|

市場調査レポート

商品コード

1636110

欧州のローターブレード:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Europe Rotor Blade - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のローターブレード:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

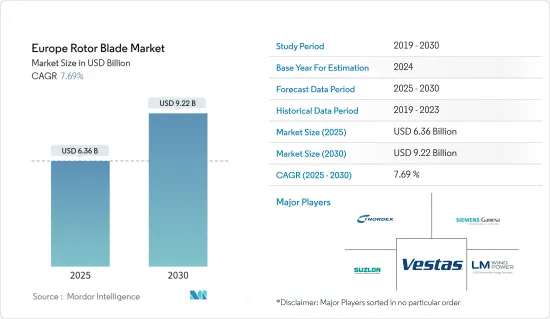

欧州のローターブレード市場規模は2025年に63億6,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは7.69%で、2030年には92億2,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、オフショアとオンショア風力発電設備の増加、風力発電コストの低下、風力発電セグメントへの投資の増加といった要因が、予測期間中の欧州のローターブレード市場を牽引すると予測されます。

- 一方、それに伴う輸送コストの高騰や、太陽光発電、水力発電などの代替クリーン電源のコスト競合などの要因は、予測期間中の市場成長を抑制する可能性があります。

- 風力発電事業では費用対効果の高いソリューションが求められており、高効率の製品には産業の力学を変える力があります。古いタービンが交換されたのは、破損が原因ではなく、より効果的なブレードが市場で販売されたからです。このように、技術の進歩は最終的にローターブレード市場に素晴らしい機会を生み出します。

欧州のローターブレード市場動向

オフショアセグメントが市場を独占

- 欧州の2022年の新規風力発電設備容量は1,859万kW。欧州の電力需要は、パンデミックの終息後、産業活動の開始や急速な都市化と相まって増加しています。この地域はまた、増加する電力需要を満たすために、再生可能エネルギーの割合が増加しています。

- 欧州には、太陽光、風力、水力、バイオマス、地熱など、発電に必要な再生可能エネルギー資源が豊富にあると考えられています。欧州の多くの国々が、世界的に再生可能エネルギー活用の最前線に立っています。脱炭素化、電力系統の持続可能性、野心的な目標、クリーンエネルギーへの移行といった要因が、欧州の風力エネルギー市場を牽引しています。

- 2022年12月、欧州委員会は2023年再生可能エネルギー源法を承認し、2023年オフショア風力エネルギー法は環境を改善し、欧州の電力市場における温室効果ガスニュートラルな電力供給の実現に焦点を当てることを目的としています。

- さらに2022年5月、欧州委員会はREPowerEU計画を発表しました。この計画には、ロシアの化石燃料を段階的に廃止し、EUにおける再生可能エネルギーの生産を促進することを目的とした一連の具体策が盛り込まれています。この計画は、同地域におけるオフショア風力発電のさらなる発展に貢献すると考えられます。

- REPowerEUの発表に伴い、オフショア風力のさらなる拡大を達成するためにエスビエル宣言が形成され、ベルギー、デンマーク、ドイツ、オランダを結ぶオフショア再生可能エネルギーシステムである「欧州のグリーン発電所」としての北海と、場合によっては北海エネルギー協力(NSEC)加盟国を含む他の北海パートナーを共同開発することが決定され、2050年までに150GWのオフショア風力という新たな目標が掲げられました。

- 国際再生可能エネルギー機関によると、欧州は世界のオフショア風力発電市場の主要地域のひとつです。2022年には4,264MWが追加され、3,066万kWに達しました。2022年3月、フランス政府はフランスの風力産業とオフショア部門協定を締結しました。この協定は、オフショア風力が重要かつ不可欠な機会であることを認識し、2050年までに50のウィンドファームで40GWのオフショア風力を開発することを約束しています。これにより、オフショア風力発電の大幅な開発が期待されます。

- また、2022年6月には、キリーベグス漁業組合とシンドバッド海洋サービスが、アイルランドのドニゴール沖に建設する浮体式風力発電所を提案し、スウェーデンの浮体式風力発電開発技術プロバイダーであるヘキシコンと覚書を交わしました。

- 以上のことから、予測期間中はオフショアセグメントが市場を独占すると予想されます。

市場を独占する英国

- 英国は、風力発電で成長している国のひとつです。同国は、欧州における風力発電の最適地として位置づけられています。2022年までに、英国は28.54GWの風力発電容量を設置します。

