|

市場調査レポート

商品コード

1636182

E-リキシャ用バッテリー:市場シェア分析、産業動向・統計、成長予測(2025~2030年)E-Rickshaw Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| E-リキシャ用バッテリー:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

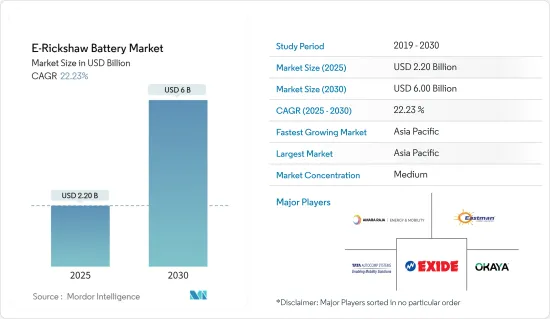

E-リキシャ用バッテリーの市場規模は2025年に22億米ドルと推定され、予測期間(2025~2030年)のCAGRは22.23%で、2030年には60億米ドルに達すると予測されます。

主要ハイライト

- 中期的には、政府のイニシアティブによってE-リキシャの普及が進み、従来の化石燃料を動力とするE-リキシャに比べて運行コストやメンテナンスコストが低いことから、予測期間中はE-リキシャ用バッテリー市場が牽引すると予想されます。

- その一方で、充電インフラが普及しておらず利用しにくいことや、E-リキシャの走行距離が限られていることが、予測期間中のE-リキシャ用バッテリー市場の成長を妨げる可能性があります。

- エネルギー密度の向上やE-リキシャ用バッテリー交換インフラの導入など、バッテリー技術における継続的な進歩は、E-リキシャ用バッテリー市場に大きな機会をもたらすと考えられます。

- アジア太平洋は、バッテリー駆動車の採用が増加しているため、e-E-リキシャ市場の支配的な地域になると予想されます。

リキシャ用バッテリー市場動向

リチウムイオンバッテリーが急成長

- さまざまな種類のバッテリー技術の中でも、リチウムイオンバッテリー(LIB)は予測期間中に最も急成長する電子リキシャ用バッテリー市場の一つになると予想されます。リチウムイオンバッテリーは、容量対重量比が良好なため、他のバッテリータイプよりも人気が高まっています。リチウムイオンバッテリーの普及を後押ししているその他の要因には、性能の向上(長寿命、低メンテナンス)、保存性の向上、価格の低下などがあります。

- リチウムイオン(Li-ion)バッテリーは、鉛バッテリーなどの他の技術に比べてさまざまな技術的利点を記載しています。平均して、リチウムイオンバッテリーは5,000回以上のサイクル寿命があり、鉛バッテリーは400~500回程度です。リチウムイオンバッテリーは、鉛バッテリーほど頻繁なメンテナンスや交換を必要としないです。さらに、これらのバッテリーは放電サイクルを通じて電圧を維持するため、電気部品の効率をより大きく、より長持ちさせることができます。

- 近年、複数の大手リチウムイオンバッテリーメーカーが、スケールメリットを得るための投資や性能向上のための研究開発活動を行っており、競合が激化し、リチウムイオンバッテリーの価格が下落しています。例えば、技術革新、製造改善、原料コストの低下により、リチウムイオンバッテリーの体積加重平均価格は2013年の780米ドル/kWhから2023年には139米ドル/kWhへと大幅に低下しました。2025年には約113米ドル/kWh、2030年には80米ドル/kWhに達する可能性が高いです。このようなバッテリーコストの低下動向は、今後数年間、E-リキシャ用バッテリー市場にとって、あらゆるバッテリーの中でリチウムイオンバッテリーを有利な選択肢にする可能性が高いです。

- リチウムイオンバッテリーは従来、携帯電話やノートパソコンなどの民生用電子機器に使用されてきました。しかし近年では、環境負荷の低さなどを理由に、各国のE-リキシャを含む電気自動車(BEV)の電源として再設計されるケースが増えています。

- 韓国財務省は2023年12月、今後5年間でリチウムバッテリー産業に38兆ウォンの施策融資を行う計画を発表しました。この施策は2024年に正式に実施されます。韓国はまた、1兆ウォンのリチウムバッテリー産業振興基金を設立し、関連技術の研究開発に736億ウォンを投資する計画です。同時に政府は、国内のリチウムバッテリー製造に必要な重要鉱物の埋蔵量を増やし、バッテリーの再利用とリサイクルのエコシステムを育成することを決定しました。これらはすべて、リチウムイオンバッテリー産業を後押しし、ひいては電子リキシャ用バッテリー市場の成長を支えるものと予想されます。

