アジア太平洋の不動産仲介-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Asia-Pacific Real Estate Brokerage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636190

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

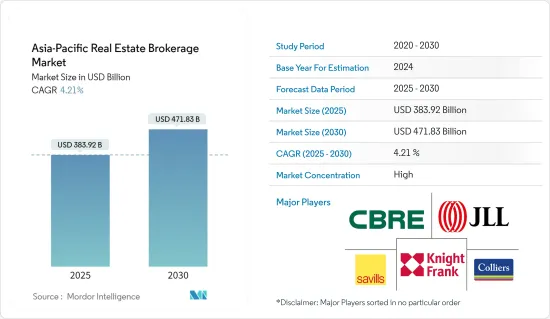

アジア太平洋の不動産仲介市場規模は2025年に3,839億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.21%で、2030年には4,718億3,000万米ドルに達すると予測されます。

主要ハイライト

- アジア太平洋の不動産仲介市場は、主に都市化と外国投資の急増によって牽引されています。同地域では、都市化が依然として支配的なメガ動向となっています。アジアは世界の都市人口の半分以上を抱え、その数は22億人を超えます。予測によると、2050年までにアジアの都市人口は50%増加し、さらに12億人の人口が増加します。

- アジア太平洋全域の都市は、世界経済の機会や持続可能性への取り組みを担っています。環境の悪化、災害の深刻化、スラムの存続、社会的排除といった課題に取り組む一方で、経済大国、イノベーションの中心地、文化遺産保護のチャンピオンとしての役割も果たしています。

- 現在、アジア太平洋の投資家のポートフォリオのうち、オフィスと店舗用不動産が3分の1を占め、大きな比重を占めています。しかし、この状況は大きく変わろうとしています。ホテルや小売業に代表されるサービス業がCOVID-19の大流行で打撃を受けた一方で、産業用不動産、特に物流センターや配送センターはすぐに回復し、成長を目の当たりにしました。その結果、不動産の資産配分が小売業から産業用不動産に傾き、顕著な軸足となっています。

- 歴史的に、オフィス用不動産は高い空室率に悩まされてきたため、住宅用不動産に軸足を移す動きもあった。しかし、2024年に向けては、特にオフィスの賃貸料が上昇すると予測されている大都市中心部では、楽観的な見方もあります。

- 投資家の視線は、ニッチな不動産セグメントに向けられつつあります。特にデータセンターは大きな注目を集めています。特に東京と上海は、アジア太平洋のデータセンター実稼働数のリーダーです。不動産市場のもう一つの新星はライフサイエンスセグメントで、多様な医療施設や不動産を網羅しています。

アジア太平洋の不動産仲介市場の動向

住宅需要が市場を牽引

- インドでは、Delhi NCRが2024年第1四半期に5,109戸の高級住宅を販売し、過去最高を記録しました。販売戸数はグルガオンが全体の79%を占め、圧倒的に多かった。Gurgaonにドワルカ高速道路が完成したことが、この需要の高まりを後押しする上で極めて重要な役割を果たし、その影響は市内の主要な通路全体に及びました。

- Gurgaonの新規立ち上げ物件は圧倒的な需要に見舞われ、ほとんどのプロジェクトが数日で完売しました。特に、DLFのセクター77プロジェクトはプレローンチから2日で満室となり、Signature Globalのセクター37Dプロジェクトはプレローンチ段階で5.4倍の申し込み超過となりました。ノイダとデリーもハイエンドの販売状況に大きく貢献しました。

- バンコクでは、最近の発売物件のプレセールスが50%を超えていることからわかるように、市場心理が上昇しています。全体的な売上は顕著に上昇し、20ベーシスポイント上昇しました。特筆すべきは、当四半期に2つのプロジェクトが完売を達成し、売れ残り率が3.2%まで低下したことです。

- 外国人バイヤーの流入が増加しており、地元バイヤーの限られた購買力を相殺するのに役立っています。第1四半期の観光客や外国人旅行者の増加(前年同期比12%増)により、賃貸需要が回復しています。様々なプロジェクトでジュニットの改修が完了したため、2024年の空室率は5.0%に上昇したが、賃貸需要が堅調であることから、この伸びは一過性のものと見られています。