- また、英国はロシアのガス供給に依存していないため、他のEU諸国と比べてロシア・ウクライナ紛争の影響を大きく受けていないです。しかし、2022年4月、英国の前首相は、戦争の影響を軽減し、国内の再生可能エネルギー開発を促進するため、エネルギー安全保障戦略を実施しました。これはひいては風力エネルギー市場の成長を支え、風力ローターブレード市場の開拓をさらに後押しすると考えられます。

- 同国はオフショア風力発電プロジェクトの先駆者の1つであるため、2016~2021年の間に、英国ではオフショア風力発電に約257億9,000万米ドルが投資され、オフショア風力発電セグメントの良好な投資環境が実証されました。

- さらに2022年4月、政府は英国のエネルギー安全保障を強化する戦略的計画を発表し、2030年までに最大50GWのオフショア風力発電容量を稼働させるという目標が盛り込まれました。50GWのオフショア風力発電目標には、5GWの大規模浮体式オフショア風力発電設備が含まれます。

- さらに2022年1月、英国政府は浮体式オフショア風力発電プロジェクトの研究開発を推進するため、8,250万米ドル以上の公的・民間資金を投入すると発表しました。同政府は、浮体式オフショア風力実証プログラムの一環として、11のプロジェクトに4,190万米ドルを投資する予定です。

- したがって、上記の点から、予測期間中は英国が市場を独占すると予想されます。

欧州のローターブレード産業概要

欧州のローターブレード市場は細分化されています。市場の主要企業(順不同)には、Nordex SE、Siemens Gamesa Renewable Energy, SA、Vestas Wind Systems A/S、Suzlon Energy Limited、LM Wind Power(GE Renewable Energy事業)などがあります。

2022年2月、NordexはドイツのロストックGVZローターブレード工場でのローターブレード生産を2022年6月末までに停止すると発表しました。この決定は主に、ロストックでは製造できない大型ブレードへのシフトによるものです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- オフショアとオンショア風力発電設備の増加

- 風力発電コストの低下

- 抑制要因

- 代替再生可能エネルギーとの競合激化

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 展開場所

- オンショア

- オフショア

- ブレード材料

- 炭素繊維

- ガラス繊維

- その他のブレード材料

- 地域

- ドイツ

- フランス

- スペイン

- 英国

- イタリア

- ノルディック

- トルコ

- ロシア

- その他の欧州

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Nordex SE

- Siemens Gamesa Renewable Energy SA

- Vestas Wind Systems A/S

- Suzlon Energy Limited

- Enercon GmbH

- LM Wind Power(GE Renewable Energy事業)

- BayWa R.E AG

- Market Ranking/Share Analysis

第7章 市場機会と今後の動向

- 高効率・軽量風力タービンの開発

The Europe Rotor Blade Market size is estimated at USD 6.36 billion in 2025, and is expected to reach USD 9.22 billion by 2030, at a CAGR of 7.69% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the growing number of offshore and onshore wind energy installations, the declining cost of wind energy, and increasing investments in the wind power sector are anticipated to drive the Europe rotor blade market during the forecast period.

- On the other hand, factors such as the accompanying high cost of transportation and cost competitiveness of alternate clean power sources like solar power, hydropower, etc., can potentially restrain the market growth during the forecast period.

- Nevertheless, the wind power business has sought cost-effective solutions, and a highly efficient product has the ability to alter the industry's dynamics. There were instances where old turbines were replaced not owing to damage but because more effective blades were sold in the market. Thus, technological advancements eventually create a wonderful opportunity for the market of rotor blades.

Europe Rotor Blade Market Trends

Offshore Segment to Dominate the Market

- Europe accounted for 18.59 GW of new wind installed capacity in 2022. The electricity demand in Europe has increased after the departure of the pandemic, coupled with the commencement of industrial activities and rapid urbanization. The region has also witnessed a growing share of renewables to fulfill the increasing electricity demand.

- Europe is considered to have ample renewable energy resources to generate electricity, such as solar, wind, hydro, biomass, geothermal, etc. A good number of countries in Europe have become at the forefront of utilizing renewable energy globally. Factors such as decarbonization, sustainability of power systems, ambitious targets, and clean energy transition have driven the offsore wind energy market of Europe.

- In December 2022, the European Commission approved the 2023 Renewable Energy Sources Act, and the 2023 Offshore Wind Energy Act aims to improve the environment and focus on achieving a greenhouse gas-neutral electricity supply in the power market of Europe.

