|

市場調査レポート

商品コード

1851590

銀行業務におけるモノのインターネット:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Internet Of Things In Banking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 銀行業務におけるモノのインターネット:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

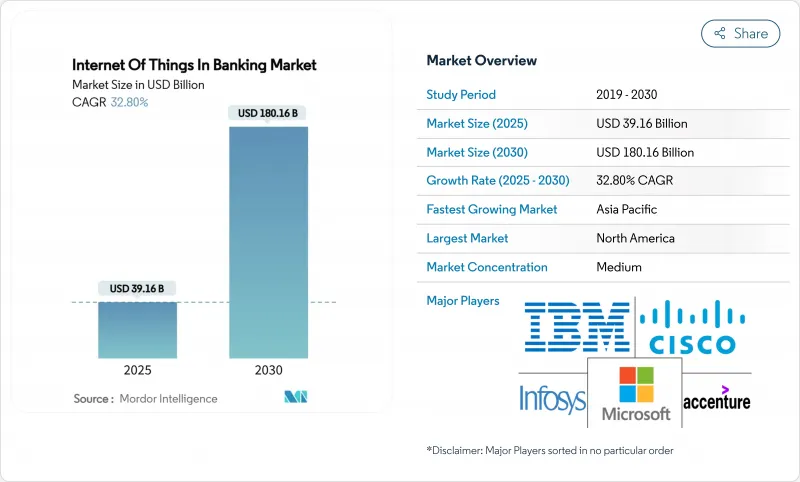

銀行業務におけるモノのインターネット市場は、2025年に391億6,000万米ドル、2030年には1,806億1,000万米ドルに達し、CAGR 32.8%で成長すると予測されています。

この成長ペースは、銀行がセンサーを多用したオペレーティング・モデル、リアルタイムのデータ・フロー、金融サービスと日常的なデバイス利用を結びつける組み込み型決済へとシフトしていることを反映しています。銀行はATMや支店、モバイル端末にコネクテッドセンサーを搭載し、現金業務の効率化、コンテキストを意識したオファーの開始、自動車やスマート家電からの決済の自動化を図っています。2026年4月発効の消費者金融保護局(CFTB)のオープンバンキング規制を筆頭に、規制強化の動きは、サードパーティの開発者がIoT信号と銀行データを融合できるようにするAPIの準備を加速させています。欧州では、PSD3や決済サービス規制案のもとで、強力な認証要件を拡大し、IoT対応取引のための安全なレールを構築することが並行して義務付けられています。半導体をめぐるサプライチェーンの制約や、5Gの展開のばらつきは依然としてデバイスの展開を抑制しているが、センサーのコスト低下やエッジコンピューティングの進歩は、銀行市場におけるモノのインターネットの持続的な拡大を10年を通じて示唆しています。

世界の銀行業務におけるモノのインターネット市場動向と洞察

オムニチャネル顧客体験の推進

銀行はATM、モバイルアプリ、ウェアラブルにセンサーを取り付け、物理的環境とデジタル環境をシームレスに行き来する旅を実現。NatWestは、5,500台のATMを19インチのタッチスクリーンとライブテレメトリーでアップグレードし、ダウンタイムが発生する前に警告を発しました。また、顧客が視線やジェスチャーを使って資金を移動できるよう、Apple Vision Pro向けのリテールバンキングアプリもリリースしました。このような統合により、金融機関は地理的位置情報、デバイスの健康状態、購入パターンをブレンドしてニーズを予測できるようになり、成熟したロールアウトではクロスセルの精度が3分の1に向上しました。センサー分析により、来店前の支店スタッフの配置、待ち行列の警告、顧客満足度を2桁上昇させる動的なパーソナライズされたオファーが可能になります。このため、銀行業務におけるモノのインターネット市場は、ユーザーの定着率の向上と運営コストの削減というメリットを享受しています。

リアルタイムの不正検知とセキュリティ

分散センサーは、ミリ秒単位で不審なパターンにフラグを立てるアノマリー・エンジンに供給されます。デバイスのテレメトリとトランザクション・ストリームを組み合わせた連合学習モデルは、プライバシー保護のためデータをローカルに保ちながら、96.3%の不正検知精度を達成しています。スマートカメラや環境センサーがATMや現金自動預け払い機を監視し、スキミング装置や改ざんのヒントとなる異常な温度上昇を検知します。エッジで適用されるブロックチェーンハッシュは、紛争解決のための不変のログを作成し、デバイス上のAIは、かつて顧客を悩ませた誤検出を減らします。早期導入企業では、導入初年度に20%以上の詐欺被害削減が報告されています。セキュリティの緊急性が継続的な投資を促し、銀行市場におけるモノのインターネットをサイバー犯罪に関連するためらいから強化しています。

