|

|

市場調査レポート

商品コード

1631643

シンガポールのeコマース-市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Singapore E-Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| シンガポールのeコマース-市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

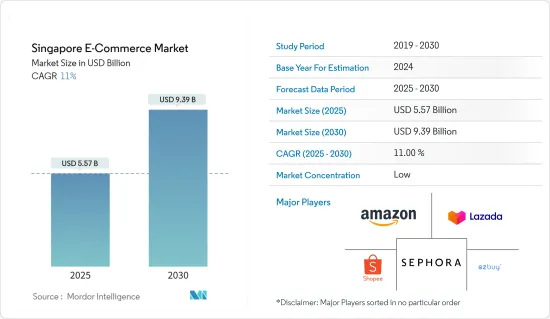

シンガポールのeコマース市場規模は2025年に55億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは11%で、2030年には93億9,000万米ドルに達すると予測されます。

主要ハイライト

- 技術の台頭はビジネスの領域に新時代を到来させ、シンガポールはこの変革を容易に歓迎しています。シンガポールにおけるeコマースの拡大は目覚ましく、顧客との接点をオンラインチャネルに求める企業が増えています。この地域のeコマースプラットフォームは、オンライン市場の管理を容易にすることで、企業がデジタル領域で繁栄するために重要な役割を果たしています。

- この地域のeコマース市場が急成長している背景には、モバイル決済の普及があります。デジタルウォレット、コードスキャン決済、モバイル決済などのオプションにより、ユーザーはモバイルデバイスで便利かつ安全に買い物をすることができます。シンガポールでモバイルウォレットの利用が増加していることは、モバイル決済が広く受け入れられていることを明確に示しています。また、同地域におけるインターネット接続の普及は、モバイル決済技術の採用を促進する上で重要な役割を果たしています。モバイル決済の普及が進むにつれ、同地域のeコマース市場は成長を遂げると考えられます。

- BNPL(Buy Now Pay Later)は、シンガポールのeコマース産業で普及しつつある決済方法です。BNPLを決済方法に取り入れることで、eコマース・ウェブサイトは幅広い消費者、特に若い層に対応することができます。これにより、消費者は購入した商品を前金で受け取り、状況に応じて分割払いすることができ、全体的な利便性とショッピング体験の満足度を高めることができます。BNPLの採用は、オンラインプラットフォームと実店舗の双方で増加しており、この地域におけるeコマース市場の拡大に向けた前向きな動向を示しています。

- 国際貿易管理局(ITA)によると、シンガポールのeコマース産業は、その広範で高速かつ信頼性の高いICTインフラ、技術に精通した国民性、デジタル経済を受け入れ、スマート国家を目指すという政府のコミットメントのおかげで、急速な成長を遂げています。シンガポール政府は、企業がビジネスを強化し成長させるためにITを活用することを積極的に奨励しています。同地域のeコマース産業を牽引する政府の取り組みが活発化していることも、市場拡大の大きな要因になると予想されます。

- さらに、ITAによると、シンガポールのeコマース市場の商品総額は2022年に82億米ドルに達し、2025年には110億米ドルに増加すると予測されています。ここ数年、コンピューターと通信機器がオンライン販売のかなりの部分を占めており、家具と家庭用機器も大きなシェアを確保しています。その他、ファッション、食品、化粧品・パーソナルケア、玩具などの主要製品カテゴリーも調査対象となりました。同地域のeコマースプラットフォームによる多額の投資も、市場の成長に大きな役割を果たしています。

- シンガポールのeコマース市場は、周辺諸国に比べて商品の品質と価格を重視しています。Temasek Holdingsの報告によると、シンガポールのeコマース市場の商品総量(GMV)は2023年に80億米ドルに達し、2025年には100億米ドルに達すると予測されています。シンガポールは、東南アジアで最も先進的なeコマース市場としての地位を固めています。

- ソーシャルのeコマースの台頭が重要性を増しています。ソーシャル・メディアを統合することで、ソーシャルのeコマースプラットフォームはソーシャルな側面とショッピングの側面を効果的に融合させ、進化する顧客のソーシャル・ショッピング需要に対応しています。技術の進歩や消費者行動の変化に伴い、eコマースはソーシャルメディア・プロモーションを通じて急速に拡大し、シンガポールのeコマース産業において徐々に重要な役割を果たすと予測されています。さらに、eコマース・ウェブサイトは、消費者のニーズの変化に対応し、技術の急速な進歩に対応するために、進化と革新を続けると考えられます。

