成長が予測されました。

全体的な動向としては、小規模な工業用地が有利な傾向にあるが、特に大規模な工業用地がある特定のサブマーケットにおいては、顕著な例外があります。例えば、ヒューストン港から車で15分以内の地域です。これらの地域は、西海岸から東海岸やメキシコ湾岸への交通の転換のおかげで、需要が急増しています。この周辺には10万平方フィートを超える工業用地が80件以上あるが、現在賃貸可能なのは1件のみです。さらに、すぐに利用できるスペースが乏しいため、ターミナルに近いテキサス州ベイタウンの工業開発が促進されようとしています。

地上貨物のインフラ整備が進むにつれ、インターモーダルターミナルがある市場では需要の急増が予想されます。これは特に、新設された貨物鉄道の沿線や、陸上国境に近い新興の貿易回廊に戦略的に位置するターミナルに当てはまる。東海岸とメキシコ湾岸の港湾では労使交渉が進行中であるが、中国からのリショアリングという広範な動向は、東海岸の港湾を通じて最適な支援を見出すと予想されます。

住宅ローン金利上昇にもかかわらず米国住宅価格は過去最高を記録

2024年4月、S&P CoreLogic Case-Shiller Home Price Indexは年率6.3%上昇し、3月の6.5%を若干下回ったもの、依然として過去最高を記録しました。FRBの利下げが住宅市場を押し上げる可能性があると推測する専門家もいるが、実際の時期や確率は依然不透明です。

しかし、新築住宅については話が違う。住宅ローン金利が上昇し、5月には7%を超えるものもあったため、米国の新築一戸建ての販売は苦戦を強いられました。米国国勢調査局とHUDのデータによると、4月比で11.7%減、2022年比で16.5%減と大幅に落ち込みました。

しかし、購入者にとっては明るい兆しもあります。販売件数の落ち込みにより、新築住宅の在庫は2008年初頭以来の水準に達し、買い手はより有利になりました。中古住宅の売り手は、クロージング費用の負担や修繕費の負担など、譲歩案を提示して対応しています。

さらに、2024年5月の新築住宅価格の中央値は500米ドル下落し41万7,400米ドルとなり、中古住宅の中央値を2,000米ドル近く下回りました。

北米の不動産仲介産業概要

北米の不動産仲介市場は活気に満ちており、多様な参入企業が市場の覇権を争っているのが特徴です。先頭を走るのは、Keller Williams Realty、RE/MAX、Coldwell Banker Real Estate、Berkshire Hathaway HomeServices、Century 21 Real Estateといった大手です。これらの産業大手は、主に広範なエージェントネットワークとオフィスセットアップを通じて機能し、住宅と商業用不動産の両方の取引に対応しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場力学

- 促進要因

- 市場を牽引する都市化の進展

- 市場を牽引する規制環境

- 抑制要因

- 市場の飽和が市場抑制要因要因

- 金利変動が市場を抑制

- 機会

- 技術の進歩

- 促進要因

- バリューチェーン/サプライチェーン分析

- 政府の規制、貿易協定、イニシアチブ

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響

第5章 市場セグメンテーション

- タイプ別

- 住宅用

- 非住宅用

- サービス別

- 販売

- レンタル

- 地域別

- 米国

- カナダ

- メキシコ

第6章 競合情勢

- 市場集中度概要

- 企業プロファイル

- Keller Williams Realty

- RE/MAX

- Coldwell Banker Real Estate

- Berkshire Hathaway HomeServices

- Century 21 Real Estate

- Sotheby's International Realty

- ERA Real Estate

- Corcoran Group

- Compass

- Douglas Elliman Real Estate*

- その他の企業

第7章 市場の将来

第8章 付録

目次

The North America Real Estate Brokerage Market size is estimated at USD 232.30 billion in 2025, and is expected to reach USD 260.28 billion by 2030, at a CAGR of 2.3% during the forecast period (2025-2030).

Key Highlights

- The North American real estate brokerage market is mainly driven by urbanization and the increasing demand for residential real estate.

- The region's expanding population is fueling the need for housing and infrastructure, propelling the real estate market. With the population on the rise, the demand for various infrastructures, including residential, commercial, and office spaces, is witnessing a notable surge.

- This surge presents a lucrative opportunity for real estate developers and investors. Understanding these demographic shifts empowers real estate stakeholders to make strategic decisions on investments, property types, and customized offerings to cater to the local demand. According to the Census Bureau, the US population is forecasted to peak at nearly 370 million by 2080 before gradually declining to around 366 million by 2100.