インドが不動産需要の高まりで有力な参入企業に浮上

- ムンバイでは、広々とした住宅を求める住宅購入者の嗜好により、ハイエンドカテゴリーの販売が新たなピークに達しました。特に、実業家、富裕層、C-suite、芸能人などが、Malabar Hill、Worli、Bandraなどの一等地にある高額マンションに引き寄せられました。

- 高級マンション販売ではThaneが21.8%のシェアを占め、Western Suburbs IIとNavi Mumbaiが僅差で続きました。South Central MumbaiとWestern Suburbs IIは、前例のない売上急増を記録しました。Prime SouthのMICL Aaradhya AvaanやEastern SuburbsのGodrej Vistasなど、注目すべき新発売がこれらの売上をさらに押し上げました。

- チェンナイの高級住宅セクターは、前四半期比141%増という目覚しい売上急増を記録し、セントラルとオフ・セントラル・サブマーケットに位置するキルパウク、コットゥルプラム、ヴァダパラニといったホットスポットが活発な動きを見せた。チェンナイ市の総販売戸数も前年比25%増となりました。チェンナイの高級住宅市場のこのような高騰は、目の肥えた顧客層と共鳴する特注品、世界のデザイン美学、最高級の設備に対する需要の高まりに起因しています。

アジア太平洋の不動産仲介産業概要

アジア太平洋の不動産仲介市場は細分化されています。ローカル、リージョナル、世界の参加者が混在しています。しかし、市場の集中度は国間だけでなく、都市内でも著しく異なります。この集中を形成する要因には、仲介会社の数、市場シェア、競合情勢、規制状況、技術の進歩などが含まれます。

市場の主要企業としては、CBRE Group、JLL、Colliers International、Knight Frank、Savillsなどが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場力学

- 促進要因

- 市場を牽引する都市化の進展

- 市場を牽引する規制環境

- 抑制要因

- 市場の飽和が市場抑制要因要因

- 金利変動が市場を抑制

- 機会

- 市場を牽引する技術の進歩

- 促進要因

- バリューチェーン/サプライチェーン分析

- 政府の規制、貿易協定、イニシアチブ

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響

第5章 市場セグメンテーション

- タイプ別

- 住宅用

- 非住宅用

- サービス別

- 販売

- レンタル

- 地域別

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- その他のアジア太平洋

第6章 競合情勢

- 市場集中概要

- 企業プロファイル

- CBRE Group

- JLL

- Colliers International

- Knight Frank

- Savills

- Cushman & Wakefield

- Century 21 Real Estate

- ERA Real Estate

- RE/MAX

- Coldwell Banker*

- その他の企業

第7章 市場の将来

第8章 付録

目次

The Asia-Pacific Real Estate Brokerage Market size is estimated at USD 383.92 billion in 2025, and is expected to reach USD 471.83 billion by 2030, at a CAGR of 4.21% during the forecast period (2025-2030).

Key Highlights

- The real estate brokerage market in Asia-Pacific is mainly driven by a surge in urbanization and foreign investment. Urbanization remains a dominant megatrend in the region. Asia hosts over half of the world's urban population, exceeding 2.2 billion people. Projections indicate that by 2050, Asia's urban populace will increase by 50%, adding another 1.2 billion residents.

- Cities across Asia and the Pacific are in charge of global economic opportunities and sustainability endeavors. While they grapple with challenges like environmental degradation, escalating disasters, persistent slums, and social exclusion, they also stand as economic powerhouses, centers of innovation, and champions of cultural heritage preservation.

- Currently, office and retail real estate make up a significant portion of the Asia-Pacific investor portfolio, accounting for a third. However, this landscape is poised for a significant shift. While service sectors, notably hotels and retail, bore the brunt of the COVID-19 pandemic, industrial real estate, especially logistics and distribution centers, recovered soon and witnessed growth, with further expansion on the horizon. Consequently, there is a notable pivot in real estate asset allocation, with a tilt from retail toward industrial properties.

- Historically, office real estate grappled with high vacancy rates, prompting some to pivot toward residential offerings. Yet, there is a glimmer of optimism for 2024, especially in major urban centers where office rentals are projected to rise.

- Investors are increasingly turning their gaze toward niche real estate segments. Data centers, in particular, have garnered significant attention. Notably, Tokyo and Shanghai are the leaders in live data center capacities in the Asia-Pacific region. Another emerging star in the real estate market is the life sciences sector, encompassing a diverse array of medical facilities and properties.