- COVID-19の流行後、シンガポールのeコマース市場は大きな変貌を遂げました。消費者行動の変化は加速し、デジタルエンゲージメントは急増し、競争は激化しました。シンガポールのeコマースの将来的な展望は、オムニチャネル・アプローチ、ソーシャル・コマース、物流・配送サービスの進歩によって形作られると予想されます。政府の関与は、シンガポールのeコマース産業の軌跡を決定する上で極めて重要であると予想されます。

シンガポールのeコマース市場動向

インターネットが市場成長に重要な役割を果たす

- インターネットはeコマースの情勢を形成する上で重要な役割を果たし、伝統的市場を世界のプラットフォームに変えました。この進化により、企業は製品やサービスを世界中に販売できるようになり、取引や書類作成のプロセスがスムーズになりました。さらに、インターネットは、企業と消費者間のコミュニケーション、相互作用、取引の力学を世界規模で変革しました。インターネット利用の増加、モバイルインターネットユーザーの拡大、5G技術の採用推進への投資により、この地域のeコマース市場は大きな成長が見込まれています。

- シンガポールではインターネットとソーシャルメディアの利用が急速に増加しており、その結果、ユーザーが多様なコンテンツと交流し、動画ベースのソーシャルメディアプラットフォームにかなりの時間を割く活気あるオンラインコミュニティが形成されています。この動向は今後も続くと予想され、シンガポールはデジタルエンゲージメントのフロントランナーとして位置づけられています。インターネットとソーシャルメディアの急速な普及は、消費財のeコマースの顕著な拡大にも拍車をかけています。インターネットの利用が拡大するにつれ、オンラインショッピングやデジタルサービスの人気も高まり、結果的に市場の成長を後押しすると予想されます。

- 同地域では、ブロードバンドの高速化、オンライン決済の採用、5G技術の進歩に後押しされ、インターネット利用が急増しています。5Gはミリ波(mmWaves)を利用することで、特に人口密度の高い地域での大容量化、拡大性の向上、ユーザーのモビリティ(移動中の車内でも)の改善、全体的な接続性の強化を可能にしています。この強化されたモバイルブロードバンドにより、これまで困難だった条件下でも、より多くの人々が高品質のインターネットサービスにアクセスできるようになります。

- GO-Globeによると、5Gの導入とインテグレーションはシンガポールの接続性に革命をもたらし、イノベーション、生産性、経済成長の新時代をもたらすといわれています。5Gインフラへの継続的な投資と促進的な規制環境の確立により、シンガポールはデジタル経済の世界的リーダーとして台頭する好位置につけています。5Gの契約数は2025年までに4Gの契約数を上回り、2027年末にはモバイル契約数の76%を占めるようになると予測されており、この地域のeコマース市場にプラスの影響を与える可能性が高いです。

- GO-Globeが提供したデータによると、シンガポールの現在の携帯電話普及率は169.6%で、2024年2月時点の携帯電話契約数は131万件と推定されます。シンガポールでは2025年までに世界全体の接続数の55%が5Gになると予測されています。Singtel、StarHub、M1は、シンガポール全土で5Gネットワークの運用を担う主要プロバイダーです。シングテルはこの進歩の先頭に立ち、2022年7月までに単独でのカバー率95%以上を達成し、政府の2025年目標を3年上回った。こうした大幅な進歩とベンダーの活動の活発化は、市場の成長を大きく後押しすると予想されます。

- Nokiaは2023年2月、シンガポールのモバイルネットワーク事業者M1とスターハブが設立した合弁会社アンティナと、厳正な入札手続きを経て、現在の全国5Gネットワーク契約の10年延長を獲得したことを明らかにしました。この契約により、Nokiaは屋内外をカバーする5Gスタンドアロン(SA)ネットワークを構築するとともに、アンティナの3.5GHz帯周波数資産を利用して現行ネットワークを強化します。この協業により、企業と消費者の双方にとって5G接続が強化され、シンガポールのダイナミックな5Gエコシステムをサポートすることが期待されます。同地域での5G導入を推進するこうしたベンダーの活動は、eコマース市場の成長を促進すると期待されています。

市場成長を牽引する飲食品産業

- シンガポール統計局によると、シンガポールの飲食品サービスの国内総生産(GDP)は52億6,000万SGD(40億2,000万米ドル)程度で、過去数年から微増しました。この減少は、COVID-19の大流行による外食産業の不利な影響によるものです。