- Further, in May 2022, the European Commission published the REPowerEU plan, which contains a series of concrete measures designed to phase out Russian fossil fuels and boost the production of renewable energy in the EU. This plan would help further develop offshore wind energy in the region.

- With the REPowerEU announcement, the Esbjerg Declaration was formed to achieve the further expansion of offshore wind and decided to jointly develop The North Sea as a Green Power Plant of Europe, an offshore renewable energy system connecting Belgium, Denmark, Germany, and the Netherlands, and possibly other North Sea partners, including the members of the North Seas Energy Cooperation (NSEC) and set out a new target of 150 GW of offshore wind by 2050.

- According to International Renewable Energy Agency, Europe is among the leading regions in the global offshore wind power market. In 2022, it added 4,264 MW, reaching 30.66 GW. In March 2022, the French government entered into an offshore sector agreement with France's wind industry. The agreement recognizes that offshore wind is a significant and vital opportunity and commits to developing 40 GW of offshore wind by 2050 spread over 50 wind farms. This is expected to witness considerable development in offshore wind power.

- Also in June 2022, The Killybegs Fishermen's Organization and Sinbad Marine Services have proposed a floating wind farm to be built offshore Donegal, Ireland, and have signed a Memorandum of Understanding with Swedish floating wind developer and technology provider, Hexicon.

- Therefore, owing to the above points, the offshore segment is anticipated to dominate the market during the forecast period.

United Kingdom to Dominate the Market

- The United Kingdom is one of the growing countries in wind energy generation. The country stands as the best location for wind power in Europe. By 2022, the United Kingdom installed a wind capacity of 28.54 GW.

- Moreover, the United Kingdom is not heavily affected by the Russia-Ukraine conflict compared to the other EU countries, Since the country is not dependent on the Russian gas supply. However, in April 2022, the former UK Prime Minister implemented an energy security strategy to lessen the war impact and boost renewable energy development within the country. This will, in turn, support the growth of the wind energy market and further aid the development of the wind rotor blade market.

- Since the country is one of the forerunners in offshore wind projects, between 2016 and 2021, nearly USD 25.79 billion was invested in offshore wind in the United Kingdom, witnessing a favorable investment environment in the offshore wind sector.

- Furthermore, in April 2022, the government announced a strategic plan to boost Britain's energy security, including an increased target of up to 50 GW of operating offshore wind capacity by 2030. The 50GW offshore wind target includes 5 GW of large-scale floating wind installations.

- Moreover, in January 2022, the UK government announced more than USD 82.5 million of public and private funding to advance research and development in floating offshore wind projects. The government plans to invest USD 41.9 million in 11 projects as part of the Floating Offshore Wind Demonstration Program.

- Therefore, owing to the above points, the United Kingdom is anticipated to dominate the market during the forecast period.

Europe Rotor Blade Industry Overview

The Europe rotor blade market is fragmented in nature. Some of the major players in the market (in no particular order) include Nordex SE, Siemens Gamesa Renewable Energy, SA, Vestas Wind Systems A/S, Suzlon Energy Limited, and LM Wind Power (a GE Renewable Energy business), among others.

In February 2022, Nordex announced that it would cease the production of rotor blades at the Rostock GVZ rotor blade site in Germany by the end of June 2022. The decision has been taken primarily due to a shift towards larger blades that are not manufactured at Rostock.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing number of offshore and onshore wind energy installations

- 4.5.1.2 Declining cost of wind energy

- 4.5.2 Restraints

- 4.5.2.1 Increasing Competition from Alternate Renewable Energy Sources

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Blade Material

- 5.2.1 Carbon Fiber

- 5.2.2 Glass Fiber

- 5.2.3 Other Blade Materials

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 France

- 5.3.3 Spain

- 5.3.4 United Kingdom

- 5.3.5 Italy

- 5.3.6 NORDIC

- 5.3.7 Turkery

- 5.3.8 Russia

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Nordex SE

- 6.3.2 Siemens Gamesa Renewable Energy SA

- 6.3.3 Vestas Wind Systems A/S

- 6.3.4 Suzlon Energy Limited

- 6.3.5 Enercon GmbH

- 6.3.6 LM Wind Power (a GE Renewable Energy business)

- 6.3.7 BayWa R.E AG

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of High Efficiency and light weight wind turbines