- アジア太平洋では、リチウムイオンバッテリーの製造が増加傾向にあります。例えば、Panasonic Groupは2024年3月、Indian Oil Corp(IOCL)と合弁会社を設立し、円筒形リチウムイオンバッテリーを製造すると発表しました。グループ会社のPanasonic Energyは、拘束力のあるタームシートに署名し、円筒形リチウムイオンバッテリーを製造する合弁会社設立の枠組みを描くためにIOCLとの協議を開始しました。この構想は、インド市場における二輪・三輪車用バッテリーの需要拡大が見込まれることによる。

- 2023年5月、StellantisはTotalEnergies、Mercedes-Benzとともに、フランスのビリーベルクロー・ドゥヴランにAutomotive Cells Company(ACC)のバッテリーギガ工場の落成式を行った。初期生産能力は13ギガワット時(GWh)で、2030年までに40ギガワット時(GWh)まで増加し、CO2排出量を最小限に抑えた高性能リチウムイオンバッテリーを供給することが期待されています。このギガファクトリーは、2030年までに欧州におけるバッテリー製造能力を250GWhに引き上げるというStellantisの目標に貢献することになります。

- さらに、エネルギー効率・再生可能エネルギー局によると、政府は2023年、北米における電気自動車用バッテリー工場の開発を発表しました。同地域の製造能力は、2021年の年間55ギガワット(GWh/年)から、2030年には1,000GWh/年に増強される見込みです。パイプラインにあるプロジェクトのほとんどは、2025~2030年の間に生産を開始すると予想されています。このことは、車載用バッテリーの市場開拓が堅調であることを示しており、今後数年間はE-リキシャ用バッテリー市場を下支えすることが期待されます。

- 2024年1月、Panasonic Energyは、カンザス州デソトに建設中の40億米ドルの電気自動車用バッテリー工場に関する最新情報を発表しました。同社によると、この製造施設はフル稼働時に毎秒66個のリチウムイオンバッテリーを生産します。470万平方フィートのバッテリー工場は、サンフラワー陸軍弾薬工場跡地に建設中で、2025年3月に生産を開始する予定です。このようなリチウムイオンバッテリーの開発は今後も世界中で継続され、E-リキシャ用バッテリー市場を支えていくと予想されます。

- 軽量化、充電時間の短縮、充電サイクル数の増加、コストの低下、リチウムイオンバッテリーの進歩といった特性により、リチウムイオンバッテリーは予測期間中、e-E-リキシャ用バッテリー市場を含む電気自動車の中で最も急成長するバッテリータイプになる可能性が高いです。

アジア太平洋が市場を独占する見込み

- アジア太平洋は、いくつかの魅力的な要因により、予測期間中、E-リキシャ用バッテリー市場を独占すると予想されます。例えば、インド、中国、バングラデシュなどの国々では、人口密度が高く、都市化が急速に進んでいるため、効率的で手ごろな価格の輸送手段に対するニーズが高まっており、E-リキシャは近距離移動に適した選択肢となっています。このような需要の高さは、E-リキシャ用バッテリーの堅調な市場に直結します。

- この地域のさまざまな新興国では、電子リキシャの導入に対する政府の支援が目立っています。特にインドなどは、公害対策と化石燃料への依存度低減に向けた広範な取り組みの一環として、E-リキシャを含む電気自動車の導入を促進するための支援的な規制、補助金、インセンティブを実施しています。例えば、インドのFAME(Faster Adoption and Manufacturing of Hybrid and Electric Vehicles)制度は、E-リキシャを含む電気自動車の採用に大きなインセンティブを与えました。

- 2024年3月、インドの重工業省(MHI)は、商用目的での二輪車と三輪車の電気自動車の採用を促進し、インドでの電気自動車の開発・製造に必要な支援を提供することを目的とした電気モビリティ推進スキーム(EMPS)を開始しました。

- EMPS-2024は、2024年4月1日から2024年7月31日までの4ヶ月間実施されます。予算は500億インドルピーで、EVに補助金を支給します。二輪車用EVには1台につき最大1万インドルピー、小型三輪車用EVには最大2万5,000ルピー、大型三輪車用EVには最大5万インドルピーが補助されます。三菱重工は、EVの販売時に補助金や需要奨励金をEVメーカーに払い戻すが、最終的な請求価格から補助金が差し引かれるため、EVの購入価格が下がり、消費者にもメリットがあります。このような取り組みにより、国内でのE-リキシャとその関連バッテリーの導入が促進されることが期待されます。