- シンガポール顧客満足度指数(CSISG)のデータによると、外食に対する顧客の嗜好は変わっていないが、安全管理制限の一定の調整に対する反応は今年動いたようです。意外なことに、レストランでの食事が減った分、テイクアウトが大幅に増えました。

- シンガポール統計局によると、2023年3月の飲食品サービス売上高は前年同月比4.7%増となり、2023年2月の0.7%減から反転しました。前月の2022年3月の飲食品サービス売上高は8.0%増(季節調整済み)でした。2023年のシンガポールの飲食品サービス産業の国内総生産(GDP)は約56億7,000万SGD(42億3,000万米ドル)に達し、前年の51億4,000万SGD(38億3,000万米ドル)から10.5%の伸びを示しました。COVID-19の大流行後、特にシンガポールが2022年にすべての食事制限を撤廃した後、産業は大きな改善を見せた。

- Value Championによると、シンガポールの主要な食事デリバリーアプリのレビューによると、GrabFoodは注文総額に対するデリバリー手数料の比率が最も高く、21%を記録しました。Foodpandaは9%で、最も低い平均手数料率を記録しました。手数料比率は、平均配達手数料総額を平均配達注文総額で割って求めました。

- 2023年4月、植物由来の食品ブランド、Wakao Foodsがシンガポールでデビューする予定でした。同ブランドは、バター・ジャックやバーベキュー・ジャックからホット&スパイシー・ソーセージまで、7種類の看板商品を投入する予定でした。コンチネンタルやジャック・シュプリーム・バーガー・パティを含むこれらの商品は、Everyday Vegan GrocerやHorecaといった著名な小売店で販売される予定です。さらに、消費者はShopee、Lazada、Amazon Singapore、Redmartなどの大手eコマースプラットフォームで若尾の製品を見つけることができます。

- この地域では、eコマースプラットフォームにおけるeコマース食品の安全基準を維持するための重要な取り組みも見られます。例えばシンガポールでは、eコマース・ウェブサイト、ソーシャル・メディアプラットフォーム、食品宅配サービスといったオンラインチャネルを通じた食品小売が一般的になりつつあります。シンガポール規格(SS)687:2022(食品eコマース・ガイドライン)が2023年1月13日に導入されました。この規格は、オンラインで販売される食品の品質と安全性を高めるために、食品eコマース産業に推奨されるプラクティスと不可欠な手順を概説しています。オンライン食品ベンダー、eコマースプラットフォーム、食品宅配会社は、この地域でこの基準を遵守することが推奨されます。

- コーヒーとスナックの店舗数の増加は、ファストフードとコーヒービジネスの成長の主要原動力のひとつです。スペシャルティコーヒーは、様々な種類のプレミアムコーヒーに対する嗜好の多様化により台頭し、市場の成長を牽引しています。米国農務省によると、シンガポールでは前年6月に60kg入りのコーヒーが10万袋消費されました。近年、カフェ、チェーンコーヒー店、スペシャルティコーヒーハウスの増加がコーヒー消費量の増加に寄与しています。

シンガポールのeコマース産業概要

シンガポールでは、顧客によるオンライン流通チャネルの普及に伴い、eコマース市場の競合が激化しています。市場は緩やかです。インターネット普及率の上昇がこれを後押ししています。さらに、LazadaやShopeeなどのブランドは、顧客のオンラインショッピング体験を向上させる顧客中心のサービスを提供することで、リーチを拡大しています。

- 2023年7月-Amazon Global Sellingは、中小企業が越境eコマースの成長見込みを活用できるよう支援することを目的に、シンガポールで初の越境eコマース・ブランドのローンチパッドを導入しました。Enterprise SingaporeとSingapore Business Federationの協力により新設された「Singapore Cross-border Brand Launchpad」は、シンガポールの中小企業100社以上を支援し、ブランドの立ち上げと拡大を図るとともに、今後24ヶ月以内に米国での輸出機会を獲得することを目的としています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 主要市場動向と小売業全体に占めるeコマースのシェア

- COVID-19がeコマース売上に与える影響

第5章 市場力学

- 市場促進要因

- 全国的なインターネット普及率の増加

- スマートフォンの普及拡大

- 市場課題

- データセキュリティ

- シンガポールのeコマース産業に関する主要な人口動向とパターンの分析(人口、インターネット普及率、eコマース普及率、年齢・所得などをカバー)

- シンガポールのeコマース産業における主要取引形態の分析(現金、カード、銀行振込、ウォレットなどの一般的な決済手段を網羅)

