日本の決済市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Japan Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1631653

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

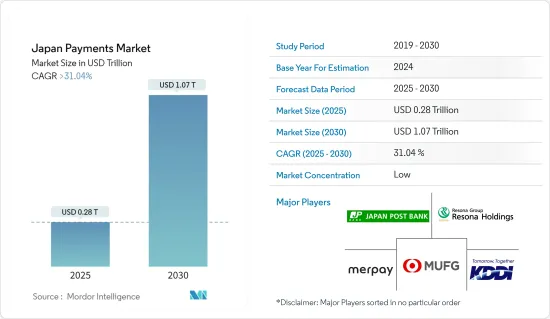

日本の決済市場規模は2025年に2,800億米ドル、2030年には1兆700億米ドルに達すると推定・予測され、予測期間中(2025~2030年)のCAGRは31.04%を超えると予想されます。

決済は、物々交換からトークンシステム(硬貨や紙幣の交換)、通貨プール(預金や銀行口座)、最終的にはキャッシュレス取引へと進化してきました。過去10年間、日本では近代的な決済システムが大幅に加速しており、これが日本市場の成長に影響を与えている主要要因の一つです。

主要ハイライト

- 日本における主要な決済手段のひとつは現金であるが、デジタル取引が急速に開発され、日本がデジタル化されつつあります。日本政府による必要なインフラの整備も、決済市場の効率的な運営を後押ししています。

- 第3世代のオンライン技術であるWeb 3.0は、構造化データとコグニティブサービスを組み合わせ、Webがユーザーの目的を理解し、達成できるようにするものです。ペイメントはWeb 3.0を利用して、よりインテリジェントで個別化された決済体験をユーザーに提供することができます。自然言語処理(NLP)と音声コマンドを使用することで、消費者は、例えば、Web 3.0技術を使用して、何をいくら決済たいかをデバイスに伝えることができます。ユーザーの過去の決済履歴や嗜好に基づき、Web 3.0技術はカスタマイズ型決済推奨やオファーを提供することもできます。こうした技術もまた、予測期間中に日本の決済市場に影響を与え、進化していくと予想されます。

- オンライン請求書決済やその他の送金サービスを可能にするシンプルさから、モバイルウォレットは日本中のeコマース事業者に非常に普及しています。さらに、これらの最新機器を使用することで、迅速かつ安全な取引が可能になります。モバイルウォレットを利用するこれらの利点により、これらの製品の利用が増加しています。この要因は、予測期間中、調査対象市場に有利な機会を生み出すと予想されます。モバイルウォレットの顧客は、ユーザーフレンドリーなUIにより、簡単に送金や受け取りができます。スマートフォンのユーザーは、ユーザーフレンドリーなUIにより、外出先でも取引を完了することができます。

- その反面、カード詐欺は、窃盗犯がカード所有者の金融情報やクレジットカード情報を利用してユーザー口座に不正に侵入し、金銭を奪うことで発生します。詐欺の被害に遭うユーザー数が大幅に増加しているのは、現在、ほとんどの人の日常生活や職業生活がバーチャルまたはオンラインになっていることに加え、日本をオンラインで狙うハッカーや組織犯罪集団が複雑化していることが原因です。こうした要因は、調査対象市場の成長を抑制する可能性が高いです。

- COVID-19は日本の決済市場に顕著な影響を与え、ゆうちょ銀行のような企業はPayPalとのライバル関係を激化させています。市場関係者は、パンデミックの影響を軽減するため、決済産業における継続的なデジタル化とイノベーションに努めています。そのため、パンデミック後の日本では、ペイメント産業の進化が続くと予想されます。

日本の決済市場の動向

オンライン販売決済が大きな市場シェアを占める見込み

- オンライン請求書決済やその他の送金サービスを可能にするシンプルさから、モバイルウォレットはeコマース事業者向けに日本全国で成人気となっています。さらに、こうした最新機器を使用することで、迅速かつ安全な取引が可能になります。モバイルウォレットを利用するこれらの利点により、これらの製品の利用が増加しています。予測期間中、オンライン決済機能は、調査対象市場において有利な機会を創出すると予想されます。

- 代替デジタル通貨はすでにこの地域で急速に受け入れられており、中でも暗号通貨は最も需要が高いです。将来のデジタルウォレットは、これらの代替デジタル資産へのオンデマンドで摩擦のないアクセスを提供し、決済取引を保存して可能にします。さらに、様々な決済ソースを利用した金融取引を可能にします。