Asia-Pacific Real Estate Brokerage Market Trends

Demand for Residential Segment Driving the Market

- In India, Delhi NCR saw a record-breaking quarter in 2024, with 5,109 high-end housing units sold. Gurgaon dominated the sales, accounting for 79% of the total. The completion of the Dwarka Expressway in Gurgaon played a pivotal role in driving this heightened demand, extending its impact across the city's major corridors.

- New launches in Gurgaon experienced overwhelming demand, with most projects selling out within days. Notably, DLF's Sector 77 project was fully booked within two days of its pre-launch, while Signature Global's Sector 37D project was oversubscribed by 5.4 times during its pre-launch phase. Noida and Delhi also made significant contributions to the high-end sales landscape.

- In Bangkok, market sentiment is on the rise, as highlighted by presales rates exceeding 50% for recent launches. Overall sales have seen a notable uptick, climbing by 20 basis points. Notably, two projects achieved a sell-out in the quarter, nudging the unsold rate down to 3.2%.

- The influx of international buyers is on the rise, helping to offset the limited purchasing power of local buyers. Apartment rental demand is rebounding, driven by a 12% year-on-year increase in tourist arrivals and expats in the first quarter. While the completion of Junit renovations in various projects pushed the vacancy rate to 5.0% in 2024, this growth is viewed as a transient blip, given the robust rental demand.

India Emerging as a Prominent Player with Rising Real Estate Demand

- In Mumbai, homebuyer preferences for spacious homes propelled sales in the high-end category to a new peak. Notably, industrialists, HNIs, C-suites, and entertainment celebrities gravitated toward high-ticket apartments in prime locales like Malabar Hill, Worli, and Bandra.

- Thane emerged as the dominant player, commanding a 21.8% share of the high-end sales, closely trailed by Western Suburbs II and Navi Mumbai. South Central Mumbai and Western Suburbs II witnessed unprecedented sales surges. Noteworthy launches like MICL Aaradhya Avaan in Prime South and Godrej Vistas in the Eastern Suburbs further bolstered these sales.

- Chennai's luxury housing sector saw a remarkable 141% surge in sales from the previous quarter, with hotspots like Kilpauk, Kotturpuram, and Vadapalani, situated in the Central and Off Central submarkets, witnessing heightened activity. Year-on-year, the city's total unit sales also climbed by 25%. This surge in Chennai's luxury housing market is attributed to rising demand for bespoke offerings, global design aesthetics, and top-tier amenities, which resonate with the discerning clientele.

Asia-Pacific Real Estate Brokerage Industry Overview

The Asia-Pacific real estate brokerage market is fragmented in nature. It witnesses a blend of local, regional, and global participants. Market concentration, however, can vary notably, not just between countries but even within cities. Factors shaping this concentration encompass the count of brokerage firms, their market shares, the competitive landscape, regulatory frameworks, and technological strides.

The key players in the market include CBRE Group, JLL, Colliers International, Knight Frank, Savills, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increasing Urbanization Driving the Market

- 4.2.1.2 Regulatory Environment Driving the Market

- 4.2.2 Restraints

- 4.2.2.1 Market Saturation Restraining the Market

- 4.2.2.2 Intrest Rate Fluctuations Restraining the Market

- 4.2.3 Opportunities

- 4.2.3.1 Technological Advancements Driving the Market

- 4.2.1 Drivers

- 4.3 Value Chain/Supply Chain Analysis

- 4.4 Government Regulations, Trade Agreements, and Initiatives

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Residential

- 5.1.2 Non-Residential

- 5.2 By Service

- 5.2.1 Sales

- 5.2.2 Rental

- 5.3 By Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 Australia

- 5.3.5 South Korea

- 5.3.6 Southeast Asia

- 5.3.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 CBRE Group

- 6.2.2 JLL

- 6.2.3 Colliers International

- 6.2.4 Knight Frank

- 6.2.5 Savills

- 6.2.6 Cushman & Wakefield

- 6.2.7 Century 21 Real Estate

- 6.2.8 ERA Real Estate

- 6.2.9 RE/MAX

- 6.2.10 Coldwell Banker*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日