- シンガポールの越境eコマース産業の分析(越境の現在の市場規模と主要動向)

- アジアのeコマース産業におけるシンガポールの現在の位置づけ

第6章 市場セグメンテーション

- B2C eコマース別

- 2022~2029年の市場規模(GMV)

- 市場セグメンテーション:用途別

- 美容・パーソナルケア

- 民生用電子機器

- ファッション・アパレル

- 飲食品

- 家具と家庭

- その他の用途(玩具、DIY、メディアなど)

- B2B eコマース別

- 2022~2029年の市場規模(GMV)

第7章 競合情勢

- 企業プロファイル

- Lazada

- Shopee

- EZbuy

- Amazon.com Inc.

- Sephora

- E Bay

- Alibaba Group Holding Ltd

- Flipkart

- Carousell

- RedMart

第8章 投資分析

第9章 市場の将来展望

The Singapore E-Commerce Market size is estimated at USD 5.57 billion in 2025, and is expected to reach USD 9.39 billion by 2030, at a CAGR of 11% during the forecast period (2025-2030).

Key Highlights

- The rise of technology has ushered in a new age in the realm of business, and Singapore has readily welcomed this transformation. The expansion of e-commerce in Singapore has been extraordinary, as an increasing number of enterprises are shifting toward online channels to connect with their clientele. E-commerce platforms in the area are playing a vital role in enabling businesses to flourish in the digital sphere by facilitating the management of online marketplaces.

- The surge in the region's e-commerce market can be attributed to the growing popularity of mobile payment methods. With options like digital wallets, code-scanning payments, and mobile payments, users can conveniently and securely make purchases on their mobile devices. The rising use of mobile wallets in Singapore is a clear indication of the widespread acceptance of mobile payments. Additionally, the increasing internet connectivity in the region is playing a significant role in driving the adoption of mobile payment technologies. As mobile payments continue to gain traction, the e-commerce market in the region is poised for growth.

- Buy now pay later (BNPL) is a payment method that is gaining traction in the Singaporean e-commerce industry. By incorporating BNPL into their payment options, e-commerce websites can cater to a wider range of consumers, particularly the younger demographic. This allows consumers to receive their purchases upfront and make payments in installments based on their circumstances, enhancing the overall convenience and satisfaction of the shopping experience. The adoption of BNPL is increasing among both online platforms and brick-and-mortar stores, indicating a positive trend toward the expansion of the e-commerce market in the region.

- According to the International Trade of Administration (ITA), Singapore's e-commerce industry is experiencing rapid growth thanks to its widespread, high-speed, and reliable ICT infrastructure, as well as its tech-savvy population and the government's commitment to embracing the digital economy and achieving its goal of becoming a Smart Nation. The Government of Singapore is actively encouraging companies to utilize IT to enhance and grow their businesses. The growing government efforts to drive the e-commerce industry in the region are anticipated to be a major factor in the market's expansion.

- Moreover, according to the ITA, the gross merchandise volume of the Singaporean e-commerce market reached USD 8.2 billion in 2022, with forecasts suggesting an increase to USD 11 billion by 2025. Over the recent years, computer and telecommunications equipment have held a substantial portion of online sales, while furniture and household equipment have also secured a significant share. Other major product categories in the market studied include fashion, food, cosmetics and personal care, and toys. The substantial investments made by the e-commerce platforms in the region are also playing a significant role in the market's growth.

- The e-commerce market in Singapore places a greater emphasis on the quality and pricing of goods than its surrounding nations. Temasek Holdings reported that the gross merchandise volume (GMV) of the Singaporean e-commerce market reached USD 8 billion in 2023, with projections to hit USD 10 billion by 2025. Singapore has solidified its position as Southeast Asia's most advanced e-commerce market.

- The rise of social e-commerce is gaining more importance. By integrating social media, social e-commerce platforms have effectively merged the social aspect with the shopping aspect to cater to the evolving social and shopping demands of customers. With ongoing technological advancements and shifts in consumer behavior, e-commerce is projected to expand rapidly through social media promotions and play a progressively vital role in Singapore's e-commerce industry. Moreover, e-commerce websites will persist in evolving and innovating to meet the changing needs of consumers and keep up with the rapid advancements in technology.

- Following the COVID-19 pandemic, the Singaporean e-commerce market experienced a profound transformation. Changes in consumer behavior were accelerated, digital engagement surged, and competition intensified. The future landscape of e-commerce in Singapore is anticipated to be shaped by omni-channel approaches, social commerce, and advancements in logistics and delivery services. Government involvement is expected to be pivotal in determining the trajectory of Singapore's e-commerce industry.