- 同様に、日本のBNPL(buy now, pay later)企業であるPaidyは、口座保有者をデジタルウォレットに瞬時にリンクさせるPaidy Linkを提供しています。Paidyは、取引を迅速化し、決済を確実にするために、自社のモデルと機械学習を採用しています。JS Capital Management、Soros Capital Management、Tybourne Capital Management、Wellington Managementは、同社の最近のシリーズD資金調達ラウンド(1億2,000万米ドル)に貢献しました。

- Bank of Japanによると、2023年8月から9月にかけて実施された調査によると、日本で最も利用されているキャッシュレス決済手段はクレジットカードでした。回答者の約68.4%が日常生活でクレジットカードを使用していると回答し、8.1%は現金のみを使用していました。さらに、日本の消費者がキャッシュレス決済を利用する最大の理由は、迅速で簡単な決済プロセスでした。回答者の67%以上が、迅速かつ簡単に決済を行うためにデジタル決済を利用していると答えました。さらに、日本消費者信用協会によると、2023年、日本のクレジットカード発行枚数は3億860万枚に達しました。前年の3億100万枚超から2.5%増加しました。

- オンラインショッピングへの支出の増加は、市場参入企業が市場シェアを獲得するために新しいリアルタイム決済ソリューションを開発する機会を生み出すと考えられます。2023年1月、日本のフィンテック企業であるSmartpayは、利用者の銀行口座から直接分割払いができる国内初のデジタル決済サービス「Smartpay Bank Direct」を開始しました。この新サービスを通じて、スマートペイは、日本のオープンバンキングシステムを利用する日本初のデジタル消費者金融会社であり、日本全国67行の提携銀行ネットワークを有すると主張しています。このデジタルペイメントサービスは、クレジットカードや口座引き落としに対応し、購入時に自動化されたシングルクリックのユーザーエクスペリエンスを記載しています。

小売エンドユーザー産業セグメントが大きな市場シェアを占める見込み

- エンドユーザーの決済習慣の変化、決済技術の革新、技術進歩、新規事業者の参入により、日本のリテール決済の状況は近年大きく変化しています。日本の消費者は現在、モバイル技術によって実現されたさまざまな新しい便利な決済手段を利用しています。最も重要な小売決済動向のひとつは、BNPL(今すぐ買って後で払う)です。さらに、電子商取引が流行を通じて新たなレベルにまで成長したため、新しい決済プラットフォームはPayIDを利用したリアルタイムの決済を可能にしました。日本では多くの小売業者がBNPLを不可欠な決済手段として受け入れており、特にBNPLの導入率が高い特定の小売市場におけるインターネット販売では、その傾向が顕著です。

- さらにApplivトピックスによると、成長する日本のeコマース産業は、Rakuten、Yahoo Japan,、Amazonの3大オンライン小売業者によって先導されており、売上高は1兆円(6,800万米ドル)を超えています。市場をリードする3社は、B2C(B2C)コマース以外のさまざまな商品やサービスを提供することで、月間アクティブユーザー数を拡大し、オンラインユーザーの40%以上に自社ブランドを浸透させました。これには、Rakutenのインターネット・バンキングサービス、Amazonの動画配信サービス、Yahooのオークションプラットフォームなどが含まれます。

- さらに、Appliv TopicsとJustSystemsが2023年に日本で実施した調査によると、消費者の間で最も利用されているeコマースサイトはAmazonで、約50%が日本のプラットフォームを主要なオンラインショッピングチャネルとして挙げています。2位はオンライン市場のRakuten Ichibaで、オンラインショッピング利用者の約3人に1人がRakutenのプラットフォームで注文しています。

- リンクによる決済は、チェックアウトプロセスを合理化するのに非常に効果的な比較的新しい決済方法です。日本では勢いを増しています。オンライン、店舗を問わず、あらゆる小売セグメントに浸透する可能性があります。これにより、企業はテキスト、電子メール、チャット、QRコードを通じて自動的に決済リンクを作成し、顧客に配布することができます。顧客は、ワンタイム・ユースのURLを使用するこれらのリンクを使って、PCI準拠のホストされたチェックアウト・ページに誘導されます。その後、顧客は決済の詳細を入力します。

- Infcurionは、全国の16~69歳の2万人を対象に「2023年消費者決済動向調査」を実施しました。QRコード決済アプリの利用は、すべての業種で増加しました。スーパーマーケット・食料品店」(13%から18%)、「タクシー」(8%から16%)、「日本のパブ・バー」(9%から14%)が大幅に増加しました。