- インドの道路交通・高速道路省によると、2023年のインドの電動三輪車の年間販売台数は58万1,000台以上です。国際エネルギー機関(IEA)のデータによると、2023年の世界の電動三輪車販売台数シェアは、中国とインドを合わせて66%を占めています。このことは、これらの国々が予測期間中も膨大な成長を続け、確認する可能性が高いことを浮き彫りにしています。

- さらに、この地域の重要なバッテリーメーカーが市場の成長を後押ししています。Exide Industries、Amara Raja Batteries、Okaya Powerなどの企業は、最新のバッテリー技術やイノベーションに容易にアクセスできます。また、これらの企業は、バッテリー性能の向上、コスト削減、E-リキシャ用バッテリーの寿命延長のための研究開発に継続的に投資しており、消費者にとってより魅力的な製品となっています。

- アジア太平洋は、労働力と原料が安いため生産コストが低く、E-リキシャ用バッテリーの競合価格設定が可能です。このコスト優位性は、さまざまな社会経済層への普及を後押しし、多くの人々にとってE-リキシャが経済的に実行可能なソリューションとなっています。

- さらに、環境意識の高まりとサステイナブル都市交通ソリューションの必要性が、市場を前進させる。E-リキシャは従来の自動E-リキシャに代わるより環境に優しい選択肢を提供し、多くのアジア太平洋諸国の環境目標に合致しています。その結果、この地域は当面、世界のE-リキシャ用バッテリー市場で主導的地位を維持すると予想されます。

- したがって、上記の要因により、アジア太平洋は予測期間中、E-リキシャ市場を独占すると予想されます。

E-リキシャ用バッテリー産業概要

E-リキシャ用バッテリー市場は適度にセグメント化されています。市場の主要企業(順不同)には、Exide Industries Ltd、Eastman Auto & Power Ltd、Amara Raja Energy &Mobility Limited、Okaya Power Private Limited、TATA AutoComp GY Batteries Pvt. Ltdなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 政府のイニシアティブによるE-リキシャの普及拡大

- 従来の化石燃料リキシャに比べ、運行・維持コストが低い

- 抑制要因

- 充電インフラが普及しておらず、アクセスしにくい

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- バッテリータイプ

- 鉛蓄バッテリー

- リチウムイオンバッテリー

- その他のバッテリー

- 車種

- 乗用車

- 貨物自動車

- 地域

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- タイ

- マレーシア

- インドネシア

- ベトナム

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- ナイジェリア

- カタール

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他の南米

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略とSWOT分析

- 企業プロファイル

- Exide Industries Ltd

- Eastman Auto & Power Ltd

- Amara Raja Energy & Mobility Limited

- Okaya EV Pvt. Ltd

- TATA AutoComp GY Batteries Pvt. Ltd

- Microtex Energy Private Limited

- Sparco Batteries Pvt. Ltd

- Gem Batteries Pvt. Ltd

- Alsym Energy Inc.

- その他の著名な企業一覧(会社名、本社所在地、関連製品とサービス、連絡先など)

- 市場ランキング分析

第7章 市場機会と今後の動向

- E-リキシャ用バッテリー交換インフラの導入

The E-Rickshaw Battery Market size is estimated at USD 2.20 billion in 2025, and is expected to reach USD 6.00 billion by 2030, at a CAGR of 22.23% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the growing adoption of e-rickshaws aided by government initiatives and the lower operational and maintenance costs compared to traditional fossil fuel-powered rickshaws are expected to drive the e-rickshaw battery market during the forecast period.

- On the other hand, the lack of widespread and accessible charging infrastructure and the limited range of e-rickshaws can hinder the growth of the e-rickshaw battery market during the forecast period.

- Ongoing advancements in battery technologies, such as increased energy density and the implementation of battery-swapping infrastructure for e-rickshaw, are likely to create vast opportunities for the e-rickshaw battery market.

- Asia-Pacific is expected to be a dominant region in the e-rickshaw market due to the increasing adoption of battery-powered vehicles.

E-Rickshaw Battery Market Trends

Lithium-ion Battery to be the Fastest Growing

- Among different types of battery technologies, lithium-ion batteries (LIB) are expected to be among the fastest-growing e-rickshaw battery markets during the forecast period. Lithium-ion batteries are gaining more popularity than other battery types due to their favorable capacity-to-weight ratio. Other factors boosting their adoption include better performance (long and low maintenance), better shelf life, and decreasing price.