Singapore E-Commerce Market Trends

Internet Plays a Significant Role in Market Growth

- The internet has played a crucial role in shaping the landscape of e-commerce, converting traditional markets into global platforms. This evolution has empowered businesses to market their products and services worldwide, facilitating smoother transactions and documentation processes. Additionally, the internet has transformed the dynamics of communication, interaction, and transactions between businesses and consumers on a global scale. With rising internet usage, expanding mobile internet user base, and investments in driving the adoption of 5G technology, the e-commerce market in the region is anticipated to witness significant growth.

- Singapore has seen a rapid increase in internet and social media usage, resulting in a vibrant online community where users interact with diverse content and dedicate a substantial amount of time to video-based social media platforms. This trend is projected to persist, positioning Singapore as a frontrunner in digital engagement. The surge in Internet and social media adoption has also fueled a notable expansion in e-commerce for consumer goods. As Internet usage continues to grow, the popularity of online shopping and digital services is anticipated to increase, consequently boosting market growth.

- The region is experiencing a surge in internet usage, propelled by rising broadband speeds, the adoption of online payments, and the advancements in 5G technology. 5G's utilization of millimeter waves (mmWaves) allows for increased capacity, especially in densely populated regions, heightened scalability, improved user mobility (even in moving vehicles), and enhanced connectivity across the board. This enhanced mobile broadband ensures that the broader public can access high-quality internet services, even in previously challenging conditions.

- As per GO-Globe, the adoption and integration of 5G is set to revolutionize connectivity in Singapore, bringing in a new era of innovation, productivity, and economic growth. With continued investment in 5G infrastructure and establishing a conducive regulatory environment, Singapore is well-positioned to emerge as a global leader in the digital economy. It is predicted that 5G subscriptions will surpass 4G subscriptions by 2025 and is expected to represent 76% of total mobile subscriptions by the end of 2027, which is likely to positively impact the e-commerce market in the region.

- As per the data provided by GO-Globe, the current mobile penetration rate in Singapore stands at 169.6%, with an estimated 1.31 million mobile phone subscriptions as of February 2024. It is projected that 55% of total worldwide connections will be 5G in Singapore by 2025. Singtel, StarHub, and M1 are the key providers responsible for the operation of 5G networks across the nation. Singtel took the lead in this advancement, achieving over 95% standalone coverage by July 2022, surpassing the government's 2025 target by three years. These significant advancements and the increasing activities of vendors are expected to greatly boost the market's growth.

- Nokia revealed in February 2023 that it secured a ten-year extension to its current nationwide 5G network agreement with Antina, the joint venture established by mobile network operators M1 and StarHub in Singapore, after a rigorous tender process. This agreement entails Nokia setting up a 5G standalone (SA) network to provide indoor and outdoor coverage, along with enhancing the current network using Antina's 3.5 GHz spectrum assets. The collaboration is expected to enhance the 5G connectivity for both businesses and consumers, supporting Singapore's dynamic 5G ecosystem. Such vendor activities in driving the 5G adoption in the region are expected to drive the growth of the e-commerce market.

The Food and Beverage Industry is Driving Market Growth

- According to the Singapore Department of Statistics, the gross domestic product (GDP) of Singapore's food and beverage services was around SGD 5.26 billion (USD 4.02 billion), up slightly from the past years. The reduction is attributable to the foodservice industry's unfavorable impact of the COVID-19 pandemic.

- While customer preferences for dining in have stayed unchanged, the response to constant adjustments in safe management limits appears to have moved this year, according to data from the Customer Satisfaction Index of Singapore (CSISG). Surprisingly, the fall in dine-in numbers was met with a considerable increase in takeout, while delivery proportions remained steady.

- According to the Singapore Department of Statistics, food and beverage service sales increased by 4.7% year-over-year in March 2023, reversing a 0.7% dip in February 2023. Over the previous month, food and beverage service sales climbed 8.0%, seasonally adjusted in March 2022. In 2023, the food and beverage services industry in Singapore saw its gross domestic product (GDP) reach around SGD 5.67 billion (USD 4.23 billion), marking a 10.5% growth from the previous year's figure of SGD 5.14 billion (USD 3.83 billion). The industry has shown significant improvement following the COVID-19 pandemic, especially after Singapore removed all dining restrictions in 2022.