日本のペイメント産業概要

日本ペイメント市場は、MerPay、Mitsubishi UFJ Financial Group、Resona Holdings、KDDI Corporation(AuPay)、Japan Post Bankなどの主要企業が存在するため、非常にセグメント化されています。市場参入企業は、製品提供を強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年11月-日本最大級の金融サービス企業であるMitsubishi UFJ Financial Group(MUFG)は、デジタルトランスフォーメーションを加速させるためにAmazon Web Services(AWS)を採用しました。MUFGは複数年にわたる契約の一環として、AWSのクラウド技術を活用し、生成型人工知能(AI)と機械学習機能を導入し、プロセスを自動化し、顧客のニーズに合わせてパーソナライズされた金融サービスを記載しています。

- 2023年7月-LINEの仮想資産・ブロックチェーン関連事業部門とPayPay Corporationは、PayPayマネーで仮想資産を購入し、暗号資産取引サービス "LINE BITMAX "でPayPayマネーに換金できる「PayPay連携サービス」の開始を発表。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の利害関係者分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 国内における決済環境の進化

- 国内におけるキャッシュレス取引の拡大に関連する主要市場動向

- COVID-19が同国の決済市場に与える影響

第5章 市場力学

- 市場促進要因

- オンライン決済の普及

- 政府による取り組み

- 市場課題

- 消費者のデータプライバシー

- 市場機会

- キャッシュレス社会への移行

- 新規参入企業によるイノベーションが普及を促進

- デジタル決済産業における主要規制と基準

- 主要事例と使用事例の分析

- 日本の決済産業に関する主要な人口動向とパターンの分析(人口、インターネット普及率、銀行普及率/非銀行人口、年齢・所得などを含む)

- 日本における顧客満足度重視の高まりと世界の動向の融合に関する分析

- 日本における現金離れと非接触決済の台頭に関する分析

第6章 市場セグメンテーション

- 決済方法

- 販売時点

- カード決済(デビットカード、クレジットカード、銀行融資プリペイドカードを含む)

- デジタルウォレット(モバイルウォレットを含む)

- 現金

- その他の決済方法

- オンライン販売

- カード決済(デビットカード、クレジットカード、銀行融資プリペイドカードを含む)

- デジタルウォレット(モバイルウォレットを含む)

- その他(代金引換、銀行振込、Buy Now, Pay Laterを含む)

- 販売時点

- エンドユーザー産業別

- 小売

- エンターテインメント

- 医療

- ホスピタリティ

- その他

第7章 競合情勢

- 企業プロファイル

- Mer Pay Co. Ltd(MerPay)

- Mitsubishi UFJ Financial Group

- Resona Holdings

- KDDI Corporation(AuPay)

- Japan Post Bank Co. Ltd.

- Rakuten Group Inc.

- NTT Docomo(D-Barai)

- PayPay Corporation

- Resona Holdings

- LINE Pay Corporation

- Sumitomo Mitsui Financial Group

- Mizuho Group

第8章 投資分析

第9章 市場の将来展望

目次

The Japan Payments Market size is estimated at USD 0.28 trillion in 2025, and is expected to reach USD 1.07 trillion by 2030, at a CAGR of greater than 31.04% during the forecast period (2025-2030).

Over time, payments have evolved from bartering to token systems (exchanging coins and paper money), currency pooling (deposits and bank accounts), and ultimately cashless transactions. Over the past decade, a significant acceleration in modern payment systems has been witnessed in Japan, among the primary factors influencing the growth of the studied market in Japan.

Key Highlights

- Although one of the leading payment methods in the nation is cash, digital transactions are developing quickly, transforming the country into a digital one. Establishing the necessary infrastructure by the Japanese government also aids in ensuring the efficient operation of the payments market.

- The third generation of online technology, Web 3.0, combines structured data and cognitive services to enable the web to understand and accomplish user objectives. Payments may use Web 3.0 to offer users more intelligent and individualized payment experiences. By using natural language processing (NLP) and voice commands, consumers can tell their devices what and how much they wish to pay using Web 3.0 technologies, for instance. Based on a user's past payment history and preferences, Web 3.0 technology can also offer customized payment recommendations and offers. Such technologies are also anticipated to evolve and influence the Japanese payments market during the forecast period.