- Lithium-ion (Li-ion) batteries offer various technical advantages over other technologies, such as lead-acid batteries. On average, Li-ion batteries offer cycles over 5,000 times compared to lead-acid batteries that last around 400-500 times. Li-ion batteries do not require as frequent maintenance and replacement as lead-acid batteries. Furthermore, these batteries maintain their voltage throughout the discharge cycle, allowing more significant and longer-lasting efficiency of electrical components.

- In recent years, several major lithium-ion battery players have been investing to gain economies of scale and R&D activities to enhance their performance, increasing the competition and declining lithium-ion battery prices. For example, due to the improving technological innovations, manufacturing improvements, and declining raw material costs, the volume-weighted average price of lithium-ion batteries decreased considerably from USD 780/kWh in 2013 to USD 139/kWh in 2023. It is likely to reach around USD 113/kWh in 2025 and USD 80/kWh in 2030. Such declining trends in battery costs are likely to make it a lucrative choice among all batteries for the e-rickshaw battery market in the coming years.

- Lithium-ion batteries have traditionally been used in consumer electronic devices like mobile phones, laptops, and others. However, in recent years, they have increasingly been redesigned for use as the power source of choice in electric vehicles (BEVs), including e-rickshaws, in various countries, owing to factors such as low environmental impact.

- In December 2023, South Korea's Ministry of Finance announced plans to provide KRW 38 trillion in policy financing to the lithium battery industry over the next five years. This policy will be formally implemented in 2024. South Korea also plans to establish a KRW 1 trillion lithium battery industry promotion fund and invest KRW 73.6 billion in research and development of related technologies. At the same time, the government decided to increase the critical mineral reserves required for domestic lithium battery manufacturing and cultivate a battery reuse and recycling ecosystem. All these are anticipated to boost the lithium-ion battery industry and, in turn, support the growth of the e-rickshaw batteries market.

- There has been an increasing trend in lithium-ion battery manufacturing in the Asia-Pacific region. For example, in March 2024, Panasonic Group announced it would form a joint venture with Indian Oil Corporation Ltd (IOCL) to manufacture cylindrical lithium-ion batteries. Panasonic Energy, a group firm, signed a binding term sheet and initiated discussions with IOCL to draw a framework for forming a joint venture to manufacture cylindrical lithium-ion batteries. This initiative is driven by the expected expansion of demand for batteries for two and three-wheel vehicles in the Indian market.

- In May 2023, Stellantis, together with TotalEnergies and Mercedes-Benz, celebrated the inauguration of Automotive Cells Company's (ACC) battery gigafactory in Billy-Berclau Douvrin, France, the first of three planned in Europe. With an initial production line capacity of 13 gigawatt-hours (GWh), rising to 40 GWh by 2030, the facility is expected to deliver high-performance lithium-ion batteries with a minimal CO2 footprint. The gigafactory will contribute to Stellantis' goal of increasing battery manufacturing capacity to 250 GWh in Europe by 2030.

- Furthermore, as per the Office of Energy Efficiency and Renewable Energy, in 2023, the government announced the development of electric vehicle battery plants in North America. The region is expected to ramp up manufacturing capacity from 55 gigawatts per year (GWh/year) in 2021 to 1000 GWh/year by 2030. Most of the projects in the pipeline are expected to initiate production between the years 2025 to 2030. This indicates a robust battery market development for automotive applications, which is expected to support the e-rickshaw battery market in the coming years.

- In January 2024, Panasonic Energy announced an update on their USD 4 billion electric vehicle battery plant, still under construction, in De Soto, Kansas. According to the company, the manufacturing facility will produce 66 lithium-ion batteries per second when operating at full capacity. The 4.7 million-square-foot battery plant is still under construction on the former Sunflower Army Ammunition Plant site, and it is expected to begin production in March 2025. Such developments in lithium-ion batteries are anticipated to continue across the globe and support the e-rickshaw battery market.

- Due to properties such as less weight, low charging time, a higher number of charging cycles, declining cost, and the growing progress in lithium-ion batteries, they are likely to be the fastest-growing battery type among electric vehicles, including the e-rickshaw battery market, during the forecast period.

Asia-Pacific Region is Expected to Dominate the Market

- The Asia-Pacific region is anticipated to dominate the e-rickshaw battery market during the forecast period due to several compelling factors. For example, the high population density and rapid urbanization in countries such as India, China, and Bangladesh are driving the need for efficient and affordable transportation solutions, positioning e-rickshaws as a preferred option for short-distance travel. This high demand directly translates to a robust market for e-rickshaw batteries.

- Various emerging countries in the region are experiencing notable government support for the adoption of e-rickshaws. In particular, countries such as India are implementing supportive regulations, subsidies, and incentives to promote the adoption of electric vehicles, including e-rickshaws, as part of broader efforts to combat pollution and reduce dependency on fossil fuels. For instance, India's Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme significantly incentivized the adoption of electric vehicles, including e-rickshaws.