- The United States ranks as the world's third most populous nation, trailing only China and India, as per the Census Bureau's Population Clock. Indonesia and Pakistan complete the top five. Consequently, as urbanization intensifies, the brokerage market is poised for significant growth.

- In weaker multifamily markets, prices are anticipated to drop by up to 6%. However, with a significant reduction in new developments and the lengthy construction lead times, a robust recovery could materialize by late 2025. Industrial prices are likely to hold steady. Notably, new federal grants totaling USD 3.3 billion are catalyzing infrastructure enhancements, particularly in the Midwest, East Coast, and Gulf Coast states, bolstering the industrial and logistics sectors.

- Office prices are on the brink of stabilizing, even though a 7-10% decline is projected for 2024. Following this, it is anticipated that there will be a notable performance divergence between prime and secondary assets. While the retail sector is witnessing a scarcity in strip retail supply, which is fostering optimism, concerns loom over declining savings and escalating credit card debt, potentially curbing consumer spending.

North America Real Estate Brokerage Market Trends

Industrial Rental Growth Faces Challenges Amidst Changing Dynamics

In 2023, the industrial rental growth trajectory was projected to face challenges due to the completion of several big-box properties. Smaller properties, typically under 100,000 square feet, were poised for heightened demand, with robust single-digit rental growth projections.

While the broader trend leans toward the favor of smaller industrial properties, there are notable exceptions, especially in select sub-markets with larger industrial offerings. Take, for instance, areas within a 15-minute drive of Port Houston. These locales have seen a surge in demand, thanks to the redirection of traffic from the West Coast to the East and Gulf Coasts. There are over 80 industrial properties exceeding 100,000 square feet in this vicinity, yet only one is currently available for lease. Moreover, the scarcity of immediately available space is poised to bolster the industrial development in Baytown, Texas, close to the terminal.

As the ground freight infrastructure receives a boost in support, markets with intermodal terminals are expected to witness a surge in demand. This is especially true for those strategically positioned along newly established freight rail lines and emerging trade corridors near land borders. Despite ongoing labor negotiations at ports along the East and Gulf Coasts, the broader trend of reshoring, moving away from China, is expected to find its optimal support through the East Coast ports.

US Home Prices Hit Record High Despite Rising Mortgage Rates

In April 2024, the S&P CoreLogic Case-Shiller Home Price Index revealed a 6.3% annual gain, slightly lower than March's 6.5% but still marking a new peak. While some experts speculate a potential Fed rate cut might boost the housing market, the actual timing and probability of such a move remain uncertain.

However, the story is different for new homes. As mortgage rates climbed, with some surpassing 7% in May, sales of newly constructed single-family homes in the United States suffered. Data from the US Census Bureau and HUD showed an 11.7% drop from April and a substantial 16.5% decline from 2022.

But there is a silver lining for buyers. The dip in sales has led to new home inventories reaching levels not seen since early 2008, giving buyers more leverage. Sellers of existing homes are responding by offering concessions, like covering closing costs and chipping in for repairs.

Moreover, for those considering new builds, the median price for a new home in May 2024 fell by USD 500 to USD 417,400, almost USD 2,000 below the median price of existing homes.

North America Real Estate Brokerage Industry Overview

The North American real estate brokerage market is vibrant, characterized by a diverse array of players vying for market dominance. Leading the pack are stalwarts such as Keller Williams Realty, RE/MAX, Coldwell Banker Real Estate, Berkshire Hathaway HomeServices, and Century 21 Real Estate. These industry giants predominantly function through extensive agent networks and office setups, catering to both residential and commercial property transactions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increasing Urbanization Driving the Market

- 4.2.1.2 Regulatory Environment Driving the Market

- 4.2.2 Restraints

- 4.2.2.1 Market Saturation Restraining the Market

- 4.2.2.2 Intrest Rate Fluctuations Restraining the Market

- 4.2.3 Opportunities

- 4.2.3.1 Technological Advancements

- 4.2.1 Drivers

- 4.3 Value Chain/Supply Chain Analysis

- 4.4 Government Regulations, Trade Agreements, and Initiatives

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Residential

- 5.1.2 Non-Residential

- 5.2 By Service

- 5.2.1 Sales

- 5.2.2 Rental

- 5.3 By Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Keller Williams Realty

- 6.2.2 RE/MAX

- 6.2.3 Coldwell Banker Real Estate

- 6.2.4 Berkshire Hathaway HomeServices

- 6.2.5 Century 21 Real Estate

- 6.2.6 Sotheby's International Realty

- 6.2.7 ERA Real Estate

- 6.2.8 Corcoran Group

- 6.2.9 Compass

- 6.2.10 Douglas Elliman Real Estate*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日