データプライバシーとサイバーセキュリティへの懸念

EUのサイバーレジリエンス法は、メーカーに自動セキュリティアップデートを搭載したデバイスの出荷を義務付けており、無線パッチ適用を維持できないベンダーが露呈しています。銀行は、カリフォルニア州の消費者プライバシー法からインドのデジタル個人データ保護法まで、多様な規則を追跡しなければならず、コンプライアンス上のオーバーヘッドが増えます。セグメンテーションが脆弱であれば、単一のセンサーでの侵害が銀行のコアを弱体化させる可能性があります。Federated-learningの試験運用では、生データをエクスポートすることなく99.94%のモデル精度を示しているが、ほとんどの金融機関は、デバイス・フリートのセキュリティ確保において、依然としてスキルギャップに直面しています。サイバー保険料の高騰はプロジェクト・コストを上昇させ、銀行業務におけるモノのインターネット市場での採用を遅らせる可能性があります。

セグメント分析

2024年の売上高の58%はサービスであり、専門知識、規制に関する洞察力、24時間体制のサポートが複雑なロールアウトの成果を左右することが明らかになりました。サービスの銀行業務におけるモノのインターネット市場規模は、レガシーコアやクラウドファブリックにセンサーを組み込むインテグレーターの需要を反映して、CAGR 33.37%で拡大すると予測されています。銀行はリスク低減のため、脅威モデリング、コンプライアンス・マッピング、デバイス・ライフサイクル・ガバナンスをアウトソーシングすることが多いです。ソリューションはハードウェア・キット、ソフトウェア・プラットフォーム、コネクティビティ・バンドルに及び、金融機関がオンプレミスのデータセンターを廃止できるようなクラウド・ネイティブ・シフトの恩恵を受けています。IBM-WiproのAI対応プラットフォームなどの共同オファーは、アナリティクスとサイバー・ハードニングをバンドルしており、ソリューション・プロバイダー間の競争を激化させています。

第2世代の導入では、従量課金のマネージド・サービスが好まれ、中小銀行は設備投資のかさむ自社構築よりもターンキー・バンドルを採用するようになっています。ベンダーは、エッジ・コンピュート・ノードにオープン・バンキングAPI用の事前認証済みコネクタをパッケージ化し、価値実現までの時間を短縮しています。ハードウェアの利ざやは依然として薄いため、サプライヤーはデバイスの監視と予知保全を中心とした年金モデルに軸足を移しています。クラウドベンダーが金融グレードのエッジスタックをリリースするにつれて、銀行業務におけるモノのインターネット市場はサービス中心の経済性にさらに傾いています。

セキュリティ・アプリケーションは2024年の売上高の36.2%を占め、CAGRは34.73%で拡大。セキュリティの銀行業務におけるモノのインターネット市場規模は2025年に141億7,000万米ドルに達し、2030年には710億米ドルを超えると予測されています。スマートATMは、温度異常、衝撃イベント、改ざんパターンを検知し、ディスペンサーを自動的にロックすることができます。デバイスレベルの暗号化とルート・オブ・トラスト・チップは現在、プレミアム端末にデフォルトで搭載されており、コンプライアンス監査にかかる時間を短縮しています。

モニタリング、データ管理、カスタマー・エクスペリエンスの各モジュールはインフラを共有しているが、分析能力はさまざまです。銀行は遠隔測定を活用して支店のエネルギー使用を最適化し、電力コストを前年比で最大12%削減しています。カスタマー・エクスペリエンス・エンジンは、フット・トラフィック・センサーとCRMの履歴を結びつけ、支店内でパーソナライズされた挨拶を行う。同じセンサーグリッド上で複数のアプリケーションをホストする統合プラットフォームは、全体的なTCOを削減し、銀行市場におけるモノのインターネット全体の魅力を広げるのに役立ちます。