- Due to their simplicity in enabling online bill payments and other money transfer services, mobile wallets are becoming extremely popular for e-commerce businesses all over Japan. Additionally, the usage of these modern instruments enables quick and secure transactions. These advantages of utilizing a mobile wallet have led to increased use of these products. This factor is anticipated to generate lucrative opportunities in the studied market during the forecast period. Customers of mobile wallets can transfer and receive money with ease due to the user-friendly UI. Users of smartphones can finish their transactions even while on the go due to the user-friendly UI.

- On the flip side, card fraud occurs when thieves use card holder's financial or credit card information to gain unauthorized entry to user accounts and take money. The substantial increase in the number of users who have fallen victim to fraud is caused by the fact that most people's everyday and professional lives are currently virtual or online, as well as the growing complexity of hackers and organized crime groups that target Japan online. Such factors are likely to restrain the growth of the studied market.

- COVID-19 notably impacted the Japanese payments market, with companies like Japan Post Bank intensifying their rivalry with PayPal. The market players are striving towards continued digitalization and innovation in the payments industry to mitigate the effects of the pandemic. Hence, the post-pandemic period is anticipated to witness a continued evolution of the payments industry in Japan.

Japan Payments Market Trends

Online Sales Mode of Payment Segment is Expected to Significant Market Share

- Due to their simplicity in enabling online bill payments and other money transfer services, mobile wallets are becoming extremely popular all over Japan for E-commerce businesses. Additionally, the usage of these modern instruments enables quick and secure transactions. These advantages of utilizing a mobile wallet have led to increased use of these products. During the forecast period, the online payment facility is anticipated to create lucrative opportunities in the studied market.

- Alternative digital currencies are already quickly being embraced in the region, with cryptocurrencies being the most in demand. Future digital wallets offer on-demand and frictionless access to these alternative digital assets and store and enable payment transactions. Furthermore, they make it possible to carry out financial transactions using various payment sources.

- Similarly, the buy now, pay later (BNPL) firm in Japan, Paidy, offers Paidy Link that instantaneously links account holders to their digital wallets. Paidy employs its models and machine learning to speed up transactions and ensure payment. JS Capital Management, Soros Capital Management, Tybourne Capital Management, and Wellington Management contributed to the company's recent USD 120 million Series D fundraising round.

- According to the Bank of Japan, Credit cards were the most used cashless means of payment in Japan, according to a survey conducted from August to September 2023. Around 68.4 percent of the respondents stated that they used credit cards in their daily lives, while 8.1 percent only used cash. Moreover, a quick and easy payment process was the leading reason for consumers in Japan to use cashless payment methods. Over 67 percent of respondents said they used digital payment methods to make payments quickly and easily. Further, according to the Japan Consumer Credit Association, In 2023, the number of credit cards issued in Japan reached 308.6 million. The number increased by 2.5 percent from over 301 million cards in the previous year.

- The rise in spending on online shopping would create an opportunity for the market players to develop new real-time payment solutions to capture the market share. In January 2023, Japanese fintech Smartpay launched Smartpay Bank Direct, the country's first digital payments service that offers installments directly from users' bank accounts. Through the new service, Smartpay claims it is Japan's first digital consumer finance company to utilize Japan's open banking system, with a network of 67 partner banks across Japan. The digital payments service supports credit cards and direct debit through an automated, single-click user experience at the point of purchase, with no additional fees or interest for consumers.

The Retail End-user Industry Segment is Expected to Hold Significant Market Share

- The retail payments landscape in Japan has undergone a significant transformation in recent years due to changes in end-user payment habits, payment innovation, technical advancements, and the entrance of new providers. Japanese consumers are now using a variety of new, convenient payment options made possible in substantial part by mobile technology. One of the most significant retail payment trends is BNPL (buy now, pay later). Additionally, the new payments platform has enabled real-time payments utilizing PayIDs since eCommerce has grown to new levels throughout the epidemic. Many retailers in Japan accept BNPL as an essential form of payment, especially for internet sales in specific retail markets where BNPL adoption is high.

- Further, according to Appliv Topics, the growing Japanese e-commerce industry is spearheaded by the three large-scale online retailers Rakuten, Yahoo Japan, and Amazon, which generate sales exceeding YEN one trillion (USD 0.068 billion). The three market leaders expanded their monthly active user bases by offering a range of products and services outside of business-to-consumer (B2C) commerce, reaching more than 40 percent of online users with their brands. This includes Rakuten's internet banking services, Amazon's video distribution services, and Yahoo's auction platform.