- According to Value Champion, GrabFood recorded the highest delivery fee ratio to the total order cost, at 21%, according to a review of leading meal delivery apps in Singapore. With a fee ratio of 9%, Foodpanda recorded the lowest average fee ratio. The fee ratio was obtained by dividing the average delivery fee total by the average total cost of the delivery order.

- In April 2023, Wakao Foods, a plant-based food brand, was set to debut in Singapore. The brand was expected to introduce seven of its signature products, ranging from Butter Jack and BBQ Jack to Hot & Spicy Sausages. These offerings, which include Continental and Jack Supreme Burger Patties, will be stocked at prominent retail outlets like Everyday Vegan Grocer and HoReCa. Additionally, consumers can find Wakao's products on leading e-commerce platforms, including Shopee, Lazada, Amazon Singapore, and Redmart.

- The region is also witnessing significant initiatives in maintaining safety standards for the e-commerce food products in the region's e-commerce platform. For instance, food retail through online channels like e-commerce websites, social media platforms, and food delivery services is becoming more common in Singapore. The Singapore Standard (SS) 687: 2022 (Guidelines for Food E-commerce) was introduced on January 13, 2023. This standard outlines recommended practices and essential procedures for the food e-commerce industry to enhance the quality and safety of food items sold online. It is recommended that online food vendors, e-commerce platforms, and food delivery firms adhere to this standard in the area.

- The increase in the number of coffee and snack outlets is one of the main drivers of the growth of the fast food and coffee business. Specialty coffees have emerged due to the diversity of tastes and preferences for various varieties of premium coffee, which is driving the market's growth. According to the US Department of Agriculture, Singapore consumed 100,000 60 kg bags of coffee in June before the previous year. In recent years, the increase in cafes, chain coffee shops, and specialty coffee houses has contributed to rising coffee consumption.

Singapore E-Commerce Industry Overview

In Singapore, competition in the e-commerce market has increased as the adoption of online sales channels by customers has grown. The market is moderate. An increase aids this growth in internet penetration. Furthermore, brands such as Lazada and Shopee are expanding their reach by providing customer-centric services that enhance customers' online shopping experience.

- July 2023 - Amazon Global Selling introduced its inaugural cross-border e-commerce brand launchpad in Singapore, aimed at assisting SMEs in tapping into growth prospects in cross-border e-commerce. The newly established "Singapore Cross-border Brand Launchpad" initiative, created in collaboration with Enterprise Singapore and the Singapore Business Federation, is set to aid more than 100 local Singapore MSMEs in launching and expanding their brands, as well as gaining access to export opportunities in the United States within the next 24 months.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness-Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Key Market Trends and Share of E-commerce of Total Retail Sector

- 4.4 Impact of COVID-19 on the E-commerce Sales

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Internet Penetration Across the Country

- 5.1.2 Increased Adoption of Smartphones

- 5.2 Market Challenges

- 5.2.1 Data Security

- 5.3 Analysis of Key Demographic Trends and Patterns Related to the E-commerce Industry in Singapore (Coverage to include Population, Internet Penetration, E-commerce Penetration, Age & Income, etc.)

- 5.4 Analysis of the Key Modes of Transaction in the E-commerce Industry in Singapore (coverage to include prevalent modes of payment such as cash, card, bank transfer, wallets, etc.)

- 5.5 Analysis of Cross-border E-commerce Industry in Singapore (Current Market Value of Cross-border and Key Trends)

- 5.6 Current Positioning of Singapore in the E-commerce Industry in Asia

6 Market Segmentation

- 6.1 By B2C E-commerce

- 6.1.1 Market Size (GMV) for the Period of 2022-2029

- 6.1.2 Market Segmentation - by Application

- 6.1.2.1 Beauty and Personal Care

- 6.1.2.2 Consumer Electronics

- 6.1.2.3 Fashion and Apparel

- 6.1.2.4 Food and Beverage

- 6.1.2.5 Furniture and Home

- 6.1.2.6 Other Applications (Toys, DIY, Media, etc.)

- 6.2 By B2B E-commerce

- 6.2.1 Market Size (GMV) for the Period of 2022-2029

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 Lazada

- 7.1.2 Shopee

- 7.1.3 EZbuy

- 7.1.4 Amazon.com Inc.

- 7.1.5 Sephora

- 7.1.6 E Bay

- 7.1.7 Alibaba Group Holding Ltd

- 7.1.8 Flipkart

- 7.1.9 Carousell

- 7.1.10 RedMart