銀行業務におけるモノのインターネットの世界市場レポートは、コンポーネント別(ソリューションとサービス)、アプリケーション別(セキュリティ、モニタリング、その他)、組織規模別(大企業と中小企業)、エンドユーザー別(リテールバンキング、コーポレートバンキング、投資銀行、その他)、地域別に分類されています。

地域分析

北米が2024年の売上高の38.5%を占め首位を維持、堅調なサイバー法制とフィンテックと銀行の早期提携が後押し。センサー対応の支店では生産性が30~40%向上し、量子トライアルアルゴリズムは従来のオプティマイザーより1,000倍高速に動作します。カナダではコネクテッド・コミュニティATMによるキャッシュサークルインクルージョンが進み、メキシコでは取引手数料を削減するIoTベースの送金キオスクが活用されています。銀行業務におけるモノのインターネット市場では、連邦政府が5Gの未整備地域への拡大を支援し、大陸間の遅延格差が平らになっています。

アジア太平洋は成長エンジンであり、CAGR 33.86%で躍進しています。中国のAIBankは、IoTデータを取り込んで融資をパーソナライズするマイクロサービス・コアで1億人以上の顧客にサービスを提供しています。インドではエッジ・ミニデータセンターを展開し、光ファイバーがまばらな農村部にモバイルバンキングを拡大しています。東南アジアのスーパーアプリは、ライドヘイリング、フードデリバリー、インスタントクレジットを融合し、IoTセンサーがドライバーのパフォーマンスを追跡してダイナミックな保険価格設定を実現。地域の規制当局がサンドボックスの承認を急ピッチで進め、銀行業務におけるモノのインターネット市場がスマートフォンの普及率上昇を確実に捉えます。

欧州ではプライバシーとESGの進展が予測されます。PSD3とPSRは認証とAPIの調和を義務付け、デバイスの安全なオンボーディングを促進します。各機関はエネルギー監視センサーを統合してカーボンフットプリントを測定し、ネット・ゼロ・ロードマップへのコミットメントと整合させる。デバイスメーカーは省電力チップを組み込み、IoTの電力消費量に関する監視に対応します。ラテンアメリカや中東・アフリカの新興地域では、決済の近代化プログラムやモバイルマネー制度が、飛躍的な展開を可能にする土壌となっています。例えば、ブラジルのPIXやナイジェリアのeNairaレールでは、IoTエンドポイントがリアルタイムの支払いを開始できるようになり、銀行業務におけるモノのインターネット市場の収益源が多様化しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- オムニチャネル顧客体験の推進

- リアルタイムの不正検知とセキュリティ

- 規制上のオープンバンキング義務

- センサーによる支店/ATMコストの最適化

- IoTを活用した組み込み決済(自動車や家電製品)

- エッジ・アナリティクス主導の超パーソナライズド・マイクロレンディング

- 市場抑制要因

- データプライバシーとサイバーセキュリティへの懸念

- デバイス/プラットフォームの相互運用性のギャップ

- 地方の5G遅延ボトルネック

- IoTエネルギー消費に関するESG精査

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 主な使用事例とケーススタディ

- 融資引受のための原材料在庫追跡

- 柔軟な貸出条件のためのファーム・アウトプット分析

- IoTを活用したサイバー攻撃防止システム

- リテール・バンキング・情勢

- Beacon対応ATM事前発表(JPMチェース)

- 身体の不自由な顧客のための支店内ナビゲーション(バークレイズ)

- Beaconによる未利用店舗の再生(米国銀行とシティ)

第5章 市場規模と成長予測

- コンポーネント別

- ソリューション

- サービス

- 用途別

- セキュリティ

- モニタリング

- データ管理

- カスタマー・エクスペリエンス・マネジメント

- その他の用途

- 組織規模別

- 大企業

- 中小企業

- エンドユーザー別

- リテール・バンキング

- コーポレート・バンキング

- インベストメント・バンキング

- 非銀行金融会社

- 保険

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Oracle Corporation

- Accenture plc

- Temenos AG

- Infosys Limited

- Software AG

- Vodafone Group plc

- Tibbo Systems

- SAP SE

- Capgemini SE

- Intel Corporation

- Amazon Web Services

- FIS Global

- NCR Atleos

- Thales Group

- Diebold Nixdorf

- HPE(Aruba)

- Huawei Technologies