- Moreover, According to a survey conducted by Appliv Topics and JustSystems in Japan in 2023, the most used e-commerce site among consumers was Amazon, with approximately 50 percent naming the Japanese platform as their primary online shopping channel. The online marketplace Rakuten Ichiba followed in second place, with around one in three online shoppers ordering over Rakuten's platform.

- Paying by link is a relatively new payment method highly effective for streamlining the checkout process. It is gaining momentum in Japan. It can penetrate all retail segments, whether online or in-store. It would allow a business to automatically produce and distribute payment links to clients via text, email, chat, and QR codes. Customers would be directed to a PCI-compliant hosted checkout page using these links, which use one-time-use URLs. They then would provide their payment details.

- According to Infcurion conducted the 2023 Consumer Payment Trend Survey covering 20,000 people aged 16-69 across the country. QR Code Payment App usage increased across all business sectors. 'Supermarkets and Grocers' (from 13% to 18%), Taxis (from 8% to 16%), and 'Japanese Pubs and Bars' (from 9% to 14%) experienced substantial increases.

Japan Payments Industry Overview

The Japan Payments Market is highly fragmented with the presence of major players like Mer Pay Co. Ltd (MerPay), Mitsubishi UFJ Financial Group, Resona Holdings, KDDI Corporation (AuPay), and Japan Post Bank Co. Ltd. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- November 2023 - Mitsubishi UFJ Financial Group (MUFG), one of Japan's largest financial services firms, has tapped Amazon Web Services (AWS) to accelerate its digital transformation. MUFG taps AWS for digital transformation As part of a multi-year agreement, MUFG will leverage AWS' cloud technologies to adopt generative artificial intelligence (AI) and machine learning capabilities, automate processes, and offer personalized financial services to meet customer needs.

- July 2023 - LINE's virtual Asset and blockchain-related business organization, and PayPay Corporation announced the launch of the "PayPay Linkage Service," which would allow users to use PayPay Money to buy virtual Asset and cash them into PayPay Money on crypto asset trading service "LINE BITMAX."

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness-Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Evolution of the payments landscape in the country

- 4.5 Key market trends pertaining to the growth of cashless transactions in the country

- 4.6 Impact of COVID-19 on the payments market in the country

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Adoption of Online Mode of Payments

- 5.1.2 Initiatives by the Government

- 5.2 Market Challenges

- 5.2.1 Data Privacy of the Consumers

- 5.3 Market Opportunities

- 5.3.1 Move towards Cashless Society

- 5.3.2 New Entrants to Drive Innovation Leading to Higher Adoption

- 5.4 Key Regulations and Standards in the Digital Payments Industry

- 5.5 Analysis of major case studies and use-cases

- 5.6 Analysis of key demographic trends and patterns related to payments industry in Japan (Coverage to include Population, Internet Penetration, Banking Penetration/Unbanking Population, Age & Income etc.)

- 5.7 Analysis of the increasing emphasis on customer satisfaction and convergence of global trends in Japan

- 5.8 Analysis of cash displacement and rise of contactless payment modes in Japan

6 MARKET SEGMENTATION

- 6.1 By Mode of Payment

- 6.1.1 Point of Sale

- 6.1.1.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.1.2 Digital Wallet (includes Mobile Wallets)

- 6.1.1.3 Cash

- 6.1.1.4 Other Modes of Payment

- 6.1.2 Online Sale

- 6.1.2.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.2.2 Digital Wallet (includes Mobile Wallets)

- 6.1.2.3 Others (includes Cash on Delivery, Bank Transfer, and Buy Now, Pay Later)

- 6.1.1 Point of Sale

- 6.2 By End-user Industry

- 6.2.1 Retail

- 6.2.2 Entertainment

- 6.2.3 Healthcare

- 6.2.4 Hospitality

- 6.2.5 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Mer Pay Co. Ltd (MerPay)

- 7.1.2 Mitsubishi UFJ Financial Group

- 7.1.3 Resona Holdings

- 7.1.4 KDDI Corporation (AuPay)

- 7.1.5 Japan Post Bank Co. Ltd.

- 7.1.6 Rakuten Group Inc.

- 7.1.7 NTT Docomo (D-Barai)

- 7.1.8 PayPay Corporation

- 7.1.9 Resona Holdings

- 7.1.10 LINE Pay Corporation

- 7.1.11 Sumitomo Mitsui Financial Group

- 7.1.12 Mizuho Group

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日