- In March 2024, the Ministry of Heavy Industries (MHI) in India launched the Electric Mobility Promotion Scheme (EMPS) that aims to boost the adoption of two-wheeler and three-wheeler electric vehicles for commercial purposes and provide the necessary support for developing and manufacturing EVs in India.

- The EMPS-2024 is being implemented for four months, from 1 April 2024 to 31 July 2024. It has a budget of INR 500 crore and provides subsidies to EVs. Subsidies of up to INR 10,000 will be provided for each two-wheeler EV, up to INR 25,000 for each small three-wheeler EV, and up to INR 50,000 for each large three-wheeler EV. The MHI will reimburse the subsidies or demand incentives to the EV manufacturers upon the sale of a vehicle, which will also benefit the consumers as the subsidy amount will be deducted from the final invoice price, thus reducing the purchase price of the EVs. Such initiatives are anticipated to boost the country's adoption of e-rickshaws and their relevant batteries.

- As per the Ministry of Road Transport and Highways in India, the annual sales of electric three-wheelers in India stood at over 581 thousand units in 2023. The data from the International Energy Agency (IEA) revealed that together, China and India accounted for 66% of the world's electric three-wheeler sales share in 2023. This highlights that these countries are likely to continue and witness vast growth during the forecast period.

- Moreover, crucial battery manufacturers in the region enhance the market's growth. Companies like Exide Industries, Amara Raja Batteries, and Okaya Power offer easy access to the latest battery technologies and innovations. Besides, these players continuously invest in research and development to improve battery performance, reduce costs, and extend the lifespan of e-rickshaw batteries, making them more attractive to consumers.

- The Asia-Pacific region benefits from lower production costs due to cheaper labor and raw materials, enabling competitive pricing of e-rickshaw batteries. This cost advantage helps drive widespread adoption across different socioeconomic segments, making e-rickshaws an economically viable solution for many.

- Furthermore, the rising environmental awareness and the need for sustainable urban transport solutions propel the market forward. E-rickshaws offer a greener alternative to traditional auto-rickshaws, aligning with the environmental goals of many Asia-Pacific nations. As a result, the region is expected to maintain its leading position in the global e-rickshaw battery market for the foreseeable future.

- Therefore, due to the abovementioned factors, the Asia-Pacific region is expected to dominate the e-rickshaw market during the forecast period.

E-Rickshaw Battery Industry Overview

The e-rickshaw battery market is moderately fragmented. Some key players in the market (not in any particular order) include Exide Industries Ltd, Eastman Auto & Power Ltd, Amara Raja Energy & Mobility Limited, Okaya Power Private Limited, and TATA AutoComp GY Batteries Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Adoption of E-Rickshaws Aided By Government Initiatives

- 4.5.1.2 Lower Operational and Maintenance Costs Compared to Traditional Fossil Fuel-powered Rickshaws

- 4.5.2 Restraints

- 4.5.2.1 Lack of Widespread and Accessible Charging Infrastructure and Limited Range of E-rickshaws

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lead-acid Battery

- 5.1.2 Lithium-ion Battery

- 5.1.3 Other Batteries

- 5.2 Vehicle Type

- 5.2.1 Passenger Carrier

- 5.2.2 Goods Carrier

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Nordic

- 5.3.2.7 Russia

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Thailand

- 5.3.3.6 Malaysia

- 5.3.3.7 Indonesia

- 5.3.3.8 Vietnam

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 Saudi Arabia

- 5.3.4.2 United Arab Emirates

- 5.3.4.3 South Africa

- 5.3.4.4 Egypt

- 5.3.4.5 Nigeria

- 5.3.4.6 Qatar

- 5.3.4.7 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Chile

- 5.3.5.4 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted & SWOT Analysis for Leading Players

- 6.3 Company Profiles

- 6.3.1 Exide Industries Ltd

- 6.3.2 Eastman Auto & Power Ltd

- 6.3.3 Amara Raja Energy & Mobility Limited

- 6.3.4 Okaya EV Pvt. Ltd

- 6.3.5 TATA AutoComp GY Batteries Pvt. Ltd

- 6.3.6 Microtex Energy Private Limited

- 6.3.7 Sparco Batteries Pvt. Ltd

- 6.3.8 Gem Batteries Pvt. Ltd

- 6.3.9 Alsym Energy Inc.

- 6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Implementation of Battery-swapping Infrastructure for E